|

시장보고서

상품코드

2062384

데님 마감제 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Denim Finishing Agents - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

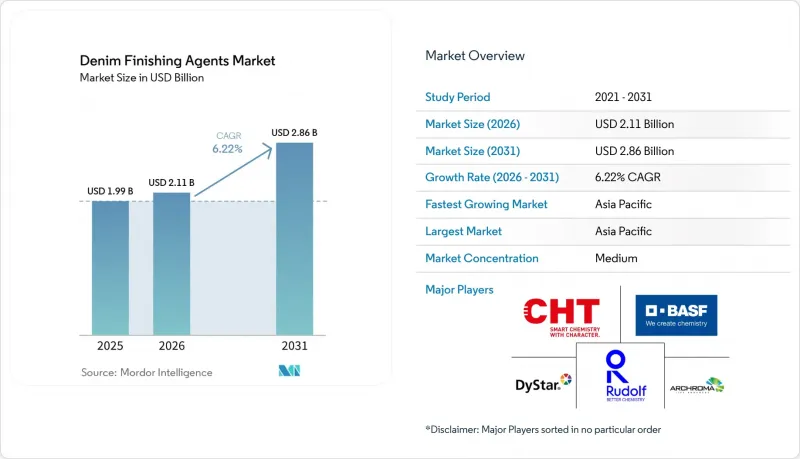

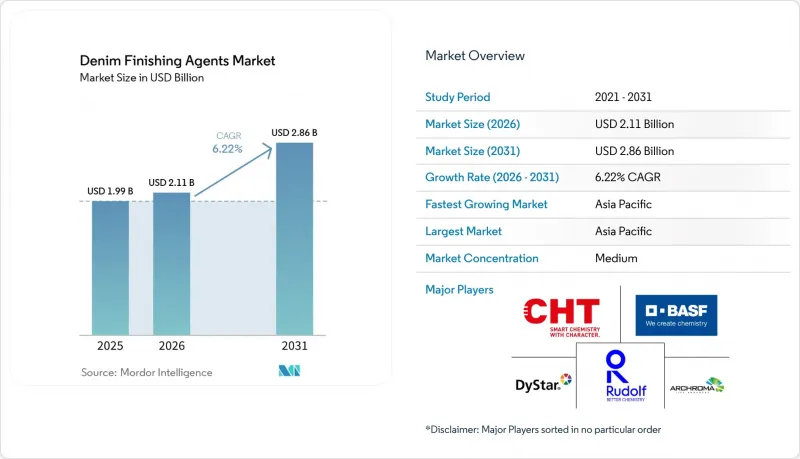

Mordor Intelligence에 의하면, 데님 마감제 시장 규모는 2025년 19억 9,000만 달러로 평가되었습니다. 2026년 21억 1,000만 달러로 확대되고 2026년부터 2031년에 걸쳐 CAGR은 6.22%를 나타내, 2031년까지 28억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 유형(섬유유연제, 수지 등), 화학적 특성(실리콘계, 비실리콘계 등), 용도 단계(스톤 워시, 효소 워시 등), 최종 사용자 산업(패션 및 의류, 섬유 제조 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 데님 마감제 시장 동향 및 분석

패션 및 캐주얼 의류 분야의 전 세계 데님 소비 증가

세계 데님 원단 생산량은 증가하고 있으며, 아시아태평양의 공장이 총 생산량의 3분의 2 가까이 차지하고 있습니다. 드레스 코드의 완화 및 데님이 단순한 작업복이 아닌 라이프스타일의 필수 아이템으로 재정의된 점이 데님 마감제 시장의 성장을 지속적으로 견인하고 있습니다. 패스트 패션 브랜드들은 디자인부터 매장 진열까지의 주기를 4주 미만으로 단축하고 있으며, 이에 따라 워시하우스가 마무리 공정을 신속하게 전환할 수 있는 모듈식 효소 블렌드에 대한 수요가 증가하고 있습니다. 2025년, 베트남에서는 4억 9,500만 미터의 데님 원단이 생산되었으며, 각 브랜드가 중국 이외의 조달처를 다각화함에 따라 전년 대비 10% 증가했습니다. 마찬가지로 인도에서도 유럽연합(EU)으로부터의 수주 증가에 힘입어 생산량은 10% 증가한 16억 5,000만 미터에 달했습니다.

지속 가능한 바이오 화학 약제로의 전환

소매업체들이 환경 부하가 낮은 것으로 입증된 원료를 점점 더 많이 채택함에 따라, 데님 마감제 시장에서는 효소계 및 기타 바이오 화학제품이 가장 빠른 성장세를 보이고 있습니다. 아크로마(Archroma)의 ‘FiberColors’ 시리즈는 양모 폐기물의 50%를 반응성 염료로 전환하는 기술로, 석유화학 유래 대체재에 비해 물 사용량을 30% 줄여줍니다. 노보자임스(Novozymes)는 아황산수소나트륨을 사용하지 않고 인디고를 산화시키는 라카아제의 변종을 도입하여, 폐수 내 화학적 산소 요구량(COD)을 최대 50%까지 줄이고 있습니다. 그러나 방적 공장은 세계 유기농 섬유 표준(GOTS) 인증을 받은 약제에 대해 15-20%의 가격 프리미엄을 부담해야 하기 때문에 방글라데시와 같이 가격에 민감한 지역에서는 문제가 되고 있습니다. BASF의 ‘Loopamid’는 사용 후 섬유에서 추출한 폴리아미드 6(PA6) 폴리머로, 공급업체의 순환형 원료에 대한 폭넓은 노력을 상징합니다.

인증된 생분해성 대체재의 높은 비용

세계 유기농 섬유 표준(GOTS) 인증에는 지속적인 감사 비용이 발생하기 때문에 EBITDA 마진이 5% 미만인 방적 공장에게는 부담이 되고 있습니다. 마찬가지로, Bluesign 인증을 받으려면 신청비와 연간 갱신 비용이 필요합니다. 인증된 효소 혼합물은 기존의 셀룰라아제보다 18-25% 더 비싸기 때문에 동남아시아의 방적 공장은 규정 준수 및 수익성을 신중하게 평가해야 합니다. 그러나 Archroma사의 ‘Denim HALO’는 장기적인 브랜드 계약을 바탕으로 할 경우, 40-56%의 물 절약 효과가 12-15%의 가격 상승을 상쇄할 수 있음을 입증하고 있습니다.

부문별 분석

효소는 연평균 성장률(CAGR) 6.58%로 가장 빠른 성장이 예상되는 반면, 섬유 유연제는 최대 시장 점유율을 유지하며 2025년에는 데님 마감제 시장 매출의 38.22%를 차지했습니다. 공장에서는 물 소비량을 줄이고 작업자의 건강 위험을 최소화하기 위해, 경석보다 셀룰라아제와 라카아제를 혼합한 재료를 선호하는 경향이 강해지고 있습니다. 수지 시장 점유율은 안정적인 양상을 보이고 있으며, 특히 주름 유지 용도로 사용되는 포름알데히드 무첨가 제품이 수요를 뒷받침하고 있습니다. 또한, 인디고 재부착이 발생하기 쉬운 레이저 가공 공정을 중심으로 방염제에 대한 수요가 증가하고 있습니다.

Archroma사의 데님용 HALO 효소 패키지는 공정 시간을 최대 30% 단축할 수 있음이 입증되어, 튀르키예와 방글라데시 등 시장에서 채택이 확대되고 있습니다. 마찬가지로, Novozymes사의 Primagreen 역시 생산 주기를 단축하여, 방적 공장이 추가 설비 투자를 하지 않고도 생산량을 늘릴 수 있게 해줍니다. 탈풀제 및 표백제는 데님 생산 전반의 동향과 일치하지만, 유럽연합(EU)의 독성 규제에 대한 우려로 인해 식물 유래 대체제로의 전환이 진행되고 있습니다.

2025년에는 실리콘계 제품이 데님 마감제 시장에서 40.46%의 점유율을 차지했지만, 효소계 및 기타 바이오 배합제는 연평균 성장률(CAGR) 6.69%로 가장 높은 성장률을 나타낼 것으로 전망됩니다. EU의 사이클로실록산 규제가 시행되고 있는 지역에서는 비실리콘계 지방산 에스테르와 폴리에틸렌 왁스가 주목을 받고 있습니다. 폴리우레탄이나 아크릴 공중합체 등의 나노 및 폴리머 분산액은 이염 문제 없이 고급스러운 마감을 구현하기 위해 점점 더 많이 사용되고 있습니다.

CHT Germany GmbH의 생분해성 폴리에틸렌 왁스 분산액은 미국의 아웃도어 브랜드들 사이에서 인기를 끌고 있는 반면, BASF의 루프아미드 PA6는 버진 석유화학제품을 포함하지 않는 수지 코팅을 가능하게 합니다. 인증 비용은 여전히 보급의 걸림돌이 되고 있지만, 데님 마감제 업계에서는 투명성이 중요한 요건으로 대두되고 있습니다.

지역별 분석

2025년, 아시아태평양은 전 세계 매출의 43.34%를 차지했으며, 중국의 생산량 30억 미터와 인도의 16억 5,000만 미터가 이를 주도했습니다. 방글라데시와 베트남은 공급망 다각화를 추구하는 해외 투자의 뒷받침을 받아 각각 생산량이 10% 성장했습니다. 캄보디아와 인도네시아를 포함한 아세안(동남아시아국가연합)의 신흥 시장은 중견 방적 공장을 유치하고 있는 반면, 태국은 케미라사가 2025년에 계획한 생산 능력 확대의 혜택을 누리고 있습니다. 아시아태평양 시장은 2031년까지 연평균 6.56%의 성장률을 보일 것으로 전망됩니다.

북미는 니어쇼어링 노력과 ZDHC(유해 화학물질 배출 제로) 인증을 받은 화학 공정에 대한 브랜드 요건의 뒷받침을 받아 여전히 2위 시장을 차지하고 있습니다. 유럽은 수량 기준의 성장세가 둔화되고는 있지만, REACH(화학물질의 등록, 평가, 허가 및 제한)에 따른 실록산 규제와 2026년 10월 발효 예정인 프랑스의 환경 라벨 표시 의무화 정책을 통해 계속해서 세계 기준에 영향을 미치고 있습니다. 남미는 완만한 성장세를 보이고 있으며, 특히 브라질에서 솔베이의 시설 개보수 작업이 주목받고 있습니다. 이는 현지에서 특수 원료 공급에 대한 신뢰를 반영한 것입니다. 중동 및 아프리카의 역할은 비교적 미미하지만, 튀르키예는 예외입니다. 튀르키예는 EU(유럽연합)로의 수출 기회를 활용하여, 구매자의 요구 사항을 충족시키기 위해 알크로마의 순환형 염료를 도입하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the denim finishing agents market size is expected to grow from USD 1.99 billion in 2025 to USD 2.11 billion in 2026 and is forecast to reach USD 2.86 billion by 2031 at 6.22% CAGR over 2026-2031.

This report is Segmented by Type (Softening Agents, Resins, and More), Chemistry (Silicone, Non-Silicone, and More), Application Stage (Stone Washing, Enzyme Washing, and More), End-User Industry (Fashion and Apparel, Textile Manufacturing, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Denim Finishing Agents Market Trends and Insights

Rising Global Denim Consumption in Fashion and Casual Wear

Global denim fabric production has increased, with mills in the Asia-Pacific region contributing nearly two-thirds of the total output. The shift toward relaxed dress codes and the repositioning of denim as a lifestyle staple, rather than solely workwear, continue to drive growth in the denim finishing agents market. Fast-fashion brands have reduced design-to-shelf cycles to under four weeks, fueling demand for modular enzyme blends that enable wash houses to switch finishes rapidly. In 2025, Vietnam produced 495 million meters of denim, marking a 10% increase as brands diversified their sourcing away from China. Similarly, India experienced a 10% rise in production, reaching 1.65 billion meters, supported by increasing orders from the European Union (EU).

Shift Toward Sustainable and Bio-Based Chemical Agents

Enzyme-based and other bio-based chemistries are experiencing the fastest growth in the denim finishing agents market as retailers increasingly adopt verified low-impact inputs. Archroma's FiberColors line, which converts 50% wool waste into reactive dyes, reduces water usage by 30% compared to petrochemical alternatives. Novozymes has introduced laccase variants that oxidize indigo without the use of sodium hydrosulfite, reducing effluent Chemical Oxygen Demand (COD) by up to 50%. However, mills face a 15-20% price premium for Global Organic Textile Standard (GOTS)-certified agents, which poses challenges in price-sensitive regions like Bangladesh. BASF's Loopamid, a polyamide 6 (PA6) polymer derived from post-consumer textiles, highlights a broader commitment among suppliers to circular feedstocks.

High Cost of Certified Biodegradable Alternatives

Global Organic Textile Standard (GOTS) certification involves recurring audit fees, creating challenges for mills operating on EBITDA margins below 5%. Similarly, Bluesign approval requires an application fee and annual renewal costs. Certified enzyme blends are priced 18-25% higher than conventional cellulase, requiring Southeast Asian mills to carefully evaluate compliance and profitability. However, Archroma's Denim HALO has demonstrated that 40-56% water savings can offset a 12-15% price increase when supported by long-term brand contracts.

Other drivers and restraints analyzed in the detailed report include:

- Demand for Customized Soft-Touch and Sensory Denim

- Laser and Ozone Finishing Boosting Specialty-Chem Demand

- Volatile Supply of Specialty Silicones and Enzymes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Enzymes are expected to achieve the fastest growth with a 6.58% Compound Annual Growth Rate (CAGR), while softening agents are projected to maintain the largest share, accounting for 38.22% of the Denim finishing agents market revenue in 2025. Mills increasingly prefer cellulase and laccase blends over pumice, reducing water consumption and minimizing health risks for workers. The market share for resins remains stable, with formaldehyde-free variants catering to crease-retention applications. Demand for anti-back-staining agents is rising, particularly in laser workflows, which are prone to indigo redeposition.

Archroma's Denim HALO enzyme package has demonstrated a reduction in process time by up to 30%, driving adoption in markets like Turkey and Bangladesh. Similarly, Novozymes' Primagreen has shortened production cycles, enabling mills to increase throughput without additional capital investment. Desizing and whitening agents are aligned with overall denim production trends, though concerns over European Union (EU) toxicity regulations are prompting a shift toward plant-based alternatives.

Silicones are projected to hold a 40.46% share of the Denim finishing agents market in 2025, but enzyme-based and other bio-based formulations are forecast to achieve the highest growth, with a 6.69% CAGR. Non-silicone fatty-acid esters and polyethylene waxes are gaining traction in regions where EU restrictions on cyclic siloxanes are in place. Nano and polymer dispersions, such as polyurethane and acrylic copolymers, are increasingly used to deliver a premium finish without migration issues.

CHT Germany GmbH's biodegradable polyethylene-wax dispersion is gaining popularity among U.S. outdoor brands, while BASF's loopamid PA6 enables resin coatings free from virgin petrochemicals. Although certification costs remain a barrier to widespread adoption, transparency is becoming a critical requirement in the Denim finishing agents industry.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 43.34% of global revenue, driven by 3.0 billion meters of production from China and 1.65 billion meters from India. Bangladesh and Vietnam each achieved a 10% growth in output, supported by foreign investments seeking diversified supply chains. Emerging ASEAN (Association of Southeast Asian Nations) markets, including Cambodia and Indonesia, are attracting mid-tier mills, while Thailand benefits from Kemira's planned capacity expansion in 2025. The Asia-Pacific market is projected to grow at a rate of 6.56% through 2031.

North America remains the second-largest market, supported by near-shoring initiatives and brand requirements for ZDHC (Zero Discharge of Hazardous Chemicals)-approved chemical processes. Europe, while experiencing slower volumetric growth, continues to influence global standards through REACH (Registration, Evaluation, Authorization and Restriction of Chemicals) siloxane restrictions and France's mandatory environmental labeling policy, set to take effect in October 2026. South America shows modest growth, highlighted by Solvay's facility upgrade in Brazil, reflecting confidence in localized specialty supply. The Middle East and Africa play a smaller role, with the exception of Turkey, which capitalizes on its export access to the EU (European Union) and integrates Archroma's circular dyes to meet buyer requirements.

- Americos Industries INC

- Archroma

- Asutex

- BASF

- CHT Germany GmbH

- DyStar Singapore Pte Ltd

- Fashion Chemicals GmbH & Co. KG

- Fineotex Chemical Limited

- Giovanni Bozzetto S.p.A.

- Huntsman

- Indokem Ltd

- Indokem Ltd.

- Kemin Industries, Inc.

- Novozymes A/S

- Resil Chemicals Pvt. Ltd.

- RUDOLF Holding SE & Co. KG

- Sarex

- Synthomer plc

- Tanatex Chemicals B.V.

- Zydex Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising global denim consumption in fashion and casual wear

- 4.2.2 Shift toward sustainable and bio-based chemical agents

- 4.2.3 Demand for customised soft-touch and sensory denim

- 4.2.4 Laser / ozone finishing boosting specialty-chem demand

- 4.2.5 AI-driven digital dosing platforms optimise chemical use

- 4.3 Market Restraints

- 4.3.1 High cost of certified biodegradable alternatives

- 4.3.2 Volatile supply of specialty silicones and enzymes

- 4.3.3 Mandatory traceability / carbon-label audits raise compliance costs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Softening Agents

- 5.1.2 Enzymes

- 5.1.3 Resins

- 5.1.4 Anti-back Staining Agents

- 5.1.5 Desizing Agents

- 5.1.6 Whitening/Brightening Agents

- 5.1.7 Others (Ozone Neutralizers, Anti-odor, Anti-microbial)

- 5.2 By Chemistry

- 5.2.1 Silicone

- 5.2.2 Non-silicone (fatty acid, polyethylene)

- 5.2.3 Enzyme/Bio-based

- 5.2.4 Nano and Polymer dispersions

- 5.3 By Application Stage

- 5.3.1 Stone Washing

- 5.3.2 Enzyme Washing

- 5.3.3 Resin Coating/Over-dye

- 5.3.4 Laser/Ozone Finishing

- 5.3.5 Garment Washing and Soft-finish

- 5.4 By End-user Industry

- 5.4.1 Fashion and Apparel

- 5.4.2 Textile Manufacturing

- 5.4.3 Industrial and Workwear

- 5.4.4 Home Textiles

- 5.4.5 Accessories and Footwear

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Nordic Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Americos Industries INC

- 6.4.2 Archroma

- 6.4.3 Asutex

- 6.4.4 BASF

- 6.4.5 CHT Germany GmbH

- 6.4.6 DyStar Singapore Pte Ltd

- 6.4.7 Fashion Chemicals GmbH & Co. KG

- 6.4.8 Fineotex Chemical Limited

- 6.4.9 Giovanni Bozzetto S.p.A.

- 6.4.10 Huntsman

- 6.4.11 Indokem Ltd

- 6.4.12 Indokem Ltd.

- 6.4.13 Kemin Industries, Inc.

- 6.4.14 Novozymes A/S

- 6.4.15 Resil Chemicals Pvt. Ltd.

- 6.4.16 RUDOLF Holding SE & Co. KG

- 6.4.17 Sarex

- 6.4.18 Synthomer plc

- 6.4.19 Tanatex Chemicals B.V.

- 6.4.20 Zydex Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment