|

시장보고서

상품코드

2062340

저융점 섬유 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Low Melting Fiber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

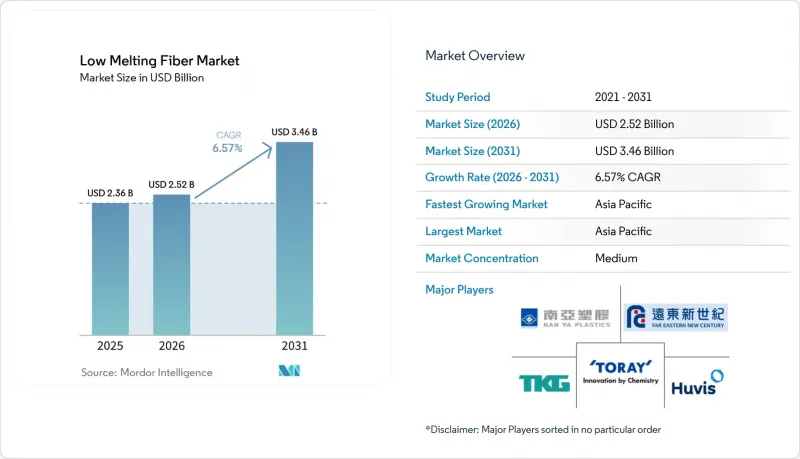

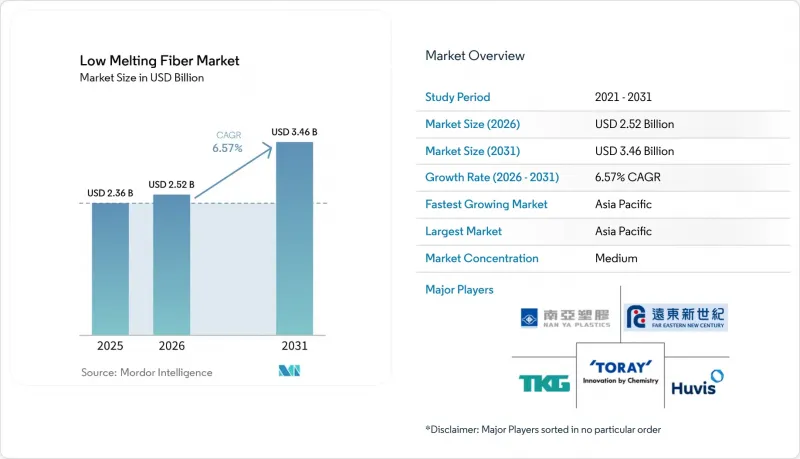

저융점 섬유 시장 규모는 2025년 23억 6,000만 달러로 평가되었습니다. 2026년 25억 2,000만 달러로 확대되고 2026년부터 2031년에 걸쳐 CAGR은 6.57%를 나타내, 2031년까지 34억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 융점(130°C 이하 및 그 이상), 구조 유형(코어·시스, 사이드·바이·사이드, 아일랜드-인-씨), 최종 사용자 산업(섬유·부직포, 자동차 및 운송, 가구 및 침구 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 저융점 섬유 시장 동향 및 인사이트

친환경적이고 지속 가능한 열접착 섬유에 대한 수요 증가

각 브랜드의 탄소 배출 감축 노력에 힘입어, 버진 폴리에스터에서 화학적 재활용 소재 및 식물 유래 대체 소재로의 전환이 가속화되고 있습니다. Indorama Ventures와 Jiaren Chemical Recycling은 버진 등급의 분자량을 유지한 섬유 재활용 PET를 생산하고 있으며, 강도를 저하시키지 않으면서 저융점 2성분 압출 성형을 가능하게 하고 있습니다. Fiberpartner사의 ‘PolyPlant BICO’는 PLA로 제작된 130℃ 내열 피복을 갖춘 바이컴포넌트 섬유로, 100% 바이오 열접착성을 자랑합니다. OEKO-TEX 클래스 1 부록 6의 기준을 충족하며, 퇴비화 가능성과 피부 안전성이 최우선으로 고려되는 위생용품을 대상으로 합니다. EU의 ‘순환형 섬유 전략’은 에코디자인 규정 및 디지털 패스포트 도입을 의무화하고 있어, ISCC Plus 물질 수지 인증을 취득한 공급업체에 대한 수요를 촉진하고 있습니다. 오리엔탈 쉔홍은 재생 폴리에스터 부문과 병에서 실로 직접 방적하는 기술을 보유하고 있으며, 추적성을 확보한 저탄소 원료 공급처로 부상하고 있습니다. 이 회사의 특수 등급 제품은 나이키나 유니클로 등 유명 브랜드에 채택되고 있습니다.

매트리스 및 침구 제조 거점 확대

미국의 섹션 301 관세를 피하기 위해, 과거에는 중국으로 향하던 매트리스 주문이 현재는 베트남이나 태국의 공장으로 흘러가고 있습니다. 이러한 전환으로 인해, 해당 지역에서는 퀼트 커버나 베개 속재료로 자주 사용되는 저융점 PSF 수요가 급증하고 있습니다. PVChem은 치밀한 전략의 일환으로 2025년 7월 VNPOLY와 협약을 체결하고, 재생 PET 칩을 해당 국가의 POY 생산 라인에 공급하기로 했습니다. 이러한 노력은 올해 하반기에 가동을 시작할 예정인, 대규모 처리 능력을 자랑하는 응이손(Nghi Son) 병 재활용 시설을 통해 더욱 강화될 것입니다. 이러한 통합적인 접근 방식을 통해, 과거 두드러졌던 수입 스테이플 섬유에 대한 의존도가 크게 줄어들 것으로 예측됩니다. 또한, 매트리스 OEM 제조업체들은 현재 리드타임 단축과 데니어 수의 유연성을 최우선으로 하고 있습니다. 이러한 변화는 현지 변환업체에 호재를 안겨주고 있으며, 중국 경쟁사보다 낮은 운송 비용을 제공함으로써 경쟁에서 우위를 점할 수 있게 되었습니다.

높은 생산 비용과 PTA·MEG 원자재 가격 변동

2026년 3월, 인도의 PTA 및 MEG 가격은 급등한 후 하락했습니다. 이러한 가격 변동으로 인해 필라멘트 제조업체들은 가격을 인상할 수밖에 없게 되었습니다. 중동 공급 경로에서 지연이 발생하고, 중국 생산자들이 국내 수요를 우선시함에 따라 MEG 현물 시장에서 공급 부족 현상이 나타났습니다. 상품화된 부문에서는 폴리에스터 가격의 프리미엄이 특정 임계치를 초과하면 구매자들이 폴리프로필렌으로 전환하기 때문에 가격 전가 효과가 감소합니다. 중국의 반탈중합 프로젝트는 상당한 에너지 절감 효과가 기대되지만, 높은 자본 요건으로 인해 즉각적인 도입이 제한되고 있습니다.

부문별 분석

2025년, 시장에서는 131-160℃의 온도대가 수요의 46.02%를 차지하며 주류를 이루었습니다. 그 매력은 주로 달력 가공 시의 부드러운 유동성과 아시아태평양 창고에서의 내구성(접착을 방지할 수 있다는 점)에 있었습니다. 130℃ 이하로 설정된 초저융점 등급은 2026년부터 2031년까지의 예측 기간 동안 연평균 성장률(CAGR) 6.72%로 확대될 것으로 전망됩니다. 이러한 인기의 상승은 PLA 기반 섬유 분야에서 중요한 역할을 수행하며, 생리대나 퇴비화 가능한 우편 봉투의 매끄러운 접착을 보장하고 있다는 점에 기인합니다. 반면, 160℃를 초과하는 고융점 등급은 주로 멜트블로우 필터 매체나 특정 엔진룸 부품에 사용됩니다. 그러나 특히 배터리 관련 분야에서 세라믹 섬유에 시장 점유율을 빼앗기고 있습니다. 저융점 섬유 시장, 특히 중융점 대 시장은 상당한 성장이 예상됩니다. 2025년 12월 유럽연합(EU)의 펠릿 손실 규제가 발효됨에 따라, 주요 공장에서는 현재 분진 포집 시스템 도입이 진행되고 있습니다. 이러한 전환은 현장에서의 봉쇄 솔루션을 보유한 통합형 기업에 유리하게 작용할 것입니다. 파 이스트 뉴 센추리(Far Eastern New Century)사는 스포츠웨어 및 압박 스타킹 분야에서 높은 수익률을 달성하기 위해, 낮은 융점에서도 탄성 회복력을 높이기 위한 투자를 전략적으로 진행하고 있습니다.

새로운 동향으로, 재활용에 대한 관심이 높아지고 있습니다. 현재 순환형 설계 사양서에는 용융 온도가 명시되어 있어, 향후 분리 처리가 효율화되고 있습니다. 유럽에서는 안목이 높은 주요 바이어들이 검증되지 않은 공급처의 제품보다는 ‘패스포트’(품질 보증서)가 첨부된 중가대 섬유 로트에 대해 더 높은 가격을 지불할 의향을 보이고 있습니다.

지역별 분석

2025년, 아시아태평양은 저융점 섬유 시장을 독점하며 51.37%라는 높은 점유율을 차지했습니다. 예측에 따르면, 해당 지역은 2026년부터 2031년까지의 예측 기간 동안 6.77%라는 견실한 연평균 성장률(CAGR)을 유지할 것으로 보입니다. 최전선에 위치한 중국은 오리엔탈 셴홍(Oriental Shenghong)에 대규모 필라멘트 생산 라인을 보유하고 있습니다. 2026년 4분기부터는 베트남 응이손(Nghi Son)의 rPET 복합 시설이 VNPOLY의 POY 압출 성형 업체에 재생 칩을 공급함으로써 현지 공급망을 강화하게 될 것입니다. 2026년 3월 원자재 가격 변동으로 인해 인도에서 가격 상승이 나타나고 있으며, 연간 수요는 견조한 추세를 보이고 있어 저융점 시장에 새로운 진출기업들을 끌어들이고 있습니다.

북미에서는 특히 한국산 PSF 수입에 대한 반덤핑 관세에 직면해 있습니다. 그 결과, 바이어들은 미국 내 생산이나 멕시코의 컨버터로 무게중심을 옮기고 있습니다. Indorama Ventures사의 목스빌 생산 라인은 위생용품 OEM 제조업체로의 운송 시간을 단축할 뿐만 아니라, 자동차 내장재 분야에서도 입지를 다지고 있습니다.

유럽에서는 2025년 12월 마감 시한을 앞두고, 펠릿 손실 규제에 대응하고, 융점 공개를 의무화하는 디지털 패스포트 도입에 주력했습니다. 독일과 이탈리아 양국은 ISCC 인증을 획득한 화학적 재활용을 통해 생산된 저융점 제품에 대해 할증 가격을 지불할 의향을 밝혔습니다. 남미, 중동 및 아프리카의 역할은 비교적 미미한 편이지만, 브라질의 생리대 시장 확대와 사우디아라비아의 대규모 인프라 투자가 카펫 안감 및 HVAC용 단열재 수요를 견인하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the low melting fiber market size is expected to grow from USD 2.36 billion in 2025 to USD 2.52 billion in 2026 and is forecast to reach USD 3.46 billion by 2031 at 6.57% CAGR over 2026-2031.

This report is Segmented by Melting Point (<=130°C, and More), Structure Type (Core-Sheath, Side-By-Side, and Islands-In-Sea), End-User Industry (Textiles and Nonwovens, Automotive and Transportation, Furniture and Bedding, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Low Melting Fiber Market Trends and Insights

Rising Demand for Eco-Friendly and Sustainable Thermal-Bond Fibers

Brand commitments to carbon reduction have accelerated the shift from virgin polyester to both chemically recycled and plant-based alternatives. Indorama Ventures and Jiaren Chemical Recycling have been producing textile-recycled PET that maintains virgin-grade molecular weight, allowing for a low-melt bicomponent extrusion without compromising strength. Fiberpartner's PolyPlant BICO, a bicomponent fiber with a 130 °C sheath made from PLA, boasts 100% bio-based thermal bonding. It meets the OEKO-TEX Class 1 Annex 6 standard and is aimed at hygiene products, where compostability and skin safety are paramount. The EU's Circular Textiles Strategy mandates ecodesign regulations and digital passports, pushing demand toward suppliers with the ISCC Plus mass-balance certification. Oriental Shenghong, with its recycled-polyester unit and a direct-spinning method from bottle to yarn, has emerged as a traceable, low-carbon feedstock provider. Its specialty grades cater to renowned brands such as Nike and Uniqlo.

Expansion of Mattress and Bedding Manufacturing Footprints

In a bid to evade U.S. Section 301 tariffs, mattress orders that once headed to China are now finding their way to factories in Vietnam and Thailand. This pivot has spurred a surge in demand for low-melt PSF in the region, a material frequently utilized in quilted covers and as filling for pillows. In a calculated maneuver, PVChem inked a pact in July 2025 with VNPOLY, directing recycled PET chips into the country's POY production lines. This effort is further strengthened by an upcoming bottle-recycling facility in Nghi Son, boasting a significant capacity, set to commence operations later this year. This integrated approach significantly reduces Vietnam's long-standing reliance on imported staple fiber, a dependency that was once pronounced. Additionally, mattress OEMs are now prioritizing shorter lead times and flexible denier counts. This evolution has created opportunities for local converters, enabling them to compete successfully by providing shipping costs that are lower than those of their Chinese rivals.

High Production Costs and PTA/MEG Feedstock Volatility

In March 2026, the prices of PTA and MEG in India surged before declining. This fluctuation compelled filament makers to increase their prices. A tightening in spot MEG availability emerged as Middle-East supply lines faced delays, while Chinese producers prioritized domestic demands. In commoditized segments, buyers shift to polypropylene when polyester premiums exceed a specific threshold, reducing the pass-through effect. Although Chinese semi-depolymerization projects promise significant energy savings, their high capital requirements limit immediate implementation.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Automotive Acoustic and Thermal-Insulation Applications

- Shift Toward Solvent-Free Hot-Melt Lamination in Functional Sportswear

- Intense Competition from Conventional Binders and U.S. Duties

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, the market saw the 131-160 °C band dominate, capturing 46.02% of the demand. Its appeal was largely due to its smooth flow during calendering and its resilience in Asia-Pacific warehouses, where it avoided sticking. Ultra-low-melt grades, set at or below 130 °C, are projected to expand at a 6.72% CAGR during the forecast period of 2026-2031. Their rising popularity is attributed to their pivotal role in PLA-based fibers, ensuring seamless bonding for hygiene pads and compostable mailers. In contrast, high-melt grades, surpassing 160 °C, are primarily used in melt-blown filter media and select under-hood components. However, they are losing market share to ceramic fibers, particularly in battery-adjacent applications. The market for low-melting fibers, especially in the mid-range band, is poised for significant growth. With the European Union's pellet-loss regulations taking effect in December 2025, major plants are now adopting dust capture systems. This transition favors integrated players with on-site containment solutions. In a calculated move, Far Eastern New Century is channeling investments into boosting elastic recovery at low-melt points, targeting the lucrative margins in sportswear and compression hosiery.

Emerging trends underscore a heightened focus on recycling; circular-design invoices now highlight melt temperatures, streamlining future separations. In Europe, discerning core buyers are willing to pay a premium for mid-range fiber lots accompanied by a "passport" - a quality assurance - over those from unverified sources.

Geography Analysis

In 2025, the Asia-Pacific region dominated the Low Melting Fiber market, capturing a substantial 51.37% share. Projections indicate the region will sustain a robust 6.77% CAGR through the forecast period of 2026-2031. China, anchored at the forefront, boasts significant filament lines at Oriental Shenghong. Starting in Q4 2026, Vietnam's Nghi Son rPET complex will bolster local supply loops by providing recycled chips to VNPOLY POY extruders. Even with feedstock price fluctuations in March 2026 leading to price hikes in India, the annual demand remains strong, attracting new players to the low-melt market.

North America finds itself contending with antidumping levies, specifically duties on imports of Korean PSF. Consequently, buyers are pivoting towards domestic U.S. production and converters in Mexico. Indorama Ventures' Mocksville line not only streamlines transit times for hygiene OEMs but also secures a position in the automotive interior sector.

Europe is preparing for a December 2025 deadline, focusing on pellet-loss compliance and the rollout of digital passports that require melt-point disclosures. Both Germany and Italy are showing a willingness to pay a premium for ISCC-certified, chemically recycled low-melt products. While South America and the Middle-East and Africa play relatively minor roles, Brazil's expanding footprint in hygiene pads and Saudi Arabia's significant infrastructure investments are driving demand for carpet backings and HVAC insulation.

- Amerex Hubei Decon Polyester Co., Ltd.

- Beaulieu Fibres International

- Far Eastern New Century Corporation

- FiberPartner ApS

- Hickory Springs Manufacturing

- IFG International Fibres Group

- Indorama Ventures Public Company Limited

- Kolon Industries, Inc.

- NAN YA PLASTICS CORPORATION

- Shaoxing Global Chemical Fiber Co., Ltd.

- Sichuan Huvis

- Sinopec Yizheng Chemical Fibre Co., Ltd.

- Suzhou Makeit Technology Co., Ltd.

- Taekwang Industrial Co., Ltd.

- TEIJIN FRONTIER (U.S.A.), INC.

- Toray Advanced Materials Korea

- VNPOLYFIBER

- XiangLu Tenglong Group

- Yangzhou Tinfulong Group Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for eco-friendly and sustainable thermal-bond fibers

- 4.2.2 Expansion of mattress and bedding manufacturing footprints

- 4.2.3 Growth in automotive acoustic and thermal-insulation applications

- 4.2.4 Shift toward solvent-free hot-melt lamination in functional sportswear

- 4.2.5 Emergence of 3-D printed fiber preforms for lightweight composites

- 4.2.6 Surging interest in biodegradable LMF grades for EV-battery thermal pads

- 4.3 Market Restraints

- 4.3.1 High production costs and PTA/MEG feed-stock volatility

- 4.3.2 Intense competition from conventional binders (adhesive powders, PP fibers)

- 4.3.3 Micro-plastic shedding restrictions on synthetic non-wovens (EU proposal)

- 4.3.4 US anti-dumping duties on Korean and Taiwanese low-melt PSF

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Melting Point

- 5.1.1 <= 130 °C

- 5.1.2 131 - 160 °C

- 5.1.3 Greater than 160 °C

- 5.2 By Structure Type

- 5.2.1 Core-Sheath

- 5.2.2 Side-by-Side

- 5.2.3 Islands-in-Sea

- 5.3 By End-user Industry

- 5.3.1 Textiles and Nonwovens

- 5.3.2 Automotive and Transportation

- 5.3.3 Furniture and Bedding

- 5.3.4 Construction and Building Materials

- 5.3.5 Hygiene and Medical Disposables

- 5.3.6 3-D Printing and Composites

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, Recent Developments)}

- 6.4.1 Amerex Hubei Decon Polyester Co., Ltd.

- 6.4.2 Beaulieu Fibres International

- 6.4.3 Far Eastern New Century Corporation

- 6.4.4 FiberPartner ApS

- 6.4.5 Hickory Springs Manufacturing

- 6.4.6 IFG International Fibres Group

- 6.4.7 Indorama Ventures Public Company Limited

- 6.4.8 Kolon Industries, Inc.

- 6.4.9 NAN YA PLASTICS CORPORATION

- 6.4.10 Shaoxing Global Chemical Fiber Co., Ltd.

- 6.4.11 Sichuan Huvis

- 6.4.12 Sinopec Yizheng Chemical Fibre Co., Ltd.

- 6.4.13 Suzhou Makeit Technology Co., Ltd.

- 6.4.14 Taekwang Industrial Co., Ltd.

- 6.4.15 TEIJIN FRONTIER (U.S.A.), INC.

- 6.4.16 Toray Advanced Materials Korea

- 6.4.17 VNPOLYFIBER

- 6.4.18 XiangLu Tenglong Group

- 6.4.19 Yangzhou Tinfulong Group Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment