|

시장보고서

상품코드

2062291

실리콘 엘라스토머 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Silicone Elastomers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

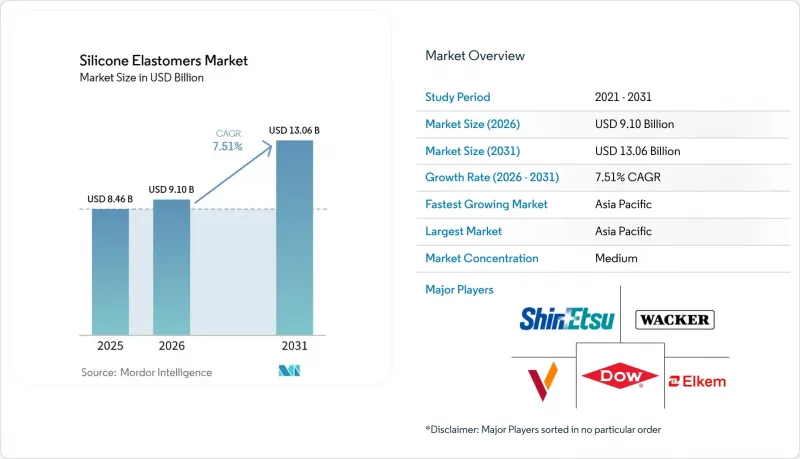

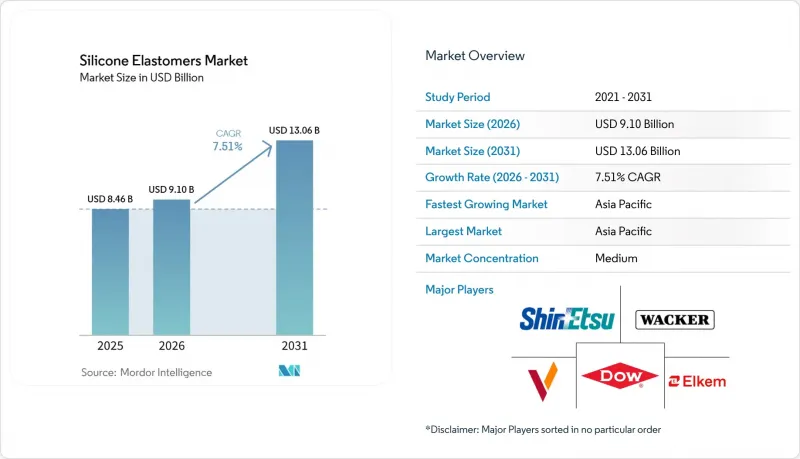

Mordor Intelligence에 의하면, 실리콘 엘라스토머 시장 규모는 2025년에 84억 6,000만 달러로 평가되었고 2026년 91억 달러에서 2031년까지 130억 6,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 7.51%를 나타낼 전망입니다.

본 보고서는 제품별(고온 가황(HTV), 상온 가황(RTV) 등), 용도별(전기 및 전자, 자동차 및 운송, 산업기계, 소비재, 건설, 기타) 및 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 실리콘 엘라스토머 시장 동향 및 분석

전자 기기의 소형화와 5G의 열 관리

5세대 기지국 및 인공지능 가속기에서 더 높은 전력 밀도에 대한 수요가 증가함에 따라, 뛰어난 열전도성을 갖춘 실리콘 열전도성 인터페이스 재료에 대한 수요가 매우 중요해지고 있습니다. 다우(Dow)사의 DOWSIL TC-5550 및 바커(Wacker)사의 SEMICOSIL 9649 TC는 이러한 요건을 충족합니다. 또한, 이러한 소재는 뛰어난 전기 절연성을 갖추고 있으며, 광범위한 온도 변화에도 견딜 수 있습니다. 알루미나 필러를 질화붕소나 그래핀으로 대체함으로써, 각 제조업체는 열저항을 대폭 낮췄습니다. 이 기술 개발은 소형 소비자용 전자기기 및 자동차용 전자기기 모두에서 수동 냉각 솔루션의 도입을 촉진하고 있습니다. 한편, 신에츠 화학공업은 중국 핑후에 새로운 공장을 설립했습니다. 이 생산 라인은 반도체 패키징에 필수적인 엄격한 이온 순도 기준을 충족하도록 특별히 설계되었으며, 이는 고순도 공급망에서 해당 지역의 중요성이 커지고 있음을 보여줍니다.

웨어러블 의료기기에 의료용 LSR의 적용

각 제조업체들은 지속형 혈당 모니터, 심장용 패치, 약물 전달 시스템 등의 기기에서 열가소성 엘라스토머에서 액상 실리콘 고무로의 전환을 추진하고 있습니다. 액상 실리콘 고무는 ISO 10993 규격을 준수할 뿐만 아니라, 피부에 자극을 주지 않으면서 장시간 접촉이 가능합니다. 듀폰은 폭넓은 경도 범위와 긴 작업 가능 시간을 갖춘 ‘Liveo C6-8XX’ 시리즈를 출시하여, 자동화 라인의 성형 가동 중단 시간을 대폭 단축했습니다. 한편, 엘켐(Elkem)사의 액상 실리콘 고무 ‘SILBIONE EC 70’은 탄소나노튜브를 통해 전도성을 갖추고 있어, 심전도 패치용 건식 전극의 제조를 가능하게 합니다. 이러한 혁신을 통해 사용 전 피부 준비 과정이 필요 없어져 임상 업무 흐름이 효율화됩니다.

실록산 원료 공급망의 변동

금속 실리콘 가격은 연초부터 연말에 걸쳐 크게 상승했습니다. 이러한 상승세는 이란산 메탄올 공급 차질과 산둥성 공장의 폭발 사고로 인해 발생했으며, 이로 인해 디메틸디클로로실란의 생산 능력이 감소했습니다. 업스트림 공정을 통합하지 않은 유럽의 변환업체들은 이익률의 급격한 하락에 직면한 반면, 업스트림 공정을 통합한 기업들은 원자재 비용 절감의 혜택을 누리며 영업이익 회복을 달성했습니다.

부문별 분석

2025년, 액상 실리콘 고무는 실리콘 엘라스토머 시장에서 45.22%의 점유율을 차지할 것으로 예상되며, 2026년부터 2031년까지 연평균 성장률(CAGR) 8.34%로 시장 점유율을 확대할 것으로 전망됩니다. 점도가 낮기 때문에 자동 사출 성형 공정을 신속하게 완료할 수 있으며, 정밀한 공차를 실현할 수 있습니다. 이러한 정밀도는 전기차용 대량 생산 웨어러블 기기 및 센서에 있어 필수적입니다. 듀폰의 ‘Liveo C6-8XX’와 엘켐의 전도성 ‘SILBIONE’ 액상 실리콘 고무는 액상 실리콘 고무의 경쟁 우위를 유지하는 기능적 강화가 특징입니다. 고온 가황 등급은 터보차저용 호스나 전선 절연체 등, 높은 사용 온도와 뛰어난 인열 강도가 요구되는 용도에서 필수적입니다. 한편, 상온 가황 실리콘은 현장 건설용 실런트로 널리 사용되고 있습니다. 상온에서 경화되며, 휘발성 유기화합물(VOC) 배출량이 극히 적다는 특징을 가지고 있습니다.

액체 실리콘 고무의 존재감이 커지고 있다는 점은 소비재 분야에서도 분명합니다. 젖병 젖꼭지, 오븐용 매트, 개인 위생용 브러시 등의 제품은 액상 실리콘 고무가 식품 등급 기준을 충족한다는 점에서 이점을 얻고 있으며, 오토클레이브 처리로 인한 맛의 변질이 없고 내구성도 확보되어 있습니다. Wacker사의 ELASTOSIL R 531/60으로 대표되는 세라마이피케이션 처리를 거친 액상 실리콘 고무는 현재 전기자동차의 버스바를 열 과열로부터 보호하고 있으며, 이는 차세대 배터리의 안전성 측면에서 실리콘이 수행하는 지극히 중요한 역할을 여실히 보여주고 있습니다.

지역별 분석

아시아태평양은 2025년 실리콘 엘라스토머 시장의 46.67%를 차지하며 시장을 주도하고 있으며, 2026년부터 2031년까지 연평균 성장률(CAGR) 8.11%로 성장할 것으로 전망됩니다. 신에츠 화학공업의 핑후 공장 투자와 와커의 장자강 공장 증설은 중국, 인도, 동남아시아의 전자기기 및 전기차 부문의 급속한 성장과 전략적으로 시기를 맞추고 있습니다. 중국의 정책 주도 통합으로 인해 가동률이 크게 상승할 것으로 예상되며, 이에 따라 업스트림 부문공급이 부족해지고 가격 결정력이 강화될 전망입니다.

북미는 시장에서 상당한 점유율을 확보했습니다. 미시간주에 위치한 듀폰의 헴록 공장에서는 바이오의약품 분야의 일회용 제품 수요와 확대되는 웨어러블 시장에 대응하기 위해 의료용 액상 실리콘 고무의 생산을 확대되고 있습니다. 동시에, 미국의 데이터센터 건설 현장에서는 주변 온도보다 낮은 글리콜 루프 환경을 견디기 위해 필수적인 실리콘 씰이 점점 더 많이 채택되고 있습니다. 한편, 멕시코 자동차 산업의 니어쇼어링 추세에 따라 실리콘 컴파운딩 사업이 자동차 조립 거점 인근으로 집약되면서, 해당 지역의 경제적 회복력이 강화되고 있습니다.

시장 점유율이 높은 유럽에서는 완만한 성장이 나타나고 있습니다. 그러나 규제상의 제약으로 인해 배합 변경 비용이 증가하고 있습니다. 그럼에도 불구하고, 해당 대륙의 탄소중립 건축 기준 도입 노력과 자동차 전기화 추진에 힘입어 수요는 견조한 추세를 보이고 있습니다. 특히, 시카(Sika)사의 ‘Sikasil WS-605 S’는 현재 건설 중인 수많은 넷 제로 고층 빌딩에 채택되고 있습니다. 그러나 다우(Dow)사가 영국 배리(Barry)의 거점을 폐쇄할 계획인 만큼, 현지 실록산 공급이 부족해질 전망이며, 각 변환업체들은 아시아 내 통합 공급원 확보에 박차를 가하고 있습니다.

남미와 중동 및 아프리카을 합친 지역의 세계 실리콘 소비량에서 차지하는 비중은 적습니다. 브라질의 전기차 보급 확대와 사우디아라비아의 야심 찬 메가 프로젝트 ‘NEOM’은 사막의 맹렬한 더위와 마모성이 강한 모래를 견디는 것으로 알려진 실리콘 실란트를 활용하여 중요한 성장 분야로 부상하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the silicone elastomers market size was valued at USD 8.46 billion in 2025 and is estimated to grow from USD 9.10 billion in 2026 to reach USD 13.06 billion by 2031, at a CAGR of 7.51% during the forecast period (2026-2031).

This report is Segmented by Product (High-Temperature Vulcanised (HTV), Room-Temperature Vulcanised (RTV), and More), Application (Electrical and Electronics, Automotive and Transportation, Industrial Machinery, Consumer Goods, Construction, Others), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Silicone Elastomers Market Trends and Insights

Electronics Miniaturization and 5G Thermal Management

As the demand for higher power densities increases in fifth-generation base stations and artificial intelligence accelerators, the requirement for silicone thermal-interface materials with advanced conductivity has become critical. Dow's DOWSIL TC-5550 and Wacker's SEMICOSIL 9649 TC meet these requirements. Additionally, these materials ensure excellent electrical insulation and can withstand a wide range of temperature cycles. By substituting alumina fillers with boron nitride and graphene, manufacturers have significantly reduced thermal resistance. This development supports the adoption of passive cooling solutions in both compact consumer electronics and automotive electronics. Meanwhile, Shin-Etsu has established a new facility in Pinghu, China. This line is specifically designed to meet the stringent ionic purity standards essential for semiconductor packaging, highlighting the region's growing importance in the high-purity supply chain.

Medical-Grade LSR Adoption in Wearable Healthcare

Manufacturers are transitioning from thermoplastic elastomers to liquid silicone rubber for devices like continuous glucose monitors, cardiac patches, and drug-delivery systems. Liquid silicone rubber not only complies with ISO 10993 standards but also allows for extended skin contact without irritating. DuPont introduced its Liveo C6-8XX series, offering a range of hardness and an extended pot life, significantly reducing molding downtime on automated lines. Meanwhile, Elkem's SILBIONE liquid silicone rubber EC 70 incorporates carbon-nanotube conductivity, enabling the creation of dry electrodes for electrocardiogram patches. This innovation eliminates the need for pre-use skin preparation and streamlines clinical workflows.

Siloxane Feedstock Supply-Chain Volatility

Metal silicon prices experienced a significant increase from the beginning to the latter part of the year. This rise was driven by disruptions in methanol supply from Iran and an explosion at a plant in Shandong, which collectively reduced the production capacity of dimethyldichlorosilane. Non-integrated European converters faced a notable decline in margins, while a company with upstream integration benefited from reduced feedstock costs and achieved a recovery in operating profit.

Other drivers and restraints analyzed in the detailed report include:

- Construction Sealants in Net-Zero Buildings

- Additive Manufacturing of Silicone Parts (3-D/LAM)

- EU REACH Cyclic-Siloxane Restrictions and Reformulation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Liquid Silicone Rubber captured 45.22% silicone elastomer market share in 2025, and its slice of the silicone elastomer market size is forecast to widen at an 8.34% CAGR through 2026 to 2031. With a low viscosity, automated injection cycles can be completed quickly, achieving precise tolerances. This precision is vital for high-volume wearables and sensors in electric vehicles. DuPont's Liveo C6-8XX and Elkem's conductive SILBIONE liquid silicone rubber showcase functional enhancements that maintain the competitive edge of liquid silicone rubber. High-temperature vulcanized grades are crucial for applications demanding high service temperatures or significant tear strength, such as in turbocharger hoses and wire insulation. Meanwhile, room-temperature vulcanized silicone is preferred for on-site construction sealants, curing at ambient conditions and boasting ultra-low volatile organic compound emissions.

Liquid silicone rubber's growing prominence is evident in consumer products. Items like bottle nipples, baking mats, and personal-care brushes benefit from liquid silicone rubber's compliance with food-grade standards, ensuring taste neutrality and durability through autoclaving. Ceramifying liquid silicone rubber, exemplified by Wacker ELASTOSIL R 531/60, is now safeguarding electric vehicle busbars from thermal runaway, highlighting silicone's pivotal role in the safety of next-generation batteries.

Geography Analysis

Asia-Pacific dominated the silicone elastomer market with a 46.67% share in 2025 and is projected to compound at 8.11% through 2026 to 2031. Shin-Etsu's investment in its Pinghu plan and Wacker's expansion at Zhangjiagang are strategically timed with the burgeoning electronics and electric vehicle sectors in China, India, and Southeast Asia. Thanks to policy-driven consolidation in China, utilization rates are projected to significantly increase, tightening upstream supply and bolstering pricing power.

North America secured a notable share of the market. DuPont's Hemlock site in Michigan is ramping up production of medical-grade liquid silicone rubber to cater to the biopharmaceutical sector's single-use needs and the growing wearables market. Simultaneously, United States data-center constructions are increasingly opting for silicone seals, crucial for enduring sub-ambient glycol loops. Meanwhile, Mexico's automotive nearshoring trend is pulling silicone compounding operations closer to vehicle assembly hubs, bolstering the region's economic resilience.

Europe, holding a significant market share, is witnessing modest growth. However, regulatory constraints are inflating reformulation costs. Despite this, the continent's commitment to net-zero building codes and a push towards automotive electrification are keeping demand robust. Notably, Sika's Sikasil WS-605 S is being utilized in numerous net-zero towers currently under construction. Yet, with Dow planning to shutter its Barry, United Kingdom site, the local merchant siloxane supply is set to tighten, nudging converters to seek integrated sources in Asia.

South America and the combined regions of the Middle East and Africa account for a smaller portion of global silicone consumption. Brazil's push towards electric vehicles and Saudi Arabia's ambitious NEOM megaproject are emerging as significant growth areas, capitalizing on silicone sealants renowned for withstanding the desert's scorching heat and abrasive sand.

- Avantor, Inc.

- Bentec Medical

- Cabot Corporation

- China National Bluestar (Group) Co., Ltd.

- CHT Germany GmbH

- Dow

- DuPont

- Elkem ASA

- KCC Silicone Corporation

- Mesgo S.p.A.

- Momentive

- Primasil Silicones Limited

- Reiss Manufacturing, Inc.

- Rogers Corporation

- Saint-Gobain

- Shin-Etsu Chemical Co., Ltd.

- Specialty Silicone Products, Inc.

- Stockwell Elastomerics

- Wacker Chemie AG

- Wynca Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electronics miniaturisation and 5G thermal management

- 4.2.2 Medical-grade LSR adoption in wearable healthcare

- 4.2.3 Construction sealants in net-zero buildings

- 4.2.4 Additive manufacturing of silicone parts (3-D/LAM)

- 4.2.5 Antimicrobial and conductive LSR for hygienic EandE uses

- 4.3 Market Restraints

- 4.3.1 Siloxane feedstock supply-chain volatility

- 4.3.2 Substitution risk from high-performance TPEs

- 4.3.3 EU REACH cyclic-siloxane restrictions and reformulation cost

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of Substitution

- 4.5.4 Threat of New Entrants

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 High-Temperature Vulcanised (HTV)

- 5.1.2 Room-Temperature Vulcanised (RTV)

- 5.1.3 Liquid Silicone Rubber (LSR)

- 5.2 By Application

- 5.2.1 Electrical and Electronics

- 5.2.2 Automotive and Transportation

- 5.2.3 Industrial Machinery

- 5.2.4 Consumer Goods

- 5.2.5 Construction

- 5.2.6 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Australia

- 5.3.1.6 Indonesia

- 5.3.1.7 Thailand

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Avantor, Inc.

- 6.4.2 Bentec Medical

- 6.4.3 Cabot Corporation

- 6.4.4 China National Bluestar (Group) Co., Ltd.

- 6.4.5 CHT Germany GmbH

- 6.4.6 Dow

- 6.4.7 DuPont

- 6.4.8 Elkem ASA

- 6.4.9 KCC Silicone Corporation

- 6.4.10 Mesgo S.p.A.

- 6.4.11 Momentive

- 6.4.12 Primasil Silicones Limited

- 6.4.13 Reiss Manufacturing, Inc.

- 6.4.14 Rogers Corporation

- 6.4.15 Saint-Gobain

- 6.4.16 Shin-Etsu Chemical Co., Ltd.

- 6.4.17 Specialty Silicone Products, Inc.

- 6.4.18 Stockwell Elastomerics

- 6.4.19 Wacker Chemie AG

- 6.4.20 Wynca Group

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment