|

시장보고서

상품코드

2062349

평판 탄소강 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Flat Carbon Steel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

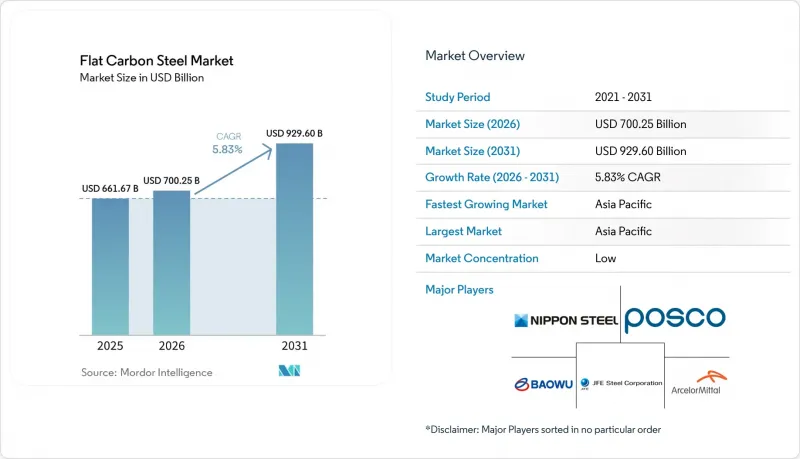

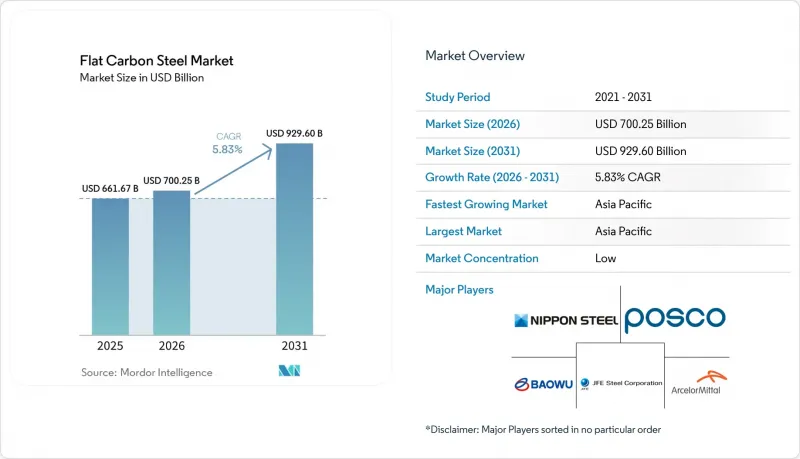

평판 탄소강 시장 규모는 2025년에 6,616억 7,000만 달러로 평가되었습니다. 2026년에 7,002억 5,000만 달러에 달하고, 2031년까지 9,296억 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR은 5.83%를 나타낼 전망입니다.

본 보고서는 제품 유형(열간 압연 코일, 냉간 압연 코일 등), 두께(초박형(0.8mm 미만) 등), 제조 방법(기본 산소 용광로(BOF) 등), 최종 용도(가전제품 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 평판 탄소강 시장 동향 및 분석

자동차 및 조선 분야 수요 증가

자동차의 전동화로 인해 차량 1대당 강재 사용량은 약 1,200Kg(이 중 최대 100Kg이 전자강판) 수준으로 유지되고 있으며, 생산 대수가 정체 상태임에도 불구하고 냉연 코일 수요는 지속되고 있습니다. 아시아 조선소들의 액화천연가스(LNG) 운반선 수주 잔고가 3년 분에 달하고 있으며, 고인성 강판과 고급 코팅재가 필요하기 때문에 조선용 강재 가격을 지탱하고 있습니다. 2024년, 인도에서는 백색가전이 6,500만 대 증가하여 아연 도금 코일의 출하량은 늘었으나, 판재 두께가 얇아짐에 따라 1대당 강재 사용량은 감소했습니다. 중국에서는 ‘선박의 안전하고 환경적으로 적절한 재활용에 관한 홍콩 국제협약’에 따라 스크랩 품질 향상에 주력하고 있으며, 자동차용 프레스 부품을 공급하는 전기 아크로(EAF) 제조업체의 원자재 비용이 상승하고 있습니다. 한국의 ‘Hyper-Gap Vision 2040’ 프로그램은 액화 이산화탄소(CO2) 운반선 및 듀얼 연료 선박용 첨단 강판 수요를 견인하고 있습니다.

전 세계 인프라 및 가전제품의 확대

2026년 1월, 미국의 건설 착공액은 연율 환산으로 1조 2,400억 달러에 달했으며, 이 중 약 200억 달러는 단 3개의 메가 프로젝트에서 비롯된 것으로, 평판강 시장에 변동을 일으키고 있습니다. 인도에서 추진 중인 11억 1,000만 루피(1,182만 달러) 규모의 인프라 계획은 2034년까지 2억 5,200만 톤의 철강 제품 수요가 발생할 것으로 전망하고 있습니다. 3조 1,000억 달러 규모의 아세안(ASEAN) 개발 프로그램은 지역 종합적 경제 동반자 협정(RCEP) 하에서 지역 내 원자재 유통을 촉진하는 동시에, 중국산 수입에 대한 의존도를 낮추고 있습니다. 2025년에는 난방·환기·공조(HVAC) 기기의 출하 대수가 20% 감소하여 770만 대를 기록했습니다. 이로 인해 캐비닛 및 덕트용 강판의 출하량에 부정적인 영향을 미치고 있습니다. 중동에서는 NEOM이나 비전 2030과 같은 프로젝트가 두꺼운 강판과 구조용 빔의 소비를 주도하고 있으며, 수요는 약 5,000만 톤으로 안정적으로 유지되고 있습니다.

철광석 및 원료탄 가격의 변동

미국의 야금용 석탄 수출량은 2026년까지 5,340만 쇼트톤으로 증가할 것으로 예상되며, 이는 전 세계 코크스 공급에 영향을 미쳐 고로 비용을 상승시키는 요인이 될 것입니다. 브라질 광산 운영의 혼란과 호주 항만의 지연으로 인해 철광석 가격은 매달 큰 변동을 보이고 있으며, 이는 제철소의 운영 자금에 영향을 미치고 있습니다. 중동의 해운 혼란으로 인해 코크스용 석탄의 현물 가격이 상승하면서, 고로(BF)와 전기 아크로(EAF) 생산 방식 간의 비용 격차가 더욱 확대되었습니다. 게다가 고로 제조업체들은 탄소세 인상에 직면해 있는 반면, EAF 제조업체들은 고철 가격 상승에 직면해 있으며, 부셸링 가격은 그로스톤당 422.50달러에 달하고 있습니다. 또한, 디젤 연료와 전기 요금의 급등으로 인해 운송비와 용해 비용도 상승하여, 평판 탄소강 업계 전체의 이익률이 하락하고 있습니다.

부문별 분석

아연 도금 강판 및 코일은 2031년까지 연평균 6.47%의 성장률을 보일 것으로 전망됩니다. 2025년에는 구조용 형강, 선박용 강판, 자동차용 패널에 대한 수요에 힘입어 열연 코일이 평판 탄소강 시장의 32.89%를 차지했습니다. 아연 도금 제품 시장 규모는 아시아 조선업의 회복과 인도 가전 산업의 성장에 힘입어 확대될 것으로 예측됩니다. 냉연 코일은 자동차용 프레스 부품에 필수적인 소재이지만, 두께가 점점 얇아지는 대체재로 인해 대체재와 관련된 과제에 직면해 있습니다. 전기 아연 도금 강판은 자동차의 노출 패널 분야에서 규모는 작지만 꾸준한 틈새 시장을 유지하고 있습니다. 그 밖의 피복 평판 탄소강 제품은 식품 포장 및 태양광 지붕 사업 확대의 혜택을 받고 있습니다.

고객이 인증된 도막 두께를 중요시하는 가운데, 사내에 아연 도금 라인 및 연속 소둔 라인을 갖춘 제철소는 경쟁 우위를 점하고 있습니다. 중국에는 충분한 강판 생산 능력이 있기 때문에 조선소는 더 높은 기준을 요구할 수 있으며, 이것이 신규 진출기업들에게는 과제가 되고 있습니다. 아르셀로미탈은 전기차(EV)용 모터 공급 및 실리콘 등급 제품으로의 사업 다각화를 도모하기 위해 프랑스의 전기강판 생산 라인에 5억 유로(5억 8,550만 달러)를 투자했습니다. 액화천연가스(LNG)의 저장 및 극저온 특성에 대한 요구 사항으로 인해, 고급 선박용 강판은 고가에 거래되고 있습니다. 가전 제조업체들은 더 엄격한 판 두께 공차에 대해 추가 비용을 지불하고 있지만, 디지털 트윈 기술을 도입한 제철소라면 이를 확실하게 생산할 수 있습니다.

두께 2mm(mm) 미만의 박판 코일은 강성을 저해하지 않으면서 냉장고나 세탁기에 0.4-0.6mm 두께의 패널이 채택되는 추세에 힘입어 6.62%의 성장이 예상됩니다. 중후판은 보, 자동차 섀시, 해상 모노파일 등에서 활용도가 높아, 2025년에는 평판 탄소강 시장에서 41.92%의 점유율을 차지했습니다. 이 시장은 두께 편차를 0.5% 미만으로 줄여주는 디지털 롤 모델의 혜택을 받고 있으며, 이를 통해 가전 제조업체(OEM)는 특수한 폭의 강판을 국내에서 조달할 수 있게 되었습니다. 0.8mm 미만의 초박형 스트립은 포장 및 전기차용 적층판 분야에서 널리 사용되고 있습니다.

두께가 10mm를 초과하는 두꺼운 강판은 풍력 발전용 타워나 조선에 필수적이지만, 여전히 생산 능력의 제약을 받고 있어 인증받은 제철소에 가격 결정권을 부여하고 있습니다. 미국의 유틸리티 프로젝트가 중·후판 수요를 견인하고 있는 반면, 아파트 건설은 스터드용 박판 강재 수요를 뒷받침하고 있습니다. 중국의 과잉 생산 능력이 중후판의 이익률에 압박을 가하고 있지만, 품질 향상으로 인해 수출 기회가 확대되고 있습니다. 데이터에 따르면, 아시아에서 생산되는 가전제품의 대당 철강 사용량은 감소하고 있지만, 생산량 증가가 재료 절감분을 상쇄하고 있어 철강 수요 증가는 지속되고 있습니다.

지역별 분석

2025년, 아시아태평양은 평판 탄소강 시장의 44.37%를 차지했으며, 2031년까지 연평균 6.72%의 성장률이 예상됩니다. 이러한 성장은 인도의 11억 1,000만 루피(1,182만 달러) 규모의 인프라 계획과 아세안(ASEAN) 국가들의 제조업 확장에 힘입어 이루어지고 있으며, 이로 인해 강판 코일 수요가 유지되고 있습니다. 중국의 ‘1.5 : 1’ 생산 능력 감축 규정에 따라 조강 생산량은 9억 6,081만 톤으로 감소했으나, 중국은 여전히 최저 비용공급국으로서 지역 가격 안정에 기여하고 있습니다. 인도의 1인당 철강 소비량은 93kg으로, 세계 평균인 219kg보다 훨씬 낮아, 평판 탄소강 시장에 큰 성장 여지가 있음을 보여줍니다. 한편, 일본과 한국은 정부 주도의 혁신 기금의 지원을 받아 선박용 강판이나 자동차용 전자강판 등 고부가가치 제품에 주력하고 있습니다.

북미에서는 탈탄소화와 리쇼어링 노력이 중시되고 있습니다. 신일철주금의 149억 달러에 달하는 US 스틸 인수에는 열간 압연 공장의 현대화와 DRI(직접 환원철) 생산 능력 확충을 목적으로 한 110억 달러 규모의 추가 자본 계획이 포함되어 있습니다. 2026년 1월의 건설 착공액은 연율로 환산해 1조 2,400억 달러에 달했으나, 이러한 성장은 산발적으로 진행되는 메가 프로젝트에 의존하고 있습니다. 섹션 122 관세로 인해 가동률은 79.1%로 상승했으나, 하류 가공업체 입장에서는 비용 증가 요인이 되고 있습니다. 캐나다와 멕시코는 자동차 조립 사업의 니어쇼어링 혜택을 누리고 있지만, 미국의 정책 전환에 대해서는 여전히 취약한 입장에 놓여 있습니다.

유럽은 탄소 규제와 치솟는 에너지 비용에 대처하는 데 고심하고 있습니다. 아르셀로미탈의 덩케르크 전기로와 마르디크의 전기강판 생산 라인은 고철을 원료로 하는 저탄소 철강 생산으로의 전환을 상징합니다. EU와 영국의 철강 수요는 최대 2,500만 톤의 강판이 필요한 해상 풍력 발전 프로젝트에 힘입어 2026년에는 3.2% 회복될 것으로 예측됩니다. 독일과 프랑스는 송전망 현대화 및 전기차 밸류체인에 대한 투자를 추진하고 있습니다. 한편, CIS(독립국가연합)의 철강 공급은 제재 조치로 인해 아시아로 방향을 전환하고 있습니다. 남미의 성장은 브라질의 철광석 수출과 현지 건설 활동에 좌우됩니다. 중동에서는 에미레이트 스틸 알칸이 생산 능력을 550만 톤으로 확대하는 등 자급자족을 목표로 하는 움직임이 두드러지고 있습니다. 만안 지역의 제철소들은 CBAM(탄소국경조정조치)의 구제 조치를 활용하여, 그린 프리미엄 강판을 유럽으로 수출할 수 있는 체제를 갖추고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the flat carbon steel market size is projected to be USD 661.67 billion in 2025, USD 700.25 billion in 2026, and reach USD 929.60 billion by 2031, growing at a CAGR of 5.83% from 2026 to 2031.

This report is Segmented by Product Type (Hot Rolled Coil, Cold Rolled Coil, and More), Thickness (Ultra-Thin (Less Than 0. 8 Mm) and More), Production Route (Basic Oxygen Furnace (BOF) and More), End-Use Application (Home Appliances and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Flat Carbon Steel Market Trends and Insights

Rising Demand in Automotive and Shipbuilding

Automotive electrification maintains steel content at approximately 1,200 kilograms per vehicle, including up to 100 kilograms of electrical steel, sustaining cold-rolled coil demand despite a plateau in unit production. Asian shipyards face three-year backlogs for liquefied natural gas (LNG) carriers, requiring high-toughness plate grades and premium coatings, which support pricing for shipbuilding steel. In 2024, India added 65 million white goods, increasing galvanized coil volumes, though thinner gauges reduced per-unit steel usage. China's focus on improving scrap quality following the Hong Kong International Convention for the Safe and Environmentally Sound Recycling of Ships is raising feed costs for electric arc furnace (EAF) mills supplying automotive stampers. South Korea's Hyper-Gap Vision 2040 program is driving demand for advanced plate in liquefied carbon dioxide (CO2) carriers and dual-fuel ships.

Global Infrastructure and Appliance Build-Out

U.S. construction starts reached an annualized USD 1.24 trillion in January 2026, with nearly USD 20 billion attributed to just three megaprojects, introducing volatility to the flat carbon steel market. India's INR 1,110 million (USD 11.82 million) infrastructure pipeline supports a projected 252 million tons of finished steel demand by fiscal year (FY) 2034. The Association of Southeast Asian Nations (ASEAN)'s USD 3.1 trillion development program is boosting regional coil flows under the Regional Comprehensive Economic Partnership (RCEP) while reducing reliance on Chinese imports. Heating, ventilation, and air conditioning (HVAC) shipments declined by 20% in 2025 to 7.7 million units, negatively impacting sheet volumes for cabinets and ducts. In the Middle East, demand remains steady at approximately 50 million tons, driven by projects like NEOM and Vision 2030, which drive heavy plate and structural beam consumption.

Volatile Iron-Ore and Coking-Coal Prices

U.S. metallurgical coal exports are projected to rise to 53.4 million short tons by 2026, affecting global coke supplies and increasing furnace costs. Disruptions in Brazilian mining operations and port delays in Australia have caused significant monthly fluctuations in iron-ore prices, impacting mill working capital. Spot coking coal prices increased following shipping disruptions in the Middle East, further widening the cost difference between blast furnace (BF) and electric arc furnace (EAF) production routes. Additionally, blast furnace producers are facing increasing carbon fees, while EAF mills are dealing with scrap price increases, with busheling reaching USD 422.50 per gross ton. Higher diesel and power tariffs have also increased freight and melting costs, reducing profit margins across the Flat carbon steel industry.

Other drivers and restraints analyzed in the detailed report include:

- Offshore Wind Tower Build-Out

- OEM Scope-3 Goals Driving Green Flat Steel

- Persistent Global Over-Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Galvanized sheet and coil are projected to grow at a rate of 6.47% by 2031. Hot rolled coil accounted for 32.89% of the flat carbon steel market share in 2025, supported by demand for structural beams, ship plates, and automotive panels. The market size for galvanized products is expected to expand alongside Asia's shipbuilding recovery and India's growing appliance industry. Cold-rolled coil, while essential for automotive stampings, faces substitution challenges due to gauge-thinning alternatives. Electro-galvanized sheet maintains a small but steady niche in automotive exposed panels. Other coated flat steel products benefit from growth in food packaging and solar-roof initiatives.

Mills with in-house galvanizing and continuous annealing lines have a competitive advantage as customers prioritize certified coating weights. China's sufficient plate capacity enables shipyards to demand higher standards, creating challenges for new market entrants. ArcelorMittal has invested EUR 500 million (USD 585.5 million) in a French electrical-steel line to supply electric vehicle (EV) motors and diversify into silicon grades. Premium ship plates command higher prices due to requirements for liquefied natural gas (LNG) containment and cryogenic properties. Appliance manufacturers pay a premium for tighter thickness tolerances, which digital-twin mills can reliably produce.

Light-gauge coil under 2 millimeters (mm) is expected to grow at 6.62%, driven by the adoption of 0.4-0.6 mm panels in refrigerators and washing machines without compromising rigidity. Medium-gauge steel held a 41.92% share of the flat carbon steel market in 2025, owing to its versatility in beams, automotive chassis, and offshore monopiles. The market benefits from digital roll models that reduce gauge spreads to below 0.5%, enabling appliance original equipment manufacturers (OEMs) to source niche widths domestically. Ultra-thin strips below 0.8 mm support applications in packaging and EV laminations.

Heavy plates over 10 mm are essential for wind towers and shipbuilding but remain capacity-constrained, giving pricing power to qualified mills. U.S. utility projects are driving medium-gauge demand, while multifamily housing supports light-gauge steel for studs. Although Chinese overcapacity pressures mid-gauge margins, quality improvements are opening export opportunities. Data indicates that appliances produced in Asia require fewer kilograms of steel per unit, but rising production volumes offset material reductions, sustaining tonnage growth.

Geography Analysis

Asia-Pacific accounted for 44.37% of the flat carbon steel market in 2025 and is projected to grow at a rate of 6.72% through 2031. This growth is supported by India's INR 1,110 million (USD 11.82 million) infrastructure pipeline and the expansion of manufacturing in ASEAN countries, which sustains demand for steel coils. China's 1.5:1 capacity-swap rule reduced crude steel output to 960.81 million tonnes, yet the country remains the lowest-cost supplier, stabilizing regional prices. India's per-capita steel consumption stands at 93 kg, significantly below the global average of 219 kg, indicating substantial growth potential for the flat carbon steel market. Meanwhile, Japan and South Korea are focusing on high-value products such as ship plates and automotive electrical steel, supported by government-backed innovation funds.

North America emphasizes decarbonization and reshoring efforts. Nippon Steel's USD 14.9 billion acquisition of U.S. Steel includes an additional USD 11 billion capital plan aimed at modernizing hot-strip mills and increasing DRI capacity. Construction starts reached an annualized USD 1.24 trillion in January 2026, though growth depends on sporadic megaprojects. Section 122 tariffs have increased utilization rates to 79.1%, but they also raise costs for downstream fabricators. Canada and Mexico benefit from near-shoring vehicle assembly operations but remain vulnerable to shifts in U.S. policies.

Europe is navigating carbon regulations and high energy costs. ArcelorMittal's Dunkirk EAF and Mardyck electrical steel line highlight the transition to scrap-based, low-carbon steel production. Steel demand in the EU and UK is expected to recover by 3.2% in 2026, driven by offshore wind projects requiring up to 25 million tonnes of steel plate. Germany and France are investing in grid upgrades and electric vehicle value chains. Meanwhile, CIS steel supply is being redirected to Asia due to sanctions. South America's growth is tied to Brazilian iron ore exports and local construction activities. In the Middle East, efforts to achieve self-sufficiency are evident, with Emirates Steel Arkan increasing capacity to 5.5 million tonnes. Gulf mills are positioning themselves to export green-premium steel plates to Europe, benefiting from CBAM relief measures.

- AM/NS India

- ARCELORMITTAL

- BlueScope Steel Limited.

- China BaoWu Steel Group Corp. Ltd.

- Cleveland-Cliffs Inc.

- Gerdau S/A

- Hyundai Steel

- JFE Steel Corporation

- JSW

- LIBERTY Steel Group

- NIPPON STEEL CORPORATION

- Nucor Corporation

- POSCO

- SAIL

- Severstal

- SSAB AB

- Tata Steel

- Thyssenkrupp Steel Europe

- United States Steel Corporation

- voestalpine Stahl GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand in automotive and shipbuilding

- 4.2.2 Global infrastructure and appliance build-out

- 4.2.3 Cost-efficient high-strength grades in construction

- 4.2.4 Offshore-wind tower build-out (heavy-gauge plate)

- 4.2.5 OEM Scope-3 goals driving 'green flat steel'

- 4.2.6 Digital-twin yield optimisation (scrap-cut)

- 4.3 Market Restraints

- 4.3.1 Volatile iron-ore and coking-coal prices

- 4.3.2 Stringent carbon-emission regulations

- 4.3.3 Persistent global over-capacity

- 4.3.4 Scarce prime scrap for EAF decarbonisation

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Hot Rolled Coil

- 5.1.2 Cold Rolled Coil

- 5.1.3 Galvanized Sheet/Coil

- 5.1.4 Electro-Galvanized Sheet

- 5.1.5 Other Coated or Treated Flat Steel

- 5.2 By Thickness

- 5.2.1 Ultra-Thin (Less than 0.8 mm)

- 5.2.2 Light-Gauge (Less than 2 mm)

- 5.2.3 Medium-Gauge (2-10 mm)

- 5.2.4 Heavy-Gauge (Greater than 10 mm)

- 5.3 By Production Route

- 5.3.1 Basic Oxygen Furnace (BOF)

- 5.3.2 Electric Arc Furnace (EAF)

- 5.3.3 Hydrogen-DRI + EAF

- 5.4 By End-Use Application

- 5.4.1 Construction and Infrastructure

- 5.4.2 Automotive and Transportation

- 5.4.3 Home Appliances

- 5.4.4 Machinery and Industrial Equipment

- 5.4.5 Renewable Energy and Power Equipment

- 5.4.6 Shipbuilding and Marine

- 5.4.7 Other Applications

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Nordic Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 AM/NS India

- 6.4.2 ARCELORMITTAL

- 6.4.3 BlueScope Steel Limited.

- 6.4.4 China BaoWu Steel Group Corp. Ltd.

- 6.4.5 Cleveland-Cliffs Inc.

- 6.4.6 Gerdau S/A

- 6.4.7 Hyundai Steel

- 6.4.8 JFE Steel Corporation

- 6.4.9 JSW

- 6.4.10 LIBERTY Steel Group

- 6.4.11 NIPPON STEEL CORPORATION

- 6.4.12 Nucor Corporation

- 6.4.13 POSCO

- 6.4.14 SAIL

- 6.4.15 Severstal

- 6.4.16 SSAB AB

- 6.4.17 Tata Steel

- 6.4.18 Thyssenkrupp Steel Europe

- 6.4.19 United States Steel Corporation

- 6.4.20 voestalpine Stahl GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment