|

시장보고서

상품코드

2062402

포인트 투 포인트 안테나 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Point-To-Point Antenna - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

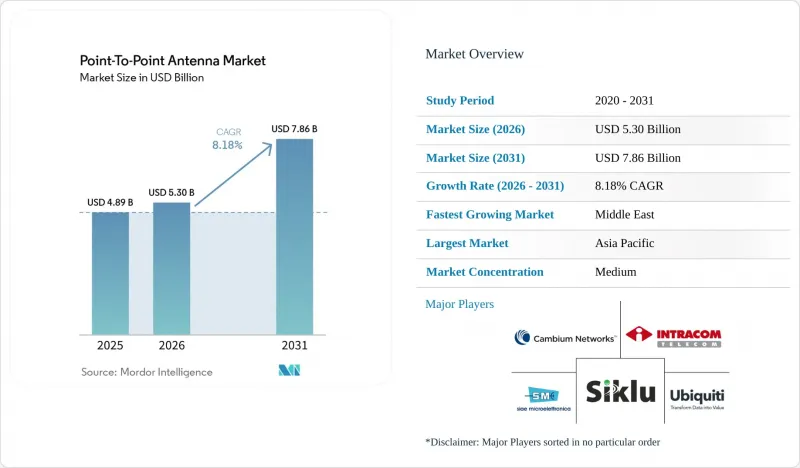

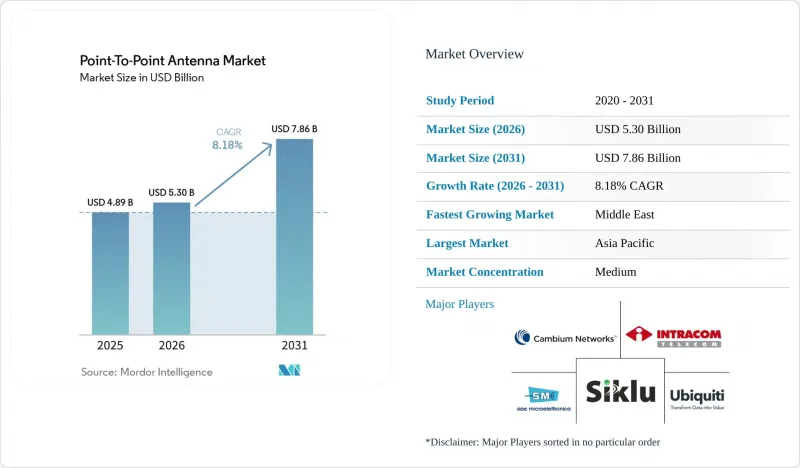

Mordor Intelligence에 의하면, 포인트 투 포인트 안테나 시장 규모는 2025년에 48억 9,000만 달러여, 2026년 53억 달러에서 2031년까지 78억 6,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 8.18%를 나타낼 것으로 예측됩니다.

본 보고서는 주파수 대역(6GHz 미만, 기타), 안테나 유형(파라볼라 안테나, 평판 및 슬롯형 도파관, 기타), 용도(통신 백홀, 무선 광대역 ISP, 기타), 최종 사용자 산업(통신 사업자, 인터넷 서비스 제공업체, 기타), 편파(단일 편파, 기타) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 포인트 투 포인트 안테나 시장 동향 및 분석

5G 백홀 용량에 대한 폭발적인 수요

5G 무선 네트워크에는 4G의 10-20배에 달하는 백홀 처리량이 필요하며, 이로 인해 통신 사업자들은 멀티 기가비트급 속도를 구현하는 mm파 및 E-밴드 시스템으로의 전환을 요구받고 있습니다. MTN 나이지리아가 2025년에 25Gbps 링크를 구축한 것은 기존의 10GHz 미만 마이크로파 경로가 새로운 대용량 경로로 대체되고 있음을 보여줍니다. Cambium Networks와 같은 벤더들은 적응형 변조 및 교차 편파 기능을 갖춘 10Gbps E-밴드 무선 장비를 공급하고 있으며, 통신 사업자는 새로운 주파수 면허를 취득하지 않고도 주파수 대역의 활용도를 극대화할 수 있습니다.

지방 광대역 자금 지원 프로그램

미국의 ‘Rural Digital Opportunity Fund(농촌 디지털 기회 기금)’와 유럽의 ‘Connecting Europe Facility 2(CEF 2)’가 제공하는 보조금은 포인트 투 포인트 백홀에 의존하는 고정 무선망 구축을 지원하고 있으며, 미국에서 낙찰된 프로젝트의 40%가 마이크로파 집선을 지정하고 있습니다. 규제상 지연 제한으로 인해 마이크로파가 위성보다 유리하기 때문에 무선 ISP는 장비에 투자하기 전에 10년간의 수익 보장을 확보할 수 있습니다. 캐나다와 스페인에서 시행되고 있는 유사한 보조금은 지역 사업자들이 라스트 마일 커버리지를 확보하기 위해 광섬유와 지점 간 연결을 결합하도록 장려하고 있습니다.

5G 모바일용 주파수 재편이 마이크로파 대역을 잠식하고 있습니다.

최근 북미 및 유럽의 규제 당국은 5G 네트워크 구축을 지원하기 위해 C-밴드 주파수 대역을 재할당했습니다. 이 결정으로 인해, 마이크로파 면허 보유자들은 통신 거리가 짧고 네트워크 커버리지를 유지하기 위해 추가 타워가 필요한 고주파 대역으로 전환할 수밖에 없게 되었습니다. 이 주파수 재할당 과정에는 총 97억 달러라는 막대한 비용이 소요되어, 사업자들의 예산에 상당한 재정적 부담을 주고 있습니다. 게다가, 이러한 전환으로 인해, 특히 E대역 주파수의 사용이 아직 국내에서 승인되지 않은 지역에서 네트워크 이용에 단기적인 공백이 발생하고 있습니다.

부문별 분석

Sub-6GHz(UHF/VHF) 대역은 2025년 매출의 46.11%를 차지했으나, 30GHz를 초과하는 mm파 시스템은 연평균 성장률(CAGR) 9.06%를 나타낼 것으로 예측되며, 이는 5G의 밀도화가 수요를 초광대역 채널로 이동시키고 있음을 여실히 보여주고 있습니다. 이 고주파 대역에서 E-밴드 및 V-밴드 링크는 최대 25Gbps의 통신 속도를 구현하여, 도시 지역의 통신 사업자들에게 멀티섹터·매시브 MIMO 사이트를 구축할 수 있는 여유를 제공합니다. 각국이 ITU-R F.2086에 따라 E-밴드 계획을 조율함에 따라, 공급업체는 단일 SKU의 무선 장비를 여러 시장에 공급할 수 있게 되어 재고 비용을 절감할 수 있습니다. 50km가 넘는 지방 구간에서는 여전히 기존의 6-30GHz 대역 마이크로파가 필수적이지만, 저비용 평판 패널의 등장으로 인해 교외 회랑에서의 그 독점적 지위는 흔들리고 있습니다.

꾸준한 규제 완화로 인해 6GHz 이하 주파수 대역이 고갈되고 있는 인도, 일본, 한국에서는 mm파가 기본적인 선택지로 자리 잡고 있습니다. mm파 기기용 지점 간(point-to-point) 안테나 시장 규모는 2031년까지 30억 달러를 넘어설 것으로 예상되며, 전체 시장 가치의 약 40%를 차지할 전망입니다. 한편, 6GHz 미만의 장비는 피크 용량보다 회절이나 비직선 시야(NLOS) 환경에서의 성능이 요구되는 방송 및 공공 안전 시스템 분야에서 여전히 확고한 입지를 유지하고 있습니다. 이러한 다양성은 라이선스 체계의 발전에 따라 위험을 분산시키는 CommScope 및 SIAE Microelettronica의 멀티밴드 제품군을 뒷받침하고 있습니다.

2025년에는 6-30GHz 대역에서 45 dBi를 초과하는 이득을 자랑하는 파라볼라 안테나가 매출의 58.38%를 차지했습니다. 그러나 풍하중 저항성과 신속한 설치가 가능하다는 점 덕분에, 플랫 패널형 및 슬롯형 도파관의 출하 대수는 연평균 성장률(CAGR) 8.78%로 증가하고 있습니다. Cambium사의 PTP 850CX는 기존 반사판보다 60% 더 작은 케이스로 동등한 전송 거리를 구현하여, 타워 임대료와 인허가 취득 기간을 절감합니다. Siklu사의 70/80GHz 위상 배열 안테나는 전자 빔 조향 기능을 갖추고 있어, 기계적인 조정 작업이 필요 없으며, 옥상 작업자가 30분 이내에 링크 설치를 완료할 수 있게 해줍니다.

도시 지역의 mm파 백홀 시장에서 평판형 지점 간 안테나 시장 점유율은 옥상 설비 크기를 제한하는 지방자치단체의 규제에 힘입어 2031년까지 45%에 육박할 것으로 전망됩니다. 반면, 사막, 산악 지대, 해상 시추 시설을 연결하는 장거리 6GHz 대역 링크의 경우, 링크 예산이 폼 팩터 문제를 상쇄하는 시장이기 때문에 파라볼라형 모델이 여전히 주류를 이룰 것으로 보입니다. 한편, 혼형이나 야기형 안테나는 신속한 구축이 요구되는 재해 복구 현장이나 서브GHz 대역의 공공 안전 네트워크에서 여전히 특수한 용도로 활용되고 있습니다.

지역별 분석

아시아태평양은 인도와 일본 등 국가들의 눈부신 발전에 힘입어 2025년 매출의 38.33%를 차지했습니다. 인도는 타워의 54%에서 여전히 마이크로파 기술에 의존하고 있는 반면, 일본은 네트워크 인프라를 강화하기 위해 2027년까지 5만 곳의 mm파 기지국을 구축하겠다는 야심 찬 목표를 세웠습니다. 2025년 12월, 인도는 고정 무선 용도를 위해 E대역 및 V대역에 더해 6개의 마이크로파 대역을 개방하는 백홀 프레임워크를 도입했습니다. 이번 조치로 인해, 그동안 지방 지역의 접속 확대를 가로막던 경매 프리미엄이 폐지되었습니다. 한편, 중국에서는 통합 RAN 조달로 인해 정확한 수량은 불분명하지만, 사례에 근거한 증거에 따르면 국영 통신 사업자는 메트로 링 네트워크에 사용되는 70GHz 링크에서 주로 국내 공급업체를 우선적으로 선정하는 것으로 보입니다.

UAE와 사우디아라비아가 주도하는 중동은 연평균 성장률(CAGR) 8.92%를 기록하며 가장 빠르게 성장하고 있는 하위 지역입니다. du와 에릭슨은 2026년 4월 두바이에서 실시된 시험에서 2km 거리에서 1Gbps의 mm파 통신을 구현하며, 스마트 시티의 IoT 백홀에 대한 적합성을 입증했습니다. 카타르의 루사일 프로젝트에서는 25Gbps E-밴드 홉을 활용해 실시간 분석 데이터를 전송하고 있으며, 이는 스마트 시티가 기가비트급 마이크로파 통신에 의존하고 있음을 보여줍니다. 북미에서는 인구 밀도가 낮은 카운티를 대상으로 하이브리드 광·무선 설계를 우선적으로 지원하는 연방 정부의 총 628억 5,000만 달러 규모의 보조금 혜택을 받고 있습니다. 그러나 C대역의 재할당으로 인해 도시 지역의 회랑에서 장거리 마이크로파 통신이 배제되면서, 70-90GHz 대역의 옥상 홉으로의 전환이 가속화되고 있습니다. 한편, 스타링크(Starlink)와 같은 위성 통신 사업자들은 외딴 지역의 유전에 서비스를 확대되고 있습니다.

유럽에서는 CEF-2를 통해 지방의 기가비트 통신망 구축에 투자하고 있으며, 광섬유 설치 비용이 1km당 5만 유로(5만 6,500달러)를 초과하는 지역이 우선적으로 선정되고 있습니다. 3.7-4.2GHz 대역의 여유 채널에서 이전하는 사업자는 더 높은 주파수 대역으로 재조정하는 데 추가 비용이 발생하기 때문에 독일과 프랑스의 통신 사업자들은 할인된 요금으로 다년 계약을 맺는 E-밴드 타워 임대 협상을 진행하고 있습니다. 남미에서는 광섬유 설치가 완료될 때까지 임시적인 마이크로파 통신을 통해 가교 역할을 하고 있습니다. 엘레트로넷(Eletronet)의 1억 5,700만 레알(3,100만 달러) 규모 2026년 확장 계획에서는 많은 타워 사이에 500미터의 간격이 발생하지만, 이는 저비용 18GHz 안테나를 통해 메워지고 있습니다. 또한, 브라질의 다양한 기후 조건으로 인해 비로 인한 신호 감쇠에 강한 듀얼 캐리어 솔루션에 대한 수요도 증가하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the point-to-point antenna market size was USD 4.89 billion in 2025, and is expected to increase from USD 5.30 billion in 2026 to USD 7.86 billion by 2031, growing at a CAGR of 8.18% over 2026-2031.

This report is Segmented by Frequency Band (Sub-6 GHz, and More), Antenna Type (Parabolic Dish, Flat Panel and Slotted Waveguide, and More), Application (Telecom Backhaul, Wireless Broadband ISP, and More), End-User Industry (Telecom Operators, Internet Service Providers, and More), Polarization (Single-Polarized, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Point-To-Point Antenna Market Trends and Insights

Explosive Demand For 5G Backhaul Capacity

5G radio networks need backhaul throughput that is 10-20 times higher than 4G, which is pushing operators to millimeter-wave and E-band systems delivering multi-gigabit speeds. MTN Nigeria's deployment of 25 Gbps links in 2025 illustrates how legacy sub-10 GHz microwave paths are being retired in favor of new high-capacity routes. Vendors such as Cambium Networks supply 10 Gbps E-band radios equipped with adaptive modulation and cross-polarization, enabling carriers to maximize spectrum use without fresh licenses.

Rural Broadband Funding Programs

Subsidies under the United States Rural Digital Opportunity Fund and the European Connecting Europe Facility 2 are underwriting fixed-wireless builds that depend on point-to-point backhaul, with 40% of U.S. winning bids specifying microwave aggregation. Because regulatory latency limits favor microwave over satellite, wireless ISPs can secure 10-year revenue guarantees before investing in equipment. Similar grants in Canada and Spain are spurring local operators to blend fiber and point-to-point links for last-mile coverage.

Spectrum Re-Farming for 5G Mobile Eroding Microwave Bands

In recent years, regulators in North America and Europe have reallocated C-band spectrum blocks to support the deployment of 5G networks. This decision has compelled microwave licensees to transition to higher-frequency bands, which are characterized by shorter ranges and require additional towers to maintain network coverage. The relocation process has incurred high costs totaling USD 9.7 billion, placing considerable financial strain on operators' budgets. Furthermore, this shift has created short-term gaps in network availability, particularly in areas where E-band frequencies have not yet received national clearance for use.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Fiber-to-Tower Buildout Creating Last-Mile Gaps

- Millimeter-Wave License Liberalization in Emerging Asia

- High Wind-Load Compliance Costs for Parabolic Dishes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Sub-6 GHz (UHF/VHF) band retained 46.11% of 2025 revenue, yet millimeter-wave systems above 30 GHz are projected to post a 9.06% CAGR, underscoring how 5G densification is tilting demand toward ultra-wide channels. Within this high-band slice, E-band and V-band links deliver up to 25 Gbps, giving urban carriers headroom for multi-sector massive-MIMO sites. As nations harmonize E-band plans under ITU-R F.2086, vendors can ship single-SKU radios to multiple markets, compressing inventory costs. Although traditional 6-30 GHz microwave remains indispensable for rural spans over 50 km, the arrival of low-cost flat panels erodes its exclusivity in suburban corridors.

Steady regulatory liberalization is making millimeter-wave the default choice in India, Japan, and South Korea, where spectrum below 6 GHz is exhausted. The point-to-point antenna market size for millimeter-wave gear is forecast to surpass USD 3 billion by 2031, accounting for almost 40% of the overall value. Conversely, sub-6 GHz units keep their foothold in broadcast and public-safety systems that need diffraction and non-line-of-sight performance rather than peak capacity. Such diversity supports multi-band portfolios from CommScope and SIAE Microelettronica, which hedge exposure as license frameworks evolve.

Parabolic dishes accounted for 58.38% of revenue in 2025, driven by their >45 dBi gain across 6-30 GHz. Yet flat-panel and slotted waveguide shipments are rising at an 8.78% CAGR thanks to wind-load advantages and quick installs. Cambium's PTP 850CX delivers comparable reach in a housing 60% smaller than legacy reflectors, cutting tower rent and permitting cycles. Siklu's 70/80 GHz phased arrays add electronic beam steering, removing mechanical alignment tasks and enabling rooftop crews to finish a link in under 30 minutes.

The point-to-point antenna market share for flat panels is likely to approach 45% in urban millimeter-wave backhaul by 2031, aided by municipal codes capping rooftop equipment size. Parabolic models will still dominate long-haul 6-GHz paths spanning deserts, mountains, and offshore rigs, markets where link budgets edge out form-factor concerns. Meanwhile, horn and Yagi variants retain specialized uses in quick-deploy disaster recovery and sub-GHz public-safety nets.

Geography Analysis

Asia-Pacific accounted for 38.33% of 2025 revenue, driven by significant developments in countries like India and Japan. India continued to rely on microwave technology for 54% of its towers, while Japan set an ambitious target of deploying 50,000 millimeter-wave sites by 2027 to enhance its network infrastructure. In December 2025, India introduced a backhaul framework that opened six microwave bands, along with E-band and V-band, specifically for fixed-wireless applications. This move eliminated auction premiums, which had previously hindered the expansion of rural connectivity. Meanwhile, in China, integrated RAN procurements obscure exact volumes; however, anecdotal evidence indicates that state carriers predominantly prefer domestic vendors for 70 GHz links used in metro ring networks.

The Middle East, led by the UAE and Saudi Arabia, is the fastest-growing sub-region, with a 8.92% CAGR. du and Ericsson validated 1 Gbps millimeter-wave reach over 2 km in Dubai's April 2026 trial, proving suitability for smart-city IoT backhaul. Qatar's Lusail project leverages 25 Gbps E-band hops to pipe real-time analytics, showcasing the smart city's dependence on gigabit microwave. North America benefits from USD 62.85 billion in combined federal subsidy pools that prioritize hybrid fiber-wireless designs in low-density counties. However, C-band re-farming has squeezed long-haul microwave out of urban corridors, hastening a pivot to 70-90 GHz rooftop hops while satellite challengers such as Starlink court remote oil fields.

Europe invests in rural gigabit coverage through CEF-2, with priority given to regions where fiber trenching costs exceed EUR 50,000 (USD 56,500) per kilometer. Operators migrating off the cleared 3.7-4.2 GHz channels incur additional costs to retune to higher bands, prompting carriers in Germany and France to negotiate multiyear E-band tower leases at discounted rates. South America is bridging fiber buildouts with interim microwave. Eletronet's BRL 157 million (USD 31 million) 2026 expansion leaves a 500-meter gap between many towers, which is filled by low-cost 18 GHz dishes. Brazil's varied climate also lifts demand for rain-fade-resistant dual-carrier solutions.

- Huawei Technologies Co. Ltd.

- CommScope Holding Company Inc.

- Ericsson AB

- Nokia Corporation

- ZTE Corporation

- Cambium Networks Corporation

- Ubiquiti Inc.

- Siklu Communication Ltd.

- SIAE Microelettronica S.p.A.

- Intracom Telecom S.A.

- Proxim Wireless Corporation

- Airspan Networks Holdings Inc.

- Redline Communications Group Inc.

- Trango Systems Inc.

- Wireless Excellence Ltd. (CableFree)

- RadioWaves Inc. (Infinite Electronics)

- mWave Industries LLC

- Rosenberger Hochfrequenztechnik GmbH & Co. KG

- L-com Inc.

- Comba Telecom Systems Holdings Ltd.

- PCTEL Inc.

- Kathrein SE

- Baylin Technologies Inc.

- ISCO International LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive Demand for 5G Backhaul Capacity

- 4.2.2 Rural Broadband Funding Programs

- 4.2.3 Rapid Fiber-to-Tower Build-out Creating Last-Mile Gaps

- 4.2.4 Proliferation of Private LTE/5G Industrial Campuses

- 4.2.5 AI-Optimized Beamforming Enhancing Link Budgets

- 4.2.6 OpenRAN mmWave Small-Cell Densification

- 4.3 Market Restraints

- 4.3.1 Spectrum Re-farming for 5G Mobile Eroding Microwave Bands

- 4.3.2 High Wind-Load Compliance Costs for Parabolic Dishes

- 4.3.3 Tightening ETSI Class-4 Antenna Radiation Regulations

- 4.3.4 Supply-Chain Volatility for Radome-Grade PTFE

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Frequency Band

- 5.1.1 Sub-6 GHz (UHF/VHF)

- 5.1.2 6-30 GHz (Microwave)

- 5.1.3 Above 30 GHz (Millimeter-Wave)

- 5.2 By Antenna Type

- 5.2.1 Parabolic Dish

- 5.2.2 Flat Panel and Slotted Waveguide

- 5.2.3 Yagi

- 5.2.4 Horn

- 5.2.5 Other Antenna Type

- 5.3 By Application

- 5.3.1 Telecom Backhaul

- 5.3.2 Wireless Broadband ISP

- 5.3.3 TV Broadcast Distribution

- 5.3.4 Military and Public Safety Networks

- 5.3.5 Enterprise Connectivity

- 5.4 By End-User Industry

- 5.4.1 Telecom Operators

- 5.4.2 Internet Service Providers

- 5.4.3 Broadcasting Companies

- 5.4.4 Defense and Government Agencies

- 5.4.5 Enterprises and Industrial Facilities

- 5.5 By Polarization

- 5.5.1 Single-Polarized

- 5.5.2 Dual-Polarized

- 5.5.3 Cross-Polarized

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.5 Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Huawei Technologies Co. Ltd.

- 6.4.2 CommScope Holding Company Inc.

- 6.4.3 Ericsson AB

- 6.4.4 Nokia Corporation

- 6.4.5 ZTE Corporation

- 6.4.6 Cambium Networks Corporation

- 6.4.7 Ubiquiti Inc.

- 6.4.8 Siklu Communication Ltd.

- 6.4.9 SIAE Microelettronica S.p.A.

- 6.4.10 Intracom Telecom S.A.

- 6.4.11 Proxim Wireless Corporation

- 6.4.12 Airspan Networks Holdings Inc.

- 6.4.13 Redline Communications Group Inc.

- 6.4.14 Trango Systems Inc.

- 6.4.15 Wireless Excellence Ltd. (CableFree)

- 6.4.16 RadioWaves Inc. (Infinite Electronics)

- 6.4.17 mWave Industries LLC

- 6.4.18 Rosenberger Hochfrequenztechnik GmbH & Co. KG

- 6.4.19 L-com Inc.

- 6.4.20 Comba Telecom Systems Holdings Ltd.

- 6.4.21 PCTEL Inc.

- 6.4.22 Kathrein SE

- 6.4.23 Baylin Technologies Inc.

- 6.4.24 ISCO International LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

(주말 및 공휴일 제외)