|

시장보고서

상품코드

2062331

캐스트 아크릴 시트 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Cast Acrylic Sheet - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

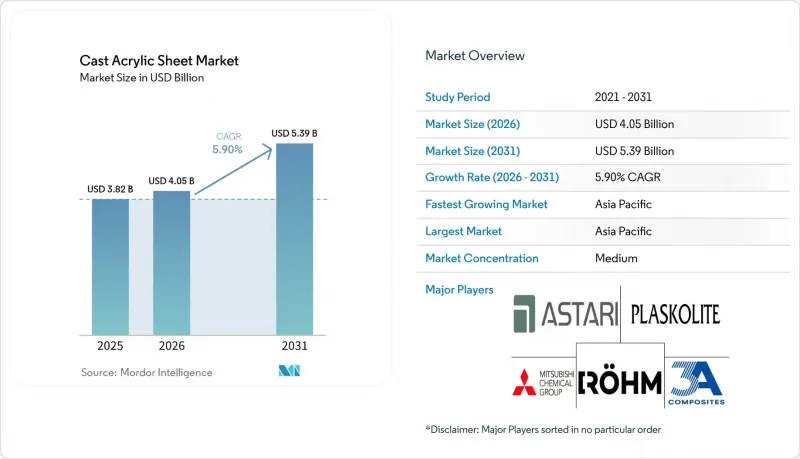

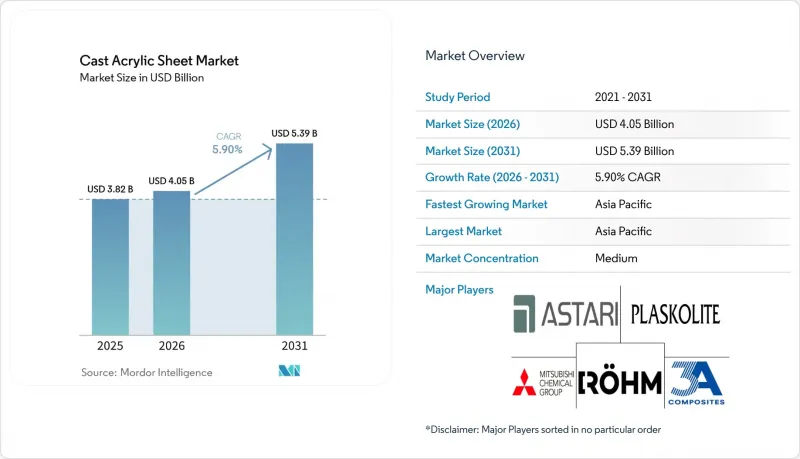

Mordor Intelligence에 의하면, 캐스트 아크릴 시트 시장 규모는 2025년 38억 2,000만 달러, 2026년 40억 5,000만 달러에서 2031년까지 53억 9,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 5.90%를 나타낼 것으로 예측됩니다.

본 보고서는 제품 유형(투명 캐스트 아크릴 시트, 착색 캐스트 아크릴 시트 등), 두께(5mm 이하, 5.1-10mm, 기타), 최종 사용자 산업(간판·디스플레이, 건축·인테리어 디자인, 기타), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

세계 캐스트 아크릴 시트 시장 동향 및 분석

간판 및 디스플레이 용도에서 수요 증가

캐스트 아크릴은 92-93%의 광투과율과 정확한 두께 공차를 제공하며, 에지 본딩 공정을 간소화할 수 있어 2025년 매출의 34.69%를 간판 및 디스플레이 용도가 차지했습니다. 아시아의 주요 소매 체인들은 내구성 기준을 충족하기 위해 기존의 PVC 보드에서 자외선 안정화 아크릴 제품으로 전환하고 있습니다. 광 확산 등급은 LED의 핫스팟 현상을 해소하여 디지털 사이니지 캐비닛의 성장을 뒷받침하고 있습니다. 수요는 안정적이며, 현재는 초기 도입 단계에서 반사 방지 및 항균 코팅을 적용한 정기적인 개보수 단계로 전환되고 있습니다. 버스 정류장 지붕과 같이 내충격성이 요구되는 용도에서는 여전히 폴리카보네이트가 선호되는 소재이지만, 내파괴성보다 광학적 투명성이 우선시되는 분야에서는 아크릴이 주류를 이루고 있습니다.

건설 및 자동차 분야에서의 유리 대체 확대

유리의 절반에 해당하는 밀도를 가진 캐스트 아크릴은 파사드의 포인트 장식, 채광창용 디퓨저, 전기차 선루프 등의 용도에서 자중을 줄여줍니다. DURAPLEX와 같은 내충격성 개선 제품은 일반 시트에 비해 10배의 내충격성을 제공하여, 각 OEM 업체들의 사이드 글레이징 컨셉에 대한 관심을 다시금 높이고 있습니다. 건축 일체형 태양광 발전(BIPV)에서는 구조용 강재의 무게를 늘리지 않으면서 모듈을 보호하기 위해 아크릴 재질의 2차 유리가 점점 더 많이 지정되고 있습니다. 유럽에서 탄소 내재량(제조 과정에서의 탄소 배출량) 공개가 도입의 추진력을 약화시키고 있습니다. 이는 캐스트 PMMA의 탄소 발자국이 4.77 kg CO2-eq/kg으로, 압출 성형 시트보다 27% 높은 수치이기 때문입니다. 그럼에도 불구하고, 장기적인 경량화와 설계의 유연성이 그 도입을 지속적으로 뒷받침하고 있습니다.

MMA 및 기타 원자재 가격 변동

2026년 2월 MMA 현물 가격은 1kg당 1.52-1.79달러 범위에서 형성되어, 중견 시트 제조업체의 전형적인 8-12%라는 본래 좁은 EBITDA 마진에 타격을 주었습니다. 2025년 미쓰비시 화학이 루이지애나주에 연산 35만 톤 규모의 복합 시설 건설을 중단함에 따라, 북미 시장의 잠재적 공급 완충 기능이 사라지게 되었습니다. 화학 재활용 원료는 원유 가격 지표에 대한 의존도가 낮은 대체 MMA 공급원을 창출함으로써 부분적인 헤지 효과를 가져옵니다.

부문별 분석

특수 등급은 2031년까지 연평균 성장률(CAGR) 6.68%를 나타낼 것으로 예측되며, 캐스트 아크릴 시트 시장에 큰 부가가치를 창출할 전망입니다. 투명 캐스트 아크릴 시트는 간판 용도로의 꾸준한 수요에 힘입어 2025년에는 36.87%의 시장 점유율을 차지했습니다. 착색, 패턴, 텍스처 가공 등 다양한 제품은 장식 분야의 틈새 시장을 충족시킵니다. 내충격성 개질 DURAPLEX 시트는 모빌리티 및 기계 보호 분야에서 새로운 기회를 창출하고 있으며, 한편 광확산성 배합은 LED 조명 기구의 효율을 향상시킵니다. 바이오 수지공급 안정성은 프리미엄 가격 전략을 뒷받침하고 있습니다. 또한, 내충격성 코어를 스크래치 방지 캡으로 감싼 공압출 필름 라미네이트 제품도 성장을 주도하고 있으며, 고급 자동차 내장재 시장 수요를 충족시키고 있습니다.

고성능 기능에 대한 수요가 증가함에 따라, 5,000시간의 Q-UV 조사 후에도 광투과율 92-93%, Delta b<=2를 유지하는 첨가제 패키지의 특허 획득을 둘러싸고 공급업체 간의 경쟁이 치열해지고 있습니다. 사내 컬러 매칭 센터, 디지털 트윈 배합 도구 및 급속 열사이클 성형 기술을 통해 개발 주기가 단축되고 OEM과의 관계가 강화되고 있습니다. 이러한 동향은 캐스트 아크릴 시트 시장이 일반 상품 중심의 접근 방식에서 솔루션 지향적인 방향으로 전환되고 있음을 보여줍니다.

지역별 분석

아시아태평양은 2025년 매출의 48.02%를 차지하며, 2026년 7월 발효될 산업 폐기물 유래 재분쇄 원료의 합법화를 규정한 재생 PMMA 기준에 힘입어 2031년까지 연평균 성장률(CAGR) 7.18%로 성장할 전망입니다. 중국의 제조업체들은 MMA의 수직 통합과 대용량 블록 캐스트를 결합하여 수족관 메가 프로젝트에 대응하고 있습니다. 한편, 일본과 한국은 전자기기의 백라이트용으로 특수한 광확산 등급을 선호하여 채택하고 있습니다. 인도는 연간 5,000톤에 불과한 제한된 국내 MMA 생산 능력으로 인해 수입에 의존할 수밖에 없지만, 인프라 지출 증가로 인해 간판 및 건축 관련 수주가 늘어나면서 남아시아의 캐스트 아크릴 시트 시장을 공고히 하고 있습니다.

북미에서는 플라스코라이트의 마타모로스 공장 인수와 로옴의 월링포드 공장 확장을 통해 공급망이 단축되고, 특수 등급 제품에 대한 대응 능력이 향상되었습니다. 그러나 미쓰비시 화학의 루이지애나주 MMA 프로젝트가 무산되면서 원료 부족 사태는 계속되고 있습니다. 기업들의 지속가능성 노력으로 인해 비중합 MMA에 대한 관심이 높아지면서, 원자재 공급난에도 불구하고 향후 캐스트 아크릴 시트 시장의 성장을 뒷받침하고 있습니다.

유럽에서는 로옴이 황산 자급 체제를 재개하고, 에보닉이 세계 최대 규모의 PMMA 공압출 라인을 가동함에 따라 독일이 지역 내 공급을 주도하고 있습니다. 그린 딜의 수명 주기 요건으로 인해 탄소 배출량이 높은 소재는 어려움을 겪고 있지만, 화학 재활용 시범 라인 및 바이오 MMA에 대한 합의가 지역 캐스트 아크릴 시트 시장의 성장을 뒷받침하고 있습니다. 지중해 지역의 요트 및 수족관 건설 수요는 두꺼운 판재 수요를 견조하게 유지하며, 동유럽의 산업 생산 부진을 상쇄하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the cast acrylic sheet market size is projected to expand from USD 3.82 billion in 2025 and USD 4.05 billion in 2026 to USD 5.39 billion by 2031, registering a CAGR of 5.90% between 2026 to 2031.

This report is Segmented by Product Type (Clear Cast Acrylic Sheet, Colored Cast Acrylic Sheet, and More), Thickness (Less Than or Equal To 5 Mm, 5. 1-10 Mm, and More), End-User Industry (Signage and Display, Architecture and Interior Design, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Global Cast Acrylic Sheet Market Trends and Insights

Growing Demand in Signage and Display Applications

Signage and display applications accounted for 34.69 of the 2025 revenue, as cast acrylic offers 92-93% light transmission and precise thickness tolerance, simplifying edge bonding. Large retail chains in Asia are transitioning from traditional PVC boards to UV-stabilized acrylic formats to comply with durability standards. Light-diffusing grades eliminate LED hot-spotting, supporting the growth of digital signage cabinets. Demand has stabilized and is now shifting from initial installations to scheduled refurbishments that incorporate anti-reflective and antimicrobial coatings. While polycarbonate remains the preferred material for high-impact applications like bus shelters, acrylic dominates in areas where optical clarity is prioritized over vandal resistance.

Increased Glass Substitution in Construction and Automotive

At half the density of glass, cast acrylic reduces dead loads in applications such as facade accents, skylight diffusers, and electric vehicle sunroofs. Impact-modified variants like DURAPLEX provide tenfold greater resistance compared to general-purpose sheets, renewing OEM interest in side-glazing concepts. Building-integrated photovoltaics increasingly specify acrylic secondary glazing to protect modules without adding structural steel weight. European embodied-carbon disclosures have slowed momentum, as cast PMMA has a carbon footprint of 4.77 kg CO2-eq/kg, which is 27% higher than extruded sheets. Nevertheless, long-term weight savings and design flexibility continue to support its adoption.

Volatility in MMA and Other Raw-Material Prices

Spot MMA prices ranged between USD 1.52 and USD 1.79 per kg in February 2026, impacting the already narrow EBITDA margins of 8-12% typical for mid-scale sheet producers. The cancellation of Mitsubishi Chemical's 350-ktpa Louisiana complex in 2025 removed a potential supply buffer for North American markets. Chemical-recycling feedstock provides a partial hedge by creating alternative MMA streams that are less dependent on crude oil benchmarks.

Other drivers and restraints analyzed in the detailed report include:

- Rise of PoS Protective Screens Post-COVID

- Sustainability Repositioning Through Bio-Based MMA Supply

- High-Impact Substitutes (Polycarbonate, PETG)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Specialty grades are anticipated to grow at a CAGR of 6.68% through 2031, adding significant value to the cast acrylic sheet market. Clear cast acrylic sheets held a 36.87% market share in 2025, driven by their established use in signage applications. Colored, patterned, and textured variants cater to decorative niches. Impact-modified DURAPLEX sheets create opportunities in mobility and machine-guard applications, while light-diffusing formulations improve LED luminaire efficiency. The availability of bio-based resins supports premium pricing strategies. Growth is also driven by co-extruded film laminates that incorporate scratch-resistant caps around impact cores, addressing demand in premium automotive interiors.

Demand for performance features has intensified competition among suppliers to patent additive packages that maintain 92-93% light transmission and Delta b<= 2 after 5,000 hours of Q-UV exposure. In-house color-matching centers, digital twin formulation tools, and rapid-heat-cycle mold technologies are reducing development cycles and strengthening OEM relationships. These trends reinforce the cast acrylic sheet market's transition from a commodity-based approach to a solution-oriented focus.

Geography Analysis

Asia-Pacific generated 48.02% of 2025 revenue and is poised for a 7.18% CAGR through 2031, supported by recycled-PMMA standards effective July 2026 that legalize post-industrial regrind feedstock. Chinese producers combine vertical MMA integration and high-capacity block casting to service aquarium megaprojects, while Japan and South Korea favor specialty light-diffusing grades for electronics backlights. India's limited 5 ktpa domestic MMA base compels import dependence, yet rising infrastructure spend lifts signage and architectural orders and fortifies the cast acrylic sheet market in South Asia.

In North America, Plaskolite's acquisition of the Matamoros facility and Rohm's Wallingford expansion shorten supply chains and provide specialty-grade agility. The loss of Mitsubishi Chemical's Louisiana MMA project, however, sustains feedstock tightness. Corporate sustainability pledges accelerate interest in depolymerized MMA, supporting future cast acrylic sheet market expansion despite raw-material headwinds.

In Europe, Germany leads regional supply after Rohm reinstated sulfuric-acid self-sufficiency and Evonik started the world's widest PMMA co-extrusion line. Green-Deal life-cycle mandates challenge high-embodied-carbon materials, yet pilot chemical-recycling lines and bio-based MMA agreements help safeguard regional cast acrylic sheet market growth. Mediterranean yacht and aquarium builds maintain steady thick-sheet demand, balancing weaker industrial output in Eastern Europe.

- 3A Composites GmbH

- Aristech Surfaces LLC

- Asia Poly Holdings Berhad

- Atoglas (Arkema)

- Cosmo Industrial Products Pvt. Ltd.

- Evonik Industries AG

- Madreperla SpA

- Margacipta

- Mitsubishi Chemical Infratec Co.,Ltd.

- Olida Ltd.

- Plaskolite

- POLYVANTIS GmbH

- PT Astari Niagara Internasional

- Roehm Chemical (Shanghai) Co., Ltd.

- Rohm GmbH

- Shaktiacryplast

- SHING FU ENTERPRISE CO., LTD.

- Simona AG

- Spartech LLC

- Taixing Donchamp Acrylic

- Trinseo

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand in signage and display applications

- 4.2.2 Increased glass substitution in construction and automotive

- 4.2.3 Rise of PoS protective screens post-COVID

- 4.2.4 Secondary glazing for BIPV and utility-scale solar farms

- 4.2.5 Premium aquaculture viewing tanks adoption

- 4.2.6 Sustainability repositioning through bio-based MMA supply

- 4.3 Market Restraints

- 4.3.1 Volatility in MMA and other raw-material prices

- 4.3.2 High-impact substitutes (polycarbonate, PETG)

- 4.3.3 Embodied-carbon scrutiny versus glass and PET

- 4.3.4 Tightening solvent-VOC emission standards in Asia

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Clear Cast Acrylic Sheet

- 5.1.2 Colored Cast Acrylic Sheet

- 5.1.3 Patterned/Textured Cast Acrylic Sheet

- 5.1.4 Specialty Grades

- 5.1.4.1 UV-resistant

- 5.1.4.2 Anti-static

- 5.1.4.3 Impact-modified

- 5.1.4.4 Light-diffusing

- 5.2 By Thickness

- 5.2.1 Less than or equal to 5 mm

- 5.2.2 5.1 - 10 mm

- 5.2.3 10.1 - 20 mm

- 5.2.4 Greater than 20 mm (Block)

- 5.3 By End-user Industry

- 5.3.1 Signage and Display

- 5.3.2 Architecture and Interior Design

- 5.3.3 Automotive and Transportation

- 5.3.4 Furniture and Design

- 5.3.5 Medical and Life Sciences

- 5.3.6 Marine and Leisure

- 5.3.7 Solar and Renewable Energy

- 5.3.8 Aquaculture and Aquariums

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3A Composites GmbH

- 6.4.2 Aristech Surfaces LLC

- 6.4.3 Asia Poly Holdings Berhad

- 6.4.4 Atoglas (Arkema)

- 6.4.5 Cosmo Industrial Products Pvt. Ltd.

- 6.4.6 Evonik Industries AG

- 6.4.7 Madreperla SpA

- 6.4.8 Margacipta

- 6.4.9 Mitsubishi Chemical Infratec Co.,Ltd.

- 6.4.10 Olida Ltd.

- 6.4.11 Plaskolite

- 6.4.12 POLYVANTIS GmbH

- 6.4.13 PT Astari Niagara Internasional

- 6.4.14 Roehm Chemical (Shanghai) Co., Ltd.

- 6.4.15 Rohm GmbH

- 6.4.16 Shaktiacryplast

- 6.4.17 SHING FU ENTERPRISE CO., LTD.

- 6.4.18 Simona AG

- 6.4.19 Spartech LLC

- 6.4.20 Taixing Donchamp Acrylic

- 6.4.21 Trinseo

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment