|

시장보고서

상품코드

2062414

저잡음 증폭기 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Low Noise Amplifier - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

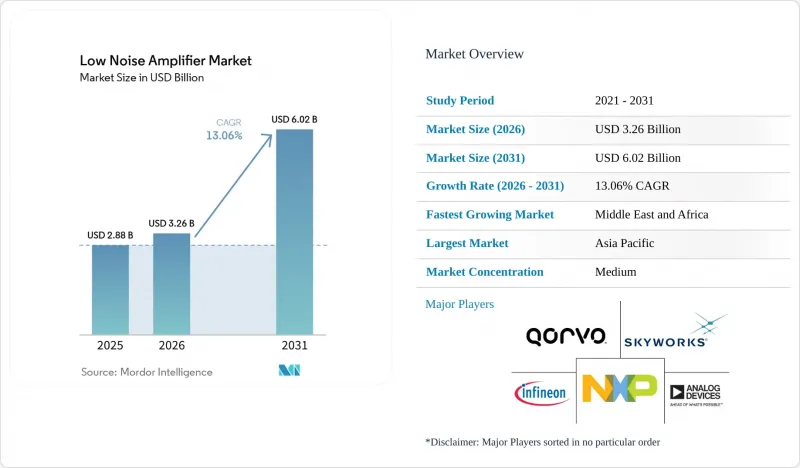

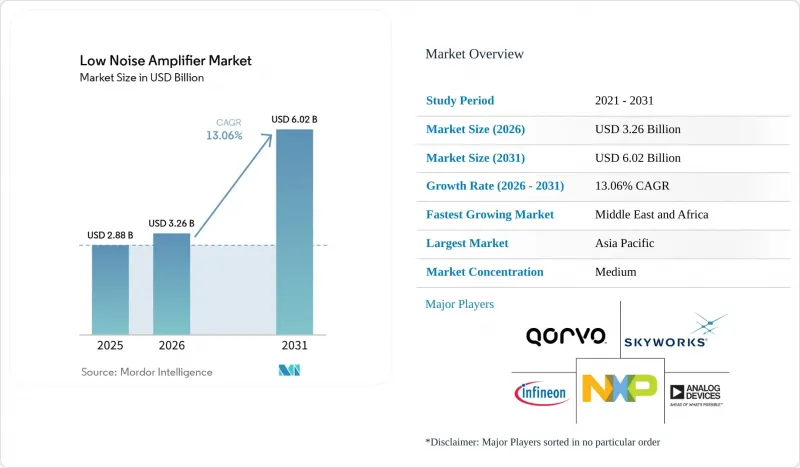

Mordor Intelligence에 의하면, 저잡음 증폭기(LNA) 시장 규모는 2025년 28억 8,000만 달러로 평가되었고, 2026년에는 32억 6,000만 달러로 추정되고, 2031년까지 60억 2,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 13.06%로 성장할 전망입니다.

본 보고서는 주파수 대역별(1GHz 미만, 1-6GHz, 6-18GHz, 기타), 반도체 기술별(GaAs, GaN, 기타), 용도별(통신·5G 인프라, 위성 통신, 항공우주 및 방위, 자동차 및 운송, 기타), 아키텍처별(디스크리트 트랜지스터 LNA, MMIC LNA, 기타) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 저잡음 증폭기 시장 동향 및 인사이트

5G 및 mm파 기지국 구축이 인프라 수요를 가속화

n77 및 n79 대역에서의 상용 5G 구축에 있어, 100MHz 이상의 채널 폭에 걸쳐 높은 선형성을 유지하면서 2.5dB 미만의 잡음 지수를 갖는 수신 체인이 현재 요구되고 있습니다. Massive-MIMO 어레이는 무선 유닛당 LNA 수를 두 배로 늘렸으며, 최근의 70nm GaN-on-SiC 소자는 83GHz에서 2.8dB를 달성하여 GaN이 mm파 기지국에 적합하다는 것이 입증되었습니다. FCC의 24GHz 대역 대역외 방사 제한 개정은 보다 강력한 제거 필터링 기능을 갖춘 아키텍처를 권장하는 것입니다. 동시에, 엔벨로프 트래킹 파워 앰프 기술로 인해 수신 경로의 감도 요구 사항이 높아지면서, 저잡음 증폭기(LNA)에 대한 수요가 더욱 증가하고 있습니다. 이 결과는 노이즈, 전력, 열 성능의 균형을 유지해야 하는 고집적도 무선 프론트엔드 분야에서 더 폭넓은 소재 및 공정 선택의 폭을 열어주므로, 저잡음 증폭기 시장에서 중요한 의미를 지닙니다. 고주파 대역의 수신 경로에 대한 필터링 요건이 강화됨에 따라 프런트엔드의 감도 요건도 높아졌으며, LNA의 사양은 무선 규격이 제시하는 수준보다 훨씬 더 엄격해졌습니다. 따라서, 낮은 잡음 지수와 대규모의 재현성 있는 생산을 동시에 달성할 수 있는 공급업체는 LNA 시장이 단순한 가입자 수 증가에 그치지 않고 5G 무선 네트워크의 고밀도화에 지속적으로 발맞추어 나가는 상황에서 더욱 유리한 입지를 차지하게 될 것입니다.

LEO 위성 군집, 멀티밴드 LNA 혁신을 주도

정지 궤도 링크의 280ms와 비교했을 때 6-30ms라는 지연 시간의 우위 덕분에, 위성 사업자들은 Ku대역, Ka대역, Q대역 간을 고속으로 전환할 수 있는 LNA를 사양에 반영해야 할 필요에 직면해 있습니다. 북극 기상 위성에 탑재된 프라운호퍼 연구소의 54GHz 대역에서 1.0-1.2dB의 잡음 지수를 실현하는 이 장치는 초저잡음 및 뛰어난 내방사선성을 갖춘 설계에 대한 수요를 여실히 보여주고 있습니다. 3GPP 릴리스 18에 따른 비지상파 네트워크 승인은 듀얼 모드 LNA의 사용을 의무화하고 있으며, 광대역 MMIC의 혁신을 촉진하고 있습니다. 그 결과, 저잡음 증폭기(LNA) 시장은 기존의 정부 조달 주기보다 더 빠르게 진행되고 있으며, 주파수 대역폭과 인증된 납기 준수를 모두 요구하는 상업용 우주 프로그램에 의해 점차 그 양상이 형성되고 있습니다.

반도체 공급망의 변동이 생산 능력을 제약하고 있습니다.

갈륨 수출 규제로 인해 2024년 8월에는 중국산 수출량이 제로가 되었으며, GaAs 및 GaN 웨이퍼공급이 부족해지면서 리드타임이 길어지고 있습니다. SDCE는 2030년까지 미국에서 6만 7,000명의 엔지니어 부족 현상이 발생하여 제조 분야의 병목 현상을 악화시킬 가능성이 있다고 예측했습니다. SEMI는 2027년까지 300mm 팹 설비에 대한 투자액이 1,370억 달러에 달할 것으로 전망하고 있지만, 생산 능력은 저잡음 증폭기 시장에 중요한 성숙한 RF 공정 노드가 아닌, 로직 및 메모리에 중점을 두게 될 것입니다. 이러한 상황은 저잡음 증폭기 시장에서 공급 회복력이 더 이상 부차적인 문제가 아니라, 통신, 국방 및 위성 관련 생산 분야에서 핵심적인 전략적 선택이 되었음을 보여줍니다. 국내에서 다양화된 화합물 반도체의 생산 능력이 더욱 확보될 때까지는 자사 공장을 보유한 공급업체나 파운드리 이용에 대한 우선권을 가진 공급업체가 비용 관리 및 납기 준수 측면에서 지속적인 우위를 유지할 가능성이 높을 것입니다.

부문별 분석

1-6GHz 대역은 2025년에 저잡음 증폭기 시장 점유율의 42.42%를 차지했습니다. 이는 해당 주파수 대역에서 작동하는 휴대전화 네트워크, Wi-Fi 기기, GNSS 기기의 매우 광범위한 도입 실적을 반영한 것입니다. 이러한 입지는 단일 최종 시장에만 기인한 것이 아니라 광범위한 사업 확장에 의해 뒷받침되고 있으며, 특정 기기 부문 수요가 둔화되더라도 다른 부문에서 수요가 지속될 경우 이 부문은 더욱 탄력성을 발휘합니다. 1GHz 미만의 대역은 LPWAN, 스마트 계량 및 기타 IoT 응용 분야에서 꾸준히 중요한 위치를 차지하고 있습니다. 이러한 용도에서는 소비 전류가 표면상의 이득이나 노이즈 성능과 마찬가지로 중요하게 여겨지는 경우가 많기 때문입니다. 한편, 18-40GHz 대역의 저잡음 증폭기(LNA) 시장 규모는 5G mm파 무선기, Ka 대역 단말기 및 고해상도 자동차용 레이더 시스템이 양산 단계에 접어들면서 2031년까지 연평균 성장률(CAGR) 16.53%로 확대될 것으로 전망됩니다. 이러한 성장 양상은 시장이 중파 대역을 핵심으로 하는 구조에서 밀리파에 대한 수요가 기존 기반보다 급속히 증가하는 한편, 여전히 공급 체계와 집적 기술 노하우에 의존하는 보다 폭넓은 제품군으로 전환되고 있음을 보여줍니다.

MDPI Electronics는 150 nm GaAs pHEMT를 이용한 17-38GHz 캐스케이드 LNA에 대해 보고했습니다. 이는 동시 노이즈 및 입력 임피던스 매칭을 통해 20-23 dB의 평탄한 이득과 1.1-2.1 dB의 잡음 지수를 달성함으로써, 해당 주파수 대역에서 설계상의 장벽이 어떻게 점차 낮아지고 있는지를 보여줍니다. 6-18GHz 대역은 방위용 레이더, 마이크로파 백홀, 위성 중간 주파수 체인에서 여전히 중요한 역할을 하고 있으며, 이러한 분야의 조달은 소비자의 교체 주기보다 프로그램 일정에 더 크게 좌우되는 경향이 있습니다. 40GHz를 초과하는 대역에서는 시장 규모가 여전히 작지만, 위성 간 링크, 특수 계측 기기 및 초기 단계의 서브-테라헤르츠(sub-THz) 센싱에 대한 수요로 인해 시장이 점차 확대되고 있습니다. MDPI Aerospace는 또한 59-71GHz 대역의 GaN/Si HEMT 프런트엔드의 성능으로 4 dB의 잡음 지수를 제시했습니다. 이는 더 엄격한 요건을 갖춘 위성 크로스링크 설계가 가까운 시일 내에 이러한 고주파 대역으로 전환될 것임을 뒷받침하는 것입니다. 모든 주파수 대역에 걸쳐 저잡음 증폭기(LNA) 시장도 LNA, 필터, 스위치 기능을 일체화한 프런트엔드 모듈에 의해 재편되고 있습니다. 이로 인해 순수한 디스크리트 칩의 역할은 축소되는 반면, 서브시스템 수준에서 RF 부품의 비중은 증가하고 있습니다.

GaAs는 2025년에 시장의 38.52%를 차지했습니다. 그 공정의 성숙도, 안정적인 잡음 성능, 그리고 파운드리 활용의 폭넓은 가능성 덕분에 여전히 많은 수신기 설계에서 기본 선택지로 자리 잡고 있기 때문입니다. 이러한 우위는 1-18GHz 대역의 GNSS, 위성 프런트엔드 및 셀룰러 LNA에서 가장 두드러지며, GaAs는 저잡음 성능과 시장이 이미 충분히 파악하고 있는 비용 구조 간의 균형을 유지하고 있습니다. GaN을 활용한 저잡음 증폭기 시장은 2031년까지 연평균 성장률(CAGR) 15.65%로 확대될 것으로 예상되며, mm파, 열 및 전력 처리 수요가 증가함에 따라 가장 빠르게 성장하는 소재 플랫폼이 될 전망입니다. 이러한 변화는 8인치 웨이퍼 생산을 목표로 하는 공급업체들의 로드맵에 힘입은 것으로, 이를 통해 6-40GHz 대역에서 GaN과 GaAs 간의 기존 비용 격차가 줄어들 가능성이 있습니다. 따라서 저잡음 증폭기 업계는 GaAs가 폭넓은 기반을 유지하는 한편, GaN이 더 높은 파손 전압과 내열성이 요구되는 응용 분야에서 시장 점유율을 확대해 나가는 등, 더욱 복합 소재화된 구조로 전환되고 있습니다.

Springer Nature의 『Arabian Journal for Science and Engineering』은 Ku 대역 및 Ka 대역 위성통신(SATCOM) 시스템용 가변형 LNA의 설계를 검증한 결과, GaAs와 GaN이 모두 이 위성 수신기 분야에서 여전히 확고한 입지를 유지하고 있음을 확인했습니다. SiGe BiCMOS는 GaAs에 근접한 노이즈 성능과 실리콘 파운드리 수준의 집적 밀도를 모두 갖추고 있어, 자동차용 레이더 및 멀티밴드 GNSS 제품 분야에서 유용한 중간적 위치를 계속해서 차지하고 있습니다. 또한, 최첨단 CMOS 노드는 절대적인 노이즈 성능보다 소비 전력, 실장 면적, 집적도가 더 중요시되는 IoT 및 소비자용 설계 분야에서도 그 적용 범위를 확대되고 있습니다. MACOM의 3억 4,500만 달러 규모 확장 계획에 대한 미국 상무부의 지원책은 통신 및 방위 관련 공급 수요에 대응하기 위해 국내 GaAs 및 GaN 생산 능력을 뒷받침함으로써, 해당 정책이 소재 경쟁 구도 형성에 어떻게 기여하고 있는지를 여실히 보여주고 있습니다. InP는 계측 기기, 전파 천문학 및 초기 단계의 센싱 분야에서 100GHz를 초과하는 대역에서 비록 제한적이긴 하지만 확고한 역할을 유지하고 있습니다. 이는 저잡음 증폭기(LNA) 업계가 여전히 하나의 제품 범주 아래에서 매우 다양한 성능 및 가격대를 아우르고 있음을 의미합니다.

지역별 분석

2025년 현재, 아시아태평양은 저잡음 증폭기(LNA) 시장 점유율의 40.75%를 차지했으며, 이러한 시장 규모는 5G 인프라 제조, 소비자 가전제품 조립 및 화합물 반도체 공급망 분야에서 이 지역이 차지하는 확고한 입지에 기인합니다. 중국은 두 가지 역할을 수행하고 있습니다. LNA를 사용하는 RF 시스템의 주요 조립 거점일 뿐만 아니라, 갈륨 관련 자재 흐름에서 중요한 업스트림 공급원으로도 작용하고 있어, 이 지역은 전 세계 공급 상황에 구조적인 영향력을 행사하고 있습니다. 한국과 대만은 파운드리 및 반도체 거점으로서 여전히 중요한 위치를 차지하고 있으며, 여러 지역에 걸쳐 통신, GNSS 및 소비자용 용도에 서비스를 제공하는 팹리스 LNA 공급업체들을 뒷받침하고 있습니다. 일본 역시 GNSS 및 IoT 수신기 부품 분야에서 중요한 역할을 하고 있으며, 이 분야에서는 웨이퍼 규모보다 공정의 성숙도와 제품의 신뢰성이 더 중요하게 여겨집니다. 인도에서는 5G 구축이 진행되면서 물류 및 정밀 농업 등의 분야에서 연결 기기의 이용이 증가하고 있어 새로운 수요층이 형성되고 있으며, 이에 따라 저잡음 증폭기(LNA) 시장은 기존의 동아시아 제조 거점을 넘어 확대되고 있습니다.

북미와 유럽은 합쳐서, 수요 중에서 부가가치가 가장 높고 인증 요건이 가장 까다로운 분야를 뒷받침하고 있습니다. 북미에서는 국내 화합물 반도체 생산 능력이 더욱 전략적인 위치를 차지하고 있으며, MACOM이 2025년 7월 리서치 트라이앵글 파크에 위치한 GaN-on-SiC 웨이퍼 제조 시설의 완전한 운영 관리권을 이관함에 따라, 현지 생산 기반에 ‘Trusted Foundry’ 기준을 충족하는 생산 능력이 추가되었습니다. 유럽에서는 인피니온(Infineon)이 28nm CMOS 레이더 MMIC 로드맵을 통해 L2+부터 L4까지의 차량 플랫폼을 지속적으로 목표로 삼고 있기 때문에 자동차용 레이더가 여전히 주요 성장 동력으로 작용하고 있습니다. 또한, 유럽의 우주 프로그램 역시 인증을 완료한 LNA 어셈블리의 조달을 뒷받침하고 있으며, ESA의 HydroGNSS 프로젝트에서 EECL이 제조한 증폭기의 궤도상 성능은 이 저잡음 증폭기(LNA) 시장에서 인증과 임무 실적이 공급업체 시장 진입을 여전히 얼마나 좌우하고 있는지를 보여주고 있습니다.

중동 및 아프리카는 2031년까지 연평균 성장률(CAGR) 17.98%를 나타낼 것으로 예측되며, 걸프협력회의(GCC) 회원국 및 아프리카의 일부 시장에서 모바일 광대역에 대한 투자가 증가함에 따라 가장 빠르게 성장하는 지역 블록이 될 전망입니다. 만안 지역의 통신 사업자들은 5G를 도입하고 있으며, 일부 서비스에서는 mm파(mmWave)를 적극적으로 채택하고 있어, 일부 유럽의 서비스보다 빠른 속도로 28GHz급 수신 부품에 대한 수요를 뒷받침하고 있습니다. 또한 나이지리아와 남아프리카공화국에서도 완전히 통합된 수입 시스템에만 의존하는 것이 아니라, 보다 직접적인 RF 부품 수요를 뒷받침하기에 충분한 규모로 LTE 및 초기 단계의 5G 인프라가 확대되고 있습니다. 남미에서는 여전히 브라질과 아르헨티나가 중심을 이루고 있으며, 이들 국가에서는 휴대전화 네트워크 업그레이드와 위성 광대역 서비스에 더해 정밀 농업 분야의 GNSS 수요도 증가하고 있습니다. 이로 인해 저잡음 증폭기 시장에서는 순수한 통신 분야의 성장과는 별개로, 지역 특유 수요 흐름이 나타나고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the low noise amplifier market size is expected to increase from USD 2.88 billion in 2025 to USD 3.26 billion in 2026 and reach USD 6.02 billion by 2031, growing at a CAGR of 13.06% over 2026-2031.

This report is Segmented by Frequency Band (Less Than 1 GHz, 1-6 GHz, 6-18 GHz, and More), Semiconductor Technology (GaAs, Gan, and More), Application (Telecom and 5G Infrastructure, Satellite Communications, Aerospace and Defense, Automotive and Transportation, and More), Architecture (Discrete Transistor LNAs, MMIC LNAs, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Low Noise Amplifier Market Trends and Insights

5G and mmWave Base-Station Rollout Accelerates Infrastructure Demand

Commercial 5G deployments in n77 and n79 bands now require receive chains with noise figures below 2.5 dB while sustaining high linearity across 100 MHz-plus channel widths. Massive-MIMO arrays multiply LNA counts per radio unit, and recent 70 nm GaN-on-SiC devices achieve 2.8 dB at 83 GHz, proving GaN's suitability for mmWave base stations. The FCC's revised out-of-band emission limits in the 24 GHz bands favor architectures with stronger rejection filtering. Simultaneously, envelope-tracking power amplifier techniques are elevating receive-path sensitivity requirements, further boosting demand for Low Noise Amplifiers. That result matters in the Low noise amplifier market because it supports a wider set of material and process choices for dense radio front ends that must balance noise, power, and thermal performance. Tighter filtering requirements in higher-frequency receive paths are also raising front-end sensitivity requirements, making LNA specifications more demanding than the radio standard alone would suggest. Vendors that can pair low noise figures with repeatable production at scale are therefore better placed as the Low noise amplifier market continues to follow 5G radio density rather than just subscriber growth.

LEO Satellite Constellations Drive Multi-Band LNA Innovation

Latency advantages of 6-30 ms, compared with 280 ms for geostationary links, compel satellite operators to specify LNAs that switch rapidly across Ku-, Ka-, and Q-bands. Fraunhofer's 1.0-1.2 dB noise-figure devices at 54 GHz on the Arctic Weather Satellite highlight demand for ultra-low-noise, radiation-tolerant designs. 3GPP Release 18 endorsement of non-terrestrial networks mandates dual-mode LNA operation, spurring wideband MMIC innovation. As a result, the Low noise amplifier market is increasingly shaped by commercial space programs that move faster than traditional government procurement cycles and demand both frequency breadth and certified delivery discipline.

Semiconductor Supply-Chain Volatility Constrains Production Capacity

Gallium export curbs reduced China's outbound volumes to zero in August 2024, throttling GaAs and GaN wafer availability and inflating lead times. SDCE projects that a 67,000-engineer talent deficit in the United States by 2030 could exacerbate fabrication bottlenecks. Although SEMI forecasts USD 137 billion in 300 mm fab equipment spending by 2027, capacity will favor logic and memory, rather than mature RF process nodes critical to the Low Noise Amplifier market.That response shows that supply resilience is no longer a background issue in the Low noise amplifier market and has become a central strategic choice for telecom, defense, and satellite-linked production. Until more domestic and diversified compound-semiconductor capacity becomes available, suppliers with captive fabs or privileged foundry access are likely to keep a durable advantage in cost control and schedule reliability.

Other drivers and restraints analyzed in the detailed report include:

- Automotive Radar Evolution Beyond 77 GHz Unlocks ADAS Potential

- Growing GNSS and IoT Device Install-Base

- High R&D Cost of Sub-0.5 dB Noise-Figure Designs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 1-6 GHz segment held 42.42% of the Low noise amplifier market share in 2025, reflecting the very large installed base of cellular networks, Wi-Fi equipment, and GNSS devices that operate across this range. That position is supported by broad deployment rather than by a single end market, which makes this band more resilient when demand softens in one device class but continues in another. The sub-1 GHz band kept steady relevance in LPWAN, smart metering, and other IoT uses where current draw often matters as much as headline gain or noise performance. At the other end, the Low noise amplifier (LNA) market size for the 18-40 GHz segment is projected to expand at a 16.53% CAGR through 2031 as 5G mmWave radios, Ka-band terminals, and higher-resolution automotive radar systems move into volume production. That growth pattern shows a market shifting from its mid-band core into a broader portfolio where millimeter-wave demand is rising faster than the legacy base but still depends on supply discipline and integration know-how.

MDPI Electronics reported a 17-38 GHz cascode LNA on 150 nm GaAs pHEMT that achieved flat 20-23 dB gain and a 1.1-2.1 dB noise figure through simultaneous noise and input matching, which illustrates how the design barriers at these frequencies are being reduced. The 6-18 GHz range remains important for defense radar, microwave backhaul, and satellite intermediate-frequency chains, where procurement is tied more to program timing than consumer replacement cycles. Above 40 GHz, the market is still narrower, but it is being pushed forward by inter-satellite links, specialized instrumentation, and early sub-THz sensing needs. MDPI Aerospace also showed 59-71 GHz GaN/Si HEMT front-end performance with a 4 dB noise figure, which supports near-term migration of more demanding satellite crosslink designs into these upper bands. Across bands, the Low noise amplifier market is also being reshaped by front-end modules that package LNA, filter, and switch functions together, which can reduce the role of pure discrete chips while increasing RF content at the subsystem level.

GaAs held 38.52% of the market in 2025 because its process maturity, stable noise performance, and broad foundry availability continue to make it the default choice for a wide share of receiver designs. That leadership is strongest in GNSS, satellite front ends, and cellular LNAs across 1-18 GHz, where GaAs balances low noise performance with a cost profile the market already understands well. The low-noise amplifier market for GaN is projected to expand at a 15.65% CAGR through 2031, making it the fastest-growing material platform as mmWave, thermal, and power-handling demands rise. This shift is supported by vendor roadmaps to 8-inch wafer production, which could narrow the historical cost gap between GaN and GaAs in the 6-40 GHz range. The low-noise amplifier industry is therefore moving toward a more mixed-material structure, where GaAs maintains its broad base while GaN gains share in applications that require higher breakdown voltage and greater heat tolerance.

Springer Nature's Arabian Journal for Science and Engineering reviewed tunable LNA design in Ku- and Ka-band SATCOM systems and confirmed that both GaAs and GaN remain strongly positioned in this satellite receiver window. SiGe BiCMOS continues to occupy a useful middle ground because it combines near-GaAs noise performance with the integration density of silicon foundries, which is valuable for automotive radar and multi-band GNSS products. Advanced CMOS nodes are also extending their reach in IoT and consumer designs where power, footprint, and integration often matter more than absolute best noise performance. The United States Department of Commerce support package for MACOM's USD 345 million expansion plan underlines how policy is now helping shape material competition by backing domestic GaAs and GaN capacity for telecom and defense-linked supply needs. InP still holds a narrow but defensible role above 100 GHz in instrumentation, radio astronomy, and early-stage sensing, which means the Low noise amplifier industry continues to span very different performance and cost tiers under one product category.

Geography Analysis

Asia-Pacific held 40.75% of the Low noise amplifier market share in 2025, and that scale stemmed from its strong position in 5G infrastructure manufacturing, consumer electronics assembly, and compound semiconductor supply chains. China plays a dual role: it is both a large assembler of RF systems that use LNAs and a critical upstream source of gallium-linked material flows, giving the region structural influence over global supply conditions. South Korea and Taiwan remain important as foundry and semiconductor hubs that support fabless LNA vendors serving telecom, GNSS, and consumer applications across several regions. Japan also keeps a meaningful role in GNSS and IoT receiver components, where process maturity and product reliability matter more than headline wafer scale. India is adding another layer of demand as 5G rollout expands and connected device use rises in sectors such as logistics and precision agriculture, which broadens the Low noise amplifier market beyond traditional East Asian manufacturing centers.

North America and Europe together anchor the highest-value, most qualification-intensive portion of demand. In North America, domestic compound-semiconductor capacity is becoming more strategic, and MACOM's July 2025 transfer of full operational control of its Research Triangle Park GaN-on-SiC wafer facility added Trusted Foundry-aligned capacity to the local base. In Europe, automotive radar remains a major pull factor because Infineon continues to target L2+ to L4 vehicle platforms with its 28 nm CMOS radar MMIC roadmap. European space programs also support procurement for qualified LNA assemblies, and the in-orbit performance of EECL's amplifiers on ESA HydroGNSS shows how certification and mission heritage still shape supplier access in this part of the Low noise amplifier (LNA) market.

The Middle East and Africa is projected to grow at a 17.98% CAGR through 2031, making it the fastest-growing regional block as mobile broadband investment rises across the Gulf Cooperation Council and several African markets. Gulf operators are adopting 5G with meaningful mmWave exposure in selected deployments, which supports demand for 28 GHz-class receive components at a faster pace than in some European rollouts. Nigeria and South Africa are also expanding LTE and early 5G infrastructure enough to support more direct RF component demand rather than relying only on fully integrated imported systems. South America remains centered on Brazil and Argentina, where cellular upgrades and satellite broadband are joined by GNSS needs in precision agriculture, which gives the Low noise amplifier market a region-specific demand stream outside pure telecom growth.

- Skyworks Solutions Inc.

- Infineon Technologies AG

- Qorvo Inc.

- NXP Semiconductors N.V.

- Analog Devices, Inc.

- Texas Instruments Incorporated

- Teledyne Technologies Incorporated

- Microchip Technology Incorporated

- MACOM Technology Solutions Holdings Inc.

- Broadcom Inc.

- Scientific Components Corporation d/b/a Mini-Circuits

- AmpliTech Group Inc.

- Marki Microwave Inc.

- RFHIC Corporation

- Guerrilla RF Inc.

- Sivers Semiconductors AB

- Pasternack Enterprises LLC

- L3Harris Technologies Inc.

- Cobham Limited

- Kratos Defense & Security Solutions Inc.

- Giga-tronics Incorporated

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 5G and mmWave Base-Station Rollout

- 4.2.2 Proliferation of LEO Satellite Constellations

- 4.2.3 Growing GNSS/IoT Device Install-base

- 4.2.4 Automotive Radar Shift to 77 GHz ADAS

- 4.2.5 Cryogenic LNAs for Quantum-Computing Scale-Up

- 4.2.6 Weather and Earth-Observation Micro-sat Programs

- 4.3 Market Restraints

- 4.3.1 High R&D Cost of Sub-0.5 dB NF Designs

- 4.3.2 Semiconductor Supply-Chain Volatility

- 4.3.3 Stringent Qualification and Compliance Costs

- 4.3.4 Thermal-Management Limits in mmWave Modules

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Frequency Band

- 5.1.1 Less than 1 GHz

- 5.1.2 1 - 6 GHz

- 5.1.3 6 - 18 GHz

- 5.1.4 18 - 40 GHz

- 5.1.5 Above 40 GHz

- 5.2 By Semiconductor Technology

- 5.2.1 GaAs

- 5.2.2 GaN

- 5.2.3 SiGe BiCMOS

- 5.2.4 CMOS

- 5.2.5 InP and Other Semiconductor Technology

- 5.3 By Application

- 5.3.1 Telecom and 5G Infrastructure

- 5.3.2 Satellite Communications

- 5.3.3 Aerospace and Defense

- 5.3.4 Automotive and Transportation

- 5.3.5 IoT and Consumer Devices

- 5.3.6 Industrial, Test and Measurement

- 5.4 By Architecture / Form Factor

- 5.4.1 Discrete Transistor LNAs

- 5.4.2 MMIC LNAs

- 5.4.3 RF Front-End Modules (with LNA)

- 5.4.4 Cryogenic / Ultra-low-temp LNAs

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Skyworks Solutions Inc.

- 6.4.2 Infineon Technologies AG

- 6.4.3 Qorvo Inc.

- 6.4.4 NXP Semiconductors N.V.

- 6.4.5 Analog Devices, Inc.

- 6.4.6 Texas Instruments Incorporated

- 6.4.7 Teledyne Technologies Incorporated

- 6.4.8 Microchip Technology Incorporated

- 6.4.9 MACOM Technology Solutions Holdings Inc.

- 6.4.10 Broadcom Inc.

- 6.4.11 Scientific Components Corporation d/b/a Mini-Circuits

- 6.4.12 AmpliTech Group Inc.

- 6.4.13 Marki Microwave Inc.

- 6.4.14 RFHIC Corporation

- 6.4.15 Guerrilla RF Inc.

- 6.4.16 Sivers Semiconductors AB

- 6.4.17 Pasternack Enterprises LLC

- 6.4.18 L3Harris Technologies Inc.

- 6.4.19 Cobham Limited

- 6.4.20 Kratos Defense & Security Solutions Inc.

- 6.4.21 Giga-tronics Incorporated

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment