|

시장보고서

상품코드

2062359

오디오 코덱 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Audio Codec - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

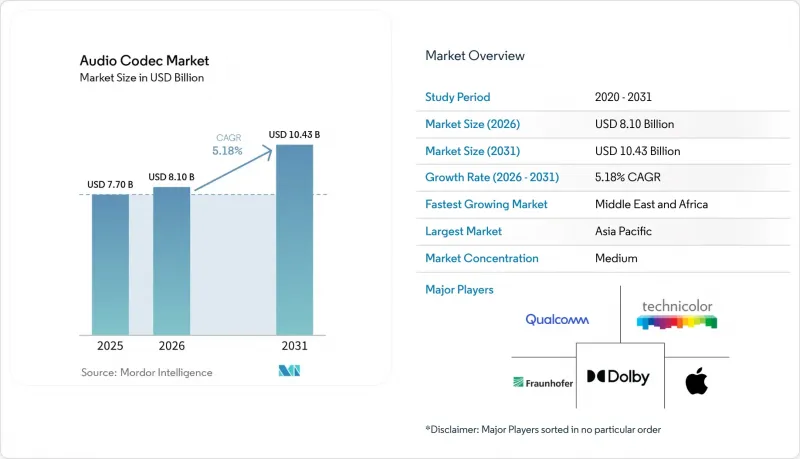

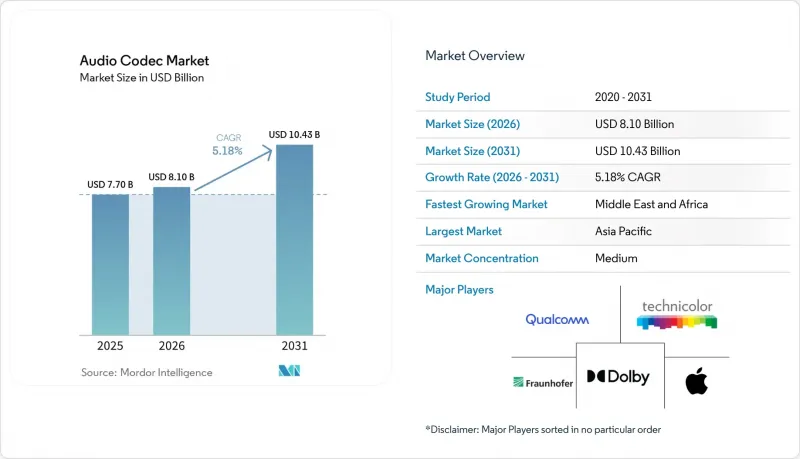

오디오 코덱 시장 규모는 2025년 77억 달러로 평가되었습니다. 2026년 81억 달러로 확대되고 2026년부터 2031년에 걸쳐 CAGR은 5.18%를 나타내, 2031년에는 104억 3,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 구성 요소별(하드웨어 DSP IP 코어, 소프트웨어 코덱), 코덱 유형별(AAC, AptX 변형, SBC, 돌비 코덱, 기타 코덱 유형), 압축 방식별(손실 압축, 무손실 압축), 최종 이용 산업별(소비자 가전, 미디어 및 엔터테인먼트, 통신·VoIP, 기타), 지역별(북미, 남미, 유럽, 아시아태평양, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 오디오 코덱 시장 동향과 인사이트

스트리밍 오디오 및 비디오의 보급 확대

스트리밍 플랫폼은 최대 256kbps의 AAC로 제한된 메인스트림 계층과 무손실 또는 공간 오디오 카탈로그를 제공하는 프리미엄 계층으로 양분되고 있으며, 이에 따라 로열티 수익원이 클라우드에서의 디코딩에서 스마트폰, 스마트 스피커, 인포테인먼트 헤드 유닛에 내장된 기기 측 IP로 이동하고 있습니다. 3세대 파트너십 프로젝트(3GPP)는 릴리스 18에서 몰입형 음성·오디오 서비스(IVAS) 코덱을 최종 확정함으로써, 통신 사업자들이 5G 데이터 요금제에 공간 오디오를 포함시킬 수 있도록 했습니다. 방송 엔지니어들은 이미 객체 기반 MPEG-H 트랙을 삽입해 두었으며, 시청자들은 자신에게 맞춘 해설을 선택할 수 있게 되었습니다. 이는 기존의 스테레오 코덱으로는 서버에서 재인코딩하지 않고서는 재현할 수 없는 기능입니다. ITU-R 음량 가이드라인을 준수함으로써, 적응형 비트레이트 스트림 전체에서 재생 레벨이 균일하게 유지되어, 청취자의 청취 피로로 인한 이탈이 감소합니다.

스마트폰 및 무선 이어폰 출하 대수 증가

2025년 전 세계 스마트폰 출하 대수는 약 12억 대로 보합세를 보였으나, 현재 중급형 단말기에는 aptX Lossless, aptX Adaptive, LC3를 하나의 라이브러리로 통합한 Qualcomm Snapdragon Sound와 같은 멀티 코덱 스택이 탑재되어 있습니다. 같은 해, TWS 이어폰의 출하 대수는 3억 5,000만 대를 돌파했으며, 각 브랜드가 20밀리초 미만의 지연 시간을 요구하는 능동형 소음 제거 기능을 추가함에 따라 평균 판매 가격이 상승했습니다. 삼성의 ‘Galaxy Buds3 Pro’는 SBC, AAC, Samsung Scalable Codec 중에서 동적으로 가장 적합한 코덱을 선택하여 음절 현상을 최소화합니다. Bluetooth Special Interest Group(SIG)의 자료에 따르면, LC3 인증을 획득한 기기의 누적 출하 대수는 5,000만 대를 넘어섰으며, 그 대부분은 보청기에 집중되어 있습니다. 보청기의 경우, 비트레이트를 50% 줄임으로써 배터리 수명을 연장할 수 있습니다.

높은 라이선스 비용과 특허 풀의 복잡성

라이선싱 비용은 AAC의 경우 기기당 0.10-0.98달러를 청구하지만, MPEG-H나 IVAS 레이어가 추가되면 고급차용 헤드 유닛의 경우 로열티 총액이 1.50달러를 초과할 가능성이 있습니다. 연간 최저 보장액 요건은 소량 생산 OEM 제조업체에 부담을 주어, 로열티가 없는 SBC나 LC3로의 전환을 촉진하고 있습니다. IVAS가 세 번째 라이선싱 계층을 추가함에 따라, 중국의 스마트폰 브랜드들은 FRAND 조건의 의무화를 요구하며 로비를 펼치고 있습니다. 독일과 미국의 법원에서 진행 중인 프라우호퍼와 돌비 간의 상호 소송은 불확실성을 가중시키고 있으며, 아프리카와 남미의 수입업체들은 특허 풀과 직접 협상해야 하는 경우 선적 지연에 직면하고 있습니다.

부문별 분석

소프트웨어 프레임워크 시장은 OEM 업체들이 펌웨어 업데이트를 통해 출시 후 새로운 형식을 도입함에 따라, 2031년까지 연평균 성장률(CAGR) 6.01%의 성장세를 유지하고 있습니다. 이는 하드웨어 IP로는 구현할 수 없는 민첩성입니다. ARM의 Helium 벡터 기능을 탑재한 Cortex-M85는 5달러 미만의 마이크로컨트롤러에서 LC3 및 Opus 디코딩이 가능해짐에 따라, IoT 웨어러블용 오디오 코덱 시장을 개척하고 있습니다. 자동차 분야에서는 ISO 26262 안전 평가에서 결정론적 처리 경로가 요구되기 때문에 여전히 하드웨어가 선호되고 있습니다. 또한, 시노프시스는 AAC 및 aptX를 통합한 사전 검증된 DSP 코어를 제공하고 있으며, 이 코어들은 자동차용 시스템 온 칩에 탑재되어 있습니다.

그럼에도 불구하고, 2025년 시점에서도 하드웨어 DSP IP 코어는 오디오 코덱 시장 점유율의 60.19%를 차지하고 있었습니다. 자동차용 인포테인먼트 및 스마트 TV 제조업체들은 채널당 전력 소비를 최소화하기 위해 고정형 가속기에 의존하고 있습니다. 그러나 테슬라와 같은 소프트웨어 정의 아키텍처는 코덱의 업데이트 주기를 반도체 로드맵과 분리시켜, 새로운 칩의 테이프아웃을 기다릴 필요 없이 LC3 및 IVAS로의 신속한 전환을 가능하게 합니다.

AAC는 iOS 및 Android에서 필수 디코딩 방식으로 채택되어 2025년 매출의 45.27%를 차지했습니다. 퀄컴의 aptX나 소니의 LDAC는 프리미엄 블루투스 헤드폰에 채택되고 있지만, SBC는 로열티가 필요하지 않기 때문에 저가형 액세서리에 계속해서 채택되고 있습니다. 돌비의 포트폴리오(AC-3, AC-4, 돌비 애트모스 포함)는 스트리밍 및 자동차 분야에서 오브젝트 기반 렌더링 라이선싱이 확대됨에 따라 2031년까지 5.95% 성장할 것으로 전망됩니다.

차세대 기술의 가치는 압축에서 오서링 및 렌더링으로 점차 이동하고 있습니다. 현재 1만 곡을 넘는 ‘Dolby Atmos Music’은 최대 128개의 오디오 오브젝트를 인코딩하므로, 재생 기기는 모든 스피커 어레이에 맞추어 출력을 최적화할 수 있습니다. 그러나 중국의 전기차 제조업체들은 대당 50달러가 넘는 라이선스 비용을 피하기 위해 MPEG-H를 선택하고 있으며, 이는 비용에 민감한 지역에서 돌비에게 가격 책정상의 과제가 되고 있음을 시사합니다.

지역별 분석

아시아태평양은 2025년 매출의 34.83%를 차지하며, 중국이 스마트폰 및 TWS(완전 무선 이어폰) 생산을 주도했습니다. 지역 정세에 따라 중국의 각 OEM 기업들은 미국 지적 재산권에 대한 의존도를 낮추기 위해 화웨이(Huawei HWA) 등의 국산 코덱 채택을 추진하고 있습니다. Bluetooth SIG에 따르면, LC3의 보급률은 저가형 액세서리에서는 뒤처지고 있지만, 프리미엄급 LDAC 및 aptX Lossless를 탑재한 기기에서는 급속히 확대되고 있습니다.

중동 및 아프리카는 기존 인프라의 제약을 받지 않는 통신 사업자들이 5G 방송 및 IVAS를 전개하고 있는 것을 배경으로, 연평균 성장률(CAGR) 5.85%를 나타낼 것으로 전망됩니다. UAE의 통신사는 두바이에서 MPEG-H 시범 운영을 실시하고, 다국어 스포츠 중계를 스트리밍으로 전송했습니다. 또한, 남아프리카공화국의 디지털 TV 전환 과정에서 AC-4 및 MPEG-H 디코더의 사용이 의무화됨에 따라, 지적재산권 소유자들은 일시적인 라이선스 수입의 급증이 예상됩니다.

북미와 유럽에서는 유닛 수 증가라기보다는 코덱의 고급화가 진행되고 있습니다. 유럽 방송사들의 듀얼 코덱 도입으로 인해 HE-AAC의 단계적 폐지가 더디게 진행되고 있으며, 북미의 전기차 제조업체들은 차별화 요소로 Dolby Atmos를 통합하고 있습니다. 남미는 여전히 가격에 민감하며, 그레이 마켓을 통한 수입품은 적절한 라이선스 없이 출하되는 경우가 많아 풀로의 회수율을 떨어뜨리고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the audio codec market size is expected to grow from USD 7.70 billion in 2025 to USD 8.10 billion in 2026 and is forecast to reach USD 10.43 billion by 2031 at 5.18% CAGR over 2026-2031.

This report is Segmented by Component (Hardware DSP IP Cores, Software Codecs), Codec Type (AAC, Aptx Variants, SBC, Dolby Codecs, Other Codec Types), Compression Type (Lossy, Lossless), End-Use Industry (Consumer Electronics, Media and Entertainment, Telecom and VoIP, and More), and Geography (North America, South America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Audio Codec Market Trends and Insights

Surge in Streaming Audio and Video Adoption

Streaming platforms are splitting into mainstream tiers capped at 256 kilobits-per-second AAC and premium tiers offering lossless or spatial catalogs, which transfers royalty flows from cloud decoding to device-side IP embedded in phones, smart speakers, and infotainment head units. The 3rd Generation Partnership Project (3GPP) finalized the Immersive Voice and Audio Services (IVAS) codec in Release 18, allowing telecom operators to bundle spatial audio in 5G data plans. Broadcast engineers are already inserting object-based MPEG-H tracks so viewers can select personalized commentary, a feature that legacy stereo codecs cannot replicate without server re-encoding. Compliance with ITU-R loudness guidelines maintains uniform playback levels across adaptive-bit-rate streams, reducing churn caused by listener fatigue.

Smartphone and Wireless-Earbud Volume Growth

Global smartphone shipments steadied at roughly 1.2 billion units in 2025, but mid-tier devices now integrate multi-codec stacks such as Qualcomm Snapdragon Sound, which packages aptX Lossless, aptX Adaptive, and LC3 in one library. Shipments of TWS earbuds crossed 350 million the same year, and average selling prices rose as brands added active noise cancellation that demands sub-20 millisecond latency. Samsung's Galaxy Buds3 Pro dynamically selects among SBC, AAC, and Samsung Scalable Codec to minimize dropouts. Bluetooth Special Interest Group (SIG) data show LC3-certified devices topping 50 million cumulative units, concentrated in hearing aids, where 50% lower bit rate extends battery life.

High Licensing Cost and Patent-Pool Complexity

Via Licensing charges USD 0.10-0.98 per unit for AAC, while MPEG-H and IVAS layers can push total royalties beyond USD 1.50 on premium car head units. Minimum annual guarantees squeeze low-volume OEMs and divert them toward royalty-free SBC or LC3. Chinese smartphone brands have lobbied for compulsory FRAND terms as IVAS adds a third licensing layer. Cross-complaints between Fraunhofer and Dolby in German and U.S. courts heighten uncertainty, and importers in Africa and South America face shipment delays when they must negotiate directly with patent pools.

Other drivers and restraints analyzed in the detailed report include:

- Standardization of Codecs in 5G Broadcast

- Growing Adoption of Bluetooth LE Audio (LC3) in Hearables

- Rise of Royalty-Free Codecs (Opus, FLAC)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software frameworks added 6.01% CAGR momentum through 2031 as OEMs use firmware pushes to insert new formats post-launch, an agility that hardware IP cannot match. ARM's Cortex-M85 with Helium vectors now decodes LC3 and Opus on sub-USD 5 microcontrollers, unlocking the audio codec market for IoT wearables. The automotive domain still favors hardware because ISO 26262 safety assessments demand deterministic paths, and Synopsys supplies pre-verified DSP cores with embedded AAC and aptX that ship in automotive system-on-chips.

Hardware DSP IP cores, nonetheless, held 60.19% audio codec market share in 2025. Automotive infotainment and smart-TV manufacturers rely on fixed accelerators to minimize per-channel power. Yet software-defined architectures such as Tesla's are decoupling codec refresh cycles from silicon roadmaps, allowing a fast pivot to LC3 or IVAS without waiting for a new chip tape-out.

AAC retained 45.27% of 2025 revenue because iOS and Android include it as a mandatory decode. Qualcomm aptX and Sony LDAC play in premium Bluetooth headphones, whereas SBC stays in budget accessories for its zero-royalty position. Dolby's portfolio, spanning AC-3, AC-4, and Dolby Atmos, is growing 5.95% to 2031 as streaming and automotive segments license object-based rendering.

Next-gen value is shifting from compression to authoring and rendering. Dolby Atmos Music, now exceeding 10,000 tracks, encodes up to 128 audio objects so playback devices can tailor output to any speaker array. Chinese EV makers, however, choose MPEG-H to avoid per-vehicle fees topping USD 50, signaling a pricing challenge for Dolby in cost-sensitive geographies.

Geography Analysis

Asia-Pacific accounted for 34.83% of 2025 revenue, with China dominating smartphone and TWS production. Regional politics spur Chinese OEMs to adopt homegrown codecs such as Huawei HWA to cut reliance on U.S. IP. The Bluetooth SIG notes LC3 penetration lags in low-cost accessories but leaps ahead in premium LDAC or aptX Lossless devices.

The Middle East and Africa are forecast to grow at a 5.85% CAGR, driven by operators deploying 5G broadcast and IVAS without legacy constraints. UAE carriers ran MPEG-H trials in Dubai, streaming multi-language sports commentary, and South Africa's digital TV transition mandates AC-4 and MPEG-H decoders, creating a one-off licensing windfall for IP owners.

North America and Europe see premiumization of codecs rather than unit growth. European broadcasters' dual-codec period slows HE-AAC sunset, and North American EV makers integrate Dolby Atmos as a differentiator. South America remains price sensitive; gray-market imports often ship without proper licenses, reducing capture rates for pools.

- Dolby Laboratories Inc.

- Qualcomm Technologies Inc.

- Fraunhofer-Gesellschaft

- Sony Corporation

- Microsoft Corporation

- DTS LLC (Subsidiary of Xperi Inc.)

- Audio Coding Technologies LLC

- RealNetworks Inc.

- Alibaba DAMO Academy

- Meta Platforms Inc.

- Samsung Electronics Co., Ltd.

- Bose Corporation

- Harman International Industries Inc.

- Synopsys Inc.

- Cadence Design Systems Inc.

- ARM Ltd.

- Imagination Technologies Ltd.

- Analog Devices Inc.

- Cirrus Logic Inc.

- Texas Instruments Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Streaming Audio and Video Adoption

- 4.2.2 Smartphone and Wireless-Earbud Volume Growth

- 4.2.3 Standardization of Codecs in 5G Broadcast

- 4.2.4 Growing Adoption of Bluetooth LE Audio (LC3) in Hearables

- 4.2.5 Automotive In-Cabin Personalised Sound Zones

- 4.2.6 On-Device AI-Enabled Neural Codecs for IoT Sensors

- 4.3 Market Restraints

- 4.3.1 High Licensing Cost and Patent-Pool Complexity

- 4.3.2 Rise of Royalty-Free Codecs (Opus, FLAC)

- 4.3.3 Edge-AI Compression Reducing External Codec Demand

- 4.3.4 Sustainability-Driven Bit-Rate Caps in Consumer Devices

- 4.4 Industry Value-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware DSP IP Cores

- 5.1.2 Software Codecs (Media Frameworks)

- 5.2 By Codec Type

- 5.2.1 AAC (Advanced Audio Coding)

- 5.2.2 aptX / aptX HD / aptX Lossless

- 5.2.3 SBC (Sub-Band Coding)

- 5.2.4 Dolby Codecs

- 5.2.5 Other Codec Types

- 5.3 By Compression Type

- 5.3.1 Lossy

- 5.3.2 Lossless

- 5.4 By End-Use Industry

- 5.4.1 Consumer Electronics

- 5.4.1.1 Smartphones

- 5.4.1.2 True Wireless Stereo / Earbuds

- 5.4.1.3 Smart Speakers

- 5.4.1.4 Televisions and Set-Top Boxes

- 5.4.1.5 Automotive Infotainment

- 5.4.2 Media and Entertainment

- 5.4.2.1 Music and Podcast Streaming

- 5.4.2.2 Broadcast and OTT Video

- 5.4.3 Telecom and VoIP

- 5.4.4 Enterprise Unified Communications

- 5.4.5 Other End-Use Industries

- 5.4.1 Consumer Electronics

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia and New Zealand

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.5 Middle East & Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Dolby Laboratories Inc.

- 6.4.2 Qualcomm Technologies Inc.

- 6.4.3 Fraunhofer-Gesellschaft

- 6.4.4 Sony Corporation

- 6.4.5 Microsoft Corporation

- 6.4.6 DTS LLC (Subsidiary of Xperi Inc.)

- 6.4.7 Audio Coding Technologies LLC

- 6.4.8 RealNetworks Inc.

- 6.4.9 Alibaba DAMO Academy

- 6.4.10 Meta Platforms Inc.

- 6.4.11 Samsung Electronics Co., Ltd.

- 6.4.12 Bose Corporation

- 6.4.13 Harman International Industries Inc.

- 6.4.14 Synopsys Inc.

- 6.4.15 Cadence Design Systems Inc.

- 6.4.16 ARM Ltd.

- 6.4.17 Imagination Technologies Ltd.

- 6.4.18 Analog Devices Inc.

- 6.4.19 Cirrus Logic Inc.

- 6.4.20 Texas Instruments Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment