|

시장보고서

상품코드

2062278

mRNA 합성 서비스 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)MRNA Synthesis Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

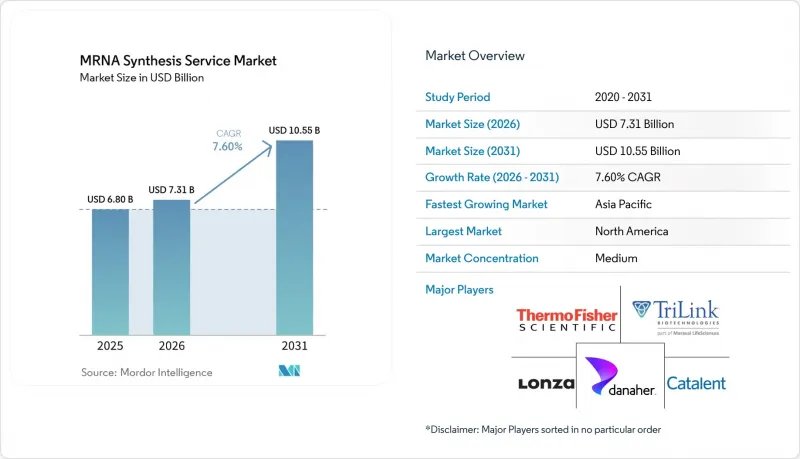

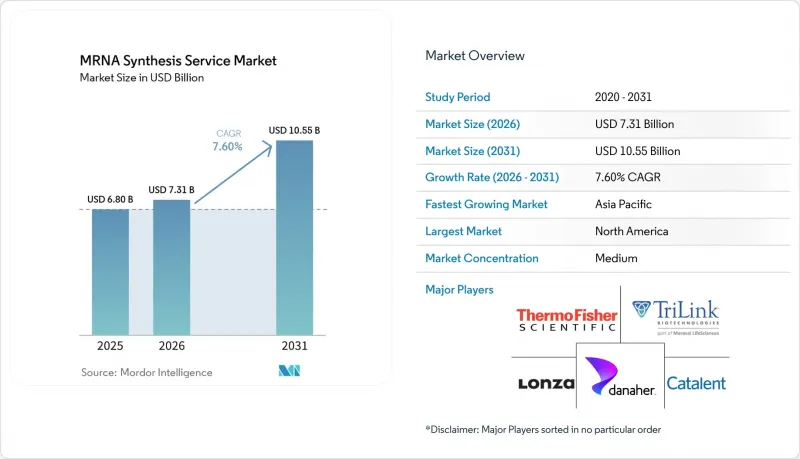

Mordor Intelligence에 의하면, mRNA 합성 서비스 시장 규모는 2025년 68억 달러에서 2026년에는 73억 1,000만 달러로 확대되어 2031년까지 105억 5,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 7.60%로 성장할 전망입니다.

본 보고서는 서비스 유형(맞춤형 mRNA 합성, GMP 등급 제조 등), 규모(연구용 등급, 전임상용 등급 등), 용도(백신, 항암제 등), 최종 사용자(생명공학 기업 및 제약 회사 등), 지역(북미, 유럽, 아시아태평양 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 mRNA 합성 서비스 시장 동향 및 인사이트

COVID-19 이후 백신 파이프라인의 확대가 치료 분야의 다각화를 주도하고 있습니다.

뉴클레오시드 변형형 COVID-19 백신의 입증된 성공에 힘입어, 현재 승인을 향해 진행 중인 종양학, RSV 및 희귀질환 프로그램이 주목을 받고 있습니다. 모더나는 맞춤형 암 백신, RSV 예방약, 그리고 인플루엔자와 COVID-19 혼합 백신을 포함해 최대 10개의 후기 단계 후보 물질을 개발하고 있습니다. 펨브롤리주맙과의 병용 요법에서 mRNA-4157이 보여준 긍정적인 결과는 악성 흑색종의 재발을 44% 감소시켰으며, 이는 면역종양학 분야에서 이 플랫폼의 유효성을 입증했습니다. 이에 대응하여 각 CDMO 기업은 고활성 및 맞춤형 배치 전용 생산 라인을 구축하여 대응하고 있습니다. TriLink BioTechnologies는 최근 후기 단계의 원료의약품 생산을 위한 대규모 cGMP 생산 라인을 구축했습니다.

아웃소싱 붐이 CDMO 경쟁 구도를 변화시키고 있습니다.

생물학적 복잡성과 자본 집약도가 높아지는 가운데, 대형 제약사들은 사내 생산 능력을 축소하고 있습니다. 화이자의 다년간에 걸친 프로그램은 제조 비용을 15억 달러 절감하는 것을 목표로 하고 있으며, 외부 전문가들과 협력하여 절감된 자금을 임상 자산에 재분배하고 있습니다. 최근의 거래들, 애질런트(Agilent)의 BIOVECTRA 9억 2,500만 달러 인수와 마라바이 생명과학(Maravai LifeSciences)의 Officinae Bio 핵산 사업부 인수는 엔드투엔드 mRNA 역량을 둘러싼 업계 재편을 여실히 보여주고 있습니다.

GMP 준수 및 검증의 병목 현상이 규모 확대를 제약하고 있습니다.

ATMP에 관한 EMA의 개정 지침 및 mRNA 백신에 관한 새로운 USP 장에 따라 출하 기준이 강화되었으며, 차세대 시퀀싱 및 직교 순도 시험과 같은 고도화된 분석이 의무화되었습니다. FDA의 ‘첨단 제조 기술 프레임워크’에 따라, 새로운 공정에 대한 상세한 문서화가 요구되게 되었습니다. 각 CDMO 기업들은 자동화된 품질 관리 시스템과 디지털 배치 기록에 대한 투자를 확대하고 있으며, 모더나(Moderna)는 공정 검증의 효율화를 통해 연구개발비용을 11억 달러 절감했습니다.

부문별 분석

2025년에도 GMP 등급 제품의 생산 비중이 46.4%로 가장 높은 점유율을 유지했습니다. 이는 확립된 인프라와 규제 당국이 검증된 플랫폼을 선호하는 경향을 반영한 것입니다. 한편, 맞춤형 암 백신 및 희귀질환 치료제에 대한 수요에 힘입어 맞춤형 합성 시장은 연평균 성장률(CAGR) 9.1%로 성장하고 있습니다. 각 CDMO 기업은 AI 도구를 도입하여 시퀀싱 설계의 신속한 반복 작업을 수행함으로써, 고객이 설계부터 IND 신청까지 6개월 이내에 진행할 수 있도록 지원하고 있습니다. 배열 설계, IVT, LNP 제제, 방출 시험을 통합적으로 제공하는 AmplifyBio와 RNAV8의 제휴 사례에서 볼 수 있듯이, 설계 최적화 및 분석 제품군은 현재 표준이 되었습니다. 성과 기반 모델이 보급됨에 따라, 맞춤형 프로젝트를 위한 mRNA 합성 서비스 시장 규모는 확대될 것으로 예측됩니다. TriLink사의 CleanCap이나 Aldevron사의 고순도 플라스미드와 같은 지적 재산상의 우위는 견고한 경쟁 우위를 창출하여 프리미엄 가격 책정을 가능하게 하고 있습니다.

서비스 메뉴의 확충은 mRNA 합성 서비스 시장 전체의 성숙도를 반영하고 있습니다. 원료 공급 계약을 통해 효소와 뉴클레오티드의 안정적인 공급이 확보되는 한편, 하이브리드 요금 체계(설비 예약료와 배치별 요금)는 CDMO가 거시경제의 변동 위험을 상쇄하는 데 도움이 되고 있습니다. 고객들이 신속한 승인 절차를 추구하는 가운데, 공급업체들은 규제 관련 컨설팅 및 동반 진단제 개발을 통합하여 스폰서의 업무 흐름에 더욱 깊이 통합되고 있습니다.

임상 GMP 배치는 매출의 38.9%를 차지하며, 주요 임상시험 및 조기 시판에 대응하고 있습니다. 그러나 모듈식 시설의 mRNA 합성 서비스 시장 점유율은 연평균 성장률(CAGR) 8.4%로 가장 빠르게 확대되고 있습니다. 컨테이너형 클린룸은 트럭 1대에 적재할 수 있으며, 토목 공사를 최소화할 수 있고, 50mg 규모의 전임상시험용 로트에서 수 Kg 규모의 상업용 로트로의 전환을 며칠 만에 완료할 수 있습니다. BioNTech사의 추산에 따르면, 2유닛 규모의 BioNTainer는 연간 5,000만 회분을 생산할 수 있으며, 기존 생산 시설에 비해 설비 투자(CAPEX)를 70% 절감할 수 있습니다. 더 소규모의 적응증에 대해서는 연속류 방식의 마이크로 리액터가 주문에 따라 로트를 생산하여 재고 비용을 절감합니다.

기존의 상업용 제조 시설에서는 여러 제품을 취급하는 방향으로 통합이 진행되고 있습니다. 론자가 로슈의 바카빌 공장을 인수함에 따라 33만 리터의 포유류 세포 배양 능력이 추가되었으며, 현재는 mRNA LNP의 최종 공정을 위해 일부 개조되고 있습니다. 이는 파이프라인의 불확실성을 보완하기 위한 자산 재활용의 한 예입니다. 하이브리드 모델(중앙에서 벌크 RNA를 생산한 후 지역에서 충전 및 마무리 작업을 수행하는 방식)은 공급망 차질에 대한 회복력을 높입니다.

지역별 분석

2025년에는 풍부한 인재, 견고한 지적재산권 보호, 그리고 적극적인 민관 자금 지원을 바탕으로 북미가 매출의 42.4%를 차지했습니다. 2025년 가동을 시작할 예정인 모데나의 3개 공장(캐나다, 영국, 호주)은 각각 연간 최대 1억 회분을 생산하며, 핵심 공정은 미국에 남겨두는 한편, 지역 간 공급망을 강화할 것입니다. 미국 생의학선진연구개발국(BARDA)은 수요가 급증할 때 생산 능력을 확보하기 위한 다년 계약인 ‘웜베이스’ 계약을 계속해서 체결하고 있습니다.

유럽은 일관된 규제 체계와 전략적인 생산 거점의 혜택을 누리고 있습니다. 독일의 바커(Wacker)사가 1억 200만 달러를 투자해 건설한 컴피턴스 센터에는 4개의 RNA 생산 라인이 추가되었으며, 그 중 절반은 연방 정부의 팬데믹 비축용으로 확보되어 있습니다. 유럽약전(European Pharmacopoeia)의 mRNA 품질에 관한 새로운 일반 장은 회원국 전체에서 로트 출하를 효율화하기 위한 기준을 규정하고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 6.4%로 가장 빠르게 성장하고 있는 지역입니다. 중국의 WuXi Biologics와 GenScript의 사업 확장, 한국 내 모더나(Moderna)와의 제휴, 그리고 BioNTech의 아세안(ASEAN) 본부로서 싱가포르가 맡은 역할은 각국이 추진하는 협력적인 국가 전략을 여실히 보여주고 있습니다. 호주의 오로라 바이오신세틱스는 연방 정부로부터 2억 달러의 지원을 활용해, 플라스미드부터 충전 및 완제품 생산에 이르는 종단간 GMP 체계를 구축하는 것을 목표로 하고 있습니다. 대만 바이오매뉴팩처링사는 바이오의약품 분야에서 반도체 파운드리 모델을 재현하는 것을 목표로 하고 있으며, 이는 해당 지역의 장기적인 포부를 보여줍니다.

중동 및 아프리카에서는 인프라 격차를 해소하기 위해 모듈식 시스템이 활용되고 있습니다. 사우디아라비아에서 HT-Bio가 KeyPlants POD를 도입한 것은 초기 도입 사례라고 할 수 있습니다. 남미에서는 브라질 및 아르헨티나와의 기술 이전 협정을 통해 확대가 진행되고 있으며, 이 지역의 백신 자급률이 향상되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the mRNA synthesis service market size is expected to increase from USD 6.80 billion in 2025 to USD 7.31 billion in 2026 and reach USD 10.55 billion by 2031, growing at a CAGR of 7.60% over 2026-2031.

This report is Segmented by Service Type (Custom MRNA Synthesis, GMP-Grade Manufacturing, and More), Scale (Research Grade, Pre-Clinical Grade, and More), Application (Vaccines, Oncology Therapeutics, and More), End-User (Biotechnology and Pharmaceutical Companies, and More), and Geography (North America, Europe, Asia Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global MRNA Synthesis Service Market Trends and Insights

Post-COVID Vaccine Pipeline Expansion Drives Therapeutic Diversification

The proven success of nucleoside-modified COVID-19 vaccines turns the spotlight on oncology, RSV, and rare-disease programs now advancing toward approval. Moderna is running as many as 10 late-stage candidates, including personalized cancer vaccines, RSV prophylactics, and a combined influenza/COVID-19 shot. Positive data on mRNA-4157 with pembrolizumab showed a 44% reduction in melanoma recurrence, validating the platform for immuno-oncology. CDMOs answer by installing dedicated suites for high-potency and personalized batches; TriLink BioTechnologies recently opened a large-scale cGMP line for late-phase drug-substance production.

Outsourcing Boom Transforms CDMO Competitive Dynamics

Big pharma is scaling back internal capacity as biological complexity and capital intensity soar. Pfizer's multi-year program targets USD 1.5 billion in manufacturing savings, reallocating funds to clinical assets while partnering with external experts. Recent deals-Agilent acquiring BIOVECTRA for USD 925 million and Maravai LifeSciences purchasing Officinae Bio's nucleic-acid unit-illustrate consolidation around end-to-end mRNA capabilities.

GMP Compliance and Validation Bottlenecks Constrain Scale-Up

Revised EMA guidelines for ATMPs and new USP chapters on mRNA vaccines tighten release criteria, mandating advanced analytics such as next-generation sequencing and orthogonal purity assays. The FDA's Advanced Manufacturing Technologies Framework now requires extensive documentation for novel processes. CDMOs invest in automated quality systems and digital batch records; Moderna cut R&D spend by USD 1.1 billion through process-validation efficiencies.

Other drivers and restraints analyzed in the detailed report include:

- High-Efficiency IVT and Capping Innovations Reduce Manufacturing Bottlenecks

- Venture and Government Funding Influx Accelerates Capacity Expansion

- Supply-Chain Crunch for High-Purity Reagents Creates Cost Pressures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

GMP-grade manufacturing retained the largest share at 46.4% in 2025, reflecting its entrenched infrastructure and regulators' preference for validated platforms. At the same time, custom synthesis is advancing at a 9.1% CAGR, fueled by demand for individualized cancer vaccines and rare-disease therapies. CDMOs embed AI tools to rapidly iterate sequence constructs, enabling clients to progress from design to IND in under six months. Design-optimization and analytical suites are now standard, as illustrated by the AmplifyBio-RNAV8 collaboration that bundles sequence design, IVT, LNP formulation, and release testing under one roof. The mRNA synthesis services market size for bespoke projects is expected to grow as pay-for-performance models become more prevalent. Intellectual property advantages-such as TriLink's CleanCap and Aldevron's high-fidelity plasmids-create durable moats and enable premium pricing.

The widening of service menus mirrors the overall maturation of the mRNA synthesis services market. Raw-material supply agreements safeguard enzyme and nucleotide availability, while hybrid fee structures (capacity reservation plus per-batch charges) help CDMOs offset macroeconomic volatility. As clients aim for accelerated approval pathways, providers integrate regulatory-affairs consulting and companion-diagnostics development, further embedding themselves in sponsor workflows.

Clinical GMP batches account for 38.9% of revenue, covering pivotal trials and early launches. The mRNA synthesis services market share for modular facilities, however, is expanding quickest at an 8.4% CAGR. Containerized cleanrooms can be fitted onto a single truck, require minimal civil works, and can transition between 50 mg preclinical runs and multi-kilogram commercial lots within days. BioNTech estimates that a two-unit BioNTainer can deliver 50 million doses annually, with 70% lower capital expenditure (capex) than a traditional plant. For more minor indications, continuous-flow micro-reactors produce on-demand lots, reducing inventory costs.

Legacy commercial-scale suites are consolidating around the use of multiple products. Lonza's acquisition of Roche's Vacaville plant added 330,000 L mammalian capacity, now partially retrofitted for mRNA LNP finishing, exemplifying asset repurposing to balance pipeline uncertainty. Hybrid models-central bulk RNA followed by regional fill-finish-enhance resilience to supply-chain shocks.

Geography Analysis

North America controlled 42.4% of revenue in 2025, anchored by a deep talent pool, robust IP protection, and aggressive public-private funding. Three Moderna plants set to go live in 2025-Canada, the U.K., and Australia-will each turn out up to 100 million doses annually, reinforcing cross-regional supply chains while retaining critical steps in the U.S.. The U.S. Biomedical Advanced Research and Development Authority (BARDA) continues to issue multi-year "warm-base" contracts guaranteeing surge capacity.

Europe benefits from cohesive regulatory frameworks and strategic manufacturing hubs. Wacker's USD 102 million competence center in Germany adds four RNA lines, half reserved for federal pandemic stockpiles. The European Pharmacopoeia's new general chapter on mRNA quality sets reference standards that streamline batch release across member states.

Asia-Pacific is the fastest-growing region at a 6.4% CAGR. China's WuXi Biologics and GenScript expansions, South Korea's Moderna partnership, and Singapore's role as BioNTech's ASEAN headquarters illustrate concerted sovereign strategies. Australia's Aurora Biosynthetics targets end-to-end GMP from plasmid to fill-finish, leveraging USD 200 million in federal backing. Taiwan Bio-Manufacturing Corp aims to replicate the semiconductor foundry model for biopharma, signaling long-term regional ambition.

Middle East & Africa tap into modular systems to bridge infrastructure gaps. HT-Bio's deployment of KeyPlants PODs in Saudi Arabia marks early adoption. South America expands through tech-transfer agreements in Brazil and Argentina, improving regional vaccine autonomy.

- TriLink BioTechnologies

- Aldevron (Danaher)

- Thermo Fisher Scientific (Patheon)

- Lonza Group

- Catalent

- Samsung Group

- AGC Biologics

- Wuxi Biologics

- Moderna

- BioNTech

- CureVac

- New England Biolabs

- Genscript

- Creative Biolabs

- BOC RNA (BOC Sciences)

- Cellerna Bioscience

- eTheRNA Manufacturing

- Kactus Biosystems

- Acuitas Therapeutics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Post-COVID Vaccine Pipeline Expansion

- 4.2.2 Outsourcing Boom To mRNA-Focused CDMOs

- 4.2.3 High-Efficiency IVT & Capping Innovations

- 4.2.4 Venture & Government Funding Influx

- 4.2.5 Modular 'mRNA-Printer' Micro-Factories

- 4.2.6 AI-Guided Sequence Optimisation & Cost Drops

- 4.3 Market Restraints

- 4.3.1 GMP Compliance & Validation Bottlenecks

- 4.3.2 Supply-Chain Crunch For High-Purity Reagents

- 4.3.3 Vaccine-Safety Perception Headwinds

- 4.3.4 Environmental Burden Of Enzymatic Reagents

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Service Type

- 5.1.1 Custom mRNA Synthesis

- 5.1.2 GMP-grade Manufacturing

- 5.1.3 Raw-Material & Enzyme Supply

- 5.1.4 Design & Optimisation Services

- 5.1.5 Analytical & QC Services

- 5.2 By Scale

- 5.2.1 Research Grade (RUO)

- 5.2.2 Pre-clinical Grade

- 5.2.3 Clinical GMP (Phase I-III)

- 5.2.4 Commercial GMP

- 5.2.5 On-Site Modular Production

- 5.3 By Application

- 5.3.1 Vaccines

- 5.3.2 Oncology Therapeutics

- 5.3.3 Rare-Disease / Protein-Replacement

- 5.3.4 Gene-Editing / CRISPR

- 5.3.5 Other Therapeutics

- 5.4 By End-User

- 5.4.1 Biotechnology Companies

- 5.4.2 Pharmaceutical Companies

- 5.4.3 CDMOs & CROs

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 TriLink BioTechnologies

- 6.3.2 Aldevron (Danaher)

- 6.3.3 Thermo Fisher Scientific (Patheon)

- 6.3.4 Lonza

- 6.3.5 Catalent

- 6.3.6 Samsung Biologics

- 6.3.7 AGC Biologics

- 6.3.8 WuXi Biologics

- 6.3.9 Moderna

- 6.3.10 BioNTech

- 6.3.11 CureVac

- 6.3.12 New England Biolabs

- 6.3.13 GenScript

- 6.3.14 Creative Biolabs

- 6.3.15 BOC RNA (BOC Sciences)

- 6.3.16 Cellerna Bioscience

- 6.3.17 eTheRNA Manufacturing

- 6.3.18 Kactus Biosystems

- 6.3.19 Acuitas Therapeutics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment