|

시장보고서

상품코드

2062419

수중 통신 시스템 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Underwater Communication System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

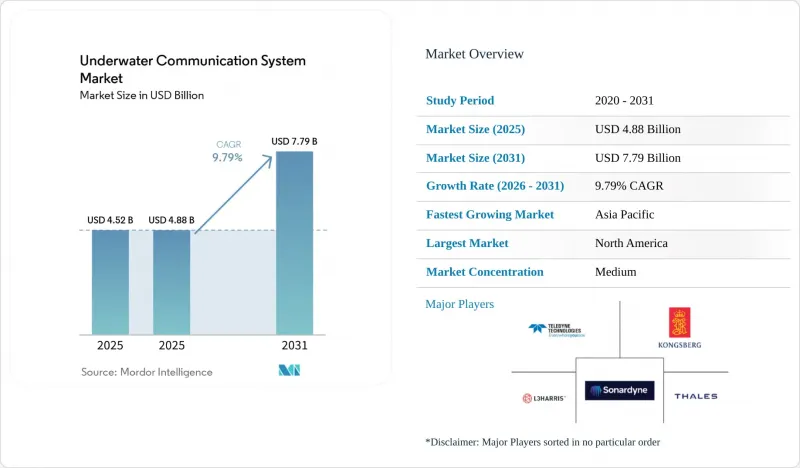

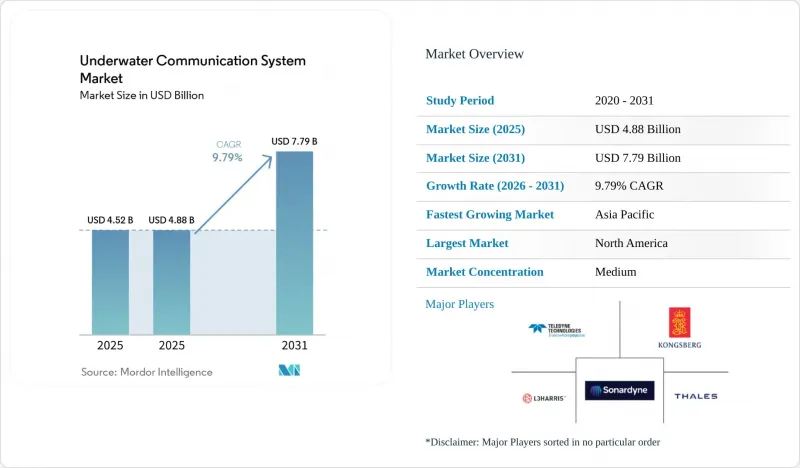

Mordor Intelligence에 의하면, 수중 통신 시스템 시장 규모는 2025년에 45억 2,000만 달러로 평가되었고, 2026년 48억 8,000만 달러로 추정되고, 2031년까지 77억 9,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 9.79%를 나타낼 전망입니다.

본 보고서는 기술별(음향 통신, 청록색 레이저, 전자기 무선 주파수, 하이브리드), 구성 요소별(하드웨어, 소프트웨어 및 서비스), 플랫폼별(잠수함 및 무인 수중정(UUV), 수상 함정 등), 용도별(국방 및 보안 등), 그리고 지역별로 분류되어 있습니다. 시장 전망은 달러(USD) 기준으로 제시되어 있습니다.

세계의 수중 통신 시스템 시장 동향 및 분석

자율형 수중 차량의 급속한 보급

해군은 유인 잠수함보다 순찰 시간당 비용을 절감하면서도 수중에서 지속적인 존재감을 유지할 수 있기 때문에 초대형 및 중형급 자율형 잠수정의 도입이 증가하고 있습니다. 미국 국방혁신단(DIU)은 2026년 3월, 오픈 아키텍처를 통한 페이로드 통합을 실증하기 위해 Dive-XL을 선정했습니다. 이 모델은 선박의 재인증 절차 없이 통신 모듈을 교체할 수 있는 모델입니다. 호주의 '고스트 샤크(Ghost Shark)' 프로젝트는 2026년 1월에 첫 선체를 인도할 예정이며, 타사 제작의 음향 또는 광트랜시버를 지원하는 모듈러 베이를 채택함으로써 공급업체의 인증 기간을 단축하고 있습니다. 일본 방위장비청은 청록색 레이저와 음향 백업 채널을 결합하여 수심 50미터에서 초당 1메가비트의 통신 링크를 구현함으로써, 신형 차량 설계에서 대역폭의 중요성을 부각시켰습니다.

하이퍼스케일러들의 해저 데이터센터 시범 사업이 가속화되고 있습니다.

마이크로소프트의 '프로젝트 나틱'은 수중 데이터 볼트의 하드웨어 고장률이 낮다는 점을 입증했으나, 이후 계약은 아직 체결되지 않았으며, 유지보수 비용 측면에서는 여전히 육상 에지 노드가 유리함을 시사하고 있습니다. 대신, 각 하이퍼스케일러 기업들은 해저 케이블에 대한 분산형 음향 감지 기술에 자금을 지원하여 기계적 스트레스의 발생을 실시간으로 감지하고 있습니다. 요코가와 전기는 2024년 12월, 해상 풍력 발전용 송전 케이블을 위한 1만 종의 센싱 플랫폼을 출시하며, 통신 수요가 컴퓨팅 오프로드가 아닌 구조 건전성 모니터링으로 전환되고 있음을 밝혔습니다.

탁한 수역에서 음향 채널의 심각한 대역폭 제한

다중 경로 간섭, 주변 선박 소음 및 퇴적물에 의한 산란으로 인해, 얕은 연안 지역에서는 음향 데이터 전송 속도가 불과 수 킬로비트/초 수준으로 크게 저하되어, 효율적인 데이터 전송에 심각한 문제를 야기하고 있습니다. IEEE Access 저널의 연구에 따르면, 탁도 수준이 50 NTU를 초과하면 20kHz에서의 신호대잡음비가 15dB 저하되어, 실질적으로 처리량이 절반으로 줄어들며 통신 신뢰성에 영향을 미치는 것으로 밝혀졌습니다. 이러한 문제를 완화하기 위해 사업자들은 업링크 전에 데이터를 압축하는 엣지 컴퓨팅을 도입하고 있지만, 이로 인해 노드의 하드웨어 비용이 5만-10만 달러 증가합니다. 그러나 이러한 접근 방식은 배터리 수명을 단축시키기 때문에 이러한 환경에서의 운영 효율성을 더욱 복잡하게 만들고 있습니다.

부문별 분석

2025년, 음향 링크는 10km 이상의 거리에서도 작동하고 위치 정밀도 요구 사항도 그리 엄격하지 않아, 수중 통신 시스템 시장 매출의 62.58%를 차지했습니다. 실험실에서 초당 170기가비트의 편파 분할 다중화가 입증됨에 따라 청록색 레이저 시장은 2031년까지 연평균 성장률(CAGR) 8.45%로 성장하고 있으나, 550나노미터를 초과하는 파장에서는 해수에 의한 흡수가 발생하기 때문에 운용 범위는 약 100미터로 제한됩니다. 전자기 시스템은 30kHz 이상의 신호가 해수 때문에 수 미터 이내에서 감쇠되어 버리기 때문에 여전히 틈새 시장에 머물러 있습니다. 음향 백본과 광 버스트 채널을 결합한 하이브리드 설계는 근접 시 고해상도 영상 전송이 필요한 임무에 대응합니다.

소프트웨어 정의 음향 모뎀은 현재 현장에서 프로그램을 변경할 수 있게 되어, 주변 소음이 급격히 증가할 경우 운영자가 반송파 주파수를 재조정할 수 있게 되었습니다. 이를 통해 가동 중단 시간이 단축되고 자산의 수명이 연장됩니다. EvoLogics사는 2024년에 JANUS 오픈 프로토콜을 도입하여 NATO 군 전체에서 함대 간 상호 운용성을 보장했습니다. 30킬로헤르츠 미만의 주파수 대역에 대한 규제의 불확실성은 여전히 지속되고 있으며, 각 관할 구역에서 음향 경로와 광 경로 모두를 인증해야 하는 부담이 장비 제조업체에 부과되고 있습니다. 한편, 갈륨 질화물 레이저 다이오드의 가격은 하락 추세를 보이고 있어, 양식용 부표나 검사용 드론에 적합한 1만 달러 미만의 광통신 단말기 개발이 기대되고 있습니다.

2025년 매출액 중 하드웨어가 57.53%를 차지했습니다. 이는 트랜스듀서, 모뎀 및 수중용 커넥터의 가격이 여전히 높은 수준을 유지하고 있기 때문입니다. 그러나 클라우드 호스팅 방식의 함대 관리 및 도크 입항 비용을 절감하는 웨이브 핫 패칭의 확산에 힘입어, 소프트웨어 및 서비스 부문은 연평균 성장률(CAGR) 8.39%를 기록하며 하드웨어 부문을 앞지르는 성장이 예상됩니다. L3Harris는 2026년 2월, 무선 방식의 암호 키 로테이션을 지원하는 26세트의 장비를 공급하는 계약을 수주했습니다. 이는 소프트웨어 제어가 현재 조달 과정에서 필수적인 요소가 되었음을 보여줍니다.

트랜스듀서의 혁신은 사용 가능한 대역폭을 확대하는 피에조 복합 스택에 초점을 맞추었습니다. 이를 통해 단일 유닛으로 여러 주파수 대역을 커버할 수 있게 되어, 부품 명세서(BOM) 비용을 절감할 수 있습니다. 케이블의 무결성과 커넥터의 신뢰성은 내압 하우징 및 부식 방지 요건으로 인해 여전히 노드 하드웨어 비용의 최대 20%를 차지하고 있습니다. 소프트웨어 측면에서는 머신러닝 기반 진단 기능이 채널 품질을 실시간으로 평가하여 출력과 주파수 조정을 권장합니다. 이를 통해 과거 현장 데이터를 예측 유지보수 알림으로 전환하여 수명 주기 비용을 절감합니다. 해상 설치 업체들이 노드의 시운전, 교육, 수년에 걸친 지원을 구독 계약에 포함시킴으로써 서비스 수익이 증가하고 있습니다.

지역별 분석

북미는 해저 통신의 현대화, 대서양 연안의 해상 풍력 발전 용량 확대, 그리고 북극권 감시 이니셔티브 덕분에 2025년 매출의 31.76%를 차지했습니다. Dive-XL 프로그램 계약 및 L3Harris의 선박용 세트 수주로 인해, 2033년까지 안정적인 수주 잔고가 확보되었습니다. 한편, 캐나다의 북극권 센서 그리드는 항로 확장에 따라 북서항로를 보호하고 있습니다. 멕시코의 멕시코만 심해 구역에서는 다중 공급업체의 센서 스트림을 처리하는 해저 통신 노드가 필요하며, 이것이 해당 지역 수요를 견인하고 있습니다.

아시아태평양은 2026-2031년 연평균 성장률(CAGR) 8.73%로 성장할 것으로 전망됩니다. 호주의 17억 호주 달러(11억 2,000만 달러) 규모의 '고스트 샤크(Ghost Shark)' 투자가 공급업체의 로드맵을 뒷받침하고 있으며, 일본의 하이브리드 광·음향 모뎀 프로토타입은 더 높은 대역폭을 향한 전략적 추진을 보여주고 있습니다. 중국의 'Transparent Ocean' 네트워크는 음향 감시망을 확대하고 있는 반면, 한국과 인도는 소프트웨어 정의 모뎀을 탑재한 신형 잠수함 건조에 자금을 투입하고 있습니다. 대만, 베트남, 인도에서의 해상 풍력 발전 사업 확대로 인해 수백 개의 수출용 케이블 모니터링 노드가 추가될 예정이지만, 이중용도 기술에 대한 수출 규제와 인증 제도의 차이가 시장 진입의 장벽으로 작용하고 있습니다.

유럽에서는 닻 끌림이나 어구 충돌을 감지하기 위해 분산형 음향 센싱 기술에 의존하는 북해 및 발트해 지역의 자산에서 꾸준한 교체 수요가 나타나고 있습니다. 나토(NATO)의 '발틱 센트리' 작전은 인프라의 취약점을 부각시키고, 도청이 어려운 음향 파형의 도입을 촉진하고 있습니다. 중동에서는 음향 대역폭의 제약을 피하기 위해 페르시아만 플랫폼에 광섬유 테더가 도입되고 있습니다. 한편, 남미 브라질의 프레솔트층 지역에서는 수 메가비트의 처리 용량을 갖춘 광 링크가 요구되고 있습니다. 칠레의 연어 양식업자와 아르헨티나의 초기 단계에 있는 해상 풍력 발전 연구는 해당 지역의 활용 범위를 넓히고, 석유 및 가스에 대한 의존도를 낮추고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the underwater communication system market size was valued at USD 4.52 billion in 2025 and is estimated to grow from USD 4.88 billion in 2026 to reach USD 7.79 billion by 2031, at a CAGR of 9.79% during the forecast period (2026-2031).

This report is Segmented by Technology (Acoustic Communication, Optical Blue-Green Laser, Electromagnetic Radio Frequency, and Hybrid), Component (Hardware, and Software and Services), Platform (Submarines and Unmanned Underwater Vehicles (UUVs), Surface Vessels, and More), Application (Defense and Security, and More), and Geography. The Market Forecasts are Provided in Terms of Value USD.

Global Underwater Communication System Market Trends and Insights

Rapid Adoption of Autonomous Underwater Vehicles

Procurement of extra-large and medium-class autonomous vehicles is rising because navies can maintain a persistent subsea presence at lower cost per patrol hour than crewed submarines. The United States Defense Innovation Unit selected Dive-XL in March 2026 to demonstrate open-architecture payload integration, a model that allows communication modules to be swapped without vessel recertification. Australia's Ghost Shark project delivered its first hull in January 2026 and uses modular bays that accept third-party acoustic or optical transceivers, trimming qualification time for vendors. Japan's Acquisition, Technology and Logistics Agency achieved a 1 megabit-per-second link at 50 meters using a blue-green laser paired with an acoustic fallback channel, underscoring bandwidth priorities in new vehicle designs.

Accelerated Subsea Data-Center Pilots by Hyperscalers

Microsoft's Project Natick proved submerged data vaults had lower hardware failure rates, yet follow-on contracts remain absent, implying that maintenance economics still favor land-based edge nodes. Hyperscalers instead fund distributed acoustic sensing on subsea cables to detect mechanical stress events in real time. Yokogawa Electric launched a 10 000-point sensing platform for offshore wind export cables in December 2024, revealing that communication demand is shifting toward structural health monitoring rather than compute off-loading.

Severe Bandwidth Limits of Acoustic Channels in Turbid Waters

Multipath interference, ambient shipping noise, and sediment scatter significantly reduce acoustic data rates to only a few kilobits per second in shallow coastal zones, creating substantial challenges for efficient data transmission. An IEEE Access study revealed that turbidity levels exceeding 50 NTU reduce signal-to-noise ratios by 15 decibels at 20 kilohertz, effectively halving throughput and impacting communication reliability. To mitigate these issues, operators embed edge compute to compress data before uplink, which adds USD 50,000-100,000 in node hardware costs. However, this approach also shortens battery life, further complicating operational efficiency in such environments.

Other drivers and restraints analyzed in the detailed report include:

- Defense Modernization Programs Focused on Contested Seabed Zones

- Growth in Offshore Renewable Energy Installations Needing Real-Time Monitoring

- High CAPEX for Hybrid Optical-Acoustic Networks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, acoustic links held 62.58% of underwater communication system market revenue because they operate over 10 kilometers with modest alignment requirements. Optical blue-green lasers are advancing at an 8.45% CAGR through 2031 as laboratories demonstrate 170 gigabit-per-second polarization-division multiplexing, yet seawater absorption beyond 550 nanometers confines operational range to roughly 100 meters. Electromagnetic systems remain niche since seawater attenuates signals above 30 kilohertz within meters. Hybrid designs pairing an acoustic backbone with an optical burst channel satisfy missions that need high-definition video off-load during close approaches.

Software-defined acoustic modems are now field-programmable, allowing operators to retune carrier frequencies when ambient noise spikes, which reduces downtime and extends asset life. EvoLogics embedded the JANUS open protocol in 2024 to guarantee fleet interoperability across NATO forces. Regulatory uncertainty around sub-30 kilohertz spectrum continues, placing the burden on equipment makers to certify both acoustic and optical paths for each jurisdiction. Meanwhile, gallium-nitride laser diodes are trending toward lower cost curves, promising sub-USD 10 000 optical endpoints suited to aquaculture pens and inspection drones.

Hardware captured 57.53% of 2025 revenue because transducers, modems, and subsea-rated connectors still command premium prices. However, the software and services segment is projected to outpace hardware with an 8.39% CAGR, fueled by cloud-hosted fleet management and by waveform hot-patching that saves dry-dock fees. L3Harris won a USD contract in February 2026 to supply 26 shipsets that support over-the-air encryption-key rotation, illustrating how software control is now a procurement must-have.

Transducer innovation focuses on piezo-composite stacks that widen the usable bandwidth envelope, permitting a single unit to cover multiple frequency bands and thereby trim bill of materials. Cable integrity and connector reliability still represent up to 20% of node hardware cost because of pressure housing and corrosion control. On the software side, machine-learning diagnostics assess channel quality in real time and recommend power or frequency adjustments, turning historical field data into predictive maintenance alerts that lower life-cycle cost. Services revenue is rising as offshore installers bundle node commissioning, training, and multi-year support into subscription contracts.

Geography Analysis

North America generated 31.76% of 2025 revenue thanks to submarine communication modernization, increasing offshore wind capacity along the Atlantic coast, and Arctic surveillance initiatives. The Dive-XL program contracts and L3Harris shipset awards provide a visible backlog through 2033, while Canada's Arctic sensor grid protects the Northwest Passage as shipping lanes expand. Mexico's deepwater Gulf of Mexico blocks require subsea communication nodes that handle multi-vendor sensor streams, reinforcing regional demand.

Asia-Pacific is forecast to grow at an 8.73% CAGR between 2026 and 2031. Australia's AUD 1.7 billion (USD 1.12 billion) Ghost Shark investment anchors supplier roadmaps, and Japan's hybrid optical-acoustic modem prototypes signal a strategic push toward higher bandwidth. China's Transparent Ocean network extends acoustic surveillance, while South Korea and India fund new submarine builds that integrate software-defined modems. Offshore wind rollouts in Taiwan, Vietnam, and India add hundreds of export-cable monitoring nodes, though export controls on dual-use technologies and diverging certification regimes create market entry hurdles.

Europe shows robust replacement demand across North Sea and Baltic assets that rely on distributed acoustic sensing to detect anchor drags and fishing-gear strikes. NATO's Baltic Sentry operation highlights infrastructure vulnerability and spurs procurement of low-intercept acoustic waveforms. The Middle East deploys fiber-optic tethers on Persian Gulf platforms to circumvent acoustic bandwidth ceilings, whereas South America's pre-salt provinces in Brazil demand optical links capable of multimegabit throughput. Chile's salmon growers and Argentina's early offshore wind studies broaden the regional application mix, lowering dependence on oil and gas alone.

- Teledyne Technologies Incorporated

- Kongsberg Gruppen ASA

- Sonardyne International Ltd.

- Ultra Electronics Maritime Systems Inc.

- L3Harris Technologies Inc.

- Thales Group

- SAAB AB

- EvoLogics GmbH

- Subnero Pte. Ltd.

- DSPComm Ltd.

- General Dynamics Mission Systems, Inc.

- Lockheed Martin Corporation

- Ocean Sonics Ltd.

- Hydroacoustics Inc.

- Nautel Ltd. (Nautel Sonar Systems)

- EdgeTech (a wholly-owned subsidiary of ORE Offshore)

- Wartsila ELAC Nautik GmbH

- Blueprint Subsea Ltd.

- JW Fishers Mfg Inc.

- CGG S.A. (Sercel)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid adoption of autonomous underwater vehicles (AUVs)

- 4.2.2 Accelerated subsea data-center pilots by hyperscalers

- 4.2.3 Defense modernization programs focused on contested seabed zones

- 4.2.4 Growth in offshore renewable energy installations needing real-time monitoring

- 4.2.5 Expansion of deep-sea mineral exploration licenses

- 4.2.6 Emergence of software-defined acoustic modems enabling dynamic spectrum use

- 4.3 Market Restraints

- 4.3.1 Severe bandwidth limits of acoustic channels in turbid waters

- 4.3.2 High CAPEX for hybrid optical-acoustic networks

- 4.3.3 Regulatory ambiguity around RF spectrum below 30 kHz

- 4.3.4 Cyber-security vulnerabilities in long-baseline positioning networks

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Acoustic Communication

- 5.1.2 Optical (Blue/Green Laser)

- 5.1.3 Electromagnetic/Radio Frequency

- 5.1.4 Hybrid

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.1.1 Modems

- 5.2.1.2 Transducers/Transceivers

- 5.2.1.3 Cables and Connectors

- 5.2.1.4 Sensors and Antennas

- 5.2.2 Software and Services

- 5.2.1 Hardware

- 5.3 By Platform

- 5.3.1 Submarines and Unmanned Underwater Vehicles (UUVs)

- 5.3.2 Surface Vessels

- 5.3.3 Offshore Fixed Platforms

- 5.3.4 Offshore Floating Platforms

- 5.3.5 Scientific and Monitoring Buoys

- 5.4 By Application

- 5.4.1 Defense and Security

- 5.4.2 Oil and Gas Exploration and Production

- 5.4.3 Environmental Monitoring and Oceanography

- 5.4.4 Scientific Research and Academia

- 5.4.5 Marine Construction and Aquaculture

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Teledyne Technologies Incorporated

- 6.4.2 Kongsberg Gruppen ASA

- 6.4.3 Sonardyne International Ltd.

- 6.4.4 Ultra Electronics Maritime Systems Inc.

- 6.4.5 L3Harris Technologies Inc.

- 6.4.6 Thales Group

- 6.4.7 SAAB AB

- 6.4.8 EvoLogics GmbH

- 6.4.9 Subnero Pte. Ltd.

- 6.4.10 DSPComm Ltd.

- 6.4.11 General Dynamics Mission Systems, Inc.

- 6.4.12 Lockheed Martin Corporation

- 6.4.13 Ocean Sonics Ltd.

- 6.4.14 Hydroacoustics Inc.

- 6.4.15 Nautel Ltd. (Nautel Sonar Systems)

- 6.4.16 EdgeTech (a wholly-owned subsidiary of ORE Offshore)

- 6.4.17 Wartsila ELAC Nautik GmbH

- 6.4.18 Blueprint Subsea Ltd.

- 6.4.19 JW Fishers Mfg Inc.

- 6.4.20 CGG S.A. (Sercel)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment