|

시장보고서

상품코드

2062424

미니 LED 디스플레이 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Mini-LED Display - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

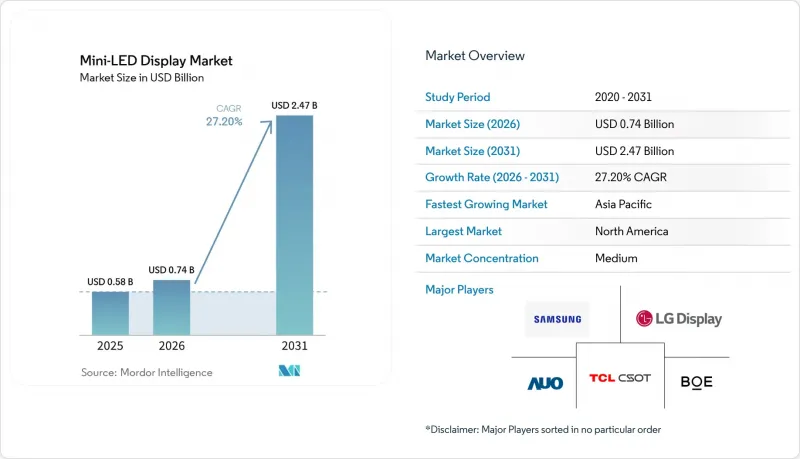

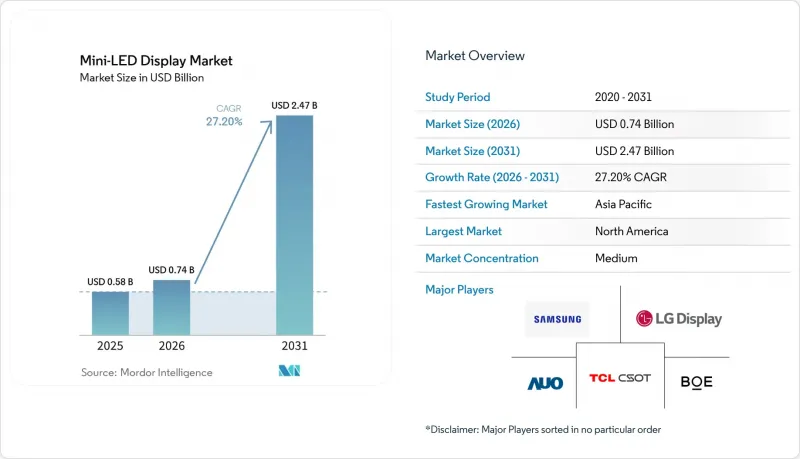

Mordor Intelligence에 의하면, 미니 LED 디스플레이 시장 규모는 2025년 5억 8,000만 달러로 평가되었고, 2026년 7억 4,000만 달러로 추정되고, 2031년까지 24억 7,000만 달러로 확대될 전망이며, 2026-2031년 연평균 복합 성장률(CAGR)은 27.20%를 나타낼 것으로 예측됩니다.

본 보고서는 용도별(TV, IT 모니터 및 노트북, 스마트폰 및 태블릿, 자동차용 디스플레이, 웨어러블 및 AR/VR), 기술별(미니 LED 백라이트 유닛, 직접 발광형 미니 LED), 백플레인 통합별(PCB 패시브 매트릭스, 유리 액티브 매트릭스, 플렉서블 하이브리드 기판), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 미니 LED 디스플레이 시장 동향 및 인사이트

미니 LED 백플레인의 비용 절감이 시장 확대를 주도

백플레인 제조 효율화를 통해 2025년에는 전년 대비 15-20%의 비용 절감이 실현되었으며, 55-65인치 TV에서 OLED와의 가격 차이가 해소되었습니다. LCD 인프라를 공유함으로써 유리 박막 트랜지스터(TFT) 백플레인 설비 투자를 상각할 수 있게 되었으며, TCL은 2025년 상반기에 미니 LED TV 출하량을 176% 증가시킬 수 있었습니다. 이는 비용과 수요 간의 탄력성을 여실히 보여줍니다. 금속 범프에서 전도성 포토레지스트 범프로의 전환을 통해 대량 전사 워크플로가 더욱 간소화되고 수율이 향상되었으며, 2031년까지 지속적인 비용 절감이 가능한 기술 기반이 마련되었습니다.

2025년 하반기, TV 제조업체들의 생산 능력이 OLED에서 전환될 전망

Samsung Electronics와 LG전자는 출하 대수 측면에서 미니 LED TV 시장을 독점하고 있는 중국 브랜드들의 경쟁 심화에 대응하기 위해, 2025년 하반기에 생산 라인을 OLED에서 RGB 미니 LED 기술로 전환했습니다. 이러한 전략적 전환을 통해 양사는 리드 타임을 단축하고 제품 라인업을 확충하는 한편, CES 2026에서 공개된 프리미엄 모델을 통해 신제품을 출시할 수 있었습니다. 이러한 움직임은 정교한 LCD 백라이트 기술을 경쟁 우위로 활용하겠다는 양사의 자신감을 여실히 보여주었으며, 진화하는 디스플레이 기술의 흐름 속에서 양사가 계속해서 입지를 공고히 하고 경쟁력을 유지할 수 있음을 확고히 했습니다.

55인치 미만 제품에서 OLED에 비해 부품 비용 면에서 갖는 우위

2025년, 55인치 미만의 미니 LED 패널은 LED 어레이 밀도가 높고 추가적인 드라이버 IC가 필요하기 때문에 OLED 패널보다 여전히 비용이 더 높았습니다. 이러한 비용 격차로 인해, 합리적인 가격이 중요한 요소인 가격에 민감한 시장 부문에서 미니 LED 기술의 보급은 제한되어 왔습니다. 그러나 QD(양자점)의 온칩 집적화가 진전됨에 따라 형광체 관련 비용 절감이 시작되었고, 미니 LED와 OLED 간의 비용 격차는 서서히 좁혀지고 있습니다. 이러한 개선에도 불구하고, 중형 디스플레이에서의 미니 LED 채택은 2028년 이후까지 제한적인 수준에 그칠 것으로 예측됩니다. 각 제조업체들은 향후 몇 년 동안 미니 LED 기술의 경쟁력을 높이기 위해 생산 공정의 최적화에 주력하고 있습니다.

부문별 분석

2025년, TV는 미니 LED 디스플레이 시장의 38.23%를 차지했습니다. 이는 OLED보다 높은 밝기를 저렴한 가격에 제공하는 프리미엄 모델에 힘입은 결과입니다. 이 부문은 중국의 급속한 생산 능력 이동과 보조금 정책의 혜택을 받았습니다. 자동차용 디스플레이 시장은 전기차(EV)에 10인치 이상의 콕핏 스크린이 점점 더 많이 채택됨에 따라, 2031년까지 연평균 성장률(CAGR) 27.55%로 성장할 것으로 전망됩니다. 이러한 대형 스크린은 운전자의 가시성을 높이고 고급 기능을 지원하기 위해 뛰어난 실외 가시성이 요구됩니다. 고성능 디스플레이에 대한 수요는 첨단 운전자 보조 시스템(ADAS) 및 인포테인먼트 기능의 통합으로 인해 더욱 확대되고 있습니다. 또한, 에너지 효율이 높고 내구성이 뛰어난 디스플레이 기술에 대한 수요 증가가 예측 기간 동안 이 부문의 성장을 견인할 것으로 전망됩니다.

전문가용 모니터와 노트북에 미니 LED가 탑재되면서 1,000니트를 넘는 밝기와 DCI-P3 100%라는 HDR 인증 기준을 충족하게 되어, 컨텐츠 크리에이터들에게 매우 매력적인 선택지가 되었습니다. 이러한 인증은 동영상 편집이나 그래픽 디자인과 같은 전문적인 용도에서 필수적인 뛰어난 색상 정확도와 밝기를 보장합니다. 스마트폰이나 태블릿에서의 적용은 제한적이었지만, 특히 애플의 iPad Pro에서는 디스플레이 성능 향상을 위해 미니 LED가 채택되었습니다. 그러나 웨어러블 기기의 경우 발열 문제와 미니 LED 기술의 높은 비용으로 인해 여전히 틈새 시장 용도로만 머물러 있습니다. 이러한 과제가 있기는 하지만, 미니 LED 기술의 발전으로 인해 다양한 기기 분야에서 점차적으로 도입이 확대될 것으로 예측됩니다.

지역별 분석

아시아태평양은 2025년에 54.74%의 시장 점유율을 차지했습니다. 이는 BOE, TCL, CSOT, Tianma와 같은 기업들이 속도와 비용 절감을 위해 LED 칩과 패널 생산을 통합한 중국의 수직 통합형 생태계에 힘입은 결과입니다. 보조금 덕분에 국내 미니 LED TV 시장 점유율이 10% 가까이 상승했습니다. 한편, 한국의 삼성디스플레이와 LG디스플레이는 시장 점유율을 지키기 위해 OLED에서 미니 LED로 생산 능력을 전환했습니다. 게다가, 해당 지역은 견고한 공급망과 정부의 지원을 바탕으로 채용이 더욱 가속화되었습니다. 가전 및 자동차 분야에서의 고성능 디스플레이 수요 증가 또한 해당 지역의 경쟁력에 기여했습니다. 아시아태평양은 미니 LED 디스플레이 시장의 혁신과 생산을 주도하는 핵심 거점으로 자리매김하고 있습니다.

북미와 유럽에서는 프리미엄 TV와 게이밍 모니터가 선호되며, 두 지역의 자동차 제조업체들은 디스플레이 품질과 기능성을 향상시키기 위해 전기차(EV)의 운전석에 미니 LED를 채택하고 있습니다. 2028년에 시행될 유럽연합(EU)의 에코디자인 규정은 백라이트의 전력 효율에 대한 요구를 더욱 강화하고 있으며, 그 결과 와트당 밝기를 향상시키는 하이존 미니 LED 설계의 채택을 촉진하고 있습니다. 이 지역들에서는 에너지 효율이 높으면서도 고해상도 디스플레이에 대한 수요 증가에 부응하기 위해 디스플레이 기술에 대한 투자도 확대되고 있습니다. 지속가능성과 혁신에 주력함으로써, 북미와 유럽은 미니 LED 시장에서 중요한 기여자로서의 입지를 확고히 하고 있습니다. 또한, 게임 및 홈 엔터테인먼트 시스템의 인기가 높아짐에 따라 프리미엄 디스플레이 솔루션에 대한 수요가 증가하고 있습니다.

중동은 상업용 부동산 및 교통 허브의 대형 디지털 사이니지에 힘입어, 2031년까지 지역별 최고 수준인 연평균 성장률(CAGR) 27.81%를 나타낼 것으로 전망됩니다. 해당 지역의 인프라 현대화와 첨단 기술 도입에 대한 집중이 미니 LED 디스플레이 수요를 견인하고 있습니다. 게다가, 스마트 시티 구축과 공공 공간 확충을 목표로 하는 정부 주도의 노력이 시장을 더욱 뒷받침하고 있습니다. 남미와 아프리카는 여전히 시장 점유율이 낮은 편이지만, 주목도가 높은 도시 프로젝트에서 미니 LED 비디오월 도입이 시작되고 있습니다. 이러한 지역에서는 광고, 엔터테인먼트, 공공 정보 시스템 등의 용도로 미니 LED 기술이 점차 도입되고 있어, 향후 성장 가능성을 보여주고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the mini-LED display market size is projected to expand from USD 0.58 billion in 2025 and USD 0.74 billion in 2026 to USD 2.47 billion by 2031, registering a CAGR of 27.20% between 2026 and 2031.

This report is Segmented by Application (Televisions, IT Monitors and Laptops, Smartphones and Tablets, Automotive Displays, and Wearables and AR/VR), Technology (Mini-LED Backlight Unit, and Direct-Emissive Mini-LED), Backplane Integration (PCB Passive Matrix, Glass Active Matrix, and Flexible Hybrid Substrate), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Mini-LED Display Market Trends and Insights

Falling Mini-LED Back-Plane Costs Drive Market Expansion

Back-plane manufacturing efficiencies drove a 15-20% year-over-year cost decline in 2025, closing the price gap with OLED in 55-65 inch televisions. Shared LCD infrastructure allowed glass thin-film transistor back-planes to amortize capital expenditures and enabled TCL to lift Mini-LED TV shipments by 176% in H1 2025, underscoring the elasticity between cost and demand. Shift from metal bumps to conductive photoresist bumps further simplified the mass-transfer workflow, boosting yields and positioning the technology for continued cost compression through 2031.

TV Makers Capacity Switches From OLED in 2H 2025

Samsung Electronics and LG Electronics reallocated production lines from OLED to RGB Mini-LED technology in late 2025 to address the growing competition from Chinese brands, which dominated the Mini-LED TV market in terms of volume. This strategic shift allowed the companies to reduce lead times, broaden their product offerings, and introduce new models through premium tiers showcased at CES 2026. The move highlighted their confidence in leveraging refined LCD back-lighting technology as a competitive advantage, ensuring they remain relevant and competitive in the evolving display technology landscape.

Bill of Materials Premium Over OLED Below 55 Inch

In 2025, Mini-LED panels below 55 inches remained costlier than OLED panels due to the higher LED-array density and the need for additional driver ICs. This cost disparity limited the penetration of Mini-LED technology in price-sensitive market segments, where affordability is a key factor. However, advancements in QD on-chip integration have started to reduce phosphor-related expenses, gradually narrowing the cost gap between Mini-LED and OLED. Despite these improvements, the adoption of Mini-LED in mid-size displays is expected to remain limited until after 2028. Manufacturers are focusing on optimizing production processes to make Mini-LED technology more competitive in the coming years.

Other drivers and restraints analyzed in the detailed report include:

- Automotive Cockpits Shift to >= 2,000-Nit Displays

- Micro-LED Yield Issues Prolonging Mini-LED Window

- HDR Halo Complaints in Gaming Monitors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Televisions accounted for 38.23% of the Mini-LED Display market in 2025, supported by premium models that offered higher brightness than OLED at lower prices. The segment benefited from rapid capacity shifts and subsidies in China. Automotive displays are projected to grow at a 27.55% CAGR through 2031 as electric vehicles increasingly adopt cockpit screens larger than 10 inches. These larger screens require superior sunlight readability to enhance driver visibility and support advanced functionalities. The demand for high-performance displays is further driven by the integration of advanced driver assistance systems (ADAS) and infotainment features. Additionally, the push for energy-efficient, durable display technologies is expected to drive growth in this segment over the forecast period.

Adoption of Mini-LED in professional monitors and laptops has strengthened since it met HDR certifications exceeding 1,000 nits and 100% DCI-P3, making it highly attractive to content creators. These certifications ensure superior color accuracy and brightness, critical for professional applications such as video editing and graphic design. Smartphones and tablets saw limited adoption, particularly with Apple's iPad Pro, which used Mini-LED for enhanced display performance. However, wearables remained a niche application due to thermal constraints and the high cost of Mini-LED technology. Despite these challenges, advancements in Mini-LED technology are expected to gradually expand its adoption across various device categories.

Geography Analysis

Asia-Pacific captured 54.74% market share in 2025, driven by China's vertically integrated ecosystem, where BOE, TCL, CSOT, and Tianma aligned LED chip and panel production for speed and cost savings. Subsidies lifted Mini-LED television share toward 10% domestically, while South Korea's Samsung Display and LG Display redirected capacity from OLED to Mini-LED to defend their market share. Additionally, the region benefited from a strong supply chain and government support, which further accelerated adoption. The increasing demand for high-performance displays in consumer electronics and automotive applications also contributed to the region's dominance. Asia-Pacific remains a key hub for innovation and production in the mini-LED display market.

North America and Europe favored premium televisions and gaming monitors, with automakers in both regions specifying Mini-LED cockpits for electric vehicles to enhance display quality and functionality. The European Union's Ecodesign rules, effective in 2028, place efficiency pressure on back-light power, inadvertently encouraging the adoption of high-zone Mini-LED designs that improve luminance per watt.These regions also witnessed growing investments in display technologies to meet e increasing demand for energy-efficient, high-resolution displays. The focus on sustainability and innovation has positioned North America and Europe as significant contributors to the Mini-LED market. Furthermore, the rising popularity of gaming and home entertainment systems has driven demand for premium display solutions.

The Middle East is projected to record the fastest regional CAGR at 27.81% through 2031, propelled by large-format digital signage in commercial real estate and transportation hubs. The region's focus on modernizing infrastructure and adopting advanced technologies has fueled the demand for Mini-LED displays. Additionally, government initiatives to develop smart cities and enhance public spaces have further boosted the market. South America and Africa remain smaller contributors but are starting to deploy Mini-LED video walls in high-visibility urban projects. These regions are gradually embracing Mini-LED technology for applications in advertising, entertainment, and public information systems, showcasing their potential for future growth.

- Samsung Electronics Co., Ltd.

- Apple Inc.

- LG Display Co., Ltd.

- BOE Technology Group Co., Ltd.

- AU Optronics Corp.

- Innolux Corporation

- TCL China Star Optoelectronics Technology Co., Ltd.

- Sony Group Corporation

- Nichia Corporation

- Everlight Electronics Co., Ltd.

- Osram GmbH

- Epistar Corporation

- Seoul Semiconductor Co., Ltd.

- Cree LED (Smart Global Holdings, Inc.)

- Nationstar Optoelectronics Co., Ltd.

- San'an Optoelectronics Co., Ltd.

- Tianma Micro-electronics Co., Ltd.

- Konka Group Co., Ltd.

- Hisense Visual Technology Co., Ltd.

- Unilumin Group Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Falling Mini-LED Back-Plane Costs

- 4.2.2 TV Makers Capacity Switches From OLED in 2H 2025

- 4.2.3 Automotive Cockpits Shift to >= 2,000-Nit Displays

- 4.2.4 Micro-LED Yield Issues Prolonging Mini-LED Window

- 4.2.5 Quantum-Dot On-Chip Patents Expiring 2026

- 4.2.6 In-Flight Entertainment Retrofits 2025-2027

- 4.3 Market Restraints

- 4.3.1 Bill of Materials Premium Over OLED Below 55 Inch

- 4.3.2 HDR Halo Complaints in Gaming Monitors

- 4.3.3 EU Ecodesign Ban on > 5 W Back-Lights 2028

- 4.3.4 Rare-Earth Phosphor Price Volatility

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 TVs

- 5.1.2 IT Monitors and Laptops

- 5.1.3 Smartphones and Tablets

- 5.1.4 Automotive Displays

- 5.1.5 Wearables and AR/VR

- 5.2 By Technology

- 5.2.1 Mini-LED Backlight Unit (BLU)

- 5.2.2 Direct-Emissive Mini-LED

- 5.3 By Backplane Integration

- 5.3.1 PCB Passive Matrix

- 5.3.2 Glass Active Matrix

- 5.3.3 Flexible Hybrid Substrate

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 Singapore

- 5.4.4.7 Malaysia

- 5.4.4.8 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Turkey

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Samsung Electronics Co., Ltd.

- 6.4.2 Apple Inc.

- 6.4.3 LG Display Co., Ltd.

- 6.4.4 BOE Technology Group Co., Ltd.

- 6.4.5 AU Optronics Corp.

- 6.4.6 Innolux Corporation

- 6.4.7 TCL China Star Optoelectronics Technology Co., Ltd.

- 6.4.8 Sony Group Corporation

- 6.4.9 Nichia Corporation

- 6.4.10 Everlight Electronics Co., Ltd.

- 6.4.11 Osram GmbH

- 6.4.12 Epistar Corporation

- 6.4.13 Seoul Semiconductor Co., Ltd.

- 6.4.14 Cree LED (Smart Global Holdings, Inc.)

- 6.4.15 Nationstar Optoelectronics Co., Ltd.

- 6.4.16 San'an Optoelectronics Co., Ltd.

- 6.4.17 Tianma Micro-electronics Co., Ltd.

- 6.4.18 Konka Group Co., Ltd.

- 6.4.19 Hisense Visual Technology Co., Ltd.

- 6.4.20 Unilumin Group Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment