|

시장보고서

상품코드

2062417

전용 백업 어플라이언스(PBBA) 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Purpose-Built Backup Appliance (PBBA) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

통합 시스템은 2025년 판매량 61.32%를 차지해 스토리지 미디어, 소프트웨어, 중복 배제 기능을 단일 SKU에 통합하는 것으로, 전용 백업 어플라이언스 시장 점유율을 촉진 했습니다.

은행 및 의료 분야의 구매자들은 통합된 지원 체계와 예측 가능한 유지보수 기간을 높이 평가했습니다. Commvault나 Veeam을 표준으로 채택한 기업들은 소프트웨어 종속성을 피할 수 있는 프로토콜을 지원하는 유연한 스토리지 풀을 선호하기 때문에 타겟 어플라이언스 시장은 2031년까지 연평균 성장률(CAGR) 11.34%를 나타낼 것으로 전망됩니다.

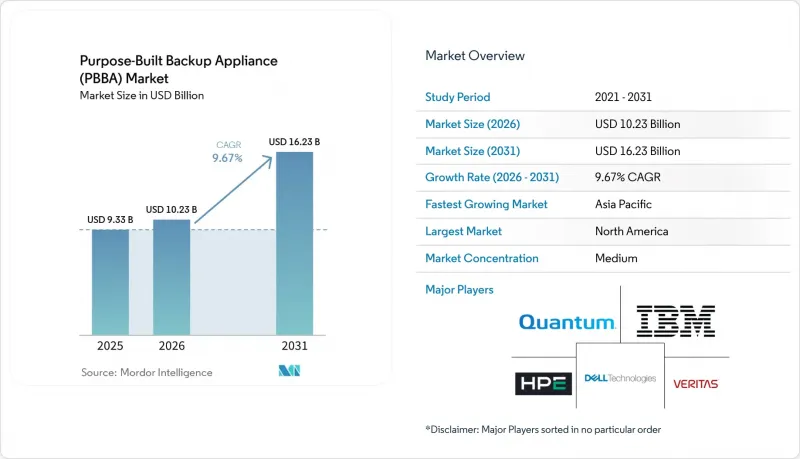

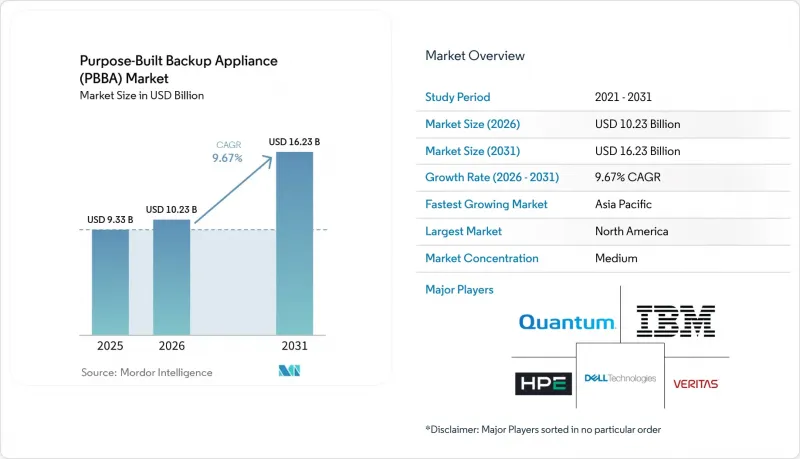

Mordor Intelligence에 따르면, 전용 백업 어플라이언스(PBBA) 시장 규모는 2025년에 93억 3,000만 달러로 평가되었고, 2026년에는 102억 3,000만 달러로 확대될 것으로 예측됩니다. 본 보고서는 어플라이언스 유형(통합형 PBBA, 타겟형 PBBA), 도입 형태(On-Premise, 클라우드 연결형 등), 폼 팩터(랙 마운트형, 타워형 등), 최종 사용자 산업(은행 및 금융 서비스, 의료, 생명과학, 정부·국방, 소매 및 전자상거래 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 전용 백업 어플라이언스(PBBA) 시장 동향 및 인사이트

랜섬웨어 공격이 급증함에 따라, 불변성 백업 대상에 대한 수요가 높아지고 있습니다.

랜섬웨어 공격자들은 성공적인 침해 사례의 96%에서 백업 저장소를 침해하므로, 불변 스토리지야말로 최전선 방어 수단이 됩니다. ExaGrid의 네트워크에 직접 연결되지 않은 저장소 계층과 같은 계층형 아키텍처는 이제 데이터를 운영 네트워크로부터 격리합니다. AI 기반 이상 탐지 기능은 의심스러운 삭제 시도를 감지하고 자동화된 안전 장치를 작동시킵니다. 사이버 보험사들은 인증된 불변 저장 대상을 도입한 고객에게 보험료를 10-15% 할인해 주고 있습니다. Object First의 Ootbi 어플라이언스는 완벽한 에어 갭을 유지하면서 11-9 수준의 내구성을 달성합니다. 이러한 경제적 및 보안상의 인센티브는 규제 대상 산업 전반에 걸쳐 전용 백업 어플라이언스(PBBA) 시장의 도입을 가속화하고 있습니다.

OECD 및 BRICS 국가들의 데이터 주권 및 사이버 복원력에 관한 규제 의무화

인도의 ‘디지털 개인 데이터 보호법’은 결제 데이터의 국내 저장을 의무화하고 있어, 현지에서의 어플라이언스 도입을 촉진하고 있습니다. 유럽에서 GDPR(EU 개인정보보호규정)이 시행됨에 따라 13억 2,000만 유로의 벌금이 부과되면서, 검증 가능한 백업 관리의 필요성이 더욱 커지고 있습니다. 브라질의 AI 전략은 디지털 주권에 관한 논의를 다시 불러일으켰으며, 지역 인프라의 역할을 부각시켰습니다. 오브젝트 잠금 및 지오펜싱 기능을 갖춘 어플라이언스를 통해 기업은 운영상의 유연성을 저해하지 않으면서도 데이터 상주 규정을 준수할 수 있습니다. InCountry와 같은 ‘Data-Residency-as-a-Service’ 플랫폼은 규정 준수를 충족하는 지역별 백업 노드에 대한 새로운 수요를 부각시키고 있습니다. NIST의 개정된 프레임워크에서는 백업의 무결성이 필수적인 복원력 관리 조치로 포함되어 있습니다.

에이전트리스형 클라우드 백업 서비스(BaaS)의 도입 확대가 On-Premise PBBA의 비용을 절감

클라우드 네이티브 솔루션은 어플라이언스 보유에 비해 총 소유 비용(TCO)을 40-60% 절감하면서도 에이전트 없는 보호 기능을 제공합니다. Veeam과 Microsoft의 파트너십은 AI 분석을 정책 관리에 활용하여 SaaS를 우선시하는 구매자들의 관심을 끌고 있습니다. 그럼에도 불구하고 데이터 현지화 규정이나 복구 시간 목표(RTO) 요건으로 인해 하이브리드 모델의 중요성은 여전히 유지되고 있으며, Commvault가 Clumio를 인수하여 클라우드 지원 범위를 확대한 배경에는 이러한 사정이 있습니다. 따라서 각 벤더사는 기존 하드웨어 제품군에 구독 서비스를 결합함으로써 리스크를 분산시키고 있습니다. 문제는 설비 투자의 방향이지, 전용 백업 어플라이언스 시장의 소멸이 아닙니다.

부문별 분석

타겟 플랫폼에 연계된 전용 백업 어플라이언스 시장 규모는 컨테이너 네이티브 데이터 흐름 및 멀티 클라우드 워크로드의 이동성 덕분에 예측 기간 후반에 통합형 모델을 넘어설 것으로 예측됩니다.

모듈식 라이선싱으로 인해 통합형과 타겟형의 구분이 모호해지고 있습니다. Quantum의 DXi 시리즈 펌웨어에서는 관리자가 하드웨어를 교체하지 않고도 모드를 전환할 수 있게 되었습니다. 이러한 유연성 덕분에 자산 수명이 최대 3개의 예산 주기만큼 연장되며, 용도 포트폴리오가 변경될 때 단계적인 전환이 지원됩니다. 또한, 벤더가 어플라이언스를 전면 교체하는 대신 무선으로 업데이트함으로써 고객 이탈을 줄이고, 지속적인 수익 기반을 마련하고 있습니다.

지연 시간에 민감한 워크로드와 주권 관련 법률로 인해 오프사이트 복제가 제한됨에 따라, On-Premise 도입은 2025년 지출의 49.82%를 계속 차지했습니다. 하이브리드 방식은 기업이 핫 데이터를 로컬 플래시 스토리지에 보관하면서 장기 보존용 사본을 저비용 오브젝트 스토리지로 전송함으로써 콜드 데이터 세트의 스토리지 비용을 절반 이상 절감할 수 있어, 2031년까지 연평균 성장률(CAGR) 10.46%로 성장하고 있습니다. WAN 최적화 알고리즘이 성숙 단계에 접어들었고, 클라우드에서 대량의 데이터를 복원할 때 발생하는 데이터 전송 비용이 여전히 높기 때문에 하이브리드 아키텍처와 관련된 전용 백업 어플라이언스 시장 규모는 꾸준히 확대될 전망입니다.

하지만 네트워크 대역폭이 클라우드 복제 용량을 제한하는 경우가 많아, 하이퍼스케일러에서 100TB를 복원할 경우 9,000달러의 전송 비용이 발생할 수 있습니다. 현재 각 벤더사는 계층형 중복 제거, 적응형 티어링, 대역폭 제어를 결합하여 제공합니다. ExaGrid의 2026년 1월 릴리스에서는 복구될 가능성이 가장 높은 데이터 세트를 우선적으로 처리하여, 미션 크리티컬한 오브젝트를 위해 대역폭을 확보합니다. 이러한 기능 강화로 인해, 복구 시간 목표(RTO)를 저해하지 않으면서 하이브리드 환경의 장점이 더욱 확대됩니다.

지역별 분석

북미는 2025년 수익의 37.78%를 차지하며, 이 지역의 사이버 보험 인수사는 보험 계약자에게 지속적인 백업 운영과 분기별 복구 테스트를 의무화하고 있습니다. 2025년, 해당 지역의 데이터센터 시장 공실률은 1.4%까지 떨어졌으며, 북부 버지니아주에서만 1,102MW의 추가 용량이 흡수되었습니다. 이러한 상황은 코로케이션 시설 내에 설치되는 고밀도 백업 장비에 대한 수요를 더욱 높였습니다. kW당 190달러를 넘는 전력 가격으로 인해, 조달 동향은 Dell의 PowerProtect DP5500과 같은 수냉식 어플라이언스 제품으로 전환되었습니다. 이 제품은 랙 유닛당 중복 제거 처리량을 향상시키는 동시에 열 부하를 줄여줍니다.

아시아태평양은 2025년부터 2030년까지 24GW의 용량을 추가하는 7,720억 달러 규모의 데이터센터 계획에 힘입어, 2031년까지 연평균 성장률(CAGR) 9.96%를 나타낼 것으로 전망됩니다. 인도의 설치 용량은 2032년까지 6배로 확대될 가능성이 있으며, 말레이시아 조호르주는 이미 897MW를 보유하고 있으며 공실률은 1% 미만입니다. 국경을 넘는 데이터 복제를 금지하는 주권법으로 인해 기업들은 현지 백업 어플라이언스를 도입할 수밖에 없게 되었으며, 하이퍼스케일 클라우드의 보급이 더딘 지역에서 전용 백업 어플라이언스 시장이 확대되고 있습니다. KPMG는 해당 지역의 데이터센터 전력 수요가 2030년까지 37,580MW에 달하고, 2024년 대비 165% 증가할 것으로 전망하고 있으며, 이에 따라 데이터 보호 인프라에 대한 수요도 가속화될 것으로 보입니다.

유럽의 성장은 금융 서비스 분야의 DORA(데이터 보호 규정) 준수에 힘입고 있는 반면, 중동 및 아프리카의 성장세는 다수의 GPU를 탑재한 데이터센터에 6GW를 할당하는 사우디아라비아의 HUMAIN 프로젝트와 같은 국가 주도의 AI 인프라에 기인하고 있습니다. 이러한 신규 시설에서는 10TB 규모의 모델 체크포인트를 수 분 이내에 복원할 수 있는 플래시 스토리지를 광범위하게 활용한 백업 어플라이언스가 필요하며, 이는 GPU에 최적화된 플랫폼에 대한 틈새 수요를 견인하고 있습니다. 남미 시장은 여전히 규모가 작으며, 브라질의 금융 규제 당국과 아르헨티나의 통신 사업자가 주요 구매층을 이루고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19Integrated systems generated 61.32% of 2025 revenue, anchoring the purpose-built backup appliance market share by combining storage media, software, and deduplication in a single SKU. Banking and healthcare buyers appreciate the unified support path and predictable maintenance windows. Target appliances are projected to log an 11.34% CAGR through 2031 as enterprises that standardize on Commvault or Veeam favor protocol-flexible storage pools that avoid software lock-in.

According to Mordor Intelligence, the market size of the Purpose-Built Backup Appliance (PBBA) market was valued at USD 9.33 billion in 2025 and is expected to increase to USD 10.23 billion in 2026. This report is Segmented by Appliance Type (Integrated PBBA, and Target PBBA), Deployment Mode (On-Premises, Cloud-Connected, and More), Form Factor (Rack-Mounted, Tower, and More), End-User Industry (Banking and Financial Services, Healthcare, Life Sciences, Government and Defense, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Purpose-Built Backup Appliance (PBBA) Market Trends and Insights

Exploding Ransomware Incidents Elevating Demand for Immutable Backup Targets

Ransomware attackers compromise backup repositories in 96% of successful breaches, making immutable storage a frontline defense. Tiered architectures such as ExaGrid's non-network-facing repository layer now isolate data from production networks. AI-driven anomaly detection flags suspicious deletions and triggers automated safeguards. Cyber-insurance providers grant 10-15% premium reductions to clients deploying certified immutable targets. Object First's Ootbi appliance achieves eleven-nines durability while maintaining a complete air gap. These economic and security incentives accelerate Purpose-Built Backup Appliance market adoption across regulated industries.

Mandatory Data-Sovereignty and Cyber-Resiliency Regulations in OECD and BRICS

India's Digital Personal Data Protection Act requires in-country storage for payment data, pushing local appliance deployments. GDPR enforcement in Europe has levied EUR 1.32 billion in fines, reinforcing the need for verifiable backup controls. Brazil's AI strategy revived the debate on digital sovereignty, highlighting the role of localized infrastructure. Appliances with object-lock and geo-fencing enable enterprises to satisfy residency rules without ceding operational flexibility. Data-Residency-as-a-Service platforms such as InCountry underscore emerging demand for compliant regional backup nodes. NIST's revised framework now embeds backup integrity as a mandatory resilience control.

Rising Adoption of Agentless Cloud Backup-as-a-Service Reducing On-Prem PBBA Spend

Cloud-native offerings deliver agentless protection with 40-60% lower total cost of ownership compared with appliance ownership. Veeam's Microsoft partnership channels AI analytics into policy management, attracting SaaS-first buyers. Even so, data-localization rules and recovery-time guarantees keep hybrid models relevant, prompting Commvault's acquisition of Clumio to widen cloud coverage. Vendors thus hedge with subscription services layered on existing hardware portfolios. The restraint lies in diverted cap-ex, not the elimination of the Purpose-Built Backup Appliance market.

Other drivers and restraints analyzed in the detailed report include:

- Cloud-Connected PBBA Integrated into Hybrid-IT Architectures

- Hardware-Level Support for Object-Lock and WORM Enabling Cyber-Insurance Discounts

- Budget Squeeze Amid Macro IT Cap-ex Re-Prioritization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The purpose-built backup appliance market size attached to target platforms is expected to outpace integrated models in the second half of the forecast horizon, driven by container-native data flows and multi-cloud workload mobility.

Modular licensing blurs the integrated-versus-target distinction. Quantum's DXi-series firmware now lets administrators flip between modes without swapping hardware. This elasticity extends asset life by up to three budget cycles and supports phased migrations when application portfolios shift. Vendors updating appliances over-the-air rather than through forklift replacements also reduce customer churn and seed recurring revenue.

On-premises installations retained 49.82% of 2025 spending as latency-sensitive workloads and sovereignty laws restrict off-site replication. Hybrid deployments are scaling at a 10.46% CAGR to 2031 because firms keep hot restores on local flash while pushing long-term copies to low-cost object stores, cutting storage expense by more than half for cold data sets. The purpose-built backup appliance market size tied to hybrid architectures should climb steadily as WAN optimization algorithms mature and cloud egress fees remain punitive for bulk restores.

Nevertheless, network bandwidth often caps cloud replication volume, and a 100 TB recovery from a hyperscaler can incur USD 9,000 in transfer fees. Suppliers now bundle layered deduplication, adaptive tiering, and bandwidth throttling. ExaGrid's January 2026 release prioritizes datasets most likely to be restored, freeing bandwidth for mission-critical objects. These enhancements widen the hybrid appeal without compromising recovery-time objectives.

Geography Analysis

North America generated 37.78% of 2025 revenue, its cyber-insurance underwriters compelling policyholders to operate immutable backups and quarterly restore tests. Vacancy in the region's data-center market fell to 1.4% during 2025, and Northern Virginia alone absorbed 1,102 MW of additional capacity, a scenario that amplified appetite for high-density backup gear placed inside colocation suites. Power pricing above USD 190 per kW tipped procurement toward liquid-cooled appliance lines such as Dell's PowerProtect DP5500, which boosts deduplication throughput per rack unit while cutting thermal load.

Asia-Pacific is on track for a 9.96% CAGR through 2031, undergirded by USD 772 billion in data-center pipelines that add 24 GW of capacity between 2025 and 2030. India's installed base could multiply sixfold by 2032, and Johor, Malaysia, already hosts 897 MW with a sub-1% vacancy rate. Sovereignty laws barring cross-border replication obligate enterprises to deploy local backup appliances, bolstering the purpose-built backup appliance market in jurisdictions where hyperscale cloud coverage lags. KPMG projects the region's data-center power demand will climb to 37,580 MW by 2030, a 165% jump from 2024 levels, indicating corresponding acceleration for associated data-protection infrastructure.

Europe's growth leans on DORA compliance across financial services, while Middle East and Africa momentum stems from sovereign AI infrastructure such as Saudi Arabia's HUMAIN project that earmarks 6 GW for GPU-rich data halls. These new facilities require flash-heavy backup appliances able to restore 10 TB model checkpoints within minutes, driving niche demand for GPU-tuned platforms. South America remains modest in scale, with Brazil's financial regulators and Argentina's telecom operators forming the primary purchase base.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- International Business Machines Corporation

- Quantum Corporation

- Veritas Technologies LLC

- Hitachi Vantara LLC

- Cohesity Inc.

- Commvault Systems Inc.

- ExaGrid Systems Inc.

- Fujitsu Limited

- NetApp Inc.

- Oracle Corporation

- Arcserve LLC

- Rubrik Inc.

- Veeam Software AG

- StorageCraft Technology Corporation

- Acronis International GmbH

- Unitrends Inc.

- Barracuda Networks Inc.

- Spectra Logic Corporation

- Druva Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Data Volumes From Edge-Generated Workloads

- 4.2.2 Stricter Global Data Protection Regulations

- 4.2.3 Declining Cost per Terabyte of Flash Storage

- 4.2.4 Integration of Backup Appliances With Cyber-Recovery Vaults

- 4.2.5 Growing Adoption of Containerized Application Architectures

- 4.2.6 ESG-Driven IT Modernization Mandates

- 4.3 Market Restraints

- 4.3.1 Proliferation of Cloud-Native Backup-as-a-Service Offerings

- 4.3.2 Budget Freezes in Public Sector IT Modernization

- 4.3.3 Skills Gap in Advanced Data Protection Administration

- 4.3.4 High Energy Consumption of On-Premises Appliances

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 Segmentation by Appliance Type

- 5.1.1 Integrated PBBA

- 5.1.2 Target PBBA

- 5.2 Segmentation by Deployment Mode

- 5.2.1 On-Premises

- 5.2.2 Cloud-Connected

- 5.2.3 Hybrid

- 5.3 Segmentation by Form Factor

- 5.3.1 Rack-Mounted

- 5.3.2 Tower

- 5.3.3 Modular / Scale-Out Nodes

- 5.4 Segmentation by End-User Industry

- 5.4.1 Banking and Financial Services

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Government and Defense

- 5.4.4 Telecom and Media

- 5.4.5 Manufacturing

- 5.4.6 Retail and e-Commerce

- 5.5 Segmentation by Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Dell Technologies Inc.

- 6.4.2 Hewlett Packard Enterprise Company

- 6.4.3 International Business Machines Corporation

- 6.4.4 Quantum Corporation

- 6.4.5 Veritas Technologies LLC

- 6.4.6 Hitachi Vantara LLC

- 6.4.7 Cohesity Inc.

- 6.4.8 Commvault Systems Inc.

- 6.4.9 ExaGrid Systems Inc.

- 6.4.10 Fujitsu Limited

- 6.4.11 NetApp Inc.

- 6.4.12 Oracle Corporation

- 6.4.13 Arcserve LLC

- 6.4.14 Rubrik Inc.

- 6.4.15 Veeam Software AG

- 6.4.16 StorageCraft Technology Corporation

- 6.4.17 Acronis International GmbH

- 6.4.18 Unitrends Inc.

- 6.4.19 Barracuda Networks Inc.

- 6.4.20 Spectra Logic Corporation

- 6.4.21 Druva Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment