|

시장보고서

상품코드

2062393

쿨 루프 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Cool Roof - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

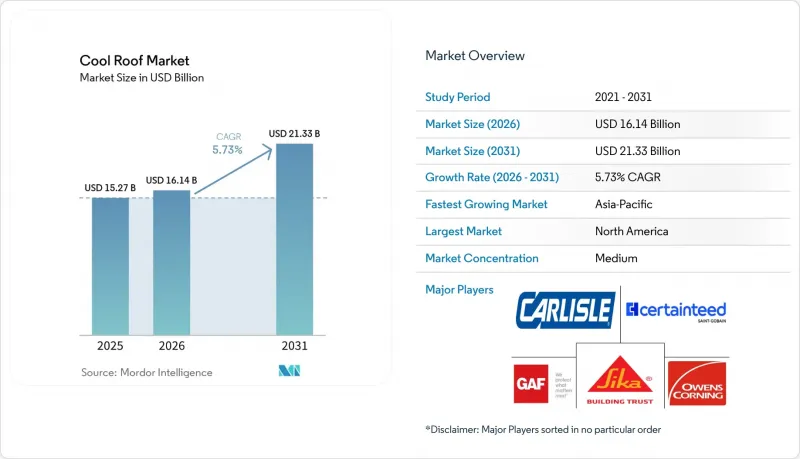

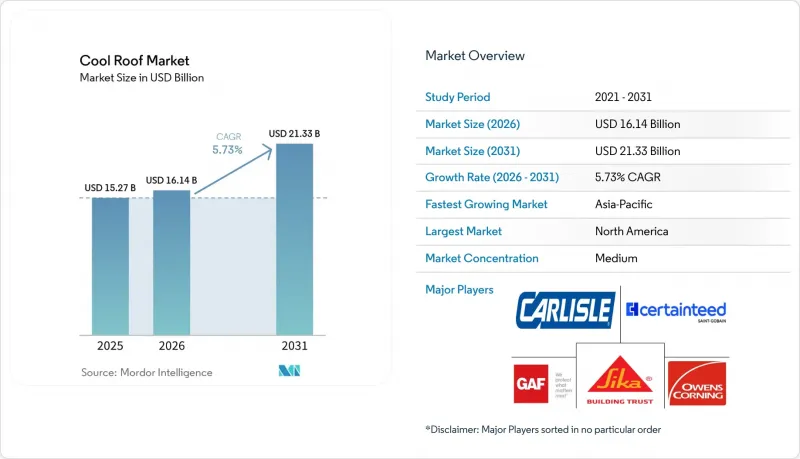

Mordor Intelligence에 의하면, 쿨 루프 시장 규모는 2025년에 152억 7,000만 달러로 평가되었고 2026년 161억 4,000만 달러에서 2031년까지 213억 3,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 5.73%를 나타낼 전망입니다.

본 보고서는 지붕의 유형(저경사 지붕, 급경사 지붕, 평지붕), 재료의 유형(쿨 루프 코팅, 단층막 등), 코팅의 화학 조성(아크릴, 엘라스토머, 실리콘 등), 용도(상업용 건물, 주택, 기타), 지역(아시아태평양, 북미, 유럽, 기타)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 쿨 루프 시장 동향과 인사이트

에너지 효율 규제 및 탄소 중립 의무

각 관할 구역에서는 건축 기준에 최소 SRI(일사 반사율) 기준치를 직접 명시함으로써, 기존에 개발업자가 반사성 지붕 대신 추가 단열재를 사용하는 것을 허용했던 상충되는 선택지를 배제하고 있습니다. 2030년까지 신축 건물의 탄소 중립을 목표로 하는 유럽 지침에 따르면, 건축가는 설계 과정의 초기 단계에서 쿨 루프를 도입해야 합니다. 한편, 중국의 성능 기준 GB 55015-2021에서는 약 30%의 에너지 절감 목표를 달성하기 위해 반사율이 높은 지붕 자재의 사용이 사실상 의무화되어 있습니다. 인도의 ‘Eco-Niwas Samhita 2024’는 지붕의 U값에 수치 상한을 도입하고, 경사가 완만한 지붕의 경우 초기 반사율 0.6을 의무화함으로써 쿨 루프 시장에 대한 강력한 규제 추진을 시사하고 있습니다. 미국에서는 LEED v5에서 경사가 완만한 지붕 구조에 대한 SRI(일사 반사율) 요건이(초기) 82에서(경과 후) 64로 상향 조정됨에 따라, 제조업체들은 오염으로 인한 열화를 견딜 수 있도록 코팅 배합을 재검토해야 하는 상황에 직면해 있습니다. 이러한 규제 변경은 사양 결정 과정을 가속화하고, 투자 회수 기간을 단축하며, 소재 혁신과 공급망 확장을 촉진하고 있습니다.

도시 열섬 현상 완화 프로그램

도시에서는 피크 시간대의 에너지 수요를 줄이고 여름철 주변 기온을 낮추기 위해 공공 인프라로서 쿨 루프에 대한 자금 지원이 늘어나고 있습니다. 예를 들어, 애틀랜타의 2025년 조례는 10,000제곱피트를 초과하는 상업용 건물에 적용되며, 2035년까지 누적 3억 1,000만 달러의 에너지 절감 효과가 예상됩니다. 하이데라바드의 이 프로그램은 2028년까지 3억제곱미터의 시공을 목표로 하고 있으며, 실내 온도를 최대 4.5°C 낮춤으로써 냉방 에너지의 대폭적인 절감을 실현할 예정입니다. 보스턴, 몬트리올, 캘리포니아주의 각 도시 등 다른 지역에서도 저소득층을 위한 건물에 쿨 루프 설치를 지원하는 보조금 제도를 운영하고 있습니다. 이러한 노력 덕분에 수요가 민간 개보수에서 공공 조달로 전환되고, 공급업체공급량이 안정됨에 따라 쿨 루프 시장 규모가 확대되고 있습니다.

기존 아스팔트 지붕에 비해 높은 초기 비용

반사 코팅의 비용은 평방피트당 0.75-2.50달러, TPO 막은 3.50-6.50달러인 반면, 기본적인 아스팔트 슁글은 평방피트당 1.00-3달러입니다. 이 50-150%의 가격 부담은 비용에 민감한 건설업체들에게 걸림돌이 되고 있습니다. 냉방 수요가 적은 온대 지역에서는 투자 회수 기간이 5년을 초과하는 경우가 있어, 쿨 루프는 선택적 개선 사항에 그치고 있습니다. 기존 지붕을 철거하고 처리하는 데는 추가로 평방피트당 1-2달러의 비용이 들지만, 철거가 필요 없는 개보수용 코팅재를 사용하면 투자 회수 기간을 5년 미만으로 단축할 수 있습니다. PACE 융자를 통해 고정자산세를 활용해 비용을 분산할 수 있는 제도는 캘리포니아주와 기타 몇몇 주에 도입이 집중되어 있습니다. 인센티브를 통해 이러한 비용 격차가 해소될 때까지는 가격이 시장 침투의 큰 걸림돌로 남아 있을 것입니다.

부문별 분석

2025년 매출액 중 저경사 지붕이 44.87%를 차지하고 있으며, 창고, 쇼핑몰, 공공시설의 쿨 루프 시장 점유율 측면에서 그 중요성이 부각되고 있습니다. 이러한 지붕은 냉각 효율을 높이기 위해 넓고 연속적인 면적을 활용하며, 막재를 뚫지 않고도 밸러스트가 장착된 태양광 패널을 설치할 수 있게 해줍니다. 2025년에 도입된 CRRC의 더욱 엄격한 3개 기후대 내후성 평가 프로토콜에 따라, 반사율이 장기간 유지되는 필름 소재가 우선적으로 채택되면서 쿨 루프 시장 확대를 뒷받침하는 프리미엄 PVC 및 TPO 제품에 대한 수요가 증가하고 있습니다. 경사가 급한 지붕에 설치할 경우, 반사형 아스팔트 슁글이 30-50%의 추가 비용을 수반하기 때문에 성장 속도는 완만합니다. 또한 주택 소유자들은 에너지 절약보다 외관을 우선시하는 경우가 많기 때문입니다. 그러나 GAF의 솔라 싱글 출시 소식은 비용이 더욱 낮아진다면 주택에서의 도입이 확대될 가능성이 있는 세트 판매형 가치 제안을 시사하고 있습니다.

2차 성장은 물류 업체들이 적층 지붕을 TPO 막으로 개보수하고 있는 추세에 힘입어, 2031년까지의 평지붕 시장에서 연평균 성장률(CAGR) 6.28% 달성에 기여하고 있습니다. 30년 통합 보증과 ENERGY STAR 인증은 경제적 매력을 높여주며, 자산운용사가 그린본드 취득 요건을 충족할 수 있도록 합니다. 또한, 지붕 시공업체들은 폐쇄형 회수 프로그램을 활용해 매립 처리 비용을 절감하고 환경 보호 노력을 강조하고 있으며, 이를 통해 쿨 루프는 기존 막재와의 차별화를 더욱 강화하고 있습니다.

쿨 루프용 코팅은 기존 기재 위에 덧발라 시공할 수 있어 철거 비용을 절감할 수 있었고, 비용 효율을 중시하는 개보수 공사에서 쿨 루프 시장 규모를 확대시킨 결과, 2025년에는 매출의 30.02%를 차지했습니다. 한편, 싱글 플라이 멤브레인은 가장 빠르게 성장하고 있는 부문으로, 2031년까지 연평균 성장률(CAGR)이 6.42%에 달할 전망입니다. 이는 새로운 물류 거점이나 데이터센터 건설 업체들이 20년의 보증 기간과 용접을 통한 밀폐 이음매를 선호하기 때문입니다. 아크릴계 엘라스토머는 여전히 가격 대비 성능이 뛰어나지만, 오염이 쌓이기 쉬운 경향이 있습니다. 한편, 실리콘이나 폴리우레탄·아크릴계 하이브리드 소재는 시간이 지나도 유지되는 우수한 반사율 덕분에 채택이 증가하고 있습니다. 아스팔트 슁글은 완만한 성장세를 보이고 있지만, 금속 지붕은 허리케인이 빈번히 발생하는 지역에서 풍압에 의한 들뜸 현상에 대한 내구성으로 인해 지지를 얻고 있습니다. 신규 출시된 나노 세라믹 탑코트는 오염 방지 효과를 제공하지만, 표준화된 시험을 통해 장기적인 성능이 입증되기 전까지는 틈새 시장 제품으로 남아 있습니다.

지역별 분석

북미는 캘리포니아주의 엄격한 건축 기준, 애틀랜타시의 의무화 조치, 그리고 LEED의 광범위한 도입에 힘입어 2025년 수요 점유율 35.50%로 1위를 차지했습니다. 연방 정부의 세제 혜택과 주 정부의 보조금이 초기 비용을 상쇄하며, 쿨 루프 시장 규모 확대를 지속적으로 이끌고 있습니다. 캐나다와 멕시코는 냉각 일수가 적어 작물 생장이 더딘 편이지만, 토론토와 몬테레이에서 진행된 도시 열섬 현상에 관한 연구가 지방 자치단체의 시범 프로그램을 뒷받침하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 6.88%를 기록하며 가장 높은 성장률을 보이고 있습니다. 인도의 지역별 확산은 2028년까지 300km² 규모의 설치를 목표로 하는 텔랑가나 주의 정책과 지붕의 U값에 상한선을 설정하는 ‘Eco-Niwas’ 규격에 힘입어 추진되고 있으며, 이로 인해 관민 양측의 입찰이 반사형 옵션으로 유도되고 있습니다. 중국의 에너지 기준인 ‘GB 55015-2021’에서는 신축 주택의 기준 충족을 위한 표준적인 수단으로 쿨 루프를 규정하고 있는 반면, 일본의 CASBEE 평가 제도는 고밀도 상업용 타워에서의 도입을 장려하고 있습니다.

유럽에서는 개정된 ‘건축물의 에너지 성능에 관한 지침’을 바탕으로 꾸준히 성장하고 있습니다. 독일과 프랑스는 EU의 의무를 SRI의 최소 기준을 반영한 국내 기준으로 적용하고 있지만, 북유럽 국가들은 겨울철 열 손실에 대한 우려로 인해 신중한 입장을 유지하고 있습니다. 남유럽에서는 여름철 극심한 더위를 완화하기 위해 이 기술이 점점 더 많이 도입되고 있으며, 밀라노나 마드리드 같은 도시의 높은 오염 수준이 오염에 강한 실리콘 코팅에 대한 수요를 촉진하고 있습니다.

중동 및 아프리카는 소규모 기반에서 점차 확장되고 있습니다. 사우디아라비아에서는 보조금 종료 후의 요금 제도 개혁으로 인해 강력한 경제적 인센티브가 발생하고 있습니다. 한편, UAE의 ‘에스티다마(Estidama)’ 인증에서는 아부다비와 두바이의 주요 프로젝트에 대해 반사형 지붕재의 사용을 의무화하고 있습니다. 남아프리카공화국의 성장은 완만하며, 하우텡 주를 제외한 지역에서는 냉방 수요가 낮은 점이 제약 요인으로 작용하고 있지만, 요하네스버그와 케이프타운의 친환경 건축 노력에 힘입어 성장세를 유지하고 있습니다. 브라질은 시험 기준을 ASTM에 부합시키고 국내 생산 능력을 강화하는 NBR 17162가 2024년에 공포됨에 따라, 남미 지역에서의 보급을 주도하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the cool roof market size was valued at USD 15.27 billion in 2025 and is estimated to grow from USD 16.14 billion in 2026 to reach USD 21.33 billion by 2031, at a CAGR of 5.73% during the forecast period (2026-2031).

This report is Segmented by Roof Type (Low-Slope Roofs, Steep-Slope Roofs, and Flat Roofs), Material Type (Cool Roof Coatings, Single-Ply Membranes, and More), Coating Chemistry (Acrylic, Elastomeric, Silicone, and More), Application (Commercial Buildings, Residential Buildings, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Cool Roof Market Trends and Insights

Energy-Efficiency Regulations and Zero-Carbon Mandates

Jurisdictions are incorporating minimum SRI thresholds directly into building codes, removing trade-off options that previously allowed developers to use additional insulation instead of reflective roofs. Europe's directive for zero-emission new buildings by 2030 requires architects to integrate cool roofs early in the design process, while China's GB 55015-2021 performance standards effectively mandate high-albedo roofing to achieve its approximately 30% energy-reduction target. India's Eco-Niwas Samhita 2024 introduces numeric caps on roof U-values and requires an initial reflectance of 0.6 for shallow slopes, signaling a strong regulatory push for the cool roof market. In the United States, LEED v5 increases SRI requirements to 82 (initial) and 64 (aged) for low-slope assemblies, driving manufacturers to reformulate coatings to withstand pollution-related degradation. These regulatory changes are expediting specification decisions, reducing payback periods, and fostering material innovation and supply chain scaling.

Urban Heat-Island Mitigation Programs

Cities are increasingly funding cool roofs as public infrastructure to reduce peak energy demand and lower ambient summer temperatures. For example, Atlanta's 2025 ordinance applies to commercial buildings over 10,000 ft2 and projects USD 310 million in cumulative energy savings by 2035. Hyderabad's program aims to cover 300 million m2 by 2028, achieving indoor temperature reductions of up to 4.5 °C and significant cooling energy savings. Other cities, such as Boston, Montreal, and various locations in California, offer grants to subsidize cool roof adoption for low-income buildings. These initiatives shift demand from private retrofits to public procurement, stabilizing supplier volumes and expanding the market footprint for cool roofs.

Higher Upfront Cost vs Conventional Asphalt Roofs

Reflective coatings cost between USD 0.75-2.50/ft2, and TPO membranes range from USD 3.50-6.50/ft2, compared to USD 1.00-3.00/ft2 for basic asphalt shingles. This 50-150% premium deters cost-sensitive builders. In temperate regions with lower cooling demands, payback periods can exceed five years, limiting cool roofs to discretionary upgrades. Tear-off disposal adds an additional USD 1-2/ft2, although retrofit coatings that avoid removal can reduce payback to under five years. While PACE financing spreads costs through property taxes, adoption remains concentrated in California and a few other states. Until incentives bridge this cost gap, price remains a significant barrier to wider market penetration.

Other drivers and restraints analyzed in the detailed report include:

- Rising Electricity Tariffs in Hot Climates

- Green-Building Certification Incentives

- Reflectivity Loss from Airborne Soot and Pollution

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Low-slope roofs accounted for 44.87% of 2025 revenue, emphasizing their importance in the cool roof market share for warehouses, malls, and institutional buildings. These roofs utilize large contiguous areas to enhance cooling efficiency and support ballasted solar arrays without membrane penetrations. CRRC's stricter three-climate aged-rating protocol, adopted in 2025, now prioritizes membranes with longer-lasting reflectance, increasing demand for premium PVC and TPO options that sustain cool roof market size gains. Steep-slope installations have slower growth as reflective asphalt shingles carry a 30-50% cost premium, and homeowners often prioritize aesthetics over energy savings. However, GAF's solar shingle launch suggests a bundled value proposition that could increase residential adoption if costs decrease further.

Secondary growth is driven by logistics operators retrofitting built-up roofs with TPO membranes, contributing to a 6.28% CAGR for flat roofs through 2031. Integrated 30-year warranties and ENERGY STAR certifications enhance financial appeal, enabling asset managers to qualify for green bonds. Roofers also utilize closed-loop take-back programs to reduce landfill fees and promote environmental credentials, further differentiating cool roofs from conventional membranes.

Cool roof coatings retained 30.02% revenue in 2025 due to their ability to overlay existing substrates, avoiding tear-off costs and expanding the cool roof market size across cost-sensitive retrofits. Single-ply membranes, however, are the fastest-growing segment, with a 6.42% CAGR through 2031, as builders of new logistics and data hubs prefer their 20-year warranties and weld-sealed seams. Acrylic elastomers remain cost-effective but are prone to dirt accumulation, while silicones and polyurethane-acrylic hybrids are increasingly specified for their superior aged reflectance. Asphalt shingles show modest growth, while metal roofs gain traction in hurricane-prone regions for their uplift resilience. Emerging nano-ceramic top-coats offer anti-soiling benefits but remain niche until standardized testing validates their long-term performance.

Geography Analysis

North America led 2025 demand with 35.50% share, driven by California's stringent building codes, Atlanta's city mandates, and widespread LEED adoption. Federal tax incentives and state grants offset upfront costs, sustaining the leading cool roof market size momentum. Canada and Mexico exhibit slower growth due to fewer cooling-degree days, though urban heat-island studies in Toronto and Monterrey are encouraging municipal pilot programs.

Asia-Pacific exhibits the fastest 6.88% CAGR through 2031. India's regional acceleration is supported by Telangana's policy targeting 300 km2 of installations by 2028 and Eco-Niwas caps on roof U-values, steering both public and private tenders toward reflective options. China's GB 55015-2021 energy code establishes cool roofs as the standard compliance path for new dwellings, while Japan's CASBEE assessments promote adoption in high-occupancy commercial towers.

Europe grows steadily on the back of the recast Energy Performance of Buildings Directive. Germany and France have translated EU mandates into national codes that incorporate SRI minimums, while Nordic countries remain cautious due to winter heat-loss concerns. Southern Europe is seeing increased adoption to mitigate extreme summer temperatures, though high pollution levels in cities like Milan and Madrid drive demand for dirt-resistant silicone coatings.

Middle-East and Africa expands from a smaller base. Saudi Arabia's post-subsidy tariff reforms create strong economic incentives, while the UAE's Estidama certification mandates reflective roofing for major projects in Abu Dhabi and Dubai. South Africa's growth is modest, limited by lower cooling needs outside Gauteng, but supported by green-building initiatives in Johannesburg and Cape Town. Brazil anchors South America's uptake following the 2024 publication of NBR 17162, which aligns testing standards with ASTM and boosts local production capacity.

- Akzo Nobel N.V.

- Asian Paints Ltd.

- Carlisle Companies Inc.

- CertainTeed, LLC

- Dow

- Elevate

- GACO

- GAF Materials LLC

- Huntsman International LLC

- IKO Industries Ltd.

- Johns Manville

- NanoTech Materials

- Nippon Paint Holdings Co., Ltd.

- Owens Corning

- PPG Industries, Inc.

- Saint-Gobain

- Sika AG

- SOPREMA Group

- TAMKO Building Products LLC

- Valspar

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Energy-efficiency Regulations and Zero-carbon Mandates

- 4.2.2 Urban Heat-Island Mitigation Programs

- 4.2.3 Rising Electricity Tariffs in Hot Climates

- 4.2.4 Green-Building Certification Incentives

- 4.2.5 Data-Centre Cooling Retrofits for Heat Reduction

- 4.3 Market Restraints

- 4.3.1 Higher Upfront Cost vs Conventional Asphalt Roofs

- 4.3.2 Reflectivity Loss from Airborne Soot and Pollution

- 4.3.3 Performance Degradation in Humid/Cloudy Zones

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Roof Type

- 5.1.1 Low-Slope Roofs

- 5.1.2 Steep-Slope Roofs

- 5.1.3 Flat Roofs

- 5.2 By Material Type

- 5.2.1 Cool Roof Coatings

- 5.2.2 Single-Ply Membranes (TPO, PVC, EPDM)

- 5.2.3 Asphalt Shingles

- 5.2.4 Metal Roofs

- 5.2.5 Tiles and Slates

- 5.2.6 Built-Up Roofs (BUR)

- 5.2.7 Modified Bitumen

- 5.2.8 Other Material Types (Green Roofs, Wood Shingles)

- 5.3 By Coating Chemistry

- 5.3.1 Acrylic

- 5.3.2 Elastomeric

- 5.3.3 Silicone

- 5.3.4 Polyurethane

- 5.3.5 Other Coating Chemistries (Aluminum, Ceramic, Nano)

- 5.4 By Build Phase

- 5.4.1 New Construction

- 5.4.2 Retrofit/Reroofing

- 5.5 By Application

- 5.5.1 Commercial Buildings

- 5.5.2 Residential Buildings

- 5.5.3 Industrial Facilities

- 5.5.4 Government and Public Infrastructure

- 5.5.5 Healthcare and Educational Campuses

- 5.5.6 Other Applications

- 5.6 By Geography

- 5.6.1 Asia-Pacific

- 5.6.1.1 China

- 5.6.1.2 India

- 5.6.1.3 Japan

- 5.6.1.4 South Korea

- 5.6.1.5 ASEAN Countries

- 5.6.1.6 Rest of Asia-Pacific

- 5.6.2 North America

- 5.6.2.1 United States

- 5.6.2.2 Canada

- 5.6.2.3 Mexico

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 NORDIC Countries

- 5.6.3.8 Rest of Europe

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle-East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 South Africa

- 5.6.5.3 Rest of Middle-East and Africa

- 5.6.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Akzo Nobel N.V.

- 6.4.2 Asian Paints Ltd.

- 6.4.3 Carlisle Companies Inc.

- 6.4.4 CertainTeed, LLC

- 6.4.5 Dow

- 6.4.6 Elevate

- 6.4.7 GACO

- 6.4.8 GAF Materials LLC

- 6.4.9 Huntsman International LLC

- 6.4.10 IKO Industries Ltd.

- 6.4.11 Johns Manville

- 6.4.12 NanoTech Materials

- 6.4.13 Nippon Paint Holdings Co., Ltd.

- 6.4.14 Owens Corning

- 6.4.15 PPG Industries, Inc.

- 6.4.16 Saint-Gobain

- 6.4.17 Sika AG

- 6.4.18 SOPREMA Group

- 6.4.19 TAMKO Building Products LLC

- 6.4.20 Valspar

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment