|

시장보고서

상품코드

2062339

수동적 방화 코팅 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Passive Fire Protection Coating - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

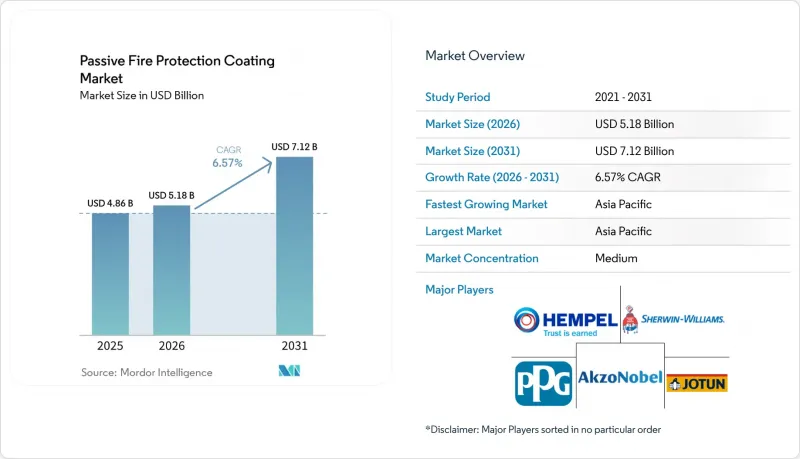

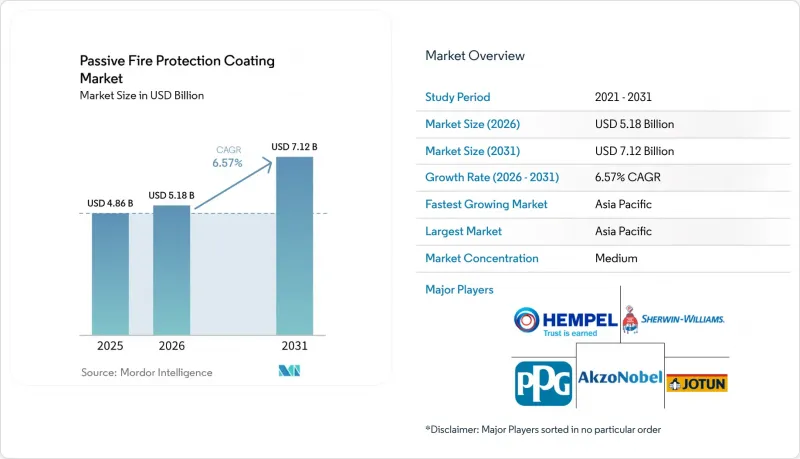

Mordor Intelligence에 의하면, 수동적 방화 코팅 시장 규모는 2025년 48억 6,000만 달러로 평가되었고, 2026년에는 51억 8,000만 달러로 추정되고, 2026-2031년 CAGR 6.57%로 성장을 지속할 전망이며, 2031년까지 71억 2,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 코팅 유형별(팽창성 코팅 등), 기술별(용제계 등), 기판별(콘크리트 등), 화재 시나리오별(셀룰로오스계 방화 등), 최종 사용자 산업별(석유 및 가스 등), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 수동적 방화 코팅 시장 동향 및 분석

상업 및 산업용 부동산에 적용되는 엄격한 방화 규제

각국 정부는 성능 기준에 기반한 건축 기준을 점점 더 많이 채택하고 있으며, 도료에 대한 제3자 인증을 의무화하고, 자산 소유자에 대한 규정 준수 기한을 단축하고 있습니다. 2025년 12월, 영국은 BS 476에서 BS EN 13501-1로 전환하여, 높이 18미터를 초과하는 구조물에서 가연성 외장재 사용을 사실상 금지함으로써 유로클래스 인증을 받은 팽창성 도료에 대한 수요를 촉진했습니다. 인도의 ‘2024년 국가 건축 기준’에 따르면, 높이 15미터를 초과하는 상업용 건물에는 IS 3809 시험을 통과한 도료의 사용이 의무화되어 있으며, 뭄바이와 방갈로르에서는 총 120만 제곱미터 규모의 사무실 공간에서 개보수 공사가 진행되고 있습니다. 2027년 3분기에 발효될 유럽연합(EU)의 개정 건설제품 규정에서는 국제표준화기구(ISO) 17025 인증을 받은 성능 선언이 의무화되며, 중소 공급업체에는 중대한 부적합에 대한 제재가 부과될 것입니다. 캘리포니아주에서는 선구적인 기업들이 건축용 도료의 휘발성 유기화합물(VOC) 함량을 1리터당 50그램으로 제한하는 ‘규칙 1113’의 2025년 개정안에 대응하고 있습니다. 이러한 규제가 확산됨에 따라, 초박형이며 VOC가 전혀 포함되지 않은 에폭시 도료가 수동적 방화 코팅 입찰에서 표준으로 자리 잡고 있습니다.

세계의 고층 빌딩 및 공공 인프라의 급속한 건설 확대

신흥 시장의 도시화를 배경으로, 높이 300미터를 넘는 초고층 건물이 사상 최대 속도로 건설되고 있어, 3시간 동안 탄화수소에 노출되어도 내구성을 유지하는 도료가 필요해지고 있습니다. 2025년, 중국에서는 높이 200미터를 넘는 87동의 빌딩이 완공되었으며, 각 건물의 철골 기둥에는 약 1만 2,000제곱미터의 팽창성 필름이 사용되었습니다. 인도의 지하철 확장 계획에서는 연기 확산을 억제하기 위해 지하 승강장에 UL 263 규격을 준수하는 도료의 사용을 의무화하고 있습니다. 공항, 항만, 6개 신도시에 걸쳐 1조 3,000억 달러 규모의 인프라 계획을 추진 중인 걸프협력회의(GCC)는 주요 자재에 2시간의 내화 성능을 요구하는 아랍에미리트(UAE)의 방화 및 생명 안전 기준을 준수하고 있습니다. 이러한 프로젝트들은 수동적 방화 코팅 시장을 견인하고 있으며, 턴키 방식의 설계·조달·시공(EPC) 계약에서 엄격한 내화 성능에 관한 조항이 일반화되고 있습니다. 도급업체들이 일괄 도급 입찰에 코팅 공정을 포함시키는 사례가 늘어나고 있어, 조달 프로세스는 효율화되는 반면 품질 보증에 드는 비용은 증가하고 있습니다.

기존 외장재에 비해 높은 시공 비용

시공이 완료된 팽창성 방화 시스템은 1제곱미터당 35-85달러가 드는 반면, 내화 성능이 없는 회반죽은 15-30달러입니다. 이러한 비용 차이는 자산 가치 대비 화재 보험 가입률이 15% 미만인 지역에서 구매 결정에 영향을 미치고 있습니다. 선진국 시장에서는 총 비용의 최대 65%를 인건비가 차지하고 있습니다. 또한, 전미부식기술자협회(NACE) 또는 부식방지도장협회(SSPC)의 인증 시공업체 부족으로 인해 미국 및 서유럽에서는 프로젝트 인도 시기가 4-6주 지연되고 있습니다. 남아시아에서는 2023년부터 2025년에 걸쳐 연간 임금 상승률이 8%를 넘어설 것으로 예상에 따라, 스프링클러의 평생 유지비가 40% 더 비싸음에도 불구하고 많은 개발업자들이 코팅 대신 스프링클러를 선택하고 있습니다.

부문별 분석

2025년, 팽창성 도료는 매출의 43.78%를 차지했으며, 시멘트계 제품의 무게의 불과 10분의 1에 불과한 무게로 60-180분의 내화 성능을 달성했습니다. 이러한 장점은 추가적인 사하중을 제한하는 것을 목적으로 하는 내진 보강 공사에서 중요합니다. 소형 베이스, 하이브리드 제품 및 나노 강화 필름은 팽창성과 소손 열흡수 기능을 결합한 이중 보호 메커니즘 덕분에 연평균 성장률(CAGR) 6.87%로 성장할 것으로 전망됩니다. 이전에는 저렴한 가격 덕분에 선호되던 시멘트계 층은 두께가 25mm에 달하고, 유효 바닥 면적을 줄이고 HVAC(난방, 환기, 공조) 배관을 복잡하게 만든다는 이유로 시장 점유율을 점차 잃어가고 있습니다. 아브레이티브 소재는 여전히 틈새 시장으로 남아 있으며, 최대 열유속이 200kW/제곱미터(kW/m²)를 초과하는 항공우주 및 해군 구획에 공급되고 있습니다.

수성 팽창성 도료는 캘리포니아주가 2025년부터 1리터당 50그램(g/L)이라는 휘발성 유기화합물(VOC) 상한선을 정함에 따라 보급이 확대되었습니다. 현재는 고층 빌딩의 시공 규격에서 표준으로 자리 잡았으며, 호흡용 보호구를 착용하지 않고도 시공할 수 있습니다. Jotun사의 Steelmaster 1200WF는 건조 필름 두께(DFT) 1,350 마이크로미터(µm)로 ICC-ES AC23 규격을 충족하며, 친환경적인 화학 성분으로도 엄격한 성능 기준을 충족할 수 있음을 입증하고 있습니다. 이러한 발전은 이익률 향상과 시공 시간 단축으로 이어져, 수동적 방화 코팅 시장 전망에 긍정적인 영향을 미치고 있습니다.

2025년 기준, 용제계 시스템은 시장의 34.88%를 차지했으며, 특히 금속 표면과 거의 같은 상태까지 블라스팅 처리를 수행하기 어려운 보수 공사에서 채택되고 있습니다. 그러나 100% 고형분 에폭시 도료는 VOC가 전혀 없습니다는 특성과 사람이 거주하는 건물에서 시공 당일부터 사용을 재개할 수 있다는 장점 덕분에, 2031년까지 연평균 성장률(CAGR) 7.22%로 성장할 전망입니다. 수성 도막은 습도가 높은 지역에서 여러 가지 문제에 직면하고 있습니다. 상대습도(RH)가 80%에 도달하면 경화에 72시간 이상이 소요되고, 비로 인해 유실될 위험이 발생하기 때문입니다. 한편, 분체 도료나 자외선(UV) 경화형은 자동차 서브프레임이나 조립식 강철 모듈에 사용되는 공장 라인으로 한정되어 있으며, 정전기 도장 부스나 UV 램프와 같은 설비 투자의 타당성이 입증되고 있습니다.

2026년 1월부터 유럽연합(EU)의 산업 배출 지침에 따라, 열산화 장치를 갖추지 않은 경우 VOC 배출량이 50밀리그램/표준입방미터(mg/N m3)를 초과하는 가동이 금지됩니다. 열산화 장비를 도입하는 데는 20만-50만 유로(23만-58만 달러)의 비용이 듭니다. 이 규제로 인해 업계는 고형분 함량 80% 이상의 도료로 전환해야 하는 상황에 놓여 있습니다. PPG사는 2029년까지 이러한 고고형분 등급 제품이 유럽 수요의 55%를 차지할 것으로 전망하고 있으며, 이는 수동적 방화 코팅 시장에서 해당 기업의 입지를 공고히할 것입니다.

지역별 분석

2025년, 아시아태평양은 매출의 37.43%를 차지한 것으로 평가되었으며, 2031년까지 연평균 성장률(CAGR) 7.21%로 성장할 전망입니다. 중국은 제14차 5개년 계획에 따라 도시 재생에 2조 7,000억 위안(3,800억 달러)을 배정했습니다. 한편, 인도의 ‘스마트 시티 미션’에서는 100개 지자체에서 방화 기준 강화가 추진되고 있습니다. 2025년 4월부터 일본에서는 높이 31미터를 초과하는 건물에 팽창성 도료의 사용이 의무화됩니다. 2026년 1월부터는 한국의 그린빌딩 인증에서 3시간의 수동적 방화 성능에 대한 가산점 제도가 도입됨에 따라, 민간 개발사들이 고급 에폭시 수지를 채택하는 추세가 확대되고 있습니다. 이러한 노력을 통해 아시아태평양 지역은 수동적 방화 코팅 시장에서 선도적인 입지를 확고히 하고 있습니다.

북미에서는 숙련된 노동력 부족으로 인해 성장에 어려움이 발생하고 있으며, 시공 비용이 15-22% 상승하고 프로젝트 공사 기간이 최대 6주 연장되고 있습니다. 그럼에도 불구하고, 1,100억 달러 규모의 ‘인프라 투자 및 고용법’에 따라 18,000개의 교량과 12,000개의 교통 기관 역에 대한 도료 자금이 배정되어, 18억-24억 달러 규모의 안정적인 수요가 확보되고 있습니다. 캐나다에서는 2025년 건축 기준 개정에 따라 6층을 초과하는 목조 건축물에 대해 2시간의 내화 성능이 의무화됨에 따라, 브리티시컬럼비아주와 온타리오주에서 판매가 급증하고 있습니다. 또한, 멕시코의 마키라도라(수출가공구역)에서는 가연성 물품을 취급하는 창고에 대해 언더라이터스 래버러토리즈(UL) 263 규격의 도료 사용이 의무화되어, 해당 지역에서의 도입이 확대되고 있습니다.

유럽, 중동 및 아프리카에서는 다양한 동향이 나타나고 있습니다. 유럽연합(EU)이 2027년 3분기에 시행할 예정인 건설제품규정(CPR) 개정에 따라 제품별 규정 준수 비용이 증가할 것으로 예상되며, 국제표준화기구(ISO) 17025 인증을 받은 시험소를 보유한 기업이 유리한 입장에 설 것으로 보입니다. 걸프협력회의(GCC)에서는 1조 3,000억 달러 규모의 프로젝트 계획에 따라 모든 신규 터미널에 2시간의 내화 성능이 의무화됨에 따라, 두바이와 아부다비의 도료 수입량이 23% 급증하고 있습니다. 반면, 사하라 이남 아프리카에서의 도입은 제한적입니다. 건물 가치의 10% 미만이 화재 보험으로 보장되고 있으며, 주요 도시 이외의 지역에서는 건축 기준이 미흡하기 때문에 수동적 방화 코팅 시장은 주로 정부 자금을 지원받는 병원이나 통신 허브로 한정되어 있습니다.

남미에서는 상황이 제각각입니다. 브라질에서는 2025년 3월부터 시행되는 건축 기준에 따라, 높이 23미터를 초과하는 주거용 고층 건물에 수동적 방화 장벽을 설치해야 하며, 이로 인해 1만 8,000동의 건물이 영향을 받을 것으로 예측됩니다. 아르헨티나에서는 부에노스아이레스의 석유화학 시설이 아르헨티나 표준화 인증 협회(IRAM)의 11910호 탄화수소 기준을 충족하도록 개보수 작업이 진행되고 있습니다. 칠레의 내진 강화 계획에 따르면, 2030년까지 21억 달러를 팽창성 방화재 교체에 투입할 방침입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the passive fire protection coating market size is expected to grow from USD 4.86 billion in 2025 to USD 5.18 billion in 2026 and is forecast to reach USD 7.12 billion by 2031 at 6.57% CAGR over 2026-2031.

This report is Segmented by Coating Type (Intumescent Coatings and More), Technology (Solvent-Based and More), Substrate (Concrete, and More), Fire Scenario (Cellulosic Fire Protection and More), End-User Industry (Oil and Gas and More), Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Passive Fire Protection Coating Market Trends and Insights

Stringent Fire-Safety Regulations In Commercial & Industrial Real Estate

Governments are increasingly adopting performance-based codes, mandating third-party certification of coatings and shortening compliance timelines for asset owners. In December 2025, the United Kingdom transitioned from BS 476 to BS EN 13501-1, effectively prohibiting combustible cladding on structures exceeding 18 meters and driving demand for Euroclass-rated intumescents. India's National Building Code 2024 mandates IS 3809-tested coatings for commercial buildings over 15 meters, leading to retrofits across 1.2 million square meters of office space in Mumbai and Bengaluru. The European Union's updated Construction Products Regulation, effective Q3 2027, requires International Organization for Standardization (ISO) 17025-verified performance declarations, imposing significant non-compliance penalties on smaller suppliers. In California, early adopters are addressing 2025 amendments to Rule 1113, capping volatile organic compound (VOC) content at 50 grams per liter for architectural coatings. As these regulations gain traction, ultra-thin, zero-VOC epoxies are becoming standard in passive fire protection coating bids.

Rapid Build-Out Of High-Rise & Public Infrastructure Worldwide

Urbanization in emerging markets is driving the construction of record numbers of super-tall structures exceeding 300 meters, necessitating coatings with three-hour hydrocarbon exposure ratings. In 2025, China completed 87 buildings, surpassing 200 meters, each utilizing approximately 12,000 square meters of intumescent film on steel columns. India's metro-rail expansion mandates Underwriters Laboratories (UL) 263-compliant coatings for underground platforms to curb smoke spread. The Gulf Cooperation Council, with a USD 1.3 trillion infrastructure agenda spanning airports, seaports, and six new cities, adheres to the United Arab Emirates Fire and Life Safety Code, which demands two-hour resistance for primary members. Such projects are bolstering the passive fire protection coating market, with stringent fire-rating clauses now common in turnkey Engineering, Procurement, and Construction (EPC) contracts. Contractors are increasingly integrating coatings into lump-sum bids, streamlining procurement but raising quality-assurance expenses.

High Installed Cost Versus Conventional Cladding

Fully installed intumescent systems cost USD 35-85/m2 compared to USD 15-30/m2 for unrated plaster, representing a cost difference that impacts purchasing decisions in regions where fire insurance penetration is below 15% of asset value. In developed markets, labor accounts for up to 65% of the total cost. Additionally, a shortage of National Association of Corrosion Engineers (NACE) or Society for Protective Coatings (SSPC)-certified applicators has extended project handover timelines by four to six weeks in the United States and Western Europe. In South Asia, annual wage inflation exceeding 8% between 2023 and 2025 has prompted many developers to choose sprinklers over coatings, despite the 40% higher lifetime maintenance costs associated with sprinklers.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of Oil, Gas & Power Assets Including LNG

- Advances In Ultra-Thin Epoxy-Intumescent Formulations

- Performance Degradation In Humid, UV-Rich Or Cryogenic Settings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Intumescents accounted for 43.78% of the revenue, achieving 60-180 minute ratings with just a tenth of the weight of cementitious products. This advantage is significant for seismic retrofits, which aim to limit added dead load. While starting from a smaller base, hybrids and nano-enhanced films are set to grow at a projected 6.87% compound annual growth rate (CAGR), due to their dual-mechanism protection that combines intumescence with ablative heat absorption. Cementitious layers, previously preferred for their low price, are losing ground due to their 25 mm thickness, which reduces usable floor space and complicates HVAC (heating, ventilation, and air conditioning) routing. Ablatives remain niche, catering to aerospace and naval compartments where peak heat flux surpasses 200 kilowatts per square meter (kW/m2).

Water-based intumescents gained traction following California's 2025 volatile organic compound (VOC) cap of 50 grams per liter (g/L). They are now standard in high-rise specifications, allowing application without respirators. Jotun's Steelmaster 1200WF, achieving ICC-ES AC23 compliance at 1,350 micrometers (µm) dry film thickness (DFT), demonstrates that eco-friendly chemistry can meet stringent performance standards. Such advancements improve profit margins and reduce installation time, positively influencing the market outlook for passive fire protection coatings.

In 2025, solvent-borne systems captured 34.88% of the market, especially in refurbishment jobs where near-white-metal blasting isn't feasible. However, 100% solids epoxies are on track for a 7.22% CAGR through 2031, driven by their zero-VOC credentials and the ability to return to service on the same day in occupied buildings. Water-based films face challenges in humid areas, where 80% relative humidity (RH) can extend curing beyond 72 hours, risking rain washout. Meanwhile, powder and ultraviolet (UV)-cured variants are limited to factory lines, used for automotive subframes and prefabricated steel modules, justifying their capital expenditure with electrostatic booths and UV lamps.

Starting January 2026, the European Union (EU) Industrial Emissions Directive will ban operations emitting over 50 milligrams per normal cubic meter (mg/N m3) VOC without thermal oxidizers, which come with a price tag of EUR 0.2-0.5 million (USD 0.23-0.58 million). This regulation is pushing the industry towards greater than or equal to 80% volume-solids chemistry. PPG forecasts that by 2029, these high-solids grades will make up 55% of European demand, solidifying their position in the passive fire protection coating market.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 37.43% of the revenue and is set to grow at a 7.21% Compound Annual Growth Rate (CAGR) through 2031. Under its 14th Five-Year Plan, China allocated CNY 2.7 trillion (USD 380 billion) for urban renewal. Meanwhile, India's Smart Cities Mission is enhancing fire codes in 100 municipalities. Starting April 2025, Japan will require intumescent coatings on buildings taller than 31 meters. In January 2026, South Korea's Green Building Certification introduced bonus points for three-hour passive protection, encouraging private developers to opt for premium epoxies. These initiatives position the Asia-Pacific region as a leader in the passive fire protection coating market.

North America's growth faces challenges due to a skilled labor shortage, leading to a 15-22% increase in installation costs and extending project timelines by up to six weeks. Nevertheless, the USD 110 billion Infrastructure Investment and Jobs Act allocates funds for coatings on 18,000 bridges and 12,000 transit stations, ensuring a consistent demand valued between USD 1.8-2.4 billion. In Canada, a 2025 code update mandates two-hour ratings for timber buildings exceeding six stories, resulting in a sales surge in British Columbia and Ontario. Additionally, Mexico's maquiladora corridors now require Underwriters Laboratories (UL) 263 coatings for warehouses handling flammable goods, broadening the regional adoption.

Europe, the Middle East, and Africa are witnessing varied developments. The European Union's (EU) Q3 2027 Construction Products Regulation (CPR) revision is set to elevate compliance costs per product, favoring firms equipped with International Organization for Standardization (ISO) 17025 laboratories. In the Gulf Cooperation Council (GCC), a USD 1.3 trillion pipeline mandates two-hour ratings for all new terminals, leading to a 23% spike in coating imports in Dubai and Abu Dhabi. Conversely, Sub-Saharan Africa's adoption is limited; with fire insurance covering under 10% of building values and weak codes outside major capitals, the market for passive fire protection coatings is largely confined to government-funded hospitals and telecom hubs.

South America sees a mix of developments. Brazil's code, effective March 2025, mandates passive barriers on residential towers exceeding 23 meters, impacting 18,000 buildings. In Argentina, Buenos Aires petrochemical sites are being retrofitted to meet Instituto Argentino de Normalizacion y Certificacion (IRAM) 11910 hydrocarbon standards. Chile's seismic resilience initiative is directing USD 2.1 billion towards intumescent upgrades until 2030.

- 3M

- Akzo Nobel N.V.

- BASF

- Contego International Inc.

- Etex Group

- Firefree Coatings, Inc.

- Hempel A/S

- Hilti Group

- Isolatek International

- Isolatek International

- Jotun

- Kansai Paint Co., Ltd.

- Morgan Advanced Materials plc

- No-Burn, Inc.

- PPG Industries, Inc.

- RPM International Inc.

- Sika AG

- Teknos Group

- The Sherwin-Williams Company

- Tremco Incorporated

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent fire-safety regulations in commercial & industrial real-estate

- 4.2.2 Rapid build-out of high-rise & public infrastructure worldwide

- 4.2.3 Expansion of oil, gas & power assets (including LNG)

- 4.2.4 Advances in ultra-thin epoxy-intumescent formulations

- 4.2.5 Digital-twin & sensor-embedded PFP systems enabling predictive maintenance

- 4.3 Market Restraints

- 4.3.1 High installed cost versus conventional cladding

- 4.3.2 Performance degradation in humid, UV-rich or cryogenic settings

- 4.3.3 Supply-chain volatility for phosphorus-based flame-retardant feedstocks

- 4.3.4 Regulatory uncertainty around nano-additive ecotoxicity

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Coating Type

- 5.1.1 Intumescent Coatings

- 5.1.2 Cementitious Coatings

- 5.1.3 Ablative Coatings

- 5.1.4 Hybrid/Nano-enhanced Coatings

- 5.2 By Technology

- 5.2.1 Solvent-based

- 5.2.2 Water-based

- 5.2.3 100%-Solids Epoxy

- 5.2.4 Powder & UV-cured

- 5.3 By Substrate

- 5.3.1 Structural Steel

- 5.3.2 Concrete

- 5.3.3 Wood

- 5.3.4 Other Substrates (Plastics, Cables, Composites)

- 5.4 By Fire Scenario

- 5.4.1 Cellulosic Fire Protection

- 5.4.2 Hydrocarbon Pool & Jet-Fire Protection

- 5.4.3 Cryogenic Spill Protection

- 5.5 By End-user Industry

- 5.5.1 Commercial & Residential Construction

- 5.5.2 Oil & Gas (Up-, Mid- & Down-stream)

- 5.5.3 Energy & Power (Conventional & Renewable)

- 5.5.4 Industrial Manufacturing

- 5.5.5 Transportation (Marine, Aerospace, Rail)

- 5.5.6 Public & Critical Infrastructure

- 5.6 By Geography

- 5.6.1 Asia-Pacific

- 5.6.1.1 China

- 5.6.1.2 India

- 5.6.1.3 Japan

- 5.6.1.4 South Korea

- 5.6.1.5 ASEAN Countries

- 5.6.1.6 Rest of APAC

- 5.6.2 North America

- 5.6.2.1 United States

- 5.6.2.2 Canada

- 5.6.2.3 Mexico

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Nordic Countries

- 5.6.3.8 Rest of Europe

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East & Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 South Africa

- 5.6.5.3 Rest of Middle East & Africa

- 5.6.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles {(includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)}

- 6.4.1 3M

- 6.4.2 Akzo Nobel N.V.

- 6.4.3 BASF

- 6.4.4 Contego International Inc.

- 6.4.5 Etex Group

- 6.4.6 Firefree Coatings, Inc.

- 6.4.7 Hempel A/S

- 6.4.8 Hilti Group

- 6.4.9 Isolatek International

- 6.4.10 Isolatek International

- 6.4.11 Jotun

- 6.4.12 Kansai Paint Co., Ltd.

- 6.4.13 Morgan Advanced Materials plc

- 6.4.14 No-Burn, Inc.

- 6.4.15 PPG Industries, Inc.

- 6.4.16 RPM International Inc.

- 6.4.17 Sika AG

- 6.4.18 Teknos Group

- 6.4.19 The Sherwin-Williams Company

- 6.4.20 Tremco Incorporated

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment