|

시장보고서

상품코드

2062421

휴대용 공기청정기 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Portable Air Purifier - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

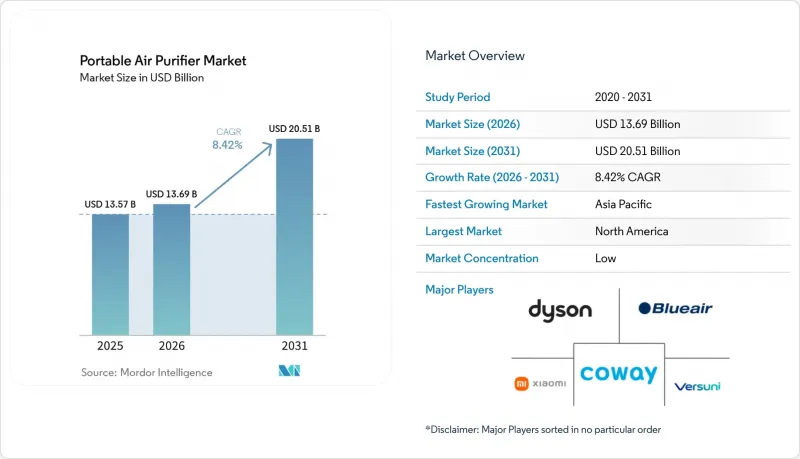

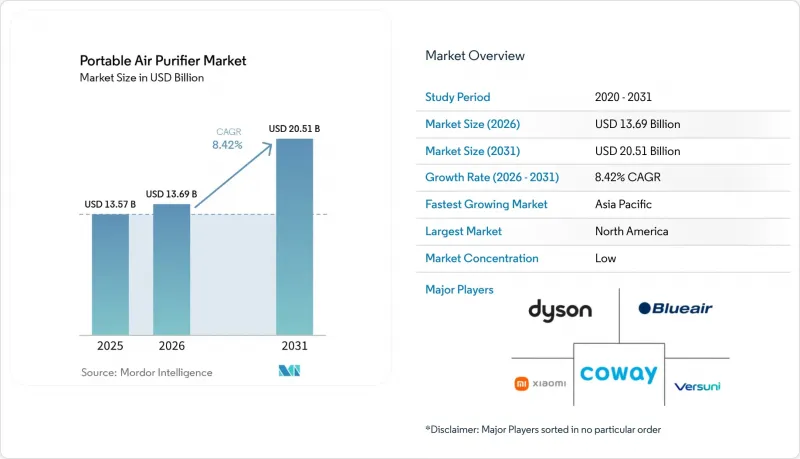

Mordor Intelligence에 의하면, 휴대용 공기청정기 시장 규모는 2025년 135억 7,000만 달러로 평가되었고, 2026년 136억 9,000만 달러로 추정되고, 2031년까지 205억 1,000만 달러로 확대될 전망이며, 2026-2031년 CAGR 8.42%를 나타낼 것으로 예측됩니다.

본 보고서는 기술별(HEPA, 활성탄, 이온식 등), 연결성별(비스마트, 스마트/IoT 지원), 기능별(단일 기능, 다기능), 용도별(개인용 및 책상용, 차량용, 실내용, 여행용 및 웨어러블), 판매 채널별(B2C 및 소매, B2B 및 직접 판매), 지역별(북미, 남미, 아시아태평양, 유럽, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준입니다.

세계의 휴대용 공기청정기 시장 동향 및 인사이트

HEPA 적용 및 성능 검증이 일반 소비자의 신뢰와 재구매를 촉진

구매자들이 검증된 CADR(청정 풍량) 및 필터의 동등성을 요구함에 따라, 표준화된 성능에 대한 인식은 틈새 시장의 차별화 요소에서 구매의 핵심 요건으로 전환되었습니다. 2025년 11월에 시작된 AHAM의 교체용 필터 검증 프로그램은 타사 필터의 품질 격차를 해소하고, 비정품 교체용 필터가 시간이 지남에 따라 기기의 성능을 저하시킬 위험을 줄여줍니다. 캘리포니아주의 0.050 ppm 배출 상한선에 기반한 오존 안전 라벨의 병행 도입은 가정, 학교, 사무실에서 저배출과 안정적인 성능을 우선시하는 기계식 또는 하이브리드 시스템으로의 전환을 촉진하고 있습니다. 이러한 프레임워크를 통해 연간 필터 예산이나 다년간의 기기 사용을 계획하는 가정 및 기관에게 휴대용 공기청정기 시장 전망이 더욱 명확해집니다. 검증을 통해 불확실성이 줄어들고 기대값이 일치함에 따라, 각 브랜드는 순정 필터의 재구매율 향상과 연계형 생태계 내 고객 유지율의 안정화라는 혜택을 누리게 됩니다. 이러한 동향은 신뢰, 규정 준수, 그리고 투명한 유지보수가 휴대용 공기청정기 시장의 지속 가능한 성장을 견인한다는 ‘프리미엄화’ 전략을 뒷받침하고 있습니다.

산불 연기에 대한 대비로 인해 가정, 학교, 중소기업에서 휴대용 HEPA 제품의 보급이 가속화되고 있습니다.

현재 북미의 지침에서는 산불 발생 시 건물을 위한 연기 대책 매뉴얼의 일환으로, 공조 설비(HVAC) 대책 외에도 휴대용 HEPA 장치의 중요성이 강조되고 있습니다. 화재 발생 시 로스앤젤레스의 주택을 대상으로 실시한 실증 조사 결과, HEPA 공기청정기가 비-HEPA 대조군에 비해 실내 PM2.5 농도를 감소시킨 것으로 밝혀졌으며, 실제 환경에서 실용적인 완화 수단으로서의 역할이 부각되었습니다. 학군 및 지자체 시설에서는 장비와 표준 운영 절차를 결합한 클린룸 전략을 수립하고 있으며, 이는 사후적인 긴급 구매가 아닌, 착실하고 체계적인 조달을 뒷받침하고 있습니다. 이러한 프로그램들은 교실에서 지역 대피소에 이르기까지, 휴대용 유닛이 체계적인 대응 계획의 일부가 되는 재현 가능한 도입 모델을 만들어내고 있습니다. 산불 시즌은 계속해서 반복되는 위험 요인으로 남아 있기 때문에 휴대용 공기청정기 시장은 깨끗한 공기를 단순한 선택적 부가품이 아닌 필수적인 인프라로 간주하는 예산에 힘입어 성장하고 있습니다.

높은 총소유비용이 가격에 민감한 시장에서 보급을 제한하고 있습니다.

소유 비용에는 본체, 필터 교체, 전기료가 포함되지만, 가정에서 여러 방을 커버해야 하는 경우 이러한 비용은 증가합니다. 가처분 소득이 제한적인 경우, 사용자는 종종 한 방을 우선시하고 가동 시간을 제한하기 때문에 정격 성능에 비해 실제로 공급되는 청정 공기의 양이 감소합니다. 기관들도 마찬가지로 이러한 고려 사항에 직면해 있으며, 계절마다 반복적으로 설치하는 클린룸 키트를 설계할 때 필터의 재고 관리, 물류, 교체 주기를 신중하게 검토하고 있습니다. 각 제조업체는 세척 가능한 프리필터 도입, 교체용 필터 정기 구매 할인, 일상 사용 시 CADR 성능을 저하시키지 않으면서 전력 소비를 줄여주는 고효율 모터 채택 등을 통해 비용 측면의 우려를 해소하고 있습니다. 이러한 노력은 어느 정도 효과를 거두고 있지만, 총 소유 비용은 여전히 신흥 시장에서의 보급 확대나, 제한된 예산 내에서 여러 방을 커버하려는 가정에게 큰 장벽이 되고 있습니다. 비용의 투명성과 검증된 필터 성능이 표준화됨에 따라, 고객들은 휴대용 공기청정기 시장의 총 소유 비용을 보다 적절하게 계획할 수 있게 될 것입니다.

부문별 분석

2025년 휴대용 공기청정기 시장에서 HEPA 필터가 48.92%의 점유율을 차지하며 1위를 차지했습니다. 또한, 미세먼지 및 가스 모두를 동시에 제어하고자 하는 수요가 증가함에 따라, 활성탄 필터 시장은 2031년까지 연평균 성장률(CAGR) 8.64%를 나타낼 것으로 전망됩니다. 규격 및 표시 제도에 따라 HEPA 필터는 여전히 미세 입자 제거를 위한 표준적인 선택지로 자리 잡고 있지만, 캘리포니아주 대기자원국(CARB)의 오존 안전 기준에 따라 주거 및 상업 환경에서는 기계식 또는 하이브리드식 필터가 권장되고 있습니다. 도시 지역의 주거 공간에서는 교통이나 산불 연기로 인한 미세먼지 노출에 직면하고, 실내에서는 청소나 건축자재에서 VOC가 방출되기 때문에 복합 미디어 스택은 연중 사용에 적합한 균형 잡힌 솔루션을 제공합니다. 휴대용 공기청정기 시장의 구매자들은 성능, 필터 수명, 소음 저감을 주요 판단 기준으로 삼고 있으며, 정기적인 필터 교체 비용이 허용 범위 내라면 HEPA+활성탄 구성으로의 업그레이드를 선호합니다. 제품 측면에서 제조업체는 모듈식 스택을 조립하고 있으며, 사용자는 지역 상황이나 계절의 변화에 따라 연기, 냄새 또는 알레르기 유발 물질에 최적화된 제품을 선택할 수 있습니다. 이러한 선택지는 시스템의 성능을 장기간 유지하고 실제 사용 시 결과의 편차를 줄여주는 검증된 교체용 필터 프로그램과 잘 부합합니다.

활성탄 수요 증가는 산불 연기로 인한 계절적 악취와 VOC(휘발성 유기화합물)에 대한 우려가 커지면서 뒷받침되고 있습니다. 이러한 문제들은 기계적 여과만으로는 거실이나 교실에서 충분히 해결할 수 없는 문제들입니다. 하이브리드 설계와 고성능 활성탄은 VOC 포집 범위를 넓혀주며, 특정 용도에서 포름알데히드와 암모니아를 저감합니다. 이에 따라, 실내 화학 물질에 대한 우려가 있는 상황에서는 다소 비싼 가격 책정도 정당화됩니다. 기관이 클린룸 키트를 구축할 때, 필터의 표준화와 안전 표시는 위험을 줄이고 조달 절차를 간소화하며, 수개월에 걸친 도입 과정의 예산 예측 가능성을 높여줍니다. 예측 기간 동안, 특히 오존 발생형 제품의 사용이 권장되지 않는 지역에서 미세먼지 및 가스 포집 기능을 통합한 균형 잡힌 구성의 제품이 휴대용 공기청정기 시장에서 더 큰 점유율을 차지할 것으로 예측됩니다. 검증 및 안전성 체계가 성숙해짐에 따라, 휴대용 공기청정기 업계는 성능, 필터 교체 주기, 일상 사용 시의 규정 준수 사항을 명확히 함으로써 제품 설계를 장기적인 소유 가치와 조화시키고 있습니다.

2025년에는 비스마트 수동식 또는 아날로그식 기기가 78.52%의 점유율을 유지한 반면, 앱 대시보드, 음성 비서, 필터 교체 예측 알림 기능을 갖춘 스마트 또는 IoT 지원 공기청정기는 연평균 성장률(CAGR) 10.09%로 성장할 것으로 전망됩니다. 사용자들은 PM 농도와 송풍 속도를 연동하여 공기 질을 명확하게 시각화한 점에 긍정적인 반응을 보이고 있으며, 이를 통해 불확실성이 줄어들어 연기가 유입될 때나 교통 혼잡 시간대에 사용 준수율이 향상되고 있습니다. 상호 운용이 가능한 표준을 지원함에 따라 플랫폼 통합이 진행되고 있으며, 이로 인해 락인(lock-in)에 대한 우려가 완화되고, 단일 앱을 통한 제어가 가능해지면서 브랜드를 넘나드는 멀티 디바이스 루틴이 확대되고 있습니다. 업무용 장비의 경우, 사용 현황 및 일정 관리 기능을 활용하여 방이 비어 있을 때의 전력 소비를 줄이고 있습니다. 이를 통해 이용 빈도가 높은 시설에서 에너지 소비를 줄이고 필터의 수명을 연장할 수 있습니다. 휴대용 공기청정기 시장에서도 연결성이 향상됨에 따라 유지보수 주기가 ‘일정 기반’에서 ‘상태 기반’으로 전환되어, 교체 시기가 최적화되고 예기치 못한 성능 저하가 줄어드는 이점을 누리고 있습니다. 가격대가 낮아지고 클라우드 비용이 전체 제품 포트폴리오에 분산됨에 따라, 더 많은 중급 제품에 핵심 스마트 기능이 탑재되어 브랜드 충성도가 강화될 것으로 기대됩니다.

고도의 연결성은 교실이나 진료소 전체에서 기기를 그룹화하고, 위치 정보를 태그하며, 원격으로 상태를 확인할 수 있게 함으로써 기관의 조달 업무도 지원합니다. 이러한 도구는 관리자가 필터 재고를 배정하거나, 실의 가동 주기를 계획하거나, 연기나 꽃가루가 많은 날에 클린룸의 표준 작업 절차 준수 여부를 확인하는 데 도움이 됩니다. 엣지 분석은 중요한 상태 기능을 유지하면서 클라우드로의 데이터 전송을 제한함으로써, 개인정보 보호가 필요한 환경을 지원할 수 있으며, 외부 트래픽을 제한하는 학교나 의료 기관에 적합합니다. 앞으로 휴대용 공기청정기 시장에서는 기기들이 예측 가능한 필터 교체 및 유지보수 일정을 갖춘 관리형 모델로 전환됨에 따라, 하드웨어와 소프트웨어의 가치 중첩이 점점 더 커질 것입니다. 이러한 움직임에 따라, 연결 기능이 없는 기기들 간의 인식되는 차이가 줄어들고, 투명성이 높은 성능 이력과 일관된 앱 지원을 갖춘 생태계의 매력이 더욱 높아집니다.

지역별 분석

북미는 2025년 매출의 44.12%를 차지했으며, 산불 대비 프로그램, 성숙한 공조 설비(HVAC) 운영 관행, 그리고 소비자 신뢰를 형성하는 안전 체계에 힘입고 있습니다. 해당 기관에서는 연기가 유입될 때 보다 깨끗한 공간을 확보하기 위해 휴대용 HEPA 장치를 사용하고 있으며, 이를 통해 가정용을 넘어선 수요가 정착되어 수년에 걸친 도입 계획이 뒷받침되고 있습니다. 캘리포니아주 대기자원국(CARB)의 오존 안전 라벨은 캘리포니아주에서 판매되는 기기에 대해 명확한 준수 기준을 설정하고 있으며, 이는 전미의 판매 채널에서 제품 라인업 결정에 영향을 미치고 있습니다. 이러한 요인들은 휴대용 공기청정기 시장의 안정적인 기반을 마련하는 동시에, 일시적인 사건으로 인한 변동을 억제합니다. 조달의 계절적 변동성을 예측하기가 점점 더 쉬워짐에 따라, 소유 비용의 투명성과 검증된 필터가 제품의 장기 보유와 보다 일관된 애프터마켓 수요를 뒷받침하고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 8.79%로 가장 빠른 성장세를 보일 것으로 전망되며, 주요 대도시권에서 PM2.5 문제가 지속되고 있는 점이 실내 공기청정기의 기초적인 수요를 뒷받침하고 있습니다. IQAir의 2025년 보고서에는 WHO 지침에 대한 광범위한 미준수 사항이 기록되어 있으며, 주요 도시의 일상생활에서 미세 입자 제거와 실내 커버 범위의 중요성이 재확인되었습니다. 가정 내 사용이 확대됨에 따라, 휴대용 공기청정기 시장에는 냉난방 조절이 제한되는 출퇴근이나 출장 시 수요를 충족시키는 개인용 및 여행용 기기가 추가되고 있습니다. 대학이나 진료소 등의 기관은 지역적인 스모그나 교통량이 많은 시기에 대응할 수 있도록, 배치, 가동 시간, 필터 교체 일정을 정한 표준 작업 절차(SOP)에 따라 장비 도입에 예산을 배정하고 있습니다. 시간이 지남에 따라 지역별 제품 구성은 HEPA 필터와 활성탄 필터의 조합, 검증된 교체용 필터 매체, 그리고 좁은 아파트에서 야간에 사용하기에 적합한 저소음 설계의 균형을 반영하게 되었습니다.

유럽에서는 성숙한 북유럽 및 서유럽 시장이 교체 주기와 프리미엄 혁신에 중점을 두는 반면, 남유럽 및 동유럽은 분진 발생 및 바이오매스 난방에 대응하는 낮은 기준선에서 시장을 확대하고 있어, 그 추세는 제각각입니다. 여과 성능 분류의 통일과 안전 의식의 고취로 인해, 국가별 기준이 서로 다르더라도 국경을 초월한 조달을 조정하기가 쉬워졌으며, 이로 인해 여러 EU 시장에 진출한 다국적 브랜드가 겪는 복잡성이 완화되고 있습니다. 중동의 구매자들은 분진 관리와 강력한 프리필터 기능을 우선시하고 있으며, 신속한 청소 주기를 지원하는 기능 세트는 일부 도시에서 나타나는 높은 배경 입자 농도에 대응하고 있습니다. 남미에서의 보급은 여전히 도시 지역에 집중되어 있으며, 지역의 지리적 조건이나 기상 패턴으로 인해 배출물이 정체되기 쉬워, 공공시설에서 이동식 클린룸 대책이 필요할 정도의 간헐적인 오염 급증을 초래하고 있습니다. 기관용 운영 매뉴얼이 널리 보급됨에 따라, 휴대용 공기청정기 시장에서는 지역별 도입 요구 사항과 시설 구성에 맞추어 제품 번들 및 교육 자료를 조정하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the portable air purifier market size is projected to expand from USD 13.57 billion in 2025 and USD 13.69 billion in 2026 to USD 20.51 billion by 2031, registering a CAGR of 8.42% between 2026 and 2031.

This report is Segmented by Technology (HEPA, Activated Carbon, Ionic, and More), Connectivity (Non-Smart, Smart/IoT-Enabled), Functionality (Single-Function, Multi-Function), Application (Personal/Desk, Car, Room, Travel/Wearable), Distribution Channel (B2C/Retail, B2B/Direct), and Geography (North America, South America, Asia-Pacific, Europe, Middle East and Africa). Market Forecasts in Value (USD).

Global Portable Air Purifier Market Trends and Insights

HEPA Adoption and Performance Verification Drive Mainstream Trust and Repeat Purchases

Recognition of standardized performance has moved from a niche differentiator to a core purchase requirement as buyers look for validated CADR and filter equivalency. AHAM's replacement-filter verification program, launched in November 2025, addresses quality gaps in third-party filters and reduces the risk that off-brand replacements undermine device performance over time. Parallel ozone-safety labeling under California's 0.050 ppm emission cap reinforces the shift toward mechanical or hybrid systems that prioritize low emissions and consistent results in homes, schools, and offices. This framework makes the portable air purifier market more predictable for households and institutions that plan for annual filter budgets and multi-year device use. As verification reduces uncertainty and aligns expectations, brands benefit from higher repeat-purchase rates for original filters and more stable retention in connected ecosystems. These developments support a premiumizing narrative in which trust, compliance, and transparent maintenance drive sustainable growth in the portable air purifier market.

Wildfire-Smoke Preparedness Accelerates Portable HEPA Uptake in Homes, Schools, and Small Businesses

Guidance in North America now emphasizes portable HEPA units alongside HVAC measures as part of smoke-readiness playbooks for buildings during wildfire events. Empirical research from Los Angeles homes during a fire event found that HEPA purifiers reduced indoor PM2.5 compared with non-HEPA controls, highlighting their role as practical mitigation tools in real-world conditions. School districts and municipal facilities are planning clean-room strategies that pair devices with standard operating procedures, which support steady institutional procurement rather than reactive emergency buys. These programs create repeatable deployment models, from classrooms to community shelters, where portable units are part of structured response plans. As wildfire seasons remain a recurring risk, the portable air purifier market is reinforced by budgets that treat clean air as essential infrastructure instead of a discretionary accessory.

High Total Cost of Ownership Limits Penetration in Price-Sensitive Markets

Ownership costs include the device, filter replacements, and electricity, and these expenses rise when a household needs multiple rooms covered. Where disposable incomes are constrained, users often prioritize a single room and limit runtime, which reduces the realized clean air delivery compared with rated performance. Institutions face similar considerations and weigh fleet filters, logistics, and replacement cycles when designing clean-room kits for recurring seasonal deployment. Manufacturers are addressing cost stress through washable pre-filters, subscription discounts for replacement media, and energy-efficient motors that cut ongoing draw without sacrificing CADR in day-to-day use. These actions help, yet total ownership outlays remain a key hurdle for broader penetration in emerging markets and for households balancing multi-room coverage with restrained budgets. As cost transparency and verified filter performance become standard, customers can better plan lifetime spend in the portable air purifier market.

Other drivers and restraints analyzed in the detailed report include:

- Asia-Pacific Urban PM2.5 Exposure Sustains Baseline Demand for Room Purifiers

- E-commerce and D2C Expand Access to Mid-Range and Premium Portables

- Noise, CADR, and Power Trade-offs Cap Usable Runtime in Bedrooms and Offices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

HEPA filtration led with 48.92% of the 2025 portable air purifier market share, and activated carbon media is projected to post an 8.64% CAGR through 2031 as buyers seek parallel control of particulates and gases. Standards and labeling help HEPA remain the default for fine particle removal, while CARB's ozone-safety rules favor mechanical or hybrid filtration in residential and commercial environments. As urban dwellings face particulate exposure from traffic and wildfire smoke, and indoor sources emit VOCs from cleaning and materials, combined media stacks create a balanced proposition for year-round use. Buyers in the portable air purifier market weigh performance, filter longevity, and noise control as core decision points, which supports upgrades to HEPA-plus-carbon configurations when recurring filter costs are manageable. On the product side, manufacturers assemble modular stacks that allow users to choose smoke, odor, or allergen-optimized variants aligned with local conditions and seasonal shifts. These choices match well with verified replacement-filter programs that preserve system performance over time and reduce variance in real-world outcomes.

Activated carbon's trajectory is amplified by wildfire smoke seasons that elevate odor and VOC concerns, which mechanical filtration alone does not address in living rooms and classrooms. Hybrid designs and advanced carbons extend VOC capture windows and mitigate formaldehyde or ammonia in select applications, which justifies a premium where indoor chemistry is a worry. As institutions build clean-room kits, filter standardization and safety labeling reduce risk, simplify procurement, and support predictable budgets for multi-month deployments. Over the forecast period, balanced stacks that integrate particulate and gas capture are expected to represent a larger share of the portable air purifier market, especially where guidance discourages ozone-producing options. As verification and safety frameworks mature, the portable air purifier industry aligns product design with long-run ownership value by clarifying performance, filter intervals, and compliance in everyday use.

Non-smart manual or analog devices retained 78.52% share in 2025, although smart or IoT-enabled purifiers are forecast to expand at a 10.09% CAGR with app dashboards, voice assistants, and predictive filter prompts. Users respond to clear air quality visualization that links PM levels with fan speed, which reduces uncertainty and improves compliance during smoke intrusions and peak traffic periods. Platform integration is improving with support for interoperable standards, which alleviates lock-in fears, enables single-app control, and expands multi-device routines across brands. Commercial fleets use occupancy and scheduling features to reduce power when rooms are empty, which cuts energy use and extends filter life in high-traffic sites. The portable air purifier market benefits as connectivity shifts maintenance from calendar-based to condition-based cycles, which supports better timing for replacements and fewer unexpected performance dips. As price points fall and cloud costs spread across product portfolios, more mid-range devices are expected to include core smart features that strengthen brand retention.

Advanced connectivity also supports institutional procurement by enabling device grouping, location tagging, and remote status checks across classrooms or clinics. These tools help administrators assign filter inventories, schedule room cycles, and verify compliance with clean-room standard operating procedures during smoke or high-pollen days. Edge analytics can support privacy-sensitive sites by limiting cloud data while keeping key status functions, which suits schools and medical offices that restrict external traffic. Over time, the portable air purifier market will see growing overlap between hardware and software value as fleets shift to managed models with predictable filter and service events. This dynamic compresses perceived differences among devices without connectivity and increases the appeal of ecosystems with transparent performance histories and consistent app support.

Geography Analysis

North America accounted for 44.12% of 2025 revenues, supported by wildfire preparedness programs, mature HVAC practices, and safety frameworks that shape consumer trust. Institutions use portable HEPA units to create cleaner rooms during smoke intrusions, which institutionalizes demand beyond households and supports multi-year fleet planning. CARB's ozone-safety labeling sets clear compliance criteria for devices sold in California, which influences assortment decisions across national channels. These factors anchor a steady baseline for the portable air purifier market while reducing variability driven by one-time events. As seasonality becomes more predictable in procurement, ownership cost transparency and verified filters support longer retention and more consistent aftermarket volumes.

Asia-Pacific is projected to record the fastest expansion at an 8.79% CAGR, with persistent PM2.5 challenges across major urban corridors that sustain baseline room purifier demand. IQAir's 2025 report documented widespread non-compliance with the WHO guideline, which reinforces the relevance of particulate removal and room coverage in daily life across key cities. As household use widens, the portable air purifier market adds personal and travel devices that bridge commuting and business travel needs where HVAC control is limited. Institutions such as universities and clinics allocate budgets to fleets that can be deployed during regional haze and high-traffic episodes, with SOPs guiding placement, runtime, and filter schedules. Over time, regional product mixes reflect a balance of HEPA-plus-carbon stacks, verified replacement media, and quiet designs that support overnight use in compact apartments.

Europe shows mixed patterns as mature Northern and Western markets tilt toward replacement cycles and premium innovations, while Southern and Eastern regions expand from lower baselines that react to dust events and biomass heating. Harmonized filtration classifications and safety awareness help align procurement across borders even when country-level standards differ, which reduces complexity for multinational brands serving several EU markets. Middle East buyers prioritize dust management and robust pre-filtration, and feature sets that support quick cleaning cycles align with higher background particulate loads in several cities. South America's adoption remains focused in urban centers where geography and weather patterns can trap emissions, which creates episodic spikes that trigger portable clean-room tactics in public buildings. As institutional playbooks spread, the portable air purifier market adapts product bundles and training materials to region-specific implementation needs and facility configurations.

- Dyson

- Philips (Versuni)

- Xiaomi

- Coway

- Blueair (Unilever)

- Sharp

- Honeywell (licensed)

- Levoit (Vesync)

- Winix

- IQAir

- LG Electronics

- Samsung

- Medify Air

- Guardian Technologies (GermGuardian)

- AirDoctor (Ideal Living)

- Airdog (IAQ Tech)

- Austin Air Systems

- Rabbit Air

- TruSens (ACCO Brands)

- Daikin

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 HEPA adoption and performance verification (HEPA/CADR) drive mainstream trust and repeat purchases

- 4.2.2 Wildfire-smoke preparedness accelerates portable HEPA uptake in homes, schools, and small businesses

- 4.2.3 Asia-Pacific urban PM2.5 exposure sustains baseline demand for room purifiers

- 4.2.4 E-commerce and D2C expand access to mid-range and premium portables

- 4.2.5 Institutional "clean-room kits" (HEPA + SOPs) become a recurring budget line in education and municipal response

- 4.2.6 Ozone-safety labeling and third-party verification shift tech mix to HEPA+carbon, raising ASPs and filter annuities

- 4.3 Market Restraints

- 4.3.1 High total cost of ownership (filters, energy, multi-room coverage) limits penetration in price-sensitive markets

- 4.3.2 Ozone/ionizer safety limits and scrutiny reduce demand for certain electronic technologies

- 4.3.3 Enforcement against non-certified online SKUs raises seller compliance costs and narrows assortment

- 4.3.4 Noise-CADR-power trade-offs cap usable runtime in bedrooms/offices

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Technology

- 5.1.1 HEPA Filtration

- 5.1.2 Activated Carbon

- 5.1.3 Ionic / Ionizers

- 5.1.4 UV-C Light Purifiers

- 5.1.5 Others

- 5.2 By Connectivity

- 5.2.1 Non-Smart (Manual/Analog)

- 5.2.2 Smart/IoT-Enabled (App and Voice Controlled)

- 5.3 By Functionality

- 5.3.1 Single-Function Air Purifiers

- 5.3.2 Multi-Function Units

- 5.4 By Application

- 5.4.1 Personal/Desk Purifiers

- 5.4.2 Car Air Purifiers

- 5.4.3 Room Air Purifiers

- 5.4.4 Travel or Wearable Purifiers

- 5.5 By Distribution Channel

- 5.5.1 B2C/Retail

- 5.5.1.1 Multi-brand Stores (big box retailers, department stores, electronics chain, home improvement centers)

- 5.5.1.2 Exclusive Brand Outlets

- 5.5.1.3 Online

- 5.5.1.4 Other Distribution Channels

- 5.5.2 B2B/Directly from the Manufacturers

- 5.5.1 B2C/Retail

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Peru

- 5.6.2.3 Chile

- 5.6.2.4 Argentina

- 5.6.2.5 Rest of South America

- 5.6.3 Asia-Pacific

- 5.6.3.1 India

- 5.6.3.2 China

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.6.3.7 Rest of Asia-Pacific

- 5.6.4 Europe

- 5.6.4.1 United Kingdom

- 5.6.4.2 Germany

- 5.6.4.3 France

- 5.6.4.4 Spain

- 5.6.4.5 Italy

- 5.6.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.6.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.6.4.8 Rest of Europe

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Dyson

- 6.4.2 Philips (Versuni)

- 6.4.3 Xiaomi

- 6.4.4 Coway

- 6.4.5 Blueair (Unilever)

- 6.4.6 Sharp

- 6.4.7 Honeywell (licensed)

- 6.4.8 Levoit (Vesync)

- 6.4.9 Winix

- 6.4.10 IQAir

- 6.4.11 LG Electronics

- 6.4.12 Samsung

- 6.4.13 Medify Air

- 6.4.14 Guardian Technologies (GermGuardian)

- 6.4.15 AirDoctor (Ideal Living)

- 6.4.16 Airdog (IAQ Tech)

- 6.4.17 Austin Air Systems

- 6.4.18 Rabbit Air

- 6.4.19 TruSens (ACCO Brands)

- 6.4.20 Daikin

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment

- 7.2 Wildfire-ready "clean-room kits" for schools/municipal buildings (portable HEPA fleets + SOPs, rapid deployment)

- 7.3 Premium HEPA+Carbon travel/desk segment optimized for USB-C PD and airline/hotel duty cycles (subscription filters)