|

시장보고서

상품코드

2062344

단열 유리창 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Insulating Glass Window - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

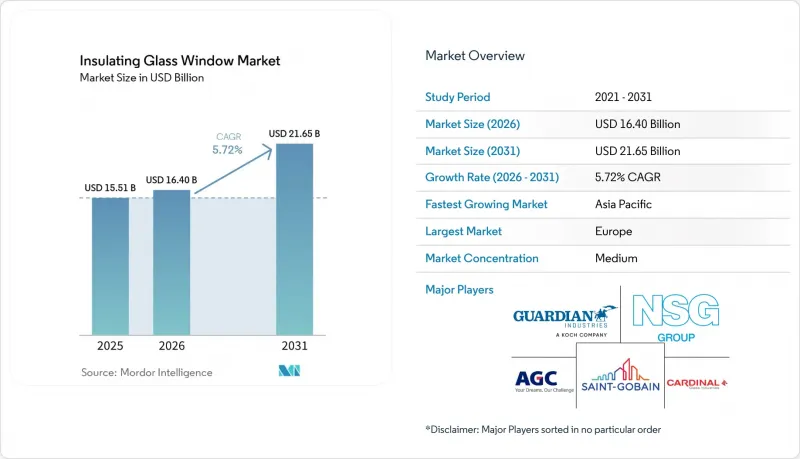

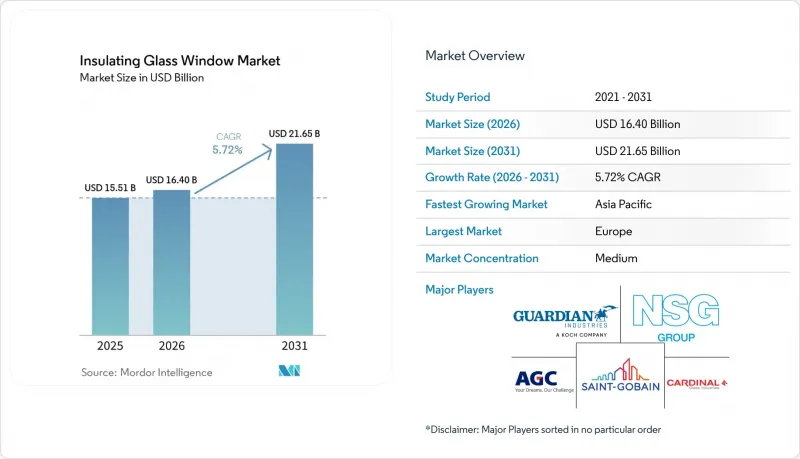

Mordor Intelligence에 의하면, 단열 유리창 시장 규모는 2025년에 155억 1,000만 달러로 평가되었고, 2026년 164억 달러로 추정되고, 2031년까지 216억 5,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 5.72%를 나타낼 전망입니다.

본 보고서는 유리 사양별(이중 유리 등), 창틀 재질별(uPVC 등), 용도별(주택, 상업용 건물 등) 및 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 단열 유리창 시장 동향 및 인사이트

주요 경제권에서의 건축 에너지 절약 기준 의무화

캘리포니아주의 ‘Title 24-2025’ 및 2025년판 뉴욕시 에너지 절약 규정에서는 온난 지역의 창문 전체 U값을 0.30으로, 한랭 지역에서는 0.25로 제한하고 있으며, 이로 인해 신축 건물에서 단층 유리가 사실상 배제되게 됩니다. 유럽연합(EU)의 2024년 ‘건축물 에너지 성능 지침(EPBD)’ 개정안에 따르면, 2027년까지 모든 신축 건물에 대해 니어 제로 에너지 기준을 의무화하고 있으며, 독일, 프랑스, 북유럽 국가들의 삼중 유리 채택률은 60% 이상으로 증가했습니다. 중국에서는 2025년 주택 건축 기준에 따라, 난방 구역에서 U값을 1.5 W/m²K 이하로 유지해야 합니다. 이 기준은 웜 에지 스페이서를 갖춘 단열 유리창에서만 달성할 수 있으며, 이로 인해 삼중 유리 유닛의 도입이 가속화되고 있습니다. 이러한 규제의 조화를 통해 대부분의 기후대에서 투자 회수 기간이 5년 미만으로 단축되었으며, 단열 유리는 단순한 업그레이드에서 표준 사양으로 전환되고 있습니다. 이러한 정책들을 종합해 볼 때, 단열 유리창 시장의 예상 연평균 성장률(CAGR)에 1.2포인트의 상승 효과를 가져올 것으로 전망됩니다.

LEED 및 BREEAM 인증 프로젝트를 통한 그린 라벨 프리미엄

‘에너지 및 환경 설계 리더십(LEED)’ v5에서는 제3자에 의한 환경 제품 선언(EPD) 및 재활용 함량 검증을 받은 유리 시스템에 대해 최대 4점의 ‘재료 투명성’ 점수가 부여됩니다. 이를 통해 1제곱미터당 100Kg 미만의 이산화탄소 환산량(kg CO2e/m2)에 해당하는 내재 탄소 발자국을 가진 단열 유리의 사용이 촉진될 것입니다. 건축연구기구 환경평가기법(BREEAM) 인터내셔널 2024에서는 파사드의 전체 수명 주기에 걸친 탄소 평가가 의무화되어 있으며, 산림관리협의회(FSC) 인증 목재를 사용하여 순음(net negative) 내재 탄소를 실현하는 목재 프레임 삼중 유리창이 권장되고 있습니다. 런던, 뉴욕, 싱가포르 등의 도시에서 인증을 받은 부동산은 2025년에 8-12%의 가격 프리미엄을 기록했으며, U값이 0.8 W/m²K 미만임이 입증된 경우 개발업자에게 1제곱미터당 150-200달러의 추가 수익으로 이어졌습니다. 이러한 가격 프리미엄 덕분에, 높은 임대료가 투자를 정당화하는 고층 복합 애플리케이션 개발 분야에서 진공 단열 유리(VIG) 및 삼중 유리 유닛에 대한 수요가 증가하고 있습니다. 이러한 추세는 예측 기간의 첫 2년 동안 단열 유리창 시장의 성장에 약 0.8포인트 기여할 것으로 예측됩니다.

단층 유리의 높은 초기 비용

인도네시아, 필리핀, 사하라 이남 아프리카 등의 지역에서는 단열 유리창이 단창에 비해 60-80% 더 비쌉니다. 이러한 지역에서는 전기 요금이 저렴하고 투자 회수 기간이 10년을 초과하기 때문에 저가형 주택에서의 도입이 제한되고 있습니다. 브라질에서는 ‘Minha Casa Minha Vida(마이 하우스 마이 라이프)’ 프로그램에서 단열 유리창이 적용 대상에서 제외되어 있으며, 그 사용은 중산층 주택이나 상업용 건물로 한정되어 있습니다. 사우디아라비아에서는 개발업체들이 혼합 방식을 채택하여, 햇빛이 직접 닿는 외벽에만 이중 유리를 사용함으로써 비용을 30% 절감하는 동시에 약 절반 수준의 에너지 절약 효과를 달성하고 있습니다.

부문별 분석

2025년 단열 유리창 시장 규모에서 이중 유리가 총 매출의 61.89%를 차지했습니다. 단열 유리창은 온대 기후 지역의 리모델링 공사에서 널리 채택되고 있는 선택지입니다. 그러나 정책 입안자들이 U값 기준을 강화함에 따라, 해당 제품 시장 점유율은 서서히 감소하고 있습니다. 북유럽이나 캐나다에서는 창문 전체의 U값이 0.7-0.9와트/제곱미터·켈빈(W/m²K)인 패시브하우스 기준을 충족하기 위해 삼중 유리가 점차 보급되고 있습니다. 또한, 4중 유리 및 진공 단열 유리(VIG)를 포함한 ‘기타’ 부문은 연평균 성장률(CAGR) 6.57%로 성장하고 있습니다. VIG의 비용은 점차 낮아지고 있으며, 현재 상업용 주문의 경우 삼중 유리와 20% 이내의 가격 차이로 좁혀져, 역사적 건축물이나 슬림한 커튼월을 위한 현실적인 선택지가 되고 있습니다.

각 제조업체는 특정 유리 유형에 맞춘 단계별 가스 충전 솔루션을 도입하고 있습니다. 구체적으로, 이중 유리에는 아르곤, 삼중 유리에는 크립톤, VIG에는 진공 챔버를 채택하여 두께와 무게의 제약에 대응할 수 있도록 최적화되어 있습니다. 4중 유리는 두께가 50-60mm, 무게가 1제곱미터당 40Kg(kg/m²)에 달하기 때문에 스칸디나비아 지역에서는 여전히 틈새 제품으로 남아 있습니다. 수요는 제한적이지만, 탄소중립 주택을 위한 KfW 40 Plus 인센티브를 통해 지원받고 있습니다. 비용 동향의 변화는 시장이 양극화되고 있음을 시사하고 있습니다. 한쪽에는 대중 시장을 겨냥한 리모델링 공사가, 다른 한쪽에는 초저에너지 신축 주택이 있으며, 각각은 단열 유리 창호 시장 내의 서로 다른 유리 카테고리에 따라 대응되고 있습니다.

지역별 분석

유럽은 2025년 예상 매출의 37.21%를 차지했으며, 이는 신축 주택의 삼중 유리 보급률을 60% 이상으로 끌어올린 ‘니어 제로 에너지’ 규정에 힘입은 결과입니다. 리모델링 수요도 커서, 영국과 독일에서는 1970년대에 제작된 창문을 프레임 개조 없이 초슬림형 삼중 유리 유닛으로 교체하는 추세가 나타나고 있습니다. 이를 통해 열 손실이 45% 감소하여 정부의 인센티브 대상이 됩니다. 생고뱅(Saint-Gobain)사가 프랑스 내 제조 설비의 전환 및 이집트에서의 생산 능력 확대를 위해 단행한 140억 유로(163억 9,000만 달러) 규모의 투자는 유럽 및 북아프리카 시장에 대한 공급을 뒷받침하고 있습니다. 남유럽은 온화한 기후로 인해 보급 속도가 완만하지만, 마드리드나 밀라노 등의 도시에 위치한 BREEAM(Building Research Establishment Environmental Assessment Method) 인증을 획득한 사무실에서는 임대료 프리미엄을 확보하기 위해 고성능 유리가 계속해서 채택되고 있습니다.

아시아태평양은 중국의 리모델링 보조금, 인도의 120만 호에 달하는 도시 개발 계획, 그리고 푸야오(Fuyao)사의 신규 제조 공장이 견인하는 베트남의 고층 아파트 붐에 힘입어 연평균 성장률(CAGR) 6.77%를 나타낼 것으로 예측됩니다. 중국의 1급 도시에서는 저방사율(Low-E) 코팅이 적용된 삼중 유리가 표준으로 사용되고 있는 반면, 3급 도시에서는 웜엣지 이중 유리가 선택되고 있습니다. 일본과 한국에서는 한랭 지역에서 삼중 유리 설치에 대한 보조금이 지급되고 있으며, 서울의 아파트 개발업체들은 판매 자료에서 창문의 U값을 강조하고 있습니다. 아세안 시장에서는 고온 다습한 기후 조건에서 엣지 씰의 내구성이 과제로 대두되고 있으나, 수명을 연장하기 위해 이중 씰 및 건조제 스페이서 기술이 점차 도입되고 있습니다.

북미에서는 ‘Title 24-2025’ 및 뉴욕주의 2025년 기준에 따라 건축 기준이 강화되어, 허용 사양에서 단층 유리가 제외됨에 따라 상업용 부동산의 시설 개선이 촉진되고 있습니다. Vitro사의 VacuMax 공장과 Fuyao사의 일리노이주 내 확장으로 인해 국내 공급이 강화되어, 아시아산 수입에 대한 의존도가 낮아지고 관세의 영향이 완화되고 있습니다. 멕시코에서는 낮과 밤의 기온 차가 큰 국경 인근 도시에서 단열 유리창이 일반적으로 사용되고 있지만, 멕시코시티의 LEED(에너지 및 환경 설계 리더십) 인증을 획득한 고층 빌딩에서는 삼중창이 선호되고 있습니다. 남미에서의 채용은 브라질과 아르헨티나에 집중되어 있지만, 높은 자금 조달 비용이 성장을 제약하고 있는 가운데, 정부의 주택 프로그램이 일정한 지원을 제공합니다. 중동에서는 NEOM이나 레드시(Red Sea) 개발과 같은 대규모 프로젝트의 유리 사양에 주목하고 있으며, 최고 50°C에 달하는 극한의 기온을 견디기 위해 해양용 등급의 실링재와 Low-E 코팅이 요구되고 있습니다. 사하라 이남 아프리카에서는 비용 문제가 여전히 중요한 요소로 작용하고 있으며, 도시 지역의 오피스 타워에서는 비용과 성능의 균형을 고려하여 주로 단열 유리창가 채택되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the insulating glass window market size was valued at USD 15.51 billion in 2025 and is estimated to grow from USD 16.40 billion in 2026 to reach USD 21.65 billion by 2031, at a CAGR of 5.72% during the forecast period (2026-2031).

This report is Segmented by Glazing Type (Double Glazing and More), Window Frame Material (uPVC and More), Application (Residential, Commercial Buildings, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Insulating Glass Window Market Trends and Insights

Mandatory Building-Energy Codes in Major Economies

California's Title 24-2025 and the 2025 New York City Energy Conservation Code now limit whole-window U-values to 0.30 in warm zones and 0.25 in colder zones, effectively removing single glazing from new construction. The European Union's 2024 Energy Performance of Buildings Directive (EPBD) revision mandates near-zero-energy standards for all new buildings by 2027, increasing triple-glazing adoption to over 60% in Germany, France, and Nordic countries. In China, the 2025 residential code requires U-values of 1.5 W/m2K or lower in heating zones, a threshold achievable by double glazing only with warm-edge spacers, accelerating the adoption of triple-glazed units. These converging regulations reduce payback periods to under five years in most climates, transitioning insulating glass from an upgrade to a standard specification. Collectively, these policies are projected to add 1.2 percentage points to the forecasted compound annual growth rate (CAGR) of the insulating glass window market.

Green-Label Premiums from LEED and BREEAM Certified Projects

Leadership in Energy and Environmental Design (LEED) v5 awards up to four material transparency points for glazing systems with third-party environmental product declarations and recycled-content verification, encouraging the use of insulating glass with embodied-carbon footprints below 100 kilograms of carbon dioxide equivalent per square meter (kg CO2e/m2). Building Research Establishment Environmental Assessment Method (BREEAM) International 2024 requires whole-life carbon assessments for facades, favoring timber-framed triple glazing that achieves net-negative embodied carbon when Forest Stewardship Council (FSC)-certified timber is used. Certified properties in cities like London, New York, and Singapore commanded 8-12% price premiums in 2025, translating to additional developer revenue of USD 150-200/m2 when U-values below 0.8 W/m2K are documented. These premiums drive demand for vacuum-insulated glass (VIG) and triple-glazed units in high-rise mixed-use developments, where higher rents justify the investment. This trend is expected to contribute approximately 0.8 percentage points to the insulating glass window market growth over the initial two forecast years.

Higher Upfront Cost Versus Single Glazing

Insulating glass has a price premium of 60-80% compared to single glazing in regions such as Indonesia, the Philippines, and sub-Saharan Africa. In these areas, low power tariffs and a payback period exceeding a decade limit its use in entry-level housing. In Brazil, the Minha Casa Minha Vida (My House My Life) program excludes insulating glass, restricting its adoption to mid-income housing and commercial buildings. In Saudi Arabia, developers adopt a mixed approach, using insulating glass only on solar-exposed facades to achieve approximately half the energy savings at 30% lower costs.

Other drivers and restraints analyzed in the detailed report include:

- Urban Housing Booms in Developing Countries

- Net-Zero-Carbon Mandates Accelerating Triple and Quad Glazing

- Edge-Seal Failures Causing Performance Loss in Hot-Humid Zones

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The insulating glass window market size for double glazing accounts for 61.89% of total revenue in 2025. Double glazing is a widely used option for retrofits in temperate climates. However, its market share is gradually declining as policymakers implement stricter U-value limits. Triple glazing is gaining adoption in northern Europe and Canada, where whole-window U-values of 0.7-0.9 watts per square meter kelvin (W/m2K) meet passive-house standards. Additionally, the "other types" segment, which includes quadruple and vacuum insulating glass (VIG), is expanding at a compound annual growth rate (CAGR) of 6.57%. The decreasing costs of VIG, now within 20% of triple glazing for commercial orders, make it a viable choice for heritage sites and slender curtain walls.

Manufacturers are introducing tiered gas-fill solutions tailored to specific glazing types: argon for double glazing, krypton for triple glazing, and vacuum chambers for VIG, optimized to address thickness and weight constraints. Quadruple glazing remains a niche product in Scandinavia due to its 50-60 millimeter thickness and 40 kilograms per square meter (kg/m2) weight. Despite limited demand, it is supported by KfW 40 Plus incentives for net-zero homes. The evolving cost dynamics suggest a bifurcation in the market, with mass-market retrofits on one side and ultra-low-energy new builds on the other, each served by distinct glazing categories within the insulating glass window market.

Geography Analysis

Europe accounted for 37.21% of the projected 2025 revenue, driven by near-zero-energy mandates that have increased triple-glazing penetration to over 60% in new housing. Retrofit demand is also significant, with ultra-thin triple-glazed units replacing 1970s-era windows in the United Kingdom and Germany without requiring frame modifications. This reduces heat loss by 45% and qualifies for government incentives. Saint-Gobain's EUR 14 billion (USD 16.39 billion) investment to convert furnaces in France and expand capacity in Egypt supports supply for both European and North African markets. Southern Europe shows slower adoption due to milder climates, but Building Research Establishment Environmental Assessment Method (BREEAM)-certified offices in cities like Madrid and Milan continue to specify high-performance glazing to secure rental premiums.

The Asia-Pacific region is expected to grow at a 6.77% compound annual growth rate (CAGR), supported by China's retrofit subsidies, India's 1.2 million-unit metro development pipeline, and Vietnam's high-rise condominium boom, which is bolstered by Fuyao's new manufacturing plant. In tier-1 Chinese cities, triple-glazed units with Low-Emissivity (Low-E) coatings are standard, while tier-3 cities opt for warm-edge double glazing. Japan and South Korea provide subsidies for triple glazing in colder regions, with Seoul's condominium developers highlighting window U-values in sales materials. Association of Southeast Asian Nations (ASEAN) markets face challenges with edge-seal durability in hot and humid climates, but are adopting dual-seal and desiccant spacer technologies to improve service life.

North America has tightened building codes with Title 24-2025 and New York's 2025 standards, which eliminate single glazing from permissible specifications and drive upgrades in commercial real estate. Domestic supply is bolstered by Vitro's VacuMax plant and Fuyao's Illinois expansion, reducing reliance on Asian imports and mitigating tariff impacts. In Mexico, double glazing is commonly installed in border cities with significant diurnal temperature variations, while Leadership in Energy and Environmental Design (LEED)-certified towers in Mexico City prefer triple-glazed units. South America's adoption is concentrated in Brazil and Argentina, where high financing costs limit growth, though governmental housing programs provide some support. The Middle East focuses on glazing specifications for large-scale projects like NEOM and the Red Sea developments, which require marine-grade seals and Low-E coatings to withstand extreme temperatures of up to 50°C. In Sub-Saharan Africa, cost considerations remain a key factor, with urban office towers primarily using double glazing to balance cost and performance.

- AeroShield

- AGC Inc.

- ALUK

- CARDINAL GLASS INDUSTRIES, INC

- Central Glass Co.

- CSG HOLDING CO., LTD.

- Fuyao Glass Industry Group

- Glaston Corporation

- Guardian Industries

- Hartung Glass

- Internorm

- Morley Glass & Glazing Ltd.

- NSG Group/Pilkington

- PRESS GLASS Holding SA

- Saint-Gobain

- sedak GmbH & Co. KG

- Sisecam Group

- Viracon

- Vitro Architectural Glass

- Xinyi Glass Holdings Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory building-energy codes in major economies

- 4.2.2 Green-label premiums from LEED and BREEAM certified projects

- 4.2.3 Urban housing booms in developing countries

- 4.2.4 Net-zero-carbon mandates accelerating triple and quad glazing

- 4.2.5 Mass-production scale-up of vacuum insulated glass (VIG)

- 4.2.6 Ultra-thin glass triples enabling retrofits without frame changes

- 4.3 Market Restraints

- 4.3.1 Higher upfront cost versus single glazing

- 4.3.2 Edge-seal failures causing performance loss in hot-humid zones

- 4.3.3 Volatile soda-ash and aluminium-spacer prices

- 4.3.4 Skilled-labour shortages for automated IG and VIG lines

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Glazing Type

- 5.1.1 Double Glazing

- 5.1.2 Triple Glazing

- 5.1.3 Other Types (Quadruple, Vacuum IG)

- 5.2 By Window Frame Material

- 5.2.1 uPVC

- 5.2.2 Aluminium

- 5.2.3 Wood

- 5.2.4 Composite

- 5.2.5 Other Materials (Fibreglass, Steel)

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Commercial Buildings

- 5.3.3 Industrial Facilities

- 5.3.4 Institutional and Public Infrastructure

- 5.3.5 Other Applications (Retail, Mixed-Use)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Nordic Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 AeroShield

- 6.4.2 AGC Inc.

- 6.4.3 ALUK

- 6.4.4 CARDINAL GLASS INDUSTRIES, INC

- 6.4.5 Central Glass Co.

- 6.4.6 CSG HOLDING CO., LTD.

- 6.4.7 Fuyao Glass Industry Group

- 6.4.8 Glaston Corporation

- 6.4.9 Guardian Industries

- 6.4.10 Hartung Glass

- 6.4.11 Internorm

- 6.4.12 Morley Glass & Glazing Ltd.

- 6.4.13 NSG Group/Pilkington

- 6.4.14 PRESS GLASS Holding SA

- 6.4.15 Saint-Gobain

- 6.4.16 sedak GmbH & Co. KG

- 6.4.17 Sisecam Group

- 6.4.18 Viracon

- 6.4.19 Vitro Architectural Glass

- 6.4.20 Xinyi Glass Holdings Limited

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment