|

시장보고서

상품코드

2062356

열전도성 필러 분산제 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Thermally Conductive Filler Dispersants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

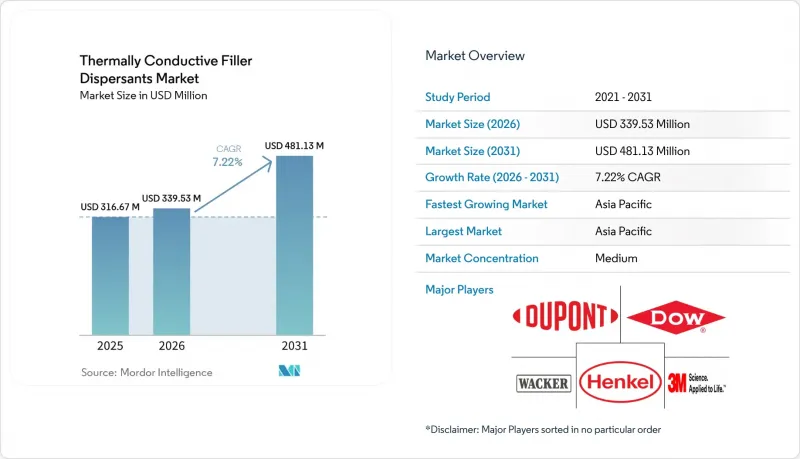

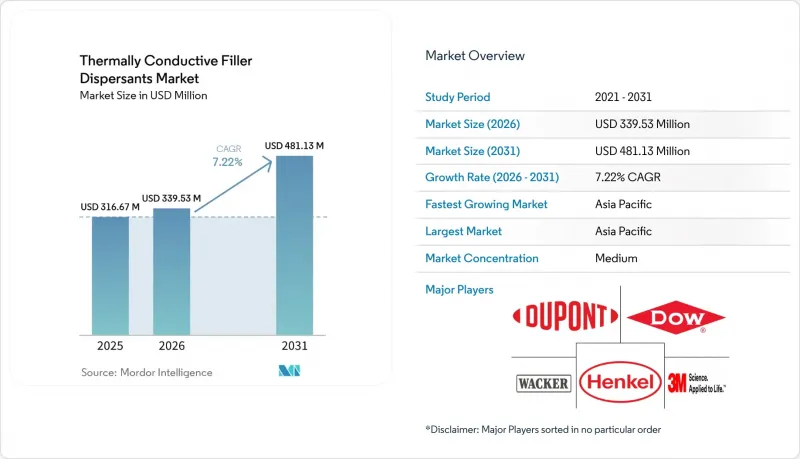

Mordor Intelligence에 의하면, 열전도성 필러 분산제 시장 규모는 2025년에 3억 1,667만 달러로 평가되었고 2026년 3억 3,953만 달러에서 2031년까지 4억 8,113만 달러에 이를 것으로 예측되며, 예측 기간 CAGR은 7.22%입니다(2026-2031년).

본 보고서는 필러의 유형(붕소 질화물, 알루미늄 산화물 등), 제형(액체 분산액 등), 용도(열 인터페이스 재료(TIM), 전기 절연성 컴파운드 등), 최종 사용자 산업(전자 등), 지역(아시아태평양, 북미 등)별로 세분화되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 열전도성 필러 분산제 시장 동향 및 분석

EV 배터리 및 파워 모듈의 열유속 밀도 급증

현재 300 Wh/kg 용량의 배터리 팩에서는 액체 냉각 및 침지 냉각이 주류를 이루고 있으며, 셀 탭의 국부적 열유속은 50 W/cm²를 초과하고 있습니다. 0.3mm의 틈새 내에서 5 W/m*K의 접착 성능을 유지하기 위해, 에보닉(Evonik)사의 ORTEGOL DA 801이나 듀폰(DuPont)사의 BETAMATE 2090과 같은 제품에는 Z축 방향의 ±0.2mm 팽창을 수용하고, 에너지를 대량으로 소비하는 오븐 경화를 불필요하게 만드는 폴리우레탄용 분산제가 사용되고 있습니다. 심천의 Feilonda 등 중국의 시스템 통합 업체들은 CATL과 협력하여 베퍼 챔버 어셈블리를 공동 설계하고, 완전한 열 모듈 내에 분산제를 통합함으로써 여유를 확보하고 있습니다. 그러나 침지 냉각이 보급됨에 따라, 10 ppm을 초과하는 잔류 이온 불순물은 여전히 과제로 남아 있습니다. 이들은 유전체의 비저항을 1 GΩ·cm 미만으로 낮추기 위해 초고순도 필러 등급으로의 전환이 진행되고 있습니다.

반도체 공정 미세화에 따른 핫스팟 관리

3D 적층형 고대역폭 메모리나 200W CPU의 경우, 패키지당 최대 4개의 TIM 인터페이스가 도입되며, 50nm 미만의 필러 간격을 유지하지 않는 한 층마다 열저항이 0.15 K cm²/W 증가합니다. 헨켈의 Bergquist TLF 6500 CGel-SF 및 인피니언의 인듐 합금 부착재에 관한 지침에 따르면, 25µ m의 본딩 라인 내에서 85 vol%의 세라믹 충전량을 안정화하고, 180°C의 리플로우 온도에서 침전을 방지하는 분산제가 요구됩니다. 이러한 첨단 패키징 기술의 발전으로 인해, 2026년까지 고고형분 페이스트 배합제 시장 규모는 8,500만 달러 증가할 것으로 예측됩니다.

고점도 시스템에서 폴리머와 필러의 상용성 한계

세라믹 함유율이 80부피%가 되면, 입자 사이의 틈이 분산제의 유체역학적 반지름의 2배 미만으로 줄어들기 때문에 입자 안정화 기능이 작동하지 않게 됩니다. 옥타데실 그래프트를 가진 병솔형 폴리실록산은 87.8%의 알루미나 함량과 8.181 W/m·K의 열전도도를 달성하지만, 선형 PDMS보다 가격이 40% 더 비싸기 때문에 그 용도는 AI 가속기로 한정되어 있습니다. 신뢰성 시험에서는 아민 말단을 가진 분산제가 이동하여, 500회의 열 사이클 후 전도도가 18% 저하되는 용해성 문제가 발생합니다. 반면, 포스폰산 에스테르계 변법에서는 전도율이 96%로 유지됩니다.

부문별 분석

2025년, 질화 붕소는 열전도성 필러 분산제 시장에서 34.22%의 점유율을 차지했습니다. 이는 면내 열전도율 300 W/m·K 및 체적 저항률 10¹³ Ω·cm라는 특성 때문입니다. 그러나 2031년까지 연평균 성장률(CAGR) 7.33%로 성장하고 있는 흑연 및 그래핀이 이 위치를 위협하고 있습니다. 이는 베트남 내 중국의 합성 흑연 생산 능력이 연간 400만 m² 증가하고 있으며, 인건비가 35% 저렴하다는 이점을 누리고 있기 때문입니다. 알루미늄 산화물은 3-5 W/m*K를 목표로 하는 비용 효율을 중시하는 용도에서 여전히 중요하며, 병솔형 폴리실록산 분산제는 재료 비용을 5분의 1로 낮추면서도 BN과의 성능 격차를 좁히고 있습니다.

실리콘 카바이드는 120 W/m·K의 열전도율을 자랑하며, 보닛 아래의 전자 기기에서 기계적 보강재로 널리 사용되고 있습니다. 단, 950°C에서의 산화 공정으로 인해 가공 비용이 1kg당 8-12달러 증가합니다. 습기에 민감한 알루미늄 질화물은 여전히 틈새 소재이지만, 파릴렌 C를 이용한 패시베이션의 이점을 누리고 있습니다. 이를 통해 끓는 물에 담근 후에도 97%의 열전도율을 유지할 수 있어, 항공우주 분야의 인증 절차를 거칠 수 있게 됩니다.

2025년 기준으로, 액체 분산계는 열전도성 필러 분산제 시장의 46.36%를 차지하고 있으며, 이는 15 Pa·s 미만의 점도로 인해 50μm 미만의 본딩 라인에 제트 도포가 가능하다는 점에 기인합니다. 그러나 페이스트 및 젤 유형은 데이터센터 사업자들이 펌프아웃(재료 유출) 없이 ±0.5mm의 적층 공차를 견딜 수 있는 소재에 대한 수요에 힘입어, 2031년까지 연평균 성장률(CAGR) 8.02%로 성장하고 있습니다. Bergquist TGF 10000은 틱소트로피와 열적 성능이 공존할 수 있음을 입증하며, 1,000회 사이클에 걸쳐 10 W/m*K의 열전도율과 5% 미만의 두께 편차를 유지합니다.

분말 첨가제는 열가소성 컴파운드 제조업체를 지원하며, 한편 젤 형태의 열전도성 재료(TIM)는 쇼어 00 경도 60-70을 제공하여 불규칙한 형상에도 잘 맞습니다. 스크린 인쇄는 18%라는 틱소트로피성 개질제의 추가 첨가량을 고려하더라도, 유닛당 0.32달러의 인건비 절감으로 이어집니다. 고형분의 상한은 여전히 부피 비율 85%로 제한되어 있으며, 이 한도를 초과하면 디스펜싱 시 유동 개시 응력 문제가 발생합니다. 병 솔로 안정화되어 따르기 쉬운 액체는 이 임계값을 초과하지만, AI 서버로만 제한됩니다. 이 경우, 700W의 칩 부하로 인해 1kg당 28달러의 분산제 비용이 정당화됩니다.

지역별 분석

아시아태평양은 2025년 매출의 44.45%를 차지하며, 중국의 AI 서버 증설 및 한국의 특수 실리콘 사업 확대를 배경으로 2031년까지 연평균 성장률(CAGR) 8.38%로 성장할 전망입니다. 심천의 페이론다는 화웨이 및 BYD와의 제휴를 통해 2024년 매출이 50억 3,100만 위안(6억 9,300만 달러)에 달할 것이며, 2025년 이익 성장률은 110%를 넘어설 것이라고 보고했습니다. 가동률 97.47%를 유지하고 있는 중국의 시첸신자재는 인건비가 35% 저렴하다는 장점을 살리기 위해 베트남에 400만 제곱미터 규모의 합성 흑연 필름 생산 능력을 확충하고 있습니다. 한국에서는 와커(Wacker)와 덴카(Denka)의 투자를 바탕으로, 울산과 익산이 BN 및 실리콘 TIM의 혁신 거점으로 자리매김하고 있습니다.

북미에서는 미시간주에 위치한 듀폰의 배터리 기술 센터가 ‘인플레이션 억제법’의 조달 규정을 준수하고 있는 반면, 헨켈의 3,000만 달러 규모 브랜든 공장 확장으로 인해 2027년까지 버그퀴스트의 생산량은 40% 증가하여, 700W GPU를 사용하는 하이퍼스케일 데이터센터에 대한 공급이 강화될 것입니다. 캐나다 수요는 전기 버스 도입 의무와 밀접한 관련이 있는 반면, 멕시코는 2차 자동차 공장에 비용 최적화된 알루미나 TIM을 공급하고 있습니다.

유럽에서는 엄격한 REACH 규제가 기반이 되고 있어, 에너지 비용 급등으로 이익률이 압박받는 상황에서도 공급업체들은 저VOC 수성 분산액으로의 전환을 요구받고 있습니다. 다우는 영국과 독일에서의 실록산 생산 감축을 검토하고 있지만, 2029년 에틸렌 원료 통합을 목표로 하는 앨버타주의 Path2Zero 크래커 계획은 예정대로 추진하고 있습니다. 한편, OEM 업체들의 탈탄소화 노력에 힘입어 재활용이 가능한 열가소성 TIM의 도입이 가속화되면서, 바이오 화학 물질에 새로운 기회가 열리고 있습니다.

남미, 중동 및 아프리카의 합계 점유율은 낮은 수준을 유지하고 있습니다. 브라질의 플렉스 연료 하이브리드 차량과 사우디 아람코의 석유화학 사업 성장이 틈새 시장인 TIM 수요를 촉진하고 있지만, 현지 충전재 생산량이 제한적이라는 점이 급속한 보급을 저해하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the thermally conductive filler dispersants market size was valued at USD 316.67 million in 2025 and is estimated to grow from USD 339.53 million in 2026 to reach USD 481.13 million by 2031, at a CAGR of 7.22% during the forecast period (2026-2031).

This report is Segmented by Filler Type (Boron Nitride, Aluminum Oxide, and More), Formulation (Liquid Dispersions, and More), Application (Thermal Interface Materials (TIMs), Electrically-Insulating Compounds, and More), End-User Industry (Electronics, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Thermally Conductive Filler Dispersants Market Trends and Insights

Surge in EV Battery and Power-Module Heat-Flux Density

Liquid and immersion cooling are now dominant in 300 Wh/kg battery packs, where local heat fluxes exceed 50 W/cm2 at cell tabs. To maintain 5 W/m*K bond lines within 0.3 mm gaps, products like Evonik's ORTEGOL DA 801 and DuPont's BETAMATE 2090 utilize polyurethane-compatible dispersants that accommodate +-0.2 mm z-axis expansion while eliminating the need for energy-intensive oven curing. Chinese integrators, such as Shenzhen Feirongda, collaborate with CATL to co-design vapor-chamber assemblies, embedding dispersants within complete thermal modules to capture margins. However, as immersion cooling becomes more widespread, residual ionic impurities above 10 ppm remain a challenge, as they reduce dielectric-fluid resistivity below 1 GΩ*cm, prompting a shift toward ultrapure filler grades.

Semiconductor Node-Shrink Driven Hotspot Management

3D-stacked high-bandwidth memory and 200 W CPUs introduce up to four TIM interfaces per package, increasing thermal resistance by 0.15 K cm2/W per layer unless sub-50 nm filler spacing is maintained. Henkel's Bergquist TLF 6500 CGel-SF and Infineon's indium-alloy attach guidelines require dispersants that stabilize 85 vol% ceramic loadings within 25 µm bond lines while preventing sedimentation at 180 °C reflow temperatures. These advancements in packaging are expected to create an incremental addressable market of USD 85 million for high-solids paste formulations by 2026.

Polymer-Filler Compatibility Limits in High-Viscosity Systems

At ceramic loadings of 80 vol%, steric stabilization fails as inter-particle gaps shrink below twice the dispersant's hydrodynamic radius. Bottlebrush polysiloxanes with octadecyl grafts achieve 87.8 vol% alumina and 8.181 W/m*K but are 40% more expensive than linear PDMS, limiting their application to AI accelerators. Compatibility issues arise during reliability tests, where amine-terminated dispersants migrate, reducing conductivity by 18% after 500 thermal cycles. In contrast, phosphonate variants retain 96% conductivity.

Other drivers and restraints analyzed in the detailed report include:

- Safety-Driven Shift to Low-VOC, Halogen-Free Dispersants

- OEM Decarbonization Targets Favor Recyclable Chemistries

- PFAS Phase-Out Tightening Specialty-Solvent Availability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Boron nitride secured 34.22% of the thermally conductive filler dispersants market share in 2025, attributed to its 300 W/m*K through-plane conductivity and 1013 Ω*cm resistivity. However, graphite and graphene, expanding at a 7.33% CAGR through 2031, are challenging this position as Chinese synthetic-graphite capacity increases by 4 million m2 annually in Vietnam, benefiting from 35% lower labor costs. Aluminum oxide remains critical for cost-sensitive applications targeting 3-5 W/m*K, with bottlebrush polysiloxane dispersants reducing the performance gap to BN at one-fifth of the material cost.

Silicon carbide, with its 120 W/m*K conductivity, is the preferred choice for mechanical reinforcement in under-hood electronics, although its 950 °C oxidation step adds USD 8-12 per kg in processing costs. Moisture-sensitive aluminum nitride remains a niche material but benefits from Parylene-C passivation, which retains 97% conductivity after boiling-water immersion, enabling aerospace qualification pipelines.

Liquid dispersions held 46.36% of the thermally conductive filler dispersants market in 2025, supported by viscosities below 15 Pa*s that allow jetting into sub-50 µm bond lines. However, paste and gel systems are growing at an 8.02% CAGR through 2031, driven by data-center operators' need for materials that can withstand +-0.5 mm stack tolerances without pump-out. Bergquist TGF 10000 demonstrates that thixotropy can coexist with thermal performance, maintaining 10 W/m*K and less than 5% thickness drift over 1,000 cycles.

Powder additives support thermoplastic compounders, while gel TIMs offer Shore 00 hardness of 60-70, conforming to irregular geometries. Screen printing reduces labor costs by USD 0.32 per unit, even after accounting for the 18% dose premium of thixotropic modifiers. The solids content ceiling remains at 85 vol%; exceeding this limit results in yield stress issues during dispensing. Bottlebrush-stabilized pourable liquids surpass this threshold but are limited to AI servers, where USD 28 per kg dispersant costs are justified by 700 W chip loads.

Geography Analysis

Asia-Pacific generated 44.45% of 2025 revenue and is set to grow at an 8.38% CAGR through 2031 on the back of China's AI-server build-outs and South Korea's specialty silicone expansions. Shenzhen Feirongda reported RMB 5.031 billion (USD 693 million) 2024 revenue and greater than 110% 2025 profit growth from partnering with Huawei and BYD. China's Siquan New Materials, running 97.47% utilization, is adding 4 million m2 synthetic-graphite film capacity in Vietnam to leverage 35% cheaper labor. South Korea, buoyed by Wacker and Denka investments, positions Ulsan and Iksan as hubs for BN and silicone TIM innovation.

In North America, DuPont's Battery Technology Center in Michigan aligns with Inflation Reduction Act sourcing rules, while Henkel's USD 30 million Brandon expansion will raise Bergquist output 40% by 2027 to serve hyperscale data centers using 700 W GPUs. Canada's demand is tied to electric-bus mandates, whereas Mexico supplies cost-optimized alumina TIMs to Tier 2 automotive plants.

Europe is anchored by strict REACH rules, pushing suppliers toward low-VOC water-based dispersions even as high energy costs squeeze margins. Dow is evaluating UK and German siloxane cutbacks but keeps its Alberta Path2Zero cracker on schedule for 2029 ethylene feedstock integration. Meanwhile, OEM decarbonization pledges accelerate recyclable thermoplastic TIM adoption, giving an opening to bio-based chemistries.

South America and Middle-East and Africa collectively hold lower shares. Brazil's flex-fuel hybrids and Saudi Aramco's petrochemical growth spur niche TIM demand, but limited local filler production continues to hinder rapid uptake.

- 3M

- Arkema

- ATLANTA

- Avient Corporation

- Cabot Corporation

- Dow

- DuPont

- Evonik Industries AG

- Henkel AG & Co. KGaA

- Momentive

- Resonac Holdings Corporation

- SANYO CHEMICAL, LTD.

- Shin-Etsu Chemical Co., Ltd.

- Sumitomo Chemical Co., Ltd.

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in EV battery and power-module heat-flux density

- 4.2.2 Semiconductor node-shrink driven hotspot management

- 4.2.3 Safety-driven shift to low-VOC, halogen-free dispersants

- 4.2.4 OEM decarbonisation targets favour recyclable dispersant chemistries

- 4.2.5 Hybrid BN + graphene filler networks lowering dispersant loadings

- 4.3 Market Restraints

- 4.3.1 Polymer/filler compatibility limits in high-viscosity systems

- 4.3.2 PFAS phase-out tightening specialty-solvent availability

- 4.3.3 Shear-induced damage to high-aspect-ratio fillers during compounding

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Filler Type

- 5.1.1 Boron Nitride (BN)

- 5.1.2 Aluminum Oxide (Al2O3)

- 5.1.3 Aluminum Nitride (AlN)

- 5.1.4 Silicon Carbide (SiC)

- 5.1.5 Graphite and Graphene

- 5.1.6 Ceramic Microspheres and Glass Beads

- 5.1.7 Other Filler Types (Carbon Black, Hybrid)

- 5.2 By Formulation

- 5.2.1 Liquid Dispersions

- 5.2.2 Powder Additives

- 5.2.3 Paste/Gel Systems

- 5.3 By Application

- 5.3.1 Thermal Interface Materials (TIMs)

- 5.3.2 Electrically-Insulating Compounds

- 5.3.3 Thermal Greases and Adhesives

- 5.3.4 Gap Fillers and Potting Compounds

- 5.3.5 Encapsulation and Underfills

- 5.3.6 Other Applications

- 5.4 By End-user Industry

- 5.4.1 Electronics

- 5.4.2 Automotive and Transportation

- 5.4.3 Building and Construction

- 5.4.4 Power Generation

- 5.4.5 Industrial

- 5.4.6 Aerospace

- 5.4.7 Other End-user Industries (Medical, etc.)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 ATLANTA

- 6.4.4 Avient Corporation

- 6.4.5 Cabot Corporation

- 6.4.6 Dow

- 6.4.7 DuPont

- 6.4.8 Evonik Industries AG

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Momentive

- 6.4.11 Resonac Holdings Corporation

- 6.4.12 SANYO CHEMICAL, LTD.

- 6.4.13 Shin-Etsu Chemical Co., Ltd.

- 6.4.14 Sumitomo Chemical Co., Ltd.

- 6.4.15 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment