|

시장보고서

상품코드

2062416

E-Compass 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)E-Compass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

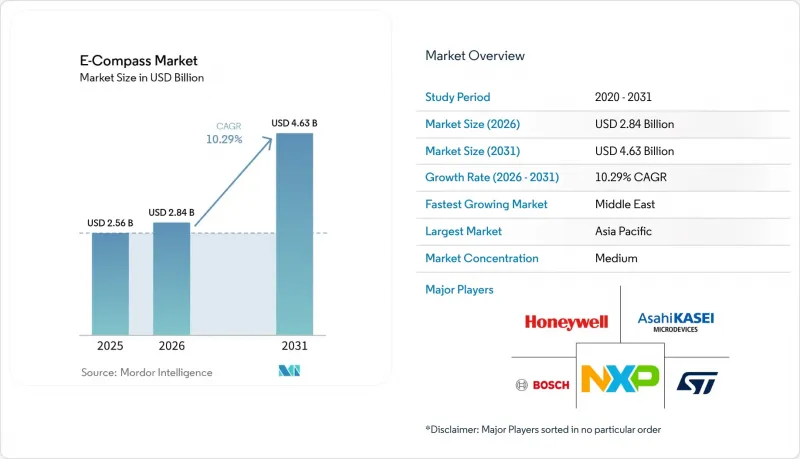

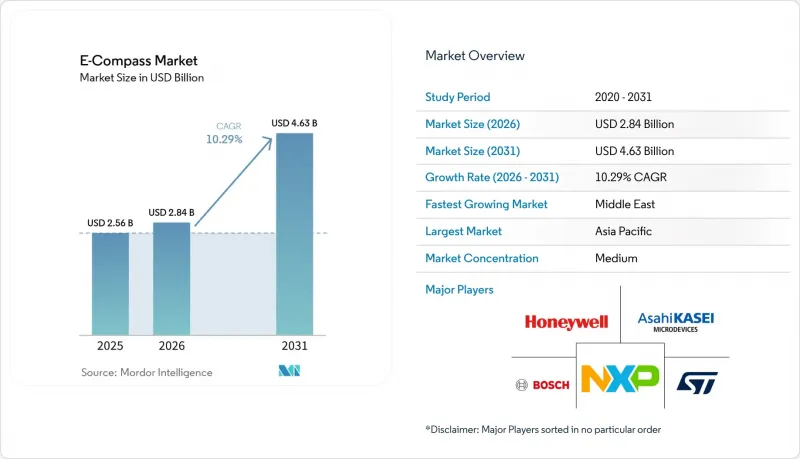

Mordor Intelligence에 의하면, 전자 나침반 시장 규모는 2025년에 25억 6,000만 달러, 2026년에 28억 4,000만 달러가 되어, 2031년까지 46억 3,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 10.29%로 성장할 전망입니다.

본 보고서는 기술별(홀 효과, 이방성, 자이언트, 터널 자기 저항, 플럭스 게이트 등), 축 방향(1-2축, 3축, 6축·9축 센서 퓨전), 용도(소비자용 전자기기 등), 폼 팩터(디스크리트 나침반 모듈, 통합형 센서 콤보, SoC 내장형 전자 나침반 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 전자 나침반 시장 동향과 인사이트

내비게이션 센서가 탑재된 스마트폰의 보급

2025년 스마트폰 가입자 수는 69억 건에 달할 것으로 예상되며, 사실상 모든 중급 기종과 플래그십 모델에는 증강현실(AR) 오버레이 및 실내 내비게이션을 위해 자력계, 가속도계, 자이로스코프의 데이터를 통합하는 9축 센서 허브가 탑재될 것입니다. 통합형 콤보 모듈을 통해 부품 원가를 25% 절감했으며, 폴더블 디스플레이에 적합한 1mm 미만의 패키지 높이를 구현했습니다. 지하철이나 쇼핑몰 내에서의 보행자 위치 추정 기술은 GNSS를 이용할 수 없는 경우 현재 자력계를 통한 방위 정보에 의존하고 있습니다. 2025년 10월에 출시된 아사히카세이의 AK09974C는 웨이퍼 레벨의 1.2×1.2mm 패키지로 0.15µT의 분해능을 구현하여 적극적인 소형화를 실현하고 있습니다. 수동으로 8자 교정을 수행하는 사용자는 40% 미만에 불과하기 때문에 각 벤더사는 수백만 건의 실행 트레이스 데이터에서 수집한 머신러닝 모델을 기반으로 한 자동 교정 기능을 개발하고 있습니다.

승용차 및 상용차에서의 ADAS 보급 확대

2025년에는 신형 승용차의 45%에 첨단 운전자 보조 시스템(ADAS)이 탑재되며, 레벨 2 이상의 각 플랫폼에는 ISO 26262 기능 안전 요건을 충족하기 위해 최소 1개의 6축 또는 9축 관성 측정 장치(IMU)가 내장됩니다. 이 IMU에 내장된 자력계는 장시간 고속도로 주행 중 자이로스코프의 드리프트를 보정하여 누적되는 진행 방향 오차를 방지합니다. 2024년에 AEC-Q100 등급 1 인증을 획득한 TDK의 ‘PositionSense’는 현재 유럽 및 일본의 OEM 제조업체에 공급되고 있으며, 2027년 모델 출시를 위한 준비가 진행 중입니다. 이 차량 운영사는 나침반이 탑재된 텔레매틱스 박스를 도입하여, 경로 최적화를 통해 연료 소비를 3-5% 절감함으로써 센서 추가 비용 15-25달러를 상쇄하고 있습니다. 2024년 이후 유럽연합(EU)에서 의무화될 긴급 제동 및 차선 유지 시스템은 사고율을 계속 높일 것입니다.

자기 간섭 및 보정 드리프트에 대한 취약성

주변의 철제 물체나 전류 루프는 지구 자기장(25-65μT)을 훨씬 웃도는 500μT 이상의 자기 간섭을 일으켜, 스마트폰, 로봇, 드론에서 30도를 넘는 방향 오차를 발생시킵니다. 도시 지역의 고층 빌딩, 지하철 선로, 공장의 모터는 이러한 왜곡을 더욱 악화시킵니다. 최종 사용자의 불과 60%만이 수동 보정을 완료했으며, 남아 있는 오차로 인해 실내 내비게이션의 정확도가 떨어지고 있습니다. 자동차 시스템에서는 GNSS와 휠 속도 인코더를 융합하여 드리프트를 줄이고 있지만, 고정형 서비스 로봇은 룩업 테이블이나 정기적으로 갱신되는 자기 이상 지도에 의존할 수밖에 없습니다. 아사히카세이는 2025년 12월, Aizip과 제휴하여 자기장 맵의 크라우드소싱을 실시함으로써, 보정 주기를 며칠에서 몇 시간으로 단축했습니다.

부문별 분석

홀 효과 및 TMR 센서는 2025년 매출의 42.19%를 차지했습니다. 이는 파워트레인, 항공전자기기 및 공장 자동화용 AEC-Q100 및 IEC 61508 규격을 충족하는 서브 나노테슬라급 감도와 열적 안정성 덕분입니다. 자동차 제조업체와 산업용 시스템 통합사업자들이 수명 주기가 긴 플랫폼을 위해 이 아키텍처를 채택하고 있어, TMR 모듈용 전자 나침반 시장은 안정적인 한 자릿수 후반대의 성장률을 기록하며 확대될 전망입니다. 홀 효과식 센서는 단가가 0.40달러 미만으로 유지되기 때문에 비용 제약이 있는 휴대전화 시장에서 점유율을 유지하고 있지만, 노이즈 플로어가 10µT인 탓에 정확도는 약 5도까지만 확보할 수 있어, 이러한 한계로 인해 고급 제품에의 채택이 제한되고 있습니다. 플럭스게이트 방식 나침반은 잠수함이나 항공기용으로 1도 미만의 정확도를 제공하지만, 소비 전력이 50-200mW에 달하기 때문에 여전히 틈새 시장 제품으로 남아 있습니다.

질소 공극 다이아몬드 또는 광자극 알칼리 증기 셀을 활용한 양자 나침반 시장은 2031년까지 연평균 성장률(CAGR) 10.99%를 나타낼 것으로 예측되며, 이는 전자 나침반 시장에서 가장 높은 성장률입니다. 이는 방위 오차가 허용되지 않는 국방 분야나 해저 환경에서 자기 간섭에 대한 내성이 있기 때문입니다. 2024년 실험실 기록에 따르면 0.1도의 정확도가 확인되었으며, 프로토타입은 자율주행차에서 시험 주행이 진행되고 있습니다. Q-Nav 등공급업체는 마이크로파 구동 노이즈를 필터링하는 FPGA 컨트롤러와 다이아몬드 센서를 일체화하여, 케이스 크기를 45cm³까지 소형화했습니다. 전력 소비량이 5-10배나 더 높음에도 불구하고, 각국 정부는 시범 도입에 자금을 지원하고 있으며, 무인 잠수함이나 우주 플랫폼의 경우 배터리 수명보다 정확도가 더 중요하게 여겨질 것으로 전망하고 있습니다. 칩 스케일의 광유도 증기 셀에 대한 병행 연구 개발을 통해, 2030년까지 양자 모듈을 수 입방 센티미터 크기로 소형화할 수 있을 것으로 보입니다.

2025년 시점에서도 3축 나침반이 출하 대수의 61.18%를 차지했습니다. 이는 스마트폰이나 드론의 비용 상한선을 충족하고, 확립된 레거시 소프트웨어 스택을 갖추고 있기 때문입니다. 한편, 개발자들이 기계적인 위치 조정 제약을 피하려는 경향이 있어, 단축 및 2축 유닛 E-나침반 시장 점유율은 12%로 하락했습니다. 가속도계와 자이로스코프를 통합한 6축 및 9축 패키지는 2026년부터 2031년까지 10.57% 증가할 것으로 예측됩니다. 이는 자동차 업계의 1차 공급업체들이 기판 면적을 40% 줄이고, 밀접하게 결합된 칼만 필터를 구현할 수 있는 단일 시스템 인 패키지(SiP) 유닛으로의 전환을 추진하고 있는 데 힘입은 바가 큽니다.

자동차 분야에서는 듀얼 9축 구성이 이중화 기능을 제공하며, ISO 26262 적합성 요건을 충족함으로써, 하나의 센서가 고장 나더라도 리밋 홈 스티어링을 보장합니다. 웨어러블 기기에서는 9축 허브를 활용해 제스처 인식 및 낙상 감지를 수행하며, 회전과 평행 이동을 구분할 때 자력계 데이터를 통해 분류 정확도가 15% 향상됩니다. PNI Sensor사의 RM3100 기반 NaviGuider는 지속적인 하드 아이언 및 소프트 아이언 자동 보정 기능을 통합하고 있으며, 수동으로 수행해야 하는 일상적인 작업으로 인해 수면으로 떠오를 수 없는 해양 글라이더를 대상으로 합니다. 하류 펌웨어가 센서 퓨전 라이브러리를 통합함에 따라, 각 제조업체는 개별 나침반에서 200Hz로 쿼터너리 벡터를 애플리케이션 프로세서에 직접 출력하는 통합 허브로 전환하고 있으며, 이를 통해 개발 기간을 단축하고 있습니다.

지역별 분석

아시아태평양은 2025년 시장 규모의 48.79%를 차지하며, 전 세계 홀 효과 및 AMR 다이 시장의 약 70%를 공급하는 중국, 일본, 한국이 주도하고 있습니다. E-나침반 시장에서 상당한 점유율을 차지하고 있음에도 불구하고, 자동차 업계의 인증 주기가 24개월 이상 소요되고 OEM 업체들이 무결점 공급을 요구함에 따라 지역 업체들은 이익률 압박에 직면해 있습니다. 중국은 국내 휴대전화 및 전기차 조립을 통해 지역 내 출하량의 35%를 차지하고 있지만, 고성능 플럭스게이트 및 양자 센서에 대한 수출 규제로 인해 방위 분야에서의 도입이 제한되고 있어, Bewis Sensing과 같은 국내 기업들이 그 공백을 메우도록 장려하고 있습니다.

일본과 한국은 2028년까지 공급량을 보장하는 유럽 및 북미 OEM 업체들과의 장기 계약을 바탕으로, 자동차용 등급의 TMR 및 통합형 IMU 모듈을 전문으로 하고 있습니다. 인도는 2024년부터 2025년까지 총 12억 달러에 달하는 전자기기 제조 지원 정책에 힘입어 주요 전자기기 제조 거점으로 부상하고 있으며, 소비자용 및 산업용 시장에서 저비용 대체 거점으로서의 입지를 굳혀가고 있습니다. 아시아태평양의 E-컴퍼스 시장 규모는 꾸준히 확대될 것으로 예상되지만, 그 성장률은 유럽 및 미국 지역에 비해 완만할 것으로 보입니다.

중동은 가장 빠른 성장세를 보이고 있으며, 2031년까지 연평균 성장률(CAGR)은 19.84%로 전망됩니다. 이는 ‘사우디 비전 2030’이 현지에서의 센서 생산을 추진하고 있으며, 방위 프로그램이 ITAR(국제무기거래규정)의 적용 대상이 아닌 항법 시스템을 조달하고 있기 때문입니다. 텔레다인사가 2025년에 다믈 공장을 가동할 예정이며, 크로네사가 2026년에 현지 생산에 관한 양해각서(MoU)를 체결한 것은 지역 공급망의 부상을 뒷받침하는 사례입니다. 북미와 유럽을 합치면 2025년 매출의 32%를 차지했습니다. 이는 내방사선성과 경사 보정 기능을 갖춘 나침반이 필요한 항공우주, 방위, 산업용 로봇 분야가 주도하고 있습니다. 남미는 5% 미만에 그쳤지만, 브라질과 아르헨티나에서 정밀 농업이 발전함에 따라 센티미터 단위의 줄 간 유도 기능을 구현하는 GNSS 지원형 나침반 어레이의 도입이 확대되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the e-Compass market size is projected to be USD 2.56 billion in 2025, USD 2.84 billion in 2026, and reach USD 4.63 billion by 2031, growing at a CAGR of 10.29% from 2026 to 2031.

This report is Segmented by Technology (Hall-Effect, Anisotropic, Giant, Tunnel Magneto-Resistive, Fluxgate, and More), Axis Orientation (1-2-Axis, 3-Axis, and 6- and 9-Axis Sensor-Fusion), Application (Consumer Electronics, and More), Form Factor (Discrete Compass Modules, Integrated Sensor-Combo, SoC-Embedded E-Compass, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global E-Compass Market Trends and Insights

Proliferation of Smartphones Integrating Navigation Sensors

Smartphone subscriptions stood at 6.9 billion in 2025, and virtually every mid-tier or flagship handset embeds a 9-axis sensor hub that blends magnetometer, accelerometer, and gyroscope data for augmented-reality overlays and indoor navigation. Integrated combo modules trimmed bill-of-material cost by 25% and enabled sub-1 millimeter package heights suitable for foldable displays. Pedestrian dead-reckoning in subways and malls now depends on magnetometer-driven heading when GNSS is unavailable. Asahi Kasei's AK09974C, released in October 2025, achieves 0.15 µT resolution in a wafer-level 1.2 X 1.2 mm package, showcasing aggressive miniaturization. Because fewer than 40% of users perform manual figure-eight calibration, vendors are building auto-calibration based on machine-learning models harvested from millions of motion traces.

Rising Adoption of ADAS in Passenger and Commercial Vehicles

Advanced Driver Assistance Systems (ADAS) were shipped in 45% of new passenger vehicles in 2025, and each Level 2+ platform includes at least one 6-axis or 9-axis inertial measurement unit to meet ISO 26262 functional-safety requirements. Magnetometers within these IMUs correct gyroscope drift during prolonged highway driving, preventing cumulative heading error. TDK's PositionSense, qualified to AEC-Q100 Grade 1 in 2024, now ships to European and Japanese OEMs, prepping 2027 model launches. Fleet operators add compass-equipped telematics boxes that shave 3-5% fuel through optimized routing, offsetting the USD 15-25 incremental sensor cost. Mandatory emergency braking and lane-keeping systems introduced in the European Union from 2024 onward continue to elevate accident rates.

Susceptibility to Magnetic Interference and Calibration Drift

Local ferrous objects and current loops create magnetic disturbances exceeding 500 µT, orders above Earth's 25-65 µT field, causing heading errors beyond 30 degrees in phones, robots, and drones. Urban skyscrapers, subway rails, and factory motors exacerbate distortion. Only 60% of end users complete manual calibration, leaving a residual offset that degrades indoor navigation. Automotive systems mitigate drift by fusing GNSS and wheel-speed encoders, but stationary service robots must rely on lookup tables or periodically updated magnetic-anomaly maps. Asahi Kasei partnered with Aizip in December 2025 to crowd-source magnetic-field maps that shorten calibration cycles from days to hours.

Other drivers and restraints analyzed in the detailed report include:

- Miniaturization and Cost Reduction Through MEMS Processes

- Expansion of Wearable and XR Devices Demanding Ultrathin Compasses

- Commodity Pricing Pressure in Consumer-Grade Devices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hall-effect, TMR sensors commanded 42.19% of 2025 revenue, anchored by sub-nanotesla sensitivity and thermal stability that meet AEC-Q100 and IEC 61508 norms for powertrain, avionics, and factory automation. The E-Compass market for TMR modules is set to grow at a steady, high-single-digit pace as carmakers and industrial integrators choose the architecture for long-life-cycle platforms. Hall-effect alternatives keep share in cost-constrained phones because their unit cost stays below USD 0.40, but their 10 µT noise floor caps accuracy at around 5 degrees, a ceiling that limits premium adoption. Fluxgate compasses deliver sub-degree precision for submarines and aircraft, but consume 50-200 mW, so they remain niche.

Quantum compasses using nitrogen-vacancy diamond or optically pumped alkali vapor cells are poised to grow at a 10.99% CAGR through 2031, the fastest in the E-Compass market, because they resist magnetic interference in defense and subsea environments where heading drift is unacceptable. A 2024 laboratory record showed 0.1-degree accuracy, and prototypes are undergoing trials on autonomous vehicles. Vendors such as Q-Nav are packaging diamond sensors with FPGA controllers that filter microwave drive noise, slimming form factors to 45 cm3. Governments fund pilot deployments despite 5-10X higher power draw, betting that unmanned underwater or space platforms will prioritize accuracy over battery life. Parallel R&D in chip-scale optically pumped vapor cells could shrink quantum modules to several cubic centimeters by 2030.

Three-axis compasses still accounted for 61.18% of shipments in 2025 because they meet the cost ceilings for smartphones and drones and have well-understood legacy software stacks. E-Compass market share for single-axis and dual-axis units slipped to 12% as developers reject mechanical alignment constraints. Six-axis and nine-axis packages that integrate accelerometers and gyroscopes are forecast to rise 10.57% over 2026-2031, helped by automotive Tier-1 moves to single-system-in-package units that save 40% of board area and enable tightly coupled Kalman filters.

In the automotive domain, dual 9-axis setups provide redundancy to meet ISO 26262 compliance requirements, ensuring limp-home steering even if one sensor fails. Wearables exploit 9-axis hubs to recognize gestures and detect falls, as magnetometer data improves classifier accuracy by 15% when distinguishing rotation from translation. PNI Sensor's RM3100-based NaviGuider bundles continuous hard-iron and soft-iron autocalibration, aimed at ocean gliders that cannot surface for manual routines. As downstream firmware unifies sensor-fusion libraries, manufacturers are transitioning from discrete compasses to integrated hubs that deliver quaternion vectors at 200 Hz directly to application processors, reducing development time.

Geography Analysis

Asia-Pacific accounted for 48.79% of the 2025 value, driven by China, Japan, and South Korea, which supply roughly 70% of the global Hall-effect and AMR dies. Despite the large E-Compass market share, regional players face margin compression because automotive qualification cycles stretch past 24 months and OEMs demand zero-defect supply. China absorbs 35% of local shipments through domestic phone and EV assembly, yet export restrictions on high-grade fluxgate and quantum sensors limit defense uptake, spurring indigenous firms like Bewis Sensing to fill the gap.

Japan and South Korea specialize in automotive-grade TMR and integrated IMU modules under long-term contracts with European and North American OEMs that guarantee volume until 2028. India is emerging as a leading electronics manufacturing hub, supported by electronics manufacturing incentives totaling USD 1.2 billion during 2024-2025, positioning the country as a low-cost alternative for consumer and industrial markets. The E-Compass market size in Asia-Pacific is expected to expand steadily but at slower margins than in Western regions.

The Middle East shows the fastest trajectory, slated for a 19.84% CAGR through 2031, as Saudi Vision 2030 drives local sensor production and defense programs procure ITAR-free navigation systems. Teledyne's 2025 launch of its Dammam plant and KROHNE's 2026 localization MoU underscore thee riseof regional supply chains. North America and Europe together accounted for 32% of 2025 revenue, driven by the aerospace, defense, and industrial robotics sectors, which demand radiation-hardened, tilt-compensated compasses. South America remained below 5%, but precision agriculture in Brazil and Argentina is prompting the adoption of GNSS-aided compass arrays for centimeter-level row guidance.

- STMicroelectronics N.V.

- Honeywell International Inc.

- Robert Bosch GmbH (Bosch Sensortec GmbH)

- Asahi Kasei Microdevices Corporation

- NXP Semiconductors N.V.

- TDK Corporation (Invensense Inc.)

- MEMSIC Semiconductor (Shanghai) Co., Ltd.

- PNI Sensor Corporation

- Analog Devices, Inc.

- Alps Alpine Co., Ltd.

- Infineon Technologies AG

- TE Connectivity Ltd.

- Shanghai Bewis Sensing Technology LLC

- Ericco International Limited

- Jewell Instruments, LLC

- Melexis N.V.

- MagnaChip Semiconductor Corp.

- Renesas Electronics Corporation

- Lake Shore Cryotronics, Inc.

- VectorNav Technologies, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Supply-Chain Analysis

- 4.3 Regulatory Landscape

- 4.4 Technological Outlook

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Market Drivers

- 4.7.1 Proliferation of Smartphones Integrating Navigation Sensors

- 4.7.2 Rising Adoption of ADAS in Passenger and Commercial Vehicles

- 4.7.3 Miniaturization and Cost Reduction Through MEMS Processes

- 4.7.4 Expansion of Wearable and XR Devices Demanding Ultrathin Compasses

- 4.7.5 Autonomous Maritime Drones Needing Tilt-Compensated Heading

- 4.7.6 Precision-Ag-Robots Deploying Row-Guidance E-Compass Arrays

- 4.8 Market Restraints

- 4.8.1 Susceptibility to Magnetic Interference and Calibration Drift

- 4.8.2 Commodity Pricing Pressure in Consumer-Grade Devices

- 4.8.3 High Power Consumption in Fluxgate and Quantum Compass Designs

- 4.8.4 Export-Control Limits on High-Sensitivity Fluxgate Modules

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Hall-Effect

- 5.1.2 Anisotropic, Giant, Tunnel Magneto-Resistive

- 5.1.3 Fluxgate

- 5.1.4 Magneto-Inductive

- 5.1.5 Quantum

- 5.2 By Axis Orientation

- 5.2.1 1-2-Axis

- 5.2.2 3-Axis

- 5.2.3 6- and 9-Axis Sensor-Fusion

- 5.3 By Application

- 5.3.1 Consumer Electronics

- 5.3.2 Automotive

- 5.3.3 Aerospace and Defense

- 5.3.4 Industrial and Robotics

- 5.3.5 Marine and Sub-Sea

- 5.3.6 Healthcare and Wearables

- 5.4 By Form Factor

- 5.4.1 Discrete Compass Modules

- 5.4.2 Integrated Sensor-Combo

- 5.4.3 SoC-Embedded E-Compass

- 5.4.4 Dev-Boards and Custom ASICs

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.1.1 Saudi Arabia

- 5.5.4.1.2 United Arab Emirates

- 5.5.4.1.3 Rest of Middle East

- 5.5.4.2 Africa

- 5.5.4.2.1 South Africa

- 5.5.4.2.2 Egypt

- 5.5.4.2.3 Rest of Africa

- 5.5.4.1 Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 STMicroelectronics N.V.

- 6.4.2 Honeywell International Inc.

- 6.4.3 Robert Bosch GmbH (Bosch Sensortec GmbH)

- 6.4.4 Asahi Kasei Microdevices Corporation

- 6.4.5 NXP Semiconductors N.V.

- 6.4.6 TDK Corporation (Invensense Inc.)

- 6.4.7 MEMSIC Semiconductor (Shanghai) Co., Ltd.

- 6.4.8 PNI Sensor Corporation

- 6.4.9 Analog Devices, Inc.

- 6.4.10 Alps Alpine Co., Ltd.

- 6.4.11 Infineon Technologies AG

- 6.4.12 TE Connectivity Ltd.

- 6.4.13 Shanghai Bewis Sensing Technology LLC

- 6.4.14 Ericco International Limited

- 6.4.15 Jewell Instruments, LLC

- 6.4.16 Melexis N.V.

- 6.4.17 MagnaChip Semiconductor Corp.

- 6.4.18 Renesas Electronics Corporation

- 6.4.19 Lake Shore Cryotronics, Inc.

- 6.4.20 VectorNav Technologies, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment