|

시장보고서

상품코드

2062329

베어링 아이솔레이터 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Bearing Isolators - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

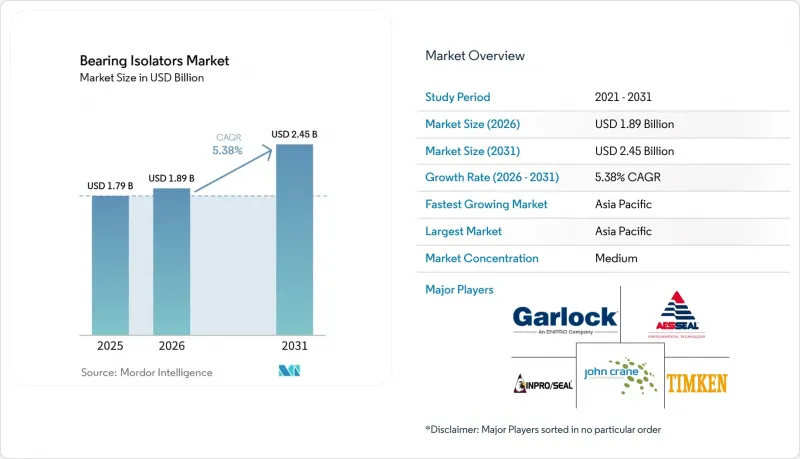

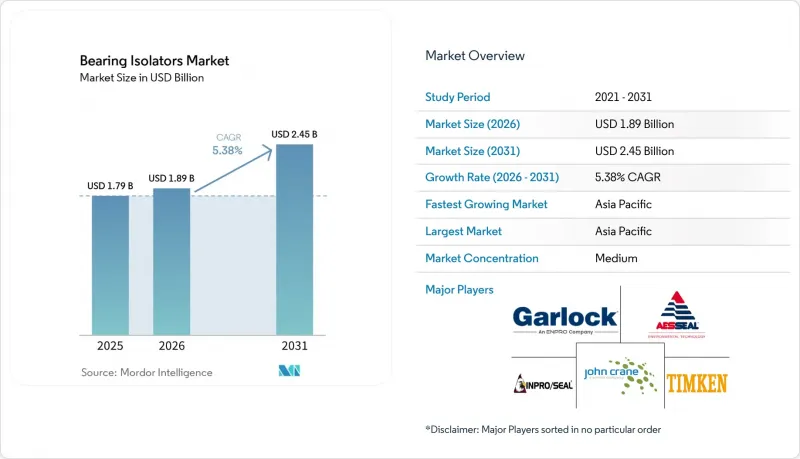

Mordor Intelligence에 의하면, 베어링 아이솔레이터 시장 규모는 2025년에 17억 9,000만 달러로 평가되었고, 2026년에 18억 9,000만 달러로 추정되고, 2031년까지 24억 5,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 5.38%로 성장할 전망입니다.

본 보고서는 유형별(비접촉형 베어링 아이솔레이터 등), 소재별(금속(청동, 스테인리스, 알루미늄) 등), 용도별(펌프, 모터 등), 최종 사용자 산업별(석유 및 가스, 화학제품 및 석유화학제품 등), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 베어링 아이솔레이터 시장 동향 및 인사이트

유지보수가 필요 없는 베어링 보호에 대한 수요 증가

현재 산업용 구매자들은 총 소유 비용을 최우선으로 고려하고 있습니다. 리브헤르(Liebherr)의 2024년형 고체 윤활 시스템은 재윤활 없이 10-15년의 수명을 실현할 것이라는 기대를 제시했습니다. 이에 이어 암스트롱(Armstrong)은 2025년에 영구 씰과 NSF/ANSI 61 규격 준수를 결합한 서큘레이터를 출시하며, 이러한 가치 제안을 한층 더 뒷받침했습니다. 300달러짜리 비접촉식 아이솔레이터는 1만 5,000달러가 드는 펌프 분해 작업을 피할 수 있게 해주며, 첫 번째 고장을 방지하는 것만으로도 투자 비용을 회수할 수 있습니다. 셰플러사가 2025년에 출시한 유도 가열 도구를 통해 작업자는 계획 정전 중에도 아이솔레이터를 설치할 수 있어 가동 중단 시간을 절반으로 줄일 수 있습니다. 서비스 중단으로 인해 하루 5만 달러의 벌금을 물게 된 수처리 사업자들은 이에 따라 미로식 또는 자기식 방식을 표준화하고 있습니다.

설비의 가동 시간 및 신뢰성에 대한 요구 증가

디지털 트윈의 도입은 더욱 확대되고 있습니다. 지멘스 에너지의 Omnivise 제품군은 2025년부터 베어링 하우징의 진동 데이터 수집을 시작하여, 씰 표면의 마모를 90일 전에 예측함으로써 강제 정지를 40% 줄였습니다. 전력구매계약(PPA)의 위약 조항에 따라, 500MW 규모의 발전소에서 가동률이 1% 하락할 때마다 200만 달러의 수익 손실이 발생하게 됩니다. 2025년 중반에 출시된 존 크레인(John Crane)사의 Type 93AX 동축 씰은 0.5mm를 초과하는 축의 흔들림에도 접촉 압력을 유지하여, 그렇지 않으면 터빈의 트립을 유발할 수 있는 누출을 방지합니다. EASA(유럽항공안전청)의 2024년 조사에 따르면, 그리스 과다 도포가 전동기 고장의 36%를 차지하고 있어, 그리스가 필요 없는 아이솔레이터로의 전환이 가속화되고 있습니다.

접촉 씰과의 비교에서 나타나는 높은 초기 비용

비접촉식 베어링 아이솔레이터는 일반적으로 엘라스토머 재질의 립 씰에 비해 3-5배의 가격 차이가 있습니다. 이러한 가격 차이는 총소유비용(TCO) 측면에서 우수함에도 불구하고, 비용 제약이 있는 시장의 조달 팀 입장에서는 정당화하기 어려운 부분입니다. 100 HP 모터용 청동 라비린스 아이솔레이터의 소매 가격은 250-350 달러인 반면, 니트릴 립 씰은 60-80 달러로, 190-270 달러의 초기 비용 차이가 발생하고 있으며, 이를 정당화하기 위해서는 수년에 걸친 투자 회수 모델의 구축이 필요합니다. 2025년 이후, 180달러에 판매되고 있는 팀켄의 ‘EcoTurn’은 이러한 가격 차이를 좁혀주고 있지만, 조달 부서와 유지보수 부서 간의 인센티브 체계가 달라서 인도와 동남아시아에서의 도입은 여전히 더딘 상황입니다.

부문별 분석

비접촉식 미로 구조는 2025년 시점에서도 베어링 아이솔레이터 시장의 46.89%를 차지했지만, 현재는 주로 펌프 및 표준 속도 모터용으로 공급되고 있습니다. 오염 환경에서 립 씰의 성능 저하를 더욱 엄격하게 규정하는 ISO 16281:2025 표준 준수가 자기식 방식으로의 전환을 가속화하고 있습니다. 자기식 구조는 예측 기간(2026-2031년) 동안 연평균 성장률(CAGR) 5.90%를 기록하며 성장할 전망이며, 마모가 전혀 없어야 하는 고속 터빈 분야에서 점점 더 선호되고 있습니다. 복합 사이클 가스 터빈 운영사 측에서는 Isomag사의 하이브리드 세라믹 모델을 통해 점검 주기가 60,000시간으로 연장되었다고 보고하고 있습니다.

미로형, 나선형 홈형 및 기타 특수 틈새 제품은 자성 유체나 엘라스토머가 극한 환경을 견디지 못하는 극저온 펌프나 해저 구동 장치에서 여전히 필수적입니다. 축의 편심이 발생하기 쉬운 경우, John Crane사의 8628VL과 같이 하이브리드 O-링과 PTFE를 조합한 설계는 1.0 mm의 편심을 허용하여 적용 가능한 설치 범위를 넓혀줍니다.

2025년 베어링 아이솔레이터 시장 규모에서 금속(청동, 스테인리스 스틸, 알루미늄) 설계가 50.87%의 점유율을 차지했으며, 부식성이 강한 석유 및 가스 업계나 제약 업계의 세척 환경에서는 청동과 스테인리스 스틸이 주도적인 역할을 하고 있습니다. 그러나 복합 및 하이브리드 소재 부문은 예측 기간(2026-2031년) 동안 6.34%의 성장 궤도에 올라 있습니다. PEEK 강화 PTFE는 2025년 실시된 실험실 테스트에서 마모를 60% 줄였으며, 나셀의 경량화가 kW당 비용 절감으로 이어지는 풍력 터빈에서의 채택을 가속화하고 있습니다.

고분자 화학이 더욱 발전하기 전까지는 사워 가스나 황산에 노출되는 환경에서는 청동이 계속해서 표준적인 선택지가 될 것입니다. 스테인리스 316L은 파커-하니핀(Parker-Hannifin)사가 150°C의 증기 멸균 주기를 견딜 수 있는 FDA(미국 식품의약국) 규격 제품을 출시함에 따라 그 기세가 더욱 거세지고 있습니다. 청동보다 65% 가벼운 알루미늄은 현재 천장 설치형 HVAC 개조 시, 더 무거운 장치를 대체하고 있습니다.

지역별 분석

아시아태평양은 2025년에 베어링 아이솔레이터 시장 점유율의 40.78%를 차지한 것으로 평가되었으며, 2031년까지 연평균 6.39%의 성장률을 기록할 전망입니다. 2024년 중국의 자동차 생산 대수 18억 대는 OEM(원청 브랜드 제조) 및 개조 수요를 모두 견인하고 있습니다. 인도의 기계 수입이 22% 증가하고 아세안(ASEAN)으로 2,260억 달러 규모의 외국인 직접 투자(FDI)가 유입되면서, 설계 단계에서 아이솔레이터 사양을 적용하는 경향이 더욱 강해지고 있습니다. 일본과 한국에서 ISO 17956:2025가 채택됨에 따라 접촉식 씰은 더욱 불리한 입장에 몰리게 되었으며, 지역 차원의 전환이 가속화되고 있습니다.

북미에서는 OSHA의 2025년 가드 규정에 따라 식품 및 제약 공장에서 립 씰 대신 NSF H1 인증을 받은 아이솔레이터로 전환하는 추세가 확산되고 있습니다. 캐나다 오일샌드에서 실시한 시험 결과, VBMag 도입 후 베어링 교체 빈도가 80% 감소했습니다. 멕시코에서의 니어쇼어링은 클린룸 조립 컨베이어용 미로형 씰 수요를 촉진하고 있습니다.

2025년 유럽 시장 점유율은 해상 풍력 발전의 확산에 힘입어 증가했습니다. System Seals사의 복합 유닛은 현재 북해의 신규 풍력 터빈 중 60%에 채택되어 있습니다. 개정된 2006/42/EC 지침에 따른 고속 트리거 레벨 상향 조치는 독일과 프랑스 전역에서 업그레이드를 촉진하고 있습니다. 러시아에서는 공급망 단절을 배경으로 자체 설계로의 전환이 진행되고 있습니다. 남미 및 중동 및 아프리카(MEA) 지역의 총 점유율은 10% 미만이지만, 광업, 석유화학, 해수 담수화 등 각 분야에서 국지적인 수요가 나타나고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the bearing isolators market size is projected to be USD 1.79 billion in 2025, USD 1.89 billion in 2026, and reach USD 2.45 billion by 2031, growing at a CAGR of 5.38% from 2026 to 2031.

This report is Segmented by Type (Non-Contact Bearing Isolators, and More), Material (Metallic (Bronze, Stainless, and Aluminum), and More), Application (Pumps, Motors, and More), End-User Industry (Oil and Gas, Chemical and Petrochemical, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Bearing Isolators Market Trends and Insights

Growing Demand for Maintenance-Free Bearing Protection

Industrial buyers now prioritize total cost of ownership. Liebherr's 2024 solid-lubrication system set expectations for 10-15-year service life without re-greasing. Armstrong followed by launching circulators in 2025 that pair permanent seals with NSF/ANSI 61 compliance, further validating the value narrative. A USD 300 non-contact isolator averts pump teardowns that cost USD 15,000, paying for itself at the first avoided failure. Schaeffler's induction-heating tools, released in 2025, let crews install isolators during planned outages, cutting downtime in half. Water-treatment operators, facing USD 50,000-per-day penalties for service interruptions, are therefore standardizing on labyrinth or magnetic formats.

Increasing Equipment Uptime and Reliability Requirements

Digital-twin adoption is deepening. Siemens Energy's Omnivise suite began ingesting bearing-housing vibration data in 2025 to predict seal-face wear 90 days ahead, reducing forced outages by 40%. Penalty clauses in power-purchase agreements make each 1% availability shortfall worth USD 2 million in lost revenue on a 500 MW station. John Crane's Type 93AX coaxial seal, launched mid-2025, holds contact pressure over 0.5 mm of shaft runout, preventing leaks that would otherwise trip turbines. An EASA (European Union Aviation Safety Agency) 2024 study found that over-greasing causes 36% of electric-motor failures, intensifying the pivot toward grease-free isolators.

Higher Initial Cost Versus Contact Seals

Non-contact bearing isolators typically command a 3-5X price premium over elastomeric lip seals, a gap that procurement teams in cost-constrained markets struggle to justify despite superior total cost of ownership. A bronze labyrinth isolator for a 100 HP motor retails at USD 250-350, whereas a nitrile lip seal costs USD 60-80, creating a USD 190-270 upfront delta that requires multi-year payback modeling to rationalize. Timken's EcoTurn, priced at USD 180 since 2025, narrows the gap, yet split incentives between procurement and maintenance still slow adoption in India and Southeast Asia.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Manufacturing and Heavy Industries in Emerging Markets

- Stricter Workplace Safety and Machinery Regulations

- Technical Limits in High-Speed or Misaligned Applications

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Non-contact labyrinth formats, while still representing the 46.89% of the Bearing Isolators market in 2025, now serve mainly pumps and standard-speed motors. Compliance with ISO 16281:2025, which more harshly derates lip seals under contamination, is hastening the pivot toward magnetic forms. Magnetic architectures are advancing at a CAGR of 5.90% for the forecast period (2026-2031) and are increasingly preferred for high-speed turbines that demand zero wear. Combined-cycle gas-turbine operators find that Isomag's hybrid ceramic models extend service intervals to 60,000 hours.

Labyrinth, spiral-groove, and other specialized niches remain essential for cryogenic pumps and subsea drives where magnetic fluids or elastomers cannot survive extreme conditions. For misalignment-prone shafts, hybrid O-ring plus PTFE concepts such as John Crane's 8628VL tolerate 1.0 mm runout, broadening addressable installations.

Metallic (Bronze, Stainless, and Aluminum) designs held 50.87% share of the Bearing Isolators market size in 2025, led by bronze and stainless steel in corrosive oil-and-gas or pharma wash-down situations. Yet the composite/hybrid materials segment is on a 6.34% expansion trajectory for the forecast period (2026-2031). PEEK-reinforced PTFE achieved 60% lower wear in 2025 lab tests, accelerating wind-turbine adoption where nacelle weight savings translate to cost per kilowatt.

Bronze will remain the default for sour-gas or sulfuric-acid exposure until polymer chemistry matures further. Stainless 316L gained momentum after Parker Hannifin introduced an FDA (Food and Drug Administration)-compliant version that survives 150°C steam-sterilization cycles. Aluminum, 65% lighter than bronze, now replaces heavier units in ceiling-mounted HVAC retrofits.

Geography Analysis

Asia-Pacific held 40.78% of the Bearing Isolators market share in 2025 and will grow at 6.39% through 2031. China's output of 1.8 billion motors in 2024 provides both OEM (Original Equipment Manufacturer) and retrofit pull. India's 22% machinery-import rise and ASEAN's USD 226 billion FDI wave reinforce a pattern of design-stage isolator specification. ISO 17956:2025 adoption in Japan and South Korea further penalizes contact seals, accelerating regional transitions.

In North America, OSHA's 2025 guarding rule is nudging food and pharma plants to swap lip seals for NSF H1-rated isolators. Canadian oil-sands trials showed an 80% cut in bearing swaps after VBMag installations. Near-shoring in Mexico is fueling labyrinth-seal demand for cleanroom assembly conveyors.

Europe's market share in 2025 was anchored by offshore-wind uptake. System Seals' composite units now appear in 60% of new North Sea turbines. The revised 2006/42/EC directive's higher-speed trigger levels catalyze upgrades across Germany and France. Russia pivots to in-house designs amid supply-chain rifts. South America and MEA together represent less than 10% but show pockets of demand in mining, petrochemicals, and desalination.

- ABB

- Advanced Sealing International

- AESSEAL

- EagleBurgmann

- Flowserve Corporation

- Freudenberg Sealing Technologies

- Garlock (Enpro Inc.)

- Huhnseal AB

- Inpro/Seal

- ISOMAG Corporation

- John Crane

- NSK Ltd.

- Parker Hannifin Corp

- Schaeffler India Limited

- SEPCO Inc.

- SKF Group

- The Timken Company

- Trelleborg Marine and Infrastructure

- Trico Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for maintenance-free bearing protection

- 4.2.2 Increasing equipment uptime and reliability requirements

- 4.2.3 Expansion of manufacturing and heavy industries in emerging markets

- 4.2.4 Stricter workplace-safety and machinery regulations

- 4.2.5 Integration of shaft-grounding bearing isolators to prevent VFD-induced EDM damage

- 4.2.6 Additive-manufactured composite isolators for lightweight retrofits in renewable-energy turbines

- 4.3 Market Restraints

- 4.3.1 Higher initial cost vs contact seals

- 4.3.2 Technical limits in high-speed or mis-aligned applications

- 4.3.3 OEM shift to fully sealed "maintenance-free" motors reducing retrofit demand

- 4.3.4 Raw-material price volatility for copper-/nickel-based alloys

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Non-Contact Bearing Isolators

- 5.1.2 Hybrid (Contact + Non-Contact) Isolators

- 5.1.3 Magnetic Bearing Isolators

- 5.1.4 Labyrinth/Spiral-Groove/Other Specialized Designs

- 5.2 By Material

- 5.2.1 Metallic (Bronze, Stainless, and Aluminum)

- 5.2.2 Non-Metallic (PTFE, UHMWPE, and Elastomers)

- 5.2.3 Composite/Hybrid Materials

- 5.3 By Application

- 5.3.1 Pumps

- 5.3.2 Motors

- 5.3.3 Gearboxes

- 5.3.4 Compressors

- 5.3.5 Fans and Blowers

- 5.3.6 Turbines (Steam, Gas, and Wind)

- 5.3.7 Other Rotating Equipment (Conveyors, Mixers, and Agitators)

- 5.4 By End-user Industry

- 5.4.1 Oil and Gas

- 5.4.2 Chemical and Petrochemical

- 5.4.3 Power Generation

- 5.4.4 Water and Waste-water Treatment

- 5.4.5 Food and Beverage Processing

- 5.4.6 Pharmaceuticals and Life Sciences

- 5.4.7 Pulp and Paper

- 5.4.8 Mining and Metals

- 5.4.9 Manufacturing and Industrial Machinery

- 5.4.10 Marine, Transportation and HVAC

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (MandA, Partnerships, Product Launches)

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 ABB

- 6.4.2 Advanced Sealing International

- 6.4.3 AESSEAL

- 6.4.4 EagleBurgmann

- 6.4.5 Flowserve Corporation

- 6.4.6 Freudenberg Sealing Technologies

- 6.4.7 Garlock (Enpro Inc.)

- 6.4.8 Huhnseal AB

- 6.4.9 Inpro/Seal

- 6.4.10 ISOMAG Corporation

- 6.4.11 John Crane

- 6.4.12 NSK Ltd.

- 6.4.13 Parker Hannifin Corp

- 6.4.14 Schaeffler India Limited

- 6.4.15 SEPCO Inc.

- 6.4.16 SKF Group

- 6.4.17 The Timken Company

- 6.4.18 Trelleborg Marine and Infrastructure

- 6.4.19 Trico Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment