|

시장보고서

상품코드

2062418

리모트 브라우저 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Remote Browser - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

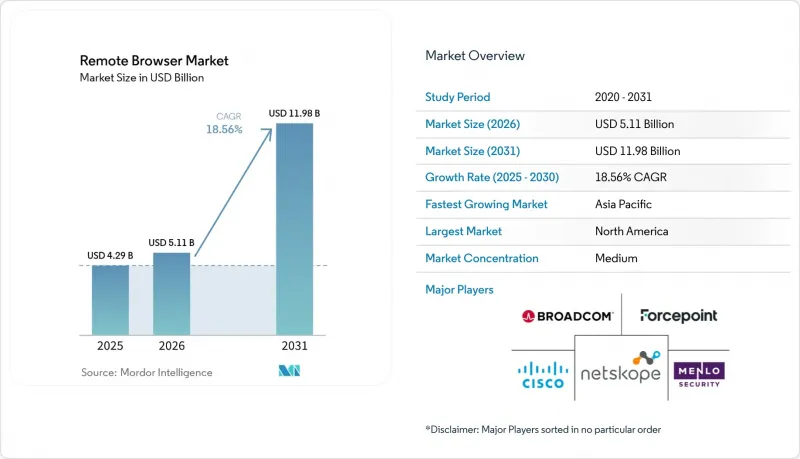

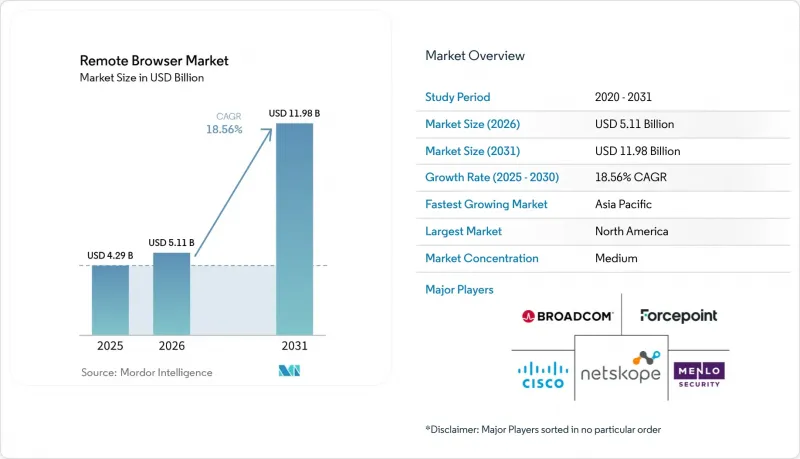

Mordor Intelligence에 의하면, 리모트 브라우저 시장 규모는 2025년에 42억 9,000만 달러로 평가되었고, 2026년 51억 1,000만 달러로 추정되고, 2031년까지 119억 8,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 18.56%를 나타낼 전망입니다.

본 보고서는 도입 형태별(클라우드 기반, 온프레미스형, 하이브리드형), 기술 유형별(DOM 재구축, 픽셀 푸싱 등), 기업 규모별(대기업, 중소기업), 최종 사용자 산업 분야별(은행, 금융서비스 및 보험(BFSI), IT 및 통신, 정부 및 국방, 의료, 교육 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 리모트 브라우저 시장 동향 및 인사이트

제로 트러스트 보안 프레임워크의 보급

NIST 특별 간행물 800-207, CISA의 제로 트러스트 성숙도 모델, 그리고 국가안보국(NSA)의 구현 지침은 각각 리모트 브라우저 격리를 데이터 보호를 위한 고급 제어 수단으로 규정함으로써, 미국 연방 정부 및 금융 부문 전반에 걸친 예산 배정을 가속화했습니다. 영국의 '사이버 보안 및 복원력 법'은 디지털 서비스 제공업체에 유사한 요건을 부과함으로써, 통신 및 공공 서비스 분야에서의 도입을 촉진했습니다. 기존의 보안 웹 게이트웨이를 브라우저 네이티브 제로 트러스트 제어 방식으로 교체한 기관에서는 1년 이내에 지연 시간이 30% 감소하고, 횡방향 이동(lateral movement) 사고가 60% 감소했다고 보고되었습니다. 이러한 추세가 맞물리면서, 전 세계 기업들은 리모트 브라우저 시장을 실험적인 시범 단계에서 핵심 아키텍처로 격상시킬 수밖에 없게 되었습니다. 각 벤더사는 ID 인식 프록시에 직접 대응하는 모듈을 제공함으로써 이에 부응하여, 정책 적용을 간소화하고 조달 주기를 수년 단위에서 수개월 단위로 단축했습니다.

중요 인프라에서의 브라우저 분리 의무화(2025년 이후 NIST 및 EU-NIS2)

NIS2 지침에 따라, 중요 서비스 사업자는 2024년 10월까지 브라우저 분리를 의무화해야 합니다. 한편, 독일의 BSI는 C5 인증의 적용 범위를 확대하고 데이터 처리 장소를 공개하도록 요구함에 따라, 규제 대상 기업들은 하이브리드 또는 On-Premise 환경에서 서비스를 제공해야만 했습니다. 미국에서는 2025년 이후 NIST 지침에 따라 중요 인프라 사업자의 브라우저 분리가 '권장'에서 '필수'로 변경되었으며, 2026 회계연도 연방 예산에서는 제로 트러스트 브라우저 도구에 12억 달러가 배정되었습니다. 프랑스의 SecNumCloud 인증은 주권적 인프라가 구축되지 않은 한, 미국 측의 공공 부문 데이터에 대한 관리 접근을 허용하지 않음으로써 압박을 한층 더 강화했습니다. 이러한 규제의 통합으로 인해 규정 준수는 즉각적인 구매 요인이 되었으며, 유럽 및 북미 전역에서 단기적인 수주를 촉진하여 리모트 브라우저 시장을 규정 준수의 필수 요건으로 확고히 자리매김하게 했습니다.

고해상도 웹 애플리케이션의 지연 및 UX 문제

픽셀 단위로 데이터를 전송하는 스트림은 1.4초에서 11.9초의 연결 지연을 유발합니다. 이는 브라우저 기반 CAD, 화상 회의, 실시간 거래 플랫폼의 경우 용납될 수 없는 일입니다. Google의 'Interaction to Next Paint' 지표로 인해 반응성이 순위 결정 요인으로 중요시되면서, 속도를 저하시키는 보안 오버레이에 대한 고객의 용인도가 낮아졌습니다. Zscaler와 같은 벤더들은 SquareX 인수를 통해 네트워크 벡터 렌더링을 도입했으나, IT 리더의 41%는 여전히 완전한 도입에 있어 가장 큰 장애물로 지연 문제를 꼽고 있습니다. 이러한 제약은 에지 노드가 드문 지역에서 가장 심각하며, 그곳에서는 왕복 시간이 대화형 워크로드의 허용 한계를 초과합니다.

부문별 분석

조직들이 데이터 소재지 규제와 성능 요건을 모두 충족하기 위해 노력함에 따라, 하이브리드 배포는 2026-2031년 연평균 18.22%의 성장률을 보일 것으로 예측되며, 이는 클라우드 전용이나 온프레미스 방식보다 더 높은 성장세를 보일 전망입니다. 2025년에는 통합 과정에서 발생하는 마찰을 해소한 하이퍼스케일러의 SASE 번들 솔루션에 힘입어, 클라우드 기반 서비스가 리모트 브라우저 시장의 62.19% 점유율을 차지했습니다. 유럽의 '헬스 데이터 스페이스 규정' 및 프랑스의 'SecNumCloud' 규정에 따라, 의료 서비스 제공업체는 보호 대상 데이터를 EU 역내에 보관해야 할 의무가 부과되었으며, 기밀성이 높은 워크플로는 온프레미스에서 처리하고 일반적인 브라우징은 클라우드 포드에 맡기는 듀얼 스택 아키텍처의 도입이 촉진되었습니다.

이러한 하이브리드 방식은 지연 시간 단축에도 기여하고 있습니다. 위험이 있는 도메인은 격리된 클라우드 컨테이너를 통해 라우팅하고, 신뢰할 수 있는 SaaS는 네이티브로 로드함으로써 응답 시간을 최대 40% 단축하고 있습니다. AWS는 운영자만 접근할 수 있도록 보장하는 유럽의 소버린 존에 78억 유로(88억 달러)를 배정했습니다. 이는 데이터 현지화가 더 이상 선택 사항이 아니라 필수 사항이 되었음을 보여주는 신호입니다. 소버린 클라우드의 용량이 확대됨에 따라, 하이브리드 격리는 은행, 의료 시스템, 공공기관을 위한 표준 설계 모델로 자리 잡고 있습니다. 이러한 추세는 리모트 브라우저 시장에서 지속적인 수익 창출을 주도하고 있으며, 지역별 규정 준수를 핵심으로 하는 공급업체의 로드맵을 더욱 확고히 하고 있습니다.

DOM 재구성은 보안과 네이티브에 가까운 사용자 경험의 균형을 동시에 달성하기 위해, 2025년에는 55.83%의 점유율을 차지했으며, 리모트 브라우저 시장을 장악했습니다. 그러나 시그니처 업데이트에 의존하고 있다는 점 때문에 취약점이 발생하며, 제로데이 공격이 감지를 회피하고 시스템에 침입할 여지를 남기고 있습니다. 픽셀 푸싱은 보다 안전한 접근 방식을 제공함으로써 이러한 위험을 효과적으로 제거합니다. 이 방식은 특히 복잡한 용도의 경우, 대역폭 소비 증가나 200밀리초를 초과하는 지연 등 심각한 단점이 따릅니다.

네트워크 벡터 렌더링은 전체 프레임을 전송하는 대신 엔드포인트에 컨텐츠 렌더링 방법을 지시함으로써 서버의 연산 부하를 절반으로 줄이고 지연 시간을 대폭 단축하여 연평균 성장률(CAGR) 18.91%를 기록했습니다. Zscaler의 SquareX 통합 및 Palo Alto Networks의 브라우저 네이티브 엔진은 벤더들이 리모트 데이터 플레인이 아닌 런타임 내에 보호 기능을 통합하고 있음을 보여줍니다. 지연을 용납할 수 없는 금융 거래 데스크나 방사선과 검사실이 초기 도입처로 꼽히고 있습니다. 앞으로 이러한 장점들로 인해 DOM 재구성의 우위는 점차 사라지고, 리모트 브라우저 시장 내의 수익 구조가 재편될 것으로 예측됩니다.

지역별 분석

2025년 리모트 브라우저 시장 규모에서 북미는 45.34%를 차지했습니다. 이는 미국 연방 정부의 제로 트러스트 의무화와 월가 은행들의 SASE 도입 가속화에 힘입은 결과입니다. 2026년도 예산에 따른 지속적인 자금 투입과 더불어, 캐나다의 GDPR(EU 개인정보보호규정)에 부합하는 정보 유출 규제로 인해 기업 수요는 유지되겠지만, 1차 공급업체 시장의 포화 상태가 다가옴에 따라 성장은 둔화될 것입니다. 해당 지역의 고밀도 엣지 그리드 덕분에 평균 지연 시간이 20밀리초 미만으로 유지되어, 클라우드 배포에 있어 성능상의 이점을 제공합니다. 경쟁이 치열해지는 가운데, Zscaler, Palo Alto Networks, Cloudflare가 세션 시작 시간 단축을 놓고 경쟁하는 반면, Authentic8과 같은 틈새 시장 업체들은 방위 산업 관련 기업을 대상으로 견고한 환경을 제안하고 있습니다.

아시아태평양은 다국적 기업들에게 국내 렌더링 노드 설치를 장려하는 중국, 인도, 베트남의 현지화 법안에 힘입어 2031년까지 연평균 성장률(CAGR) 18.28%를 나타낼 것으로 예측되며, 이는 지역별로는 가장 높은 수치입니다. 아카마이는 2024년 아시아에서 800억 건 이상의 웹 애플리케이션 공격을 기록했으며, 이 중 110억 건이 API를 표적으로 삼아 경계 방어 체계의 취약성이 여실히 드러났습니다. 일본과 한국은 EU의 적정성 인정의 혜택을 누리고 있지만, 국내 구매자들은 여전히 고객의 데이터 주권에 대한 기대에 부응하기 위해 하이브리드 방식을 선호하고 있습니다. 호주의 중요 인프라 관련 개정법과 싱가포르의 핀테크 추진은 규제 불균일성이 다지역 진출을 필요로 하는 이 지역의 특징을 잘 보여주고 있으며, 이로 인해 리모트 브라우저 시장의 총 잠재 시장 규모가 확대되고 있습니다.

유럽에서는 NIS2, 데이터법, 그리고 향후 시행될 유럽 건강 데이터 공간 규제로 인해 촉발된 규정 준수 열풍에 동참하고 있습니다. 프랑스의 SecNumCloud 규정은 EU 전용 관리 도메인을 구축하지 않는 한, 비주권적인 미국 공급업체를 사실상 배제하고 있습니다. 이에 반해 AWS는 78억 유로(88억 달러) 규모의 주권 프로그램으로 대응했으며, 마이크로소프트는 15개국에서 국내 내 Copilot 처리를 약속했습니다. 독일의 BSI는 C5 감사에 위치 투명성을 추가하고, 은행들이 신뢰할 수 있는 SaaS와 기밀성이 높은 워크로드를 분리하는 하이브리드 구성으로 전환할 것을 권장하고 있습니다. 남미와 중동 및 아프리카는 뒤처져 있지만, 성장세가 가속화될 조짐이 보입니다. 브라질의 은행 규제, 사우디아라비아의 '비전 2030', 남아프리카공화국의 금융 시범 사업은 해당 지역의 법규가 리모트 브라우저 시장을 지속적으로 확대하고 있음을 보여줍니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the remote browser market size was valued at USD 4.29 billion in 2025 and estimated to grow from USD 5.11 billion in 2026 to reach USD 11.98 billion by 2031, at a CAGR of 18.56% during the forecast period (2026-2031).

This report is Segmented by Deployment Mode (Cloud-Based, On-Premise, and Hybrid), Technology Type (DOM Reconstruction, Pixel Pushing, and More), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (BFSI, IT and Telecommunications, Government and Defense, Healthcare, Education, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Remote Browser Market Trends and Insights

Proliferation of Zero-Trust Security Frameworks

NIST Special Publication 800-207, CISA's Zero Trust Maturity Model, and the National Security Agency's implementation guidance each positioned remote browser isolation as an advanced control for data protection, accelerating budget allocation across U.S. federal and financial sectors.The United Kingdom's Cyber Security and Resilience Act replicated these expectations for digital service providers, thereby driving adoption across telecommunications and public services. Agencies that replaced legacy secure web gateways with browser-native zero-trust controls reported a 30% reduction in latency and a 60% drop in lateral movement incidents within 1 year. Combined, these policies compelled global enterprises to elevate the remote browser market from experimental pilot to core architecture. Vendors responded with modules that map directly to identity-aware proxies, simplifying policy enforcement and closing procurement cycles in months rather than years.

Mandatory Browser Isolation for Critical Infrastructure (Post-2025 NIST and EU-NIS2)

The NIS2 Directive required operators of essential services to isolate browsers by October 2024, while Germany's BSI broadened C5 attestation to expose data-processing locales, forcing regulated entities toward hybrid or on-premise rendering. In the United States, post-2025 NIST guidance moved browser isolation from recommended to expected for critical infrastructure operators, and FY 2026 federal budgets earmarked USD 1.2 billion for zero-trust browser tools. France's SecNumCloud qualification compounded pressure by disallowing U.S. administrative access to public-sector data unless sovereign infrastructure is in place. These converging rules turned compliance into an immediate buying trigger, lifting near-term bookings across Europe and North America and solidifying the remote browser market as a compliance necessity.

Latency and UX Issues in High-Fidelity Web Apps

Pixel-pushing streams introduce connection delays of 1.4 to 11.9 seconds, which are unacceptable for browser-based CAD, video conferencing, and real-time trading platforms. Google's Interaction to Next Paint metric elevated responsiveness to a ranking factor, raising customer intolerance for any security overlay that hampers speed. Although vendors such as Zscaler adopted network vector rendering through the SquareX acquisition, 41% of IT leaders still cite latency as the top barrier to full deployment. The constrain is most severe in regions with sparse edge nodes, where round-trip times eclipse acceptable thresholds for interactive workloads.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Sophisticated Web-Based Phishing-as-a-Service Kits

- Work-from-Anywhere Permanence Boosting SaaS Attack Surface

- Budget Compression in SME Cybersecurity Stacks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid deployments are forecast to grow at 18.22% between 2026 and 2031, outpacing cloud-only and on-premise alternatives as organizations reconcile data-residency statutes with performance needs. Cloud-based services owned 62.19% of the Remote Browser Market share in 2025, propelled by SASE bundles from hyperscalers that eliminated integration friction. Europe's Health Data Space Regulation and France's SecNumCloud rules forced healthcare providers to keep protected data on EU soil, prompting dual-stack architectures that steer sensitive workflows to on-premise rendering while leaving general browsing to cloud pods.

The hybrid approach also mitigates latency, routing risky domains through isolated cloud containers while allowing trusted SaaS to load natively, slicing response times by as much as 40%. AWS earmarked EUR 7.8 billion (USD 8.8 billion) for European sovereign zones that guarantee operator-only access, a signal that data localization is now mandatory rather than discretionary. As sovereign cloud capacity scales, hybrid isolation is becoming the default blueprint for banks, health systems, and public agencies. This dynamic drives recurring revenue in the remote browser market and cements vendor roadmaps centered on regional compliance.

DOM reconstruction dominated the Remote Browser Market with a 55.83% share in 2025, as it balances security with near-native UX. However, its reliance on signature updates creates vulnerabilities, leaving gaps for zero-day exploits to bypass detection and infiltrate systems. Pixel-pushing effectively eliminates this risk by providing a more secure approach. This method comes with significant trade-offs, including increased bandwidth consumption and latency exceeding 200 milliseconds, particularly in complex applications.

Network vector rendering grew at an 18.91% CAGR by instructing endpoints on how to render content instead of shipping full frames, halving server compute load and slashing latency. Zscaler's SquareX integration and Palo Alto Networks' browser-native engine illustrate how vendors are embedding protection within the runtime rather than in a distant data plane. Financial trading desks and radiology labs, both intolerant of delay, are early adopters. Over time, these advantages are expected to erode DOM reconstruction's lead and redistribute revenue inside the remote browser market.

Geography Analysis

North America accounted for 45.34% of the Remote Browser Market size in 2025, driven by U.S. federal zero-trust mandates and rapid SASE adoption among Wall Street banks. Continued funding in FY 2026 budgets, plus Canada's GDPR-style breach rules, sustain enterprise demand, though growth moderates as saturation nears in tier-one enterprises. The region's dense edge grids hold average latency below 20 milliseconds, giving cloud deployments a performance edge. Competition is fierce, with Zscaler, Palo Alto Networks, and Cloudflare racing to compress session start times while niche players such as Authentic8 pitch hardened environments for defense contractors.

Asia-Pacific is projected to expand at 18.28% through 2031, the highest regional CAGR, spurred by localization laws in China, India, and Vietnam that push multinationals toward in-country rendering nodes. Akamai logged more than 80 billion web app attacks in Asia during 2024, including 11 billion targeting APIs, spotlighting the fragility of the perimeter. Japan and South Korea benefit from EU adequacy, yet domestic buyers still prefer hybrid modes to assuage customer data-sovereignty expectations. Australia's critical infrastructure amendments and Singapore's fintech push round out a region where regulatory heterogeneity demands multi-region deployments, thereby elevating the total addressable market for the remote browser market.

Europe rides a compliance wave triggered by NIS2, the Data Act, and the forthcoming European Health Data Space Regulation. France's SecNumCloud rule effectively bars non-sovereign U.S. vendors unless they erect EU-only administrative domains. AWS answered with a EUR 7.8 billion (USD 8.8 billion) sovereign program, while Microsoft pledged in-country Copilot processing for 15 nations. Germany's BSI added location transparency to C5 audits, driving banks toward hybrid setups that split trusted SaaS from sensitive workloads. South America, the Middle East, and Africa trail but show pockets of acceleration, Brazilian banking regulations, Saudi Vision 2030, and South African finance pilots illustrating how regional statutes continually enlarge the remote browser market.

- Forcepoint LLC

- Netskope, Inc.

- Menlo Security, Inc.

- Broadcom Inc.

- Cisco Systems, Inc.

- Cloudflare, Inc.

- Zscaler, Inc.

- Authentic8, Inc.

- Citrix Systems, Inc.

- Ericom Software Ltd.

- McAfee, LLC

- Cyberinc Corporation

- HP Inc.

- Kasm Technologies Inc.

- Perimeter 81 Ltd.

- Light Point Security, LLC

- Proofpoint, Inc.

- Fortinet, Inc.

- Palo Alto Networks, Inc.

- Check Point Software Technologies Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Zero-Trust Security Frameworks

- 4.2.2 Mandatory Browser Isolation for Critical Infrastructure (Post-2025 NIST and EU-NIS2)

- 4.2.3 Surge in Sophisticated Web-Based Phishing-as-a-Service Kits

- 4.2.4 Work-from-Anywhere Permanence Boosting SaaS Attack Surface

- 4.2.5 Browser-Native Ransomware Payloads Targeting Edge and Chrome

- 4.2.6 Integration of RBI into SASE Suites by Hyperscalers

- 4.3 Market Restraints

- 4.3.1 Latency and UX Issues in High-Fidelity Web Apps

- 4.3.2 Budget Compression in SME Cybersecurity Stacks

- 4.3.3 Competing Client-Side Hardening (Embedded Safe-Browsing APIs)

- 4.3.4 Fragmented Regional Data-Residency Mandates Complicating Cloud RBI Rollout

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-Based

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Technology Type

- 5.2.1 DOM Reconstruction

- 5.2.2 Pixel Pushing

- 5.2.3 Network Vector Rendering

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-User Industry

- 5.4.1 BFSI

- 5.4.2 IT and Telecommunications

- 5.4.3 Government and Defense

- 5.4.4 Healthcare

- 5.4.5 Education

- 5.4.6 Other End-User Industry

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Forcepoint LLC

- 6.4.2 Netskope, Inc.

- 6.4.3 Menlo Security, Inc.

- 6.4.4 Broadcom Inc.

- 6.4.5 Cisco Systems, Inc.

- 6.4.6 Cloudflare, Inc.

- 6.4.7 Zscaler, Inc.

- 6.4.8 Authentic8, Inc.

- 6.4.9 Citrix Systems, Inc.

- 6.4.10 Ericom Software Ltd.

- 6.4.11 McAfee, LLC

- 6.4.12 Cyberinc Corporation

- 6.4.13 HP Inc.

- 6.4.14 Kasm Technologies Inc.

- 6.4.15 Perimeter 81 Ltd.

- 6.4.16 Light Point Security, LLC

- 6.4.17 Proofpoint, Inc.

- 6.4.18 Fortinet, Inc.

- 6.4.19 Palo Alto Networks, Inc.

- 6.4.20 Check Point Software Technologies Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment