|

시장보고서

상품코드

2062290

비닐 아세테이트 단일중합체 에멀젼 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Vinyl Acetate Homopolymer Emulsion - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

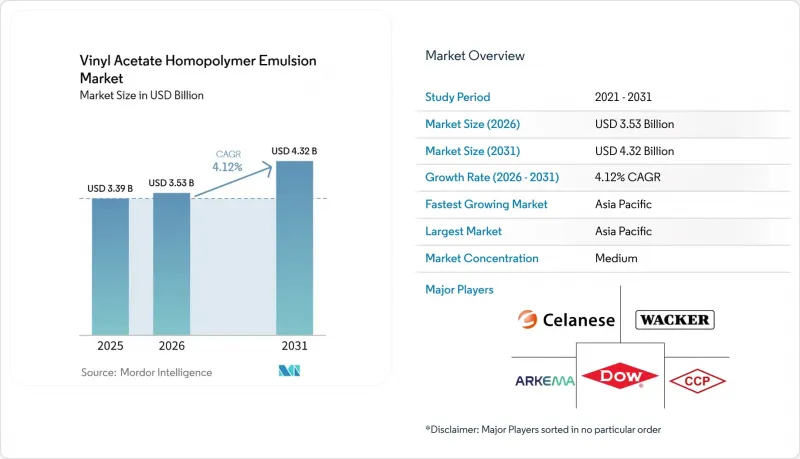

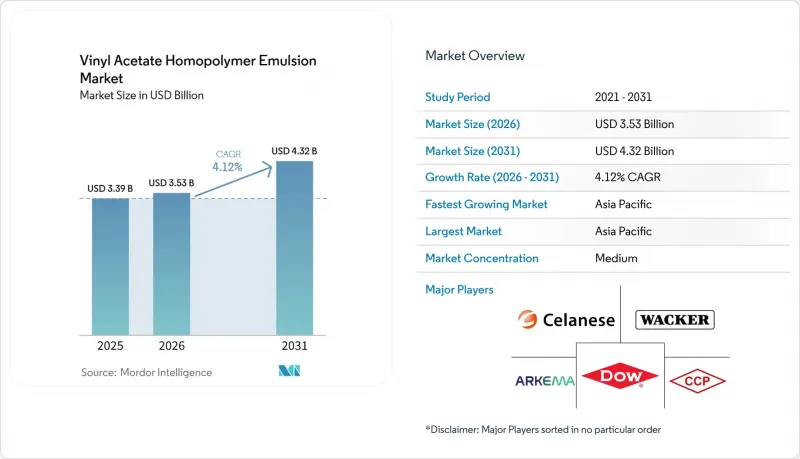

비닐 아세테이트 단일중합체 에멀젼 시장 규모는 2025년 33억 9,000만 달러로 평가되었습니다. 2026년 35억 3,000만 달러에서 2031년까지 43억 2,000만 달러로 확대되고 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 4.12%를 나타낼 것으로 예측됩니다.

본 보고서는 용도(페인트 및 코팅, 접착제 등), 최종 사용자 산업(건축 및 건설, 포장, 자동차 및 운송, 기타 최종 사용자 산업) 및 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 비닐 아세테이트 단일중합체 에멀젼 시장 동향 및 분석

저VOC 도료 및 코팅에 대한 규제 동향

2026년 6월 1일, 중국은 GB 30981.1-2025 및 GB 30981.2-2025 규정을 시행하여 포름알데히드, 중금속, 방향족 화합물 및 휘발성 유기 화합물(VOC)에 대한 제한을 강화했습니다. 동시에, GB 37824-2019에서는 기준 지역에서 특정 임계치를 초과하는 비메탄 탄화수소 배출량에 대해 상당한 수준의 감축 효율을 의무화하고 있습니다. 이러한 규제로 인해 배합 설계자들은 수성 시스템으로의 전환을 강요받고 있습니다. 이러한 점에서 비닐아세테이트 단일중합체 에멀젼은 고가의 열산화 장치를 필요로 하지 않으면서도 규정을 확실하게 준수할 수 있게 해줍니다. 유럽에서도 유사한 추세가 나타나고 있으며, 퍼플루오로알킬 물질 및 폴리플루오로알킬 물질에 대한 규제 확대와 휘발성 유기 화합물의 배출 기준 강화가 진행되고 있습니다. 한편, 미국에서는 환경보호청(EPA)이 정한 에어로졸 도료 규제의 적용 기한이 2027년 초로 설정되어 있습니다. 전 세계적으로 하류 사용자들은 방향족 화합물을 포함하지 않고 잔류 모노머가 최소한인 바인더를 선호하고 있습니다. 이러한 추세로 인해, 사전 인증을 완료하고 규정을 준수하는 등급의 제품을 공급하는 공급업체에게는 경쟁 우위가 생깁니다. 규제 강화로 인해 산업용 금속 및 플라스틱 코팅 분야에서 고고형분 용제 기반 시스템에서 벗어나는 추세가 가속화되고 있습니다. 이러한 전환에 따라 비닐아세테이트 호모폴리머 에멀션 시장이 확대되고 있습니다. 특히, 아시아태평양의 코팅 원료 제조업체 대다수가 현재 구매 결정 시 ‘수성 규제에 대한 준수’를 최우선으로 삼고 있어, 조달 선택에 미치는 정책의 영향이 뚜렷이 드러나고 있습니다.

아시아 및 유럽에서의 종이·티슈 생산 확대

도시화와 위생용품의 보급 확대에 따라 중국, 인도, 아세안(ASEAN) 국가들에서 티슈 제조 설비의 생산 능력이 대폭 확대되고 있습니다. 균일한 피막 형성 및 강력한 접착력으로 잘 알려진 비닐아세테이트 호모폴리머 에멀전은 고속 코팅기에 널리 사용되고 있으며, 스티렌·아크릴계 대체재와 비교해도 여전히 비용 효율성이 뛰어난 선택지입니다. 유럽에서는 제지 업체들이 그래픽 용지 생산 라인에서 재활용이 가능한 포장용지 등급으로 전환함에 따라, 맞춤형 유변학적 특성을 지닌 저취 바인더에 대한 수요가 급증하고 있습니다. 최근 출시된 제품들은 위생, 포장, 재활용성이라는 우선순위들이 조화를 이루고 있음을 여실히 보여주고 있습니다. 이러한 혁신을 통해 열에 민감한 스낵이나 과자류를 기존의 플라스틱 포장재에서 보다 지속 가능한 배리어 코팅 종이로 전환할 수 있게 됩니다. 일반적으로 이러한 배리어 코팅이 적용된 제품은 비닐 아세테이트 단일중합체 에멀젼에 의존하고 있습니다. 이러한 에멀전은 광물계 또는 나노셀룰로오스계 첨가제와 호환성이 좋을 뿐만 아니라, 수성 식품 모의액에 대해서도 내성을 나타내며, 용제계 시스템에 비해 배합의 유연성을 높여줍니다. 이를 통해 선순환이 만들어집니다. 펄프 생산 확대가 코팅 수요를 끌어올리면, 코팅 기술의 혁신이 종이와 연질 플라스틱 간의 경쟁을 더욱 촉진하게 됩니다.

VAM 원료 가격 변동

에틸렌과 아세트산으로 제조되는 비닐아세테이트 단량체의 비용은 분기마다 큰 변동을 보이는 원유나 천연가스 등 업스트림 부문의 벤치마크 가격과 밀접한 관련이 있습니다. 대만과 미국의 주요 비닐아세테이트 단량체 생산 공장이 가동을 중단함에 따라 현물 가격이 크게 상승했고, 예상치 못한 가동 중단에 대한 업계의 취약성이 여실히 드러났습니다. 수송 병목 현상과 관세 변경으로 인해 심화된 지역 간 가격 격차로 인해, 아시아의 에멀젼 제조업체들은 국내산 에틸렌과 수입 에틸렌 사이에서 줄타기 같은 대응을 강요받고 있습니다. 이러한 가격 변동은 고정가격 계약의 이익률을 떨어뜨릴 뿐만 아니라, 원가 가산 방식에 따른 가격 전가를 복잡하게 만들고 있으며, 이는 특히 중소 사료 제조업체들에게 뚜렷한 과제로 대두되고 있습니다. 셀레네즈나 와커와 같은 대기업들은 후방 통합된 비닐아세테이트 모노머 생산 능력과 에틸렌 공급망을 보유하고 있어 이러한 가격 변동의 영향을 어느 정도 피할 수 있지만, 그럼에도 연차 보고서에서 원자재 가격 변동이 수익에 있어 중대한 위험 요소임을 인정하고 있습니다. 이에 대응하여 조달 부서는 공급처 다각화를 추진하고, 장기 에틸렌 스왑 계약 확보에 힘쓰고 있으나, 이러한 헤지 거래에는 추가적인 간접비와 거래 상대방 리스크가 수반된다는 점을 인식하고 있습니다.

부문별 분석

페인트 및 코팅 분야는 총 매출에 크게 기여하여, 2025년 매출의 36.22%를 차지하며, 용도별 비닐 아세테이트 단일중합체 에멀젼 시장 점유율 1위 자리를 확고히 했습니다. 이 분야에서는 중국의 수성 시스템으로의 전환과 유럽의 VOC 규제 강화를 배경으로, 건축용 배합이 주류를 이루고 있습니다. 동 기간 동안, 코모노머 그래프트 처리를 거친 고성능 에멀전이 용제형 산업용도료 시장 점유율을 서서히 잠식하며, 용도 기반을 확대할 것으로 예측됩니다.

부직포의 용도는 비교적 좁은 시장 기반에서 시작될 것으로 예측됩니다. 2026년부터 2031년까지 연평균 성장률(CAGR) 4.22%로 증가할 것으로 예측됩니다. 위생용품 제조업체들은 저취성과 부드러움을 이유로 비닐아세테이트 호모폴리머 바인더를 점점 더 선호하고 있습니다. 특히, 동남아시아의 주요 기저귀 제조업체 중 다수가 현지에서 공급되는 등급을 승인하고 있습니다. 한편, 접착제 부문은 꾸준한 성장을 보이고 있습니다. 이는 주로 재활용이 가능한 단일 소재 포장재로 전환되고 있기 때문이며, 이에 따라 재밀봉 가능 시스템 및 콜드 씰 시스템에 대한 수요가 증가하고 있습니다. 이러한 시스템은 고점도 호모폴리머 분산액에 의존하고 있습니다. 섬유 및 기타 용도는 전체 가치에서 차지하는 비중은 작지만, 디지털 인쇄용 바인더나 특수 실런트에 있어 중요한 시험 무대가 되고 있습니다. 이러한 분야에서 성공을 거둔 혁신은 종종 대량 생산 부문으로 전환되어, 제품 파이프라인의 지속적인 흐름을 보장하고 있습니다.

지역별 분석

아시아태평양은 여전히 수요의 중심지이며, 2025년 매출의 46.67%를 차지했으며, 2026년부터 2031년까지 연평균 성장률(CAGR) 4.65%를 나타낼 전망입니다. 도료 생산량에서 중국이 차지하는 우위와 위생용품 생산이 급증하고 있는 인도의 상황이 맞물려 시장의 성장세를 이끌고 있습니다. 비닐아세테이트 단량체 및 비닐아세테이트-에틸렌 에멀젼의 대규모 생산 능력을 갖춘 세레네즈의 난징 복합 단지는 해당 지역의 막대한 수요를 충족시키기 위해 필수적인 현지 공급 전략의 모범 사례로 꼽히고 있습니다. 규제 동향, 특히 중국의 GB 30981 시리즈는 수성 제품으로의 전환을 확고히 하고 있습니다. 한편, 동남아시아국가연합(ASEAN) 지역의 위생용품 공장은 더욱 큰 호재가 되고 있습니다. 주택 공급량을 두 배로 늘리겠다는 인도의 야심 찬 목표는 건설 관련 도료 수요를 뒷받침하고 있습니다. 또한, 수성 도료에 대한 상품 및 서비스세(GST) 인하안은 수성 도료의 보급을 크게 가속화할 가능성이 있습니다.

북미와 유럽은 합쳐서 전 세계 지출의 상당 부분을 차지하고 있습니다. 미국에서는 환경보호청(EPA)의 에어로졸 도료 규제 기한에 더해, 휘발성 유기화합물(VOC)에 관한 주 차원의 규제로 인해 소비재 분야에서 비닐아세테이트 호모폴리머의 사용이 촉진되고 있습니다. 동시에, 켄튀르키예주에서 와커사의 사업 확장이 국내 공급망을 강화하고 있습니다. 유럽의 순환형 경제 추진은 단일 소재 배리어 용도에 대한 수요를 뒷받침하고 있습니다. 알케마가 다우의 연포장용 접착제 사업을 전략적으로 인수한 것은 이 정책적 호재를 활용하기 위한 유리한 입지를 해당 기업에 마련해 주고 있습니다. 건설 시장은 성숙기에 접어들었으나, 기존 건물의 에너지 효율 개선 의무와 자동차 경량화에 대한 집중적인 노력이 계속해서 완만한 성장을 이끌고 있습니다.

남미는 전 세계 매출에서 차지하는 비중은 작지만, 브라질의 인프라 프로젝트와 자동차 OEM에 대한 투자로 인해 혜택을 보고 있습니다. 그러나 환율 변동은 특히 원자재 수입 비용 측면에서 과제로 대두되고 있습니다. 이러한 불확실성으로 인해 컨버터는 현지 조달로 방향을 전환하고 있습니다. 이러한 동향에 대응하여 신세마는 제품의 현지화를 추진하여, 기존에는 유럽에서 수입하던 등급을 미국 및 라틴아메리카의 공장으로 전환함으로써 운송비와 관세에 대한 의존도를 낮췄습니다. 중동 및 아프리카는 절대적인 규모는 작지만, 눈부신 성장을 보이는 지역들이 곳곳에 흩어져 있습니다. 이러한 확대는 사우디아라비아나 남아프리카공화국 등 가처분 소득 증가 및 위생용품 소비 확대와 맞물려 주택 정책이 추진되고 있는 지역에서 특히 두드러지지만, 그 기반은 소규모이며 생산 능력의 한계로 인한 제약에도 직면해 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the vinyl acetate homopolymer emulsion market size is projected to expand from USD 3.39 billion in 2025 and USD 3.53 billion in 2026 to USD 4.32 billion by 2031, registering a CAGR of 4.12% between 2026 to 2031.

This report is Segmented by Application (Paints and Coatings, Adhesives, and More), End-User Industry (Building and Construction, Packaging, Automotive and Transportation, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Vinyl Acetate Homopolymer Emulsion Market Trends and Insights

Regulatory Shift Toward Low-VOC Paints And Coatings

On June 1, 2026, China enforced its GB 30981.1-2025 and GB 30981.2-2025 regulations, tightening limits on formaldehyde, heavy metals, aromatics, and volatile organic compounds. Concurrently, GB 37824-2019 mandates a significant level of abatement efficiency for non-methane hydrocarbon emissions exceeding a specific threshold in standard regions. These regulations steer formulators towards waterborne systems. Here, vinyl acetate homopolymer emulsions ensure compliance, sidestepping the need for expensive thermal oxidizers. Europe mirrors this trend with expanding bans on per- and polyfluoroalkyl substances and reduced volatile organic compound limits, while the United States sets a deadline in early 2027 for aerosol-coating regulations issued by the Environmental Protection Agency. Across the globe, downstream users prioritize binders devoid of aromatics and with minimal residual monomers. This trend gives a competitive advantage to suppliers who provide pre-qualified, regulation-compliant grades. The tightening regulations are also hastening the shift away from high-solids solvent systems in industrial metal and plastic coatings. This shift broadens the market for vinyl acetate homopolymer emulsions. Notably, a large proportion of Asia-Pacific coating formulators now prioritize "waterborne compliance" in their purchasing decisions, highlighting the influence of policy on procurement choices.

Growing Paper And Tissue Production In Asia And Europe

Urbanization and the increasing adoption of sanitary products are driving significant growth in tissue machine capacity in China, India, and ASEAN. Vinyl acetate homopolymer emulsions, known for their uniform film formation and strong adhesion, are favored by high-speed coaters and remain a cost-effective choice compared to styrene-acrylic alternatives. In Europe, as mills pivot from graphic-paper lines to recyclable packaging grades, there is a surge in demand for low-odor binders with customized rheology. A recent product launch highlights the merging priorities of hygiene, packaging, and recyclability. This innovation allows heat-sensitive snacks and confections to transition from traditional plastics to a more sustainable barrier-coated paper. Typically, these barrier-coated formats rely on vinyl acetate homopolymer emulsions. These emulsions not only harmonize with mineral or nanocellulose additives but also resist aqueous food simulants, offering greater formulation flexibility compared to solvent systems. This creates a beneficial cycle: as pulp expansion boosts coating demand, innovations in coating further propel paper's competition with flexible plastics.

VAM Feedstock Price Volatility

Produced from ethylene and acetic acid, the cost of vinyl acetate monomer is closely linked to upstream benchmarks of crude oil and natural gas, which experienced significant quarterly fluctuations. Outages at major vinyl acetate monomer units in Taiwan and the United States caused a significant increase in spot prices, highlighting the industry's susceptibility to unexpected downtimes. Regional price disparities, intensified by freight bottlenecks and tariff changes, compel Asian emulsion producers to navigate a tightrope between domestic and imported ethylene. This price volatility not only diminishes margins on fixed-price contracts but also complicates the cost-plus price pass-through, a challenge especially pronounced for smaller formulators. While major players like Celanese and Wacker, with their backward-linked vinyl acetate monomer capacities and ethylene pipelines, enjoy some insulation from these swings, they still acknowledge feedstock fluctuations as a significant earnings risk in their annual reports. In response, procurement teams are broadening their supply sources and securing longer-term ethylene swap contracts, albeit with the understanding that these hedges introduce additional overhead and counterparty risks.

Other drivers and restraints analyzed in the detailed report include:

- Boom In Non-Woven Hygiene Output Across South And Southeast Asia

- Adoption As Functional Barrier Coatings For Recyclable Mono-Material Packaging

- Competition From Acrylic And VAE Copolymer Emulsions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Paints and Coatings contributed significantly to the overall revenue, equivalent to 36.22% of 2025 revenue, anchoring the vinyl acetate homopolymer emulsion market share lead in applications. Architectural formulations dominate within this slice, buoyed by China's shift to waterborne systems and Europe's tightening VOC ceilings. During the same horizon, performance-grade emulsions with co-monomer grafting are expected to chip away at solvent-borne industrial coatings, broadening the application base.

Non-Woven applications are anticipated to begin from a relatively smaller market base. are forecast to rise at a 4.22% CAGR between 2026 and 2031. Hygiene converters are increasingly favoring vinyl acetate homopolymer binders due to their low-odor profile and softness. Notably, a significant number of leading diaper producers in Southeast Asia have approved grades supplied locally. Meanwhile, the adhesive segment is experiencing steady growth. This is largely driven by a shift towards recyclable mono-material packaging, which has heightened the demand for resealable and cold-seal systems. These systems, in turn, depend on high-tack homopolymer dispersions. Although textile and other applications contribute a smaller share to the overall value, they serve as crucial testing grounds for digital-printing binders and specialty sealants. Innovations that prove successful in these areas often transition to higher-volume segments, ensuring a continuous flow in the product pipeline.

Geography Analysis

Asia-Pacific remains the demand epicenter, accounting for 46.67% of 2025 revenue and expanding at a 4.65% CAGR through 2026 to 2031. China's dominance in coatings volumes, coupled with India's surge in hygiene production, drives the market's momentum. Celanese's Nanjing complex, with significant production capacity for vinyl acetate monomer and vinyl acetate ethylene emulsion, stands as a testament to the localized supply strategies essential for catering to the region's vast consumption. Regulatory momentum, particularly China's GB 30981 series, solidifies the shift towards waterborne products. Meanwhile, hygiene plants in the Association of Southeast Asian Nations region offer an incremental boost. India's ambitious goal to double housing availability anchors the demand for construction-related coatings. Furthermore, a proposed reduction in the goods and services tax on water-based paints could significantly accelerate their adoption.

North America and Europe collectively represent a substantial portion of global spending. In the United States, the Environmental Protection Agency's deadline for aerosol coatings, combined with state-level regulations on volatile organic compounds, promotes the adoption of vinyl acetate homopolymer in consumer goods. Concurrently, Wacker's expansion in Kentucky fortifies the domestic supply chain. Europe's push towards a circular economy fuels demand for mono-material barrier applications. Arkema's strategic acquisition of Dow's flexible-packaging adhesives business positions it to benefit from this policy momentum. Despite the maturity of construction markets, mandates for retrofit energy efficiency and a focus on automotive lightweighting continue to drive modest growth.

While South America accounts for a smaller share of global revenue, it reaps benefits from Brazilian infrastructure projects and investments in original equipment manufacturer automotive. However, currency volatility poses challenges, especially in raw-material import costs. This unpredictability nudges converters towards local sourcing. Responding to this trend, Synthomer has localized its products, transitioning previously imported European grades to its United States and Latin American plants, thereby reducing exposure to freight and duties. The Middle East and Africa, though smaller in absolute size, witness pockets of significant growth. This expansion is particularly notable where Saudi and South African housing initiatives align with a rising disposable income and increased hygiene consumption, albeit starting from a modest base and facing constraints due to limited polymerization capacity.

- Allnex GmbH

- Arkema (Bostik)

- Celanese Corporation

- Chang Chun Group

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Hexion Inc.

- Kuraray Co., Ltd.

- Shaanxi XuTai Technology Co., Ltd

- Sinopec Sichuan Vinylon Works

- Synthomer plc

- Tailored Adhesives.

- Vinavil S.p.A.

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory shift toward low-VOC paints and coatings

- 4.2.2 Growing paper and tissue production in Asia and Europe

- 4.2.3 Boom in non-woven hygiene output across South and Southeast Asia

- 4.2.4 Adoption as functional barrier coatings for recyclable mono-material packaging

- 4.2.5 Demand for digital-printing-grade binder emulsions

- 4.3 Market Restraints

- 4.3.1 VAM feed-stock price volatility

- 4.3.2 Competition from acrylic and VAE copolymer emulsions

- 4.3.3 Difficulty meeting food-contact migration limits without costly cross-linkers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Application

- 5.1.1 Paints and Coatings

- 5.1.2 Adhesives

- 5.1.3 Textiles

- 5.1.4 Non-woven

- 5.1.5 Other Applications (Sealants, etc.)

- 5.2 By End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Packaging

- 5.2.3 Automotive and Transportation

- 5.2.4 Other End-user Industries (Furniture, Footwear, Paper and Printing)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Allnex GmbH

- 6.4.2 Arkema (Bostik)

- 6.4.3 Celanese Corporation

- 6.4.4 Chang Chun Group

- 6.4.5 Dow

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 Hexion Inc.

- 6.4.9 Kuraray Co., Ltd.

- 6.4.10 Shaanxi XuTai Technology Co., Ltd

- 6.4.11 Sinopec Sichuan Vinylon Works

- 6.4.12 Synthomer plc

- 6.4.13 Tailored Adhesives.

- 6.4.14 Vinavil S.p.A.

- 6.4.15 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment