|

시장보고서

상품코드

2062328

열경화성 성형 재료 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Thermoset Molding Compound - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

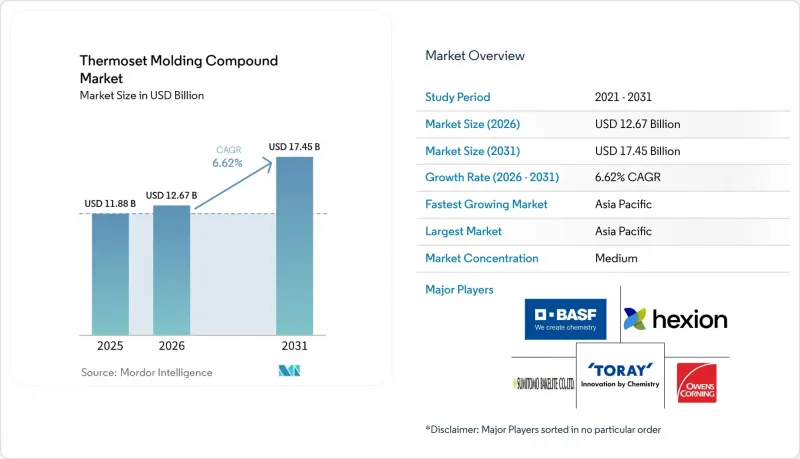

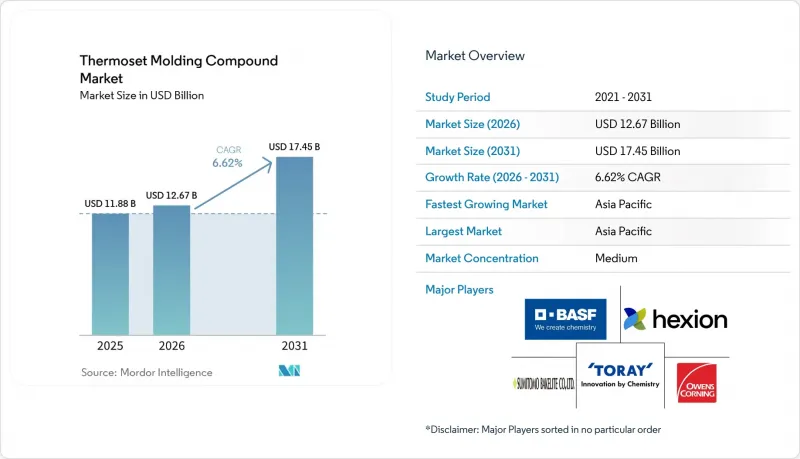

Mordor Intelligence에 의하면, 열경화성 성형 재료 시장 규모는 2025년에 118억 8,000만 달러로 평가되었고, 2026년에 126억 7,000만 달러로 추정되고, 2031년까지 174억 5,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 6.62%로 성장할 전망입니다.

본 보고서는 수지 유형별(에폭시, 멜라민 포름알데히드, 요소 포름알데히드 등), 섬유 보강재별(유리 섬유, 탄소섬유 등), 용도별(전기 및 전자, 자동차, 항공우주, 건설 등), 그리고 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 열경화성 성형 컴파운드 시장 동향 및 인사이트

전기 및 전자 분야에서의 활용 확대

800V 전기차 인버터 및 5G 기지국의 열 관리 요건에 따라, 에폭시 수지의 사양은 열전도율 0.80 W/m/K 이상, 유전율 4.0 이하로 변화하고 있습니다. 하이브리드 hBN-AlN 필러 시스템은 할로겐을 사용하지 않고도 UL 94 V-0 난연 등급을 달성하며, 105°C 연속 사용 시험을 통과해야 하는 데이터센터용 전원 장치를 지원합니다. 중국의 인쇄회로기판 생산액은 2026년까지 546억 달러에 달할 것으로 예상되며, 이는 FR-4 및 고주파 적층 기판용 에폭시 수요를 뒷받침하고 있습니다. AI 가속기용 반도체 패키징 분야에서는 유리전이온도가 150°C를 초과하는 시클로알킬계 에폭시가 점점 더 선호되면서, 페놀 수지 시장 점유율을 잠식하고 있습니다. 현재 12개월 미만으로 단축된 인증 주기로 인해, 디지털 시뮬레이션 및 사내 신속한 시제품 제작 능력을 제공하는 공급업체들이 유리한 입지를 점하고 있습니다.

자동차 및 항공우주 분야의 경량화 추진

유럽의 차량 CO2 배출량 상한선 95g/km 규제로 인해, 각 OEM 업체들은 브래킷, 크로스빔, 배터리 인클로저를 강철에서 유리섬유 페놀 수지 및 탄소섬유 에폭시 수지로 전환하여 차량 중량을 최대 50%까지 줄여야만 하는 상황에 처해 있습니다. BASF의 스프레이 전사 성형 공정을 통해 클래스 A 차체 패널을 3분 주기로 생산할 수 있게 되었으며, 도장 소성로가 필요 없어짐에 따라 에너지 사용량을 40% 절감할 수 있습니다. 항공우주 분야에서는 HexPly M51 프리프레그가 180°C에서 40분 만에 경화되므로, 오토클레이브의 에너지 소비를 30% 절감하고 1교대당 생산 능력을 향상시킵니다. 한국공급망에서는 비구조 영역에서 페놀계 시트 성형 컴파운드를 대체할 가능성이 있는 유리 매트 열가소성 범퍼 빔의 시범 도입이 진행되고 있습니다. 모빌리티 플랫폼 전반에 걸쳐 경량화는 규제 크레딧 확보 및 배터리 주행 거리 연장과 직결되며, 열경화성 성형 컴파운드 시장의 가치 제안을 강화하고 있습니다.

재활용성이 낮고 폐기 시 발생하는 비용

비가역적인 가교 반응으로 인해, 열경화성 스크랩의 대부분은 매립 처분이나 고비용의 열분해 처리에 국한되어 있습니다. 열분해 처리 비용은 톤당 200-400달러로, 이는 원료의 가치의 2배에 해당합니다. EU 지침 2018/851은 2030년까지 복합재료의 70%를 회수하는 것을 목표로 하고 있지만, 기계적 분쇄를 거치면 재료가 저가치의 충전재로 전락하고 맙니다. 3MW급 풍력 터빈 1기에서 20톤의 블레이드 폐기물이 발생하며, 유럽에서는 14,000기의 블레이드가 폐기될 것으로 예상되어 독일과 덴마크의 매립지 용량에 부담을 주고 있습니다. 분해를 전제로 한 설계(Design-for-disassembly)는 차량 1대당 50-100달러의 인건비 증가를 초래하기 때문에 확대 생산자 책임 제도가 확대되지 않는 한 OEM 업체들의 도입은 진전되지 않을 것입니다. 비트리머 제조 공장에 5,000만 달러의 투자가 필요하며, 이는 통합형 수지 대기업만이 감당할 수 있는 금액이기 때문에 단기적인 보급은 더딘 상황입니다.

부문별 분석

페놀 수지는 마찰재 및 전기차 모터 하우징에 대한 수요를 바탕으로, 2025년에는 열경화성 성형 컴파운드 시장 점유율의 28.02%를 차지했습니다. 배기가스 규제를 충족하는 제품이 가전제품의 내부 부품으로 채택됨에 따라, 페놀 수지 열경화성 성형 컴파운드 시장 규모는 완만하게 확대될 것으로 전망됩니다. 에폭시 수지는 AI 반도체 패키징 및 15MW급 풍력 발전용 블레이드 외판에 대한 수요를 바탕으로, 2031년까지 연평균 성장률(CAGR) 7.02%를 기록하며 시장을 선도하고 있습니다. 폴리에스터 BMC는 비용 효율을 중시하는 위생 도기 분야에서 뒤처지고 있는 반면, 멜라민 및 요소 유도체는 배출 규제 강화로 인해 시장 점유율이 줄어들고 있습니다.

에폭시 수지 배합 제조업체들은 AI 가속기 패키지의 요구 사항을 충족하는 Tg(유리 전이 온도) 150°C 이상이며 흡습률이 1%인 시클로알킬계 제품의 상용화를 추진하고 있습니다. 중국의 페놀 수지 생산량은 2024년에 160만 톤을 넘어섰으며, 산동성천이 25%의 점유율로 1위를 차지하고 있어 아시아의 비용 우위를 입증하고 있습니다. 비닐 에스테르나 디알릴 프탈레이트와 같은 틈새 시장용 시스템은 각각 내식성 및 고전압 절연 분야에서 입지를 차지하고 있으며, 가격은 2-5배의 프리미엄이 붙고 있습니다. 열경화성 성형 컴파운드 업계에서는 실패가 용납되지 않는 분야에서 이러한 비용을 감당하고 있습니다.

지역별 분석

아시아태평양은 2025년에 열경화성 성형 컴파운드 시장 매출의 45.72%를 차지한 것으로 평가되었으며, 중국의 400만 톤에 달하는 에폭시 수지 생산 능력과 급증하는 해상 풍력 발전 설비의 성장에 힘입어 2031년까지 연평균 성장률(CAGR) 7.43%로 확대될 것으로 전망됩니다. 인도의 반덤핑 관세는 1조 4,000억 달러 규모의 인프라 계획과 관련된 국내 수지 프로젝트를 촉진하고 있습니다. 일본의 각 OEM 업체들은 전기차용 기어에 PM-5700 페놀 수지 컴파운드를 채택하고 있으며, 2030년까지 1,300만 달러의 매출을 목표로 하고 있습니다. 한국의 장섬유 열가소성 수지 관련 계획은 대체재의 위협을 시사하고 있지만, 해당 지역의 열경화성 성형 컴파운드 시장은 의무화된 난연 성능 요건으로 인해 여전히 견조한 모습을 유지하고 있습니다.

북미에서는 중국산 에폭시에 대한 미국의 반덤핑 관세로 인해 공급 부족에 직면해 있어, 조달처를 멕시코나 캐나다로 전환하고 있지만, 국내 생산 능력은 이전 수입량의 40% 미만에 그치고 있습니다. 헥셀사의 2025년 매출액 18억 9,000만 달러는 항공우주 분야의 높은 수요를 보여주고 있으며, 아르케마사의 켄튀르키예주에 위치한 폴란 1233zd 공장은 국내 풍력 블레이드 재활용 추진 정책을 뒷받침하고 있습니다.

유럽에서는 0.1ppm(100만 분의 1)의 포름알데히드 허용 기준과 70%의 복합재 재활용 의무가 균형을 이루고 있어, 기존 페놀 수지 제조업체들에게 혁신 아니면 철수라는 선택을 강요하고 있습니다. 독일과 덴마크는 블레이드 폐기물의 급증에 직면해 있으며, 비트리머에 관한 연구 협력이 가속화되고 있습니다. 남미 및 중동 및 아프리카은 규모는 작지만 성장 의지가 강하며, 석유화학 및 수자원 인프라 분야에 사용되는 내식성 비닐에스테르계 수지를 중시하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the thermoset molding compound market size is projected to be USD 11.88 billion in 2025, USD 12.67 billion in 2026, and reach USD 17.45 billion by 2031, growing at a CAGR of 6.62% from 2026 to 2031.

This report is Segmented by Resin Type (Epoxy, Melamine Formaldehyde, Urea Formaldehyde, and More), Fiber Reinforcement (Glass Fiber, Carbon Fiber, and More), Application (Electrical and Electronics, Automotive, Aerospace, Construction, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Thermoset Molding Compound Market Trends and Insights

Growing Use in Electrical and Electronics

Thermal-management requirements for 800-volt EV inverters and 5G base stations are driving epoxy specifications toward thermal conductivities above 0.80 W/m/K and dielectric constants below 4.0. Hybrid hBN-AlN filler systems now deliver UL 94 V-0 flame ratings without halogens, supporting data-center power supplies that must pass 105°C continuous-use tests. China's printed-circuit-board output is forecast to hit USD 54.6 billion by 2026, sustaining epoxy demand for FR-4 and high-frequency laminates. Semiconductor packaging for AI accelerators increasingly favors cycloaliphatic epoxies with glass-transition temperatures above 150°C, eroding phenolic share. Shorter qualification cycles, now under 12 months, reward suppliers offering digital simulation and in-house rapid prototyping capabilities.

Automotive and Aerospace Lightweighting Push

European fleet CO2 ceilings of 95 g/km are compelling OEMs to shift brackets, crossbeams, and battery enclosures from steel to glass-fiber phenolic and carbon-fiber epoxy, trimming vehicle mass by up to 50%. BASF's spray transfer molding process enables Class-A body panels in 3-minute cycles, eliminating paint-bake ovens and cutting energy usage 40%. In aerospace, HexPly M51 prepreg cures in 40 minutes at 180°C, reducing autoclave energy 30% and unlocking single-shift throughput. Korea's supply chain is piloting glass-mat thermoplastic bumper beams that threaten phenolic sheet-molding compounds in non-structural zones. Across mobility platforms, lightweighting ties directly to regulatory credits and extended battery range, enhancing the thermoset molding compound market value proposition.

Poor Recyclability and End of Life Costs

Irreversible cross-linking confines most thermoset scrap to landfill or costly pyrolysis, where gate fees run USD 200-400 per tonne, double virgin material value. EU Directive 2018/851 targets 70% composite recovery by 2030, yet mechanical grinding downgrades materials to low-value fillers. A single 3-MW wind turbine yields 20 tonnes of blade waste, and Europe expects 14,000 blade retirements, straining landfill space in Germany and Denmark. Design-for-disassembly adds USD 50-100 per vehicle in labor, discouraging OEM adoption unless extended producer responsibility regimes expand. Vitrimer plants require USD 50 million investment, affordable only for integrated resin majors, slowing near-term penetration.

Other drivers and restraints analyzed in the detailed report include:

- Renewable Energy Composite Demand Surge

- Infrastructure Prefabs Adopting High Durability Compounds

- Formaldehyde Based Compound HSE Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Phenolic resins delivered 28.02% of the Thermoset Molding Compound market share in 2025 on the back of friction materials and EV motor housings. The Thermoset Molding Compound market size for phenolics is projected to advance modestly as emission-controlled variants secure appliance interiors. Epoxy is pacing ahead at a 7.02% CAGR through 2031 on demand for AI semiconductor packaging and 15-MW wind-blade skins. Polyester BMC trails in cost-sensitive sanitary ware, while melamine and urea derivatives fade under emission scrutiny.

Epoxy formulators are commercializing cycloaliphatic grades with Tg above 150°C and 1% moisture uptake, aligning with AI accelerator packages. China's phenolic output surpassed 1.60 million tons in 2024, led by Shandong Shengquan with 25% share, underscoring Asia's cost edge. Niche systems such as vinyl-ester and diallyl phthalate occupy corrosion-resistant and high-voltage insulation segments, respectively, at 2-5X price premiums, which the thermoset molding compound industry absorbs where failure is not an option.

Geography Analysis

Asia-Pacific anchored 45.72% of the Thermoset Molding Compound market revenue in 2025 and is projected to rise at a 7.43% CAGR to 2031, propelled by China's 4.0 million-ton epoxy capacity and surging offshore wind installations. Indian anti-dumping duties are catalyzing domestic resin projects linked to a USD 1.4 trillion infrastructure pipeline. Japanese OEMs are adopting PM-5700 phenolic compounds in EV gears, targeting USD 13 million sales by 2030. Korean programs around long-fiber thermoplastics signal emerging substitution threats, yet the thermoset molding compound market in the region remains resilient on mandated flame performance.

North America faces supply tightness after U.S. anti-dumping margins on Chinese epoxy, shifting procurement to Mexico and Canada, while domestic capacity lags 40% below prior import volumes. Hexcel's USD 1.89 billion sales in 2025 underscore aerospace pull, and Arkema's Kentucky Forane 1233zd plant backs domestic wind-blade recyclability initiatives.

Europe balances 0.1 ppm (parts per million) formaldehyde thresholds with 70% composite recycling mandates, pressuring phenolic incumbents to innovate or exit. Germany and Denmark confront blade-waste surges, accelerating vitrimer research collaborations. South America and Middle East-Africa remain smaller but growth-oriented, emphasizing corrosion-resistant vinyl-ester systems for petrochemical and water infrastructure.

- Arkema

- Ashland

- BASF

- Chang Chun Group

- Core Molding Technologies

- CSP

- DIC Corporation

- Hexcel Corporation

- Hexion Inc.

- Huntsman

- IDI Composites International

- Menzolit

- Mitsubishi Gas Chemical Next Company, Inc.

- Momentive

- Owens Corning

- Plenco

- Polynt SpA

- POLYTEC HOLDING AG

- Resonac Holdings Corporation

- Scott Bader Company Ltd

- Sumitomo Bakelite Co., Ltd.

- Toray Advanced Composites

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing use in electrical and electronics

- 4.2.2 Automotive and aerospace lightweighting push

- 4.2.3 Renewable-energy composite demand surge

- 4.2.4 Infrastructure prefabs adopting high-durability compounds

- 4.2.5 Regional epoxy capacity build-up post anti-dumping duties

- 4.2.6 Dynamic-covalent/vitrimer technologies enabling recyclability

- 4.3 Market Restraints

- 4.3.1 Poor recyclability/end-of-life costs

- 4.3.2 Formaldehyde-based compound HSE risks

- 4.3.3 Protectionist trade barriers disrupting supply chains

- 4.3.4 Emergent thermoplastic composites cannibalising low-temperature uses

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Epoxy

- 5.1.2 Phenolic

- 5.1.3 Polyester

- 5.1.4 Melamine Formaldehyde

- 5.1.5 Urea Formaldehyde

- 5.1.6 Other Thermoset Resins

- 5.2 By Fiber Reinforcement

- 5.2.1 Glass Fiber

- 5.2.2 Carbon Fiber

- 5.2.3 Other Reinforcements

- 5.3 By Application

- 5.3.1 Electrical and Electronics

- 5.3.2 Automotive

- 5.3.3 Aerospace

- 5.3.4 Construction

- 5.3.5 Consumer Goods

- 5.3.6 Other Applications

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Strategic Developments

- 6.2 Market Share(%)/ Ranking Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Arkema

- 6.3.2 Ashland

- 6.3.3 BASF

- 6.3.4 Chang Chun Group

- 6.3.5 Core Molding Technologies

- 6.3.6 CSP

- 6.3.7 DIC Corporation

- 6.3.8 Hexcel Corporation

- 6.3.9 Hexion Inc.

- 6.3.10 Huntsman

- 6.3.11 IDI Composites International

- 6.3.12 Menzolit

- 6.3.13 Mitsubishi Gas Chemical Next Company, Inc.

- 6.3.14 Momentive

- 6.3.15 Owens Corning

- 6.3.16 Plenco

- 6.3.17 Polynt SpA

- 6.3.18 POLYTEC HOLDING AG

- 6.3.19 Resonac Holdings Corporation

- 6.3.20 Scott Bader Company Ltd

- 6.3.21 Sumitomo Bakelite Co., Ltd.

- 6.3.22 Toray Advanced Composites

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment