|

시장보고서

상품코드

2062436

PLC, SCADA, DCS 교육 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)PLC, SCADA, And DCS Training - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

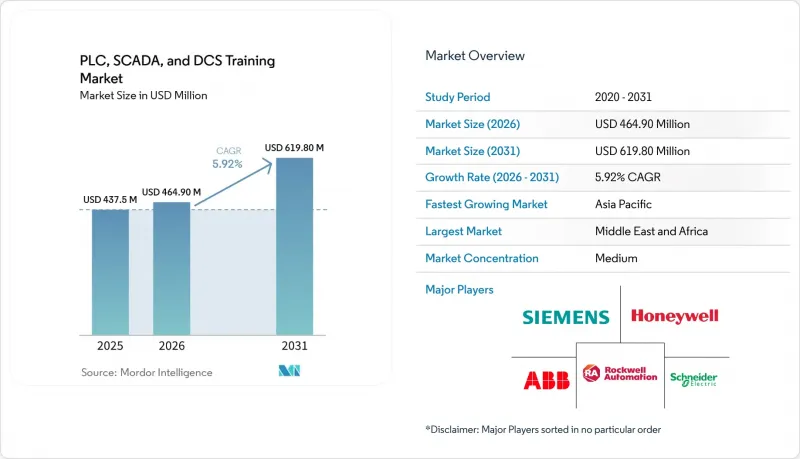

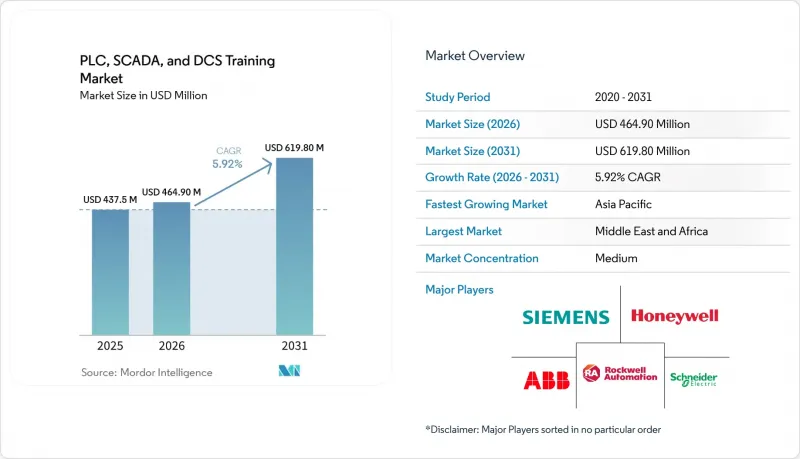

Mordor Intelligence에 의하면, PLC, SCADA, DCS 교육 시장 규모는 2025년 4억 3,750만 달러로 평가되었고, 2026년 4억 6,490만 달러로 추정되고, 2031년까지 6억 1,980만 달러로 확대될 전망이며, 2026-2031년 연평균 복합 성장률(CAGR)은 5.92%를 나타낼 것으로 예측됩니다.

본 보고서는 교육 형식별(강사 주도형 대면 교육, 가상 강사 주도형 등), 시스템 유형별(PLC, SCADA, DCS), 최종 사용자 산업별(석유 및 가스, 발전, 제조 및 디스크리트, 화학제품 및 석유화학제품 등), 지역별(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 PLC, SCADA, DCS 교육 시장 동향 및 인사이트

기존 시스템으로의 전환에는 재교육 프로그램이 필요합니다.

설비 소유주들은 노후화된 PLC 및 DCS 플랫폼에서 현재의 통합 엔지니어링 환경으로 전환하고 있으며, 가동 시간을 확보하기 위해서는 단계적인 전환 기간 동안 엔지니어들이 기존 시스템과 신규 시스템 모두에 정통해야 합니다. 주요 OEM의 교육 카탈로그에서는 마이그레이션 프로세스와 역할 기반 마이그레이션 모듈이 명확하게 다루어지고 있습니다. 이는 그린필드 방식의 도입으로는 브라운필드 프로젝트에 필요한 이중 시스템 대응 능력을 충족시킬 수 없기 때문입니다. 시스템 통합 업체들 또한 베테랑 인력의 퇴직으로 인해 레거시 시스템에 대한 전문 지식이 부족하다는 점을 지적하고 있으며, 시운전이나 가동과 같은 중요한 단계에서 그 효과를 확인할 수 있는 체계적인 재교육의 필요성이 커지고 있습니다. OEM 교육 서비스에서는 마이그레이션에 중점을 둔 과정과 고급 마이그레이션 실습을 확대하고 있어, 기술자들이 실제 환경에 대한 위험 부담 없이 에뮬레이션된 환경이나 최신 릴리스에서 실습할 수 있게 되었습니다. 지역별 채용 데이터에 따르면, 기술직 채용 결정까지의 기간이 길어짐에 따라 시운전 일정이 지연되고 있으며, 이는 외부 채용에 의존하기보다는 현직 직원에 대한 재교육을 실시해야 한다는 주장을 뒷받침하고 있습니다. 마이그레이션 프로젝트는 부문화된 아키텍처로의 업그레이드나 안전한 원격 액세스와 중복되는 경우가 많기 때문에 이러한 이중적인 기술 요건은 현재 사이버 보안 및 네트워크 세분화 실무와도 밀접하게 연관되어 있습니다. 따라서 실습 및 사후 평가 체크포인트를 갖춘 체계적인 전환 학습 과정은 가동을 중단하지 않고 제어 시스템을 현대화하는 플랜트에서 표준적인 접근 방식으로 자리 잡고 있습니다.

세계적으로 의무화가 진행되고 있는 OEM 인증

각 벤더사는 고객 지원, 보증 내용, 소프트웨어 접근 권한을 검증된 역량 개발 경로와 연계하고 있으며, 이에 따라 인증 자격은 '있으면 좋은 것'에서 복잡한 도입 과정에서 '실무상 필수 요건'으로 변화하고 있습니다. 록웰사는 역할 기반 학습 계획을 검증된 숙련도와 연계하고, '평가, 훈련, 실무, 평가'의 사이클을 통합함으로써 고용주가 성과를 추적하고, 권한을 기술 수준에 맞추어 조정할 수 있도록 지원합니다. 하네웰은 기초 지식과 현장에서 검증된 전문 지식을 구분하기 위해 강의, 지도 하에 진행되는 실습, 감독 하에 실시되는 시험을 결합한 다단계 프로그램을 구축하고 있습니다. 보안 인증 또한 안전한 개발 라이프사이클의 증거이자 IEC 62443에 기반한 시스템 수준의 검증을 요구하는 ISASecure 체계를 통해 생태계 전반에 걸쳐 표준화가 진행되고 있으며, 이는 통합업체 및 운영업체의 교육 계획으로까지 확대되고 있습니다. 지멘스는 고용주가 다양한 수준의 숙련도를 벤치마킹하고, 검증 가능한 기술 배지를 바탕으로 인재 확보 전략을 조정할 수 있도록 지원하는 파트너 자격 인증 프로그램을 운영하고 있습니다. 플랜트에서 클라우드 기반 SCADA를 더 많이 도입하고 릴리스 주기가 빈번해짐에 따라, 팀이 플랫폼의 기능과 보안 설정 방법에 대해 항상 최신 정보를 파악할 수 있도록 인증 주기가 단축되고 있습니다. 따라서 PLC, SCADA, DCS 교육 시장은 공급업체의 지원 수준이나 프로젝트 참여 자격을 직원의 자격 요건과 연계하는 조달 정책의 영향을 받고 있습니다.

훈련 예산은 설비 투자 주기와 연동됩니다.

교육 수요는 시운전 성수기에는 증가하지만, 예산이 유지보수나 린 운영에 배정되면 둔화되며, 그 결과 역량 강화 계획이 지연되거나 규모가 축소될 가능성이 있습니다. 업계 단체의 조사에 따르면, 인력 부족은 생산성 저하와 가동 중단 위험으로 이어진다고 합니다. 그러나 자본 계획이 엄격해지면, 많은 공장에서는 교육비나 출장비가 다른 지출 항목과 경쟁 관계에 놓이게 되어 여전히 교육을 미루고 있습니다. OEM 카탈로그에는 공장을 떠나야 하는 며칠간의 강사 주도형 과정이나 실습 위주의 교육이 포함되어 있어, 이는 예산 주기 내 비용 부담을 가중시키고 있습니다. 각 공급업체는 자금을 사전에 확보하고 분기별 투자를 안정화하기 위해 교육 예산을 배분하는 계약상 체계를 도입함으로써 이 과제에 대응하고 있습니다. 또한 고용주 측에서도 실무 중심의 실습을 유지하면서 출장이나 근무 조정의 부담을 줄이기 위해 블렌디드 교육이나 가상 실험실의 활용을 검토하고 있습니다. 채용난이 지속되고 있는 상황은 다음 투자 주기에 대비하기 위해 경기 둔화기에 연수를 실시하는 것이 합리적이라는 점을 뒷받침하고 있습니다. 그럼에도 불구하고, 모든 기업이 사이클 전반에 걸쳐 기술 향상 프로그램에 대한 꾸준한 투자를 유지하기 위한 거버넌스나 인센티브를 갖추고 있는 것은 아닙니다.

부문별 분석

2025년 매출 중 강사 주도형 대면 교육이 45.44%를 차지한 반면, 고용주들이 실무 중심의 실습과 유연한 온라인 지도의 균형을 맞추어감에 따라 블렌디드 러닝은 2031년까지 연평균 성장률(CAGR) 11.64%로 성장할 것으로 전망됩니다. PLC, SCADA, DCS 교육 시장은 감독 하에 진행되는 실습을 통해 실무 능력을 유지하면서도 생산 현장을 떠나는 시간을 단축할 수 있는 혼합 학습의 이점을 누리고 있습니다. OEM 및 교육 기관은 자기 주도형 모듈과 강사 주도 실습을 결합한 블렌디드 학습 체계를 구축하고 있으며, 이를 통해 학습자는 실무 과제에 충분히 대비한 상태로 임할 수 있어, 성과 저하 없이 총 수강 시간을 단축할 수 있습니다. 교육 팀은 대규모 수강생 그룹이나 분산된 직원들을 대상으로 혼합형 학습을 확대함에 있어 수료율과 만족도 데이터를 중시하고 있으며, 이는 기업이 수강생 그룹에 지속적으로 투자하도록 장려하고 있습니다. 클라우드 기반 제어 환경을 활용한 가상 강사 주도형 교육을 통해, 참가자는 어디서나 에뮬레이션된 컨트롤러 및 엔지니어링 도구에 접근할 수 있게 되어, 소규모 지사에서도 하드웨어에 쉽게 접근할 수 있게 됩니다. 또한, 과정 제공업체는 마이크로러닝이나 이러닝 입문 교재를 활용하여 수업 시간을 단축하는 한편, 인증 기준을 충족하기 위해 실습을 통한 검증을 여전히 요구하고 있습니다.

기업들은 몰입형 시뮬레이터와 디지털 트윈을 통합한 방식을 계속해서 선호하고 있으며, 이를 통해 운영자는 장비에 대한 위험 부담 없이 장애 복구 및 인터록 로직 연습을 수행할 수 있습니다. 이 모델은 교대 근무를 넘나들며 일관된 교육 경험을 제공하며, 인력 배치의 현실과 근무 시간의 우선순위에 맞추어 짧은 세션으로 진행할 수 있습니다. 언어 및 지역별 규제를 포함한 각 지역의 요구 사항에 따라, 서비스 제공업체들은 동일한 혼합형 아키텍처를 활용해 맞춤형 컨텐츠를 제공합니다. 이를 통해 기업은 각 사업장 간에 교육 과정을 표준화할 수 있게 됩니다. 블렌디드형 컨텐츠에 성과 기반 역량 모델이나 역할 기반 성과 평가를 결합한 공급업체는 더 높은 재채용률을 기록하고 있습니다. PLC, SCADA, DCS 교육 시장은 인력 부족의 압박 속에서 플랜트들이 기술 검증 범위를 확대함에 따라, 블렌디드형 및 가상 실습 환경으로 계속 전환될 것으로 예측됩니다.

지역별 분석

2025년, 아시아태평양은 세계 매출의 39.44%를 차지했습니다. 이는 중국, 인도, 일본, 동남아시아의 제조 생태계가 자동화 기술 도입 기반을 확대했기 때문입니다. 이 지역의 PLC, SCADA, DCS 교육 시장은 교육 포털 및 현지 교육 제공에 대한 OEM의 투자 혜택을 받고 있으며, 이에 따라 컨트롤러, SCADA, 안전, 사이버 보안 교육 과정에 대한 제공 역량이 확대되고 있습니다. 인도 및 동남아시아 공급업체와 파트너들은 PLC, 로봇 공학, SCADA 운영에 관한 실무 중심 프로그램을 지속적으로 제공하고 있으며, 플랜트 내 각 직무별 단기 기술 재교육 과정을 보완하는 수주간의 선택 과정도 마련되어 있습니다. 싱가포르에서는 업계 단체, 교육 기관, OEM 간의 '인더스트리 4.0' 및 '인더스트리 5.0' 관련 협력을 통해, 실험실 체험 및 실무 중심의 시운전 실습을 표준화한 전문 교육 과정의 제공 체계가 확대되고 있습니다. 디지털 트윈 방식을 도입하는 플랜트가 늘어남에 따라, 지역 팀들은 공급업체의 플랫폼을 활용하여 중앙 집중식 출장 없이도 운영자의 시뮬레이션 훈련 및 역량 강화를 도모하고 있습니다. 따라서 아시아태평양의 PLC, SCADA, DCS 교육 시장은 대규모 현지 맞춤형 서비스와 고처리량 생산 환경에 적합한 교육 형식에 힘입어 성장하고 있습니다.

중동 및 아프리카에서는 산업 다각화와 인프라 구축 계획에 따라 공정 산업 및 유틸리티 분야의 교육 수요가 증가하고 있으며, 2031년까지 연평균 성장률(CAGR) 12.35%로 시장이 확대될 것으로 전망됩니다. 해당 지역의 프로그램에서는 중요 인프라 분야의 운영자, 엔지니어, 유지보수 담당자를 대상으로 사이버 보안을 고려한 교육과 역할에 따른 역량 개발을 중점적으로 실시했습니다. OEM 업체들은 광범위한 지리적 범위와 외딴 지역에서의 물류 복잡성을 완화하기 위해 몰입형 및 가상 훈련 요소를 도입하고 있습니다. 해당 지역의 PLC, SCADA, DCS 교육 시장은 가동 중인 시설 내에 도입 가능한 혼합형이자 현장 대응형 학습 시스템으로 지속적으로 전환되고 있습니다. 점점 더 많은 산업 분야 사용자들이 클라우드 히스토리안 및 중앙 집중식 운영 센터를 도입함에 따라, 해당 지역의 SCADA 운영자 교육 과정에는 보안 대책, 경보 관리, 그리고 여러 거점에 분산된 설비 군에 맞춘 KPI가 통합되어 있습니다. 기술 교육 기관과의 산업 간 협력을 통해 초급 기술자 양성 규모가 확대될 것이며, 이후 도입된 플랫폼에서 OEM별 맞춤형 역량 강화 교육이 실시될 것으로 예측됩니다.

북미에서는 대학과의 제휴, OEM 교육 허브, 통합업체 생태계를 통해 여전히 강력한 입지를 유지하고 있지만, 인구 통계학적 요인과 채용 측면의 제약이 교육 형식에 지속적인 영향을 미치고 있습니다. 북미의 PLC, SCADA, DCS 교육 시장에서는 고용주들이 직무 내용에 부합하고 실기 시험을 통해 숙련도를 평가하는 성과 기반 역량 모델을 선호하는 경향이 뚜렷합니다. 고용주들은 이동 시간을 줄이면서도 수강생들이 자격증을 취득하기 전에 실기 평가를 확실히 마칠 수 있도록 블렌디드 학습 및 가상 실습 환경을 확대되고 있습니다. 기업의 교육 센터와 지역 연구소에서는 로봇 공학, 제어, 비전 시스템 분야의 수용 능력을 지속적으로 확대하고 있어, 고용주는 수강생들을 시간대를 달리하여 그룹별로 파견할 수 있게 되었습니다. 유럽의 프로그램은 여전히 다양하며, 각국의 언어, 규제, 레거시 시스템의 현대화가 국가별 차이를 낳고 있습니다. OEM 아카데미와 현지 파트너들은 수요에 부응하기 위해 교육실, 실습 공간, 강사진을 확충하고 있습니다. 남미의 PLC, SCADA, DCS 교육 시장은 주요 제조업 클러스터와 광업 분야 특유 수요를 중심으로 성장하고 있습니다. 광업 분야에서는 벤더 주도의 프로그램 및 파트너 네트워크의 지원을 받아, PLC 및 SCADA 시스템에 관한 운영자 및 유지보수 담당자 교육이 계속해서 최우선 과제로 남아 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the pLC, sCADA, and dCS training market size is projected to expand from USD 437.5 million in 2025 and USD 464.90 million in 2026 to USD 619.80 million by 2031, registering a CAGR of 5.92% between 2026 to 2031.

This report is Segmented by Training Mode (Instructor-Led Classroom, Virtual Instructor-Led, and More), System Type (PLC, SCADA, and DCS), End-User Industry (Oil & Gas, Power Generation, Manufacturing & Discrete, Chemicals & Petrochemicals, and More), and Geography (North America, South America, Europe, Asia-Pacific, Middle East & Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global PLC, SCADA, And DCS Training Market Trends and Insights

Brownfield Migrations Require Retraining Programs

Equipment owners are transitioning from aging PLC and DCS platforms to current integrated engineering environments, which require engineers to maintain fluency in both outgoing and incoming systems during staged cutovers to protect uptime. Training catalogs from major OEMs explicitly address migration tracks and role-based transition modules because greenfield-style onboarding does not cover dual-system competencies needed for brownfield projects. System integrators also flag a shortage of legacy-system expertise as senior personnel retire, heightening the need for structured retraining that can be validated during critical phases such as commissioning and start-up. OEM education services have expanded migration-focused courses and advanced transition labs so technicians can practice on emulated and current releases without production risk. Regional hiring data confirms that time-to-fill for technical roles extends commissioning timelines, which reinforces the case for retraining incumbent staff rather than relying on external hires. This dual-competency need now overlaps with cybersecurity and network segmentation practices, as migration projects often coincide with upgrades to segmented architectures and secure remote access. Structured migration learning paths with hands-on labs and post-assessment checkpoints are therefore becoming the norm for plants modernizing controls while operating at capacity.

OEM Certifications Increasingly Mandated Globally

Vendors have aligned customer support, warranty features, and software access with verified competency pathways, moving certification from a nice-to-have to a practical requirement for complex deployments. Rockwell ties role-based learning plans to validated proficiency and integrates Evaluate, Train, Practice, and Assess cycles so employers can track outcomes and align privileges to skill level. Honeywell structures multi-tier programs that combine classroom hours, supervised labs, and proctored exams to distinguish foundational knowledge from field-proven expertise. Security certifications are also normalizing across the ecosystem through ISASecure schemes that require secure development lifecycle evidence and system-level validation against IEC 62443, which then cascades into integrator and operator training plans. Siemens runs partner qualification and certification programs that help employers benchmark multi-level proficiency and align procurement with verifiable skill badges. As plants adopt more cloud-connected SCADA and more frequent release cycles, certification cycles are tightening to ensure teams remain current on platform features and secure configuration practices. The PLC, SCADA, and DCS Training market is therefore influenced by procurement policies that link vendor support tiers and project eligibility to staff credentials.

Training Budgets Cyclic with CAPEX Cycles

Training demand expands during commissioning waves and slows when budgets rotate toward maintenance and lean operations, which can delay or narrow upskilling plans. Industry association research ties workforce gaps to productivity and downtime risks. Yet, many plants still defer training when capital plans tighten because course fees and travel compete with other spend categories. OEM catalogs show multi-day instructor-led courses and lab-based practicums that require time away from the plant, which increases the perceived cost during the budget cycle. Vendors are countering this with contractual mechanisms that pre-commit funds and match training allocations to stabilize investment across quarters. Employers also look to blended formats and virtual labs to reduce travel and shift coverage burdens while maintaining practical exercises. Persistent hiring gaps reinforce the logic of training during slowdowns to prepare for the next investment cycle. Still, not all firms have the governance or incentives to maintain steady investment in skills programs through the cycle.

Other drivers and restraints analyzed in the detailed report include:

- Workforce Shortages in Industrial Automation

- Remote Monitoring Growth Drives SCADA Skills

- High Opportunity Cost of Downtime Events

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Instructor-led classroom training accounted for 45.44% of 2025 revenue, while blended learning is projected to grow at a 11.64% CAGR through 2031 as employers balance hands-on labs with flexible online instruction. The PLC, SCADA, and DCS Training market benefits from blended tracks that reduce time away from production while preserving practical skills that require supervised exercises. OEMs and academies have formalized blended structures that pair self-paced modules with instructor-led labs, so learners arrive prepared for hands-on tasks, reducing overall seat time without sacrificing outcomes. Training teams have emphasized completion and satisfaction data as they scale blended modalities for large cohorts and distributed workforces, which supports enterprise buy-in for repeat cohorts. Virtual instructor-led training using cloud-hosted control environments gives participants access to emulated controllers and engineering tools from any location, which democratizes hardware access for smaller sites. Course providers also use microlearning and e-learning primers to reduce classroom time, while still requiring lab validation to meet certification thresholds.

Enterprises continue to favor formats that integrate immersive simulators and digital twins, enabling operators to practice failure recovery and interlock logic without equipment risk. This model delivers consistent training experiences across shifts and can be conducted in shorter sessions that align with staffing realities and uptime priorities. Regional needs, including language and localized regulations, are driving providers to offer tailored content with the same blended architecture, enabling enterprises to standardize curricula across sites. Vendors that combine blended content with outcome-based competency models and role-based performance checks are seeing stronger repeat adoption. The PLC, SCADA, and DCS Training market is expected to keep shifting toward blended and virtual labs as plants scale skill verification under staffing pressure.

Geography Analysis

Asia-Pacific accounted for 39.44% of global revenue in 2025, as manufacturing ecosystems across China, India, Japan, and Southeast Asia expanded the installed base of automation technologies. The PLC, SCADA, and DCS Training market in the region benefits from OEM investment in training portals and local delivery, which scales capacity for controller, SCADA, safety, and cybersecurity curricula. Vendors and partners in India and Southeast Asia continue to roll out practical programs for PLCs, robotics, and SCADA operations, with multi-week options that complement shorter skill refreshers across plant roles. Singapore's Industry 4.0 and 5.0 collaborations between associations, academies, and OEMs are expanding capacity for professional training lines that standardize lab experiences and hands-on commissioning practice. As more plants adopt digital twin approaches, regional teams leverage vendor platforms for operator rehearsal and competency acceleration without the need for centralized travel. The PLC, SCADA, and DCS Training market in Asia-Pacific is therefore anchored by localized delivery at scale and formats that align with high-throughput production environments.

The Middle East and Africa are projected to advance at 12.35% CAGR through 2031 as industrial diversification and infrastructure programs increase training demand in process industries and utilities. Regional programs emphasize cybersecurity-aligned training and role-based competency for operators, engineers, and maintainers in critical infrastructure sectors. OEMs are adding immersive and virtual training elements that reduce logistics complexity across large geographic footprints and remote sites. The PLC, SCADA, and DCS Training market in the region continues to shift toward blended, on-site-ready learning systems that can be deployed within operating facilities. As more industrial users adopt cloud historians and centralized operations centers, SCADA operator training in the region integrates security practices, alarm management, and KPIs tailored to multi-site fleets. Cross-industry partnerships with technical academies are expected to increase the throughput of entry-level technicians, followed by OEM-specific upskilling on installed platforms.

North America maintains a significant presence with university partnerships, OEM training hubs, and integrator ecosystems, though demographic and hiring constraints continue to shape training formats. The PLC, SCADA, and DCS Training market in North America reflects strong employer preference for outcome-based competency models that align with job roles and measure proficiency with practical exams. Employers are scaling blended and virtual labs to reduce travel time while ensuring students still complete hands-on assessments before earning credentials. Enterprise training centers and regional labs continue to add capacity for robotics, controls, and vision systems, enabling employers to send cohorts in staggered blocks. Programs in Europe remain diverse, with national languages, regulations, and legacy modernizations driving country-level differences; OEM academies and local partners are expanding training rooms, stations, and instructors to meet demand. The PLC, SCADA, and DCS Training market in South America centers on core manufacturing clusters and sector-specific demand in mining, where operator and maintenance training on PLCs and SCADA systems remains a priority, supported by vendor-led programs and partner networks.

- Siemens (SITRAIN)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Brownfield migrations require retraining programs

- 4.2.2 OEM certifications increasingly mandated globally

- 4.2.3 Workforce shortages in industrial automation

- 4.2.4 Remote monitoring growth drives SCADA skills

- 4.2.5 IEC 62443 role-based training adoption

- 4.2.6 Digital twins embedded in training curricula

- 4.3 Market Restraints

- 4.3.1 Training budgets cyclic with CAPEX cycles

- 4.3.2 High opportunity cost of downtime events

- 4.3.3 Siloed vendor ecosystems hinder cross-training

- 4.3.4 Credential inflation confuses employer signals

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Training Ecosystem Mapping (OEM, SI, Independents)

- 4.9 Insights on Certification Pathways by Major Vendors

- 4.10 Cybersecurity Curriculum Alignment (IEC 62443)

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Training Mode

- 5.1.1 Instructor-Led Classroom

- 5.1.2 Virtual Instructor-Led (VILT)

- 5.1.3 Self-Paced e-Learning

- 5.1.4 Blended Learning

- 5.2 By System Type

- 5.2.1 PLC

- 5.2.2 SCADA

- 5.2.3 DCS

- 5.3 By End-User Industry

- 5.3.1 Oil & Gas

- 5.3.2 Power Generation

- 5.3.3 Manufacturing & Discrete

- 5.3.4 Chemicals & Petrochemicals

- 5.3.5 Food & Beverage

- 5.3.6 Pharmaceuticals & Life Sciences

- 5.3.7 Water & Wastewater

- 5.3.8 Mining & Metals

- 5.3.9 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Chile

- 5.4.2.4 Peru

- 5.4.2.5 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.4.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.4.3.8 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East & Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East & Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Siemens (SITRAIN)

- 6.4.1.1 Rockwell Automation (Rockwell Automation University)

- 6.4.1.2 Schneider Electric (Training, AVEVA)

- 6.4.1.3 ABB (ABB University)

- 6.4.1.4 Emerson (Educational Services, DeltaV)

- 6.4.1.5 Honeywell (Automation College)

- 6.4.1.6 Yokogawa (Training Services)

- 6.4.1.7 Mitsubishi Electric (FA Learning)

- 6.4.1.8 Omron (Training)

- 6.4.1.9 Phoenix Contact (Training)

- 6.4.1.10 Beckhoff Automation (Training)

- 6.4.1.11 WAGO (Training)

- 6.4.1.12 Bosch Rexroth (Training)

- 6.4.1.13 GE Digital (Proficy SCADA Training)

- 6.4.1.14 AVEVA (Wonderware) Training

- 6.4.1.15 Inductive Automation (Inductive University)

- 6.4.1.16 Delta Electronics (Industrial Automation Training)

- 6.4.1.17 Advantech (Academy)

- 6.4.1.18 Hitachi Industrial (Training)

- 6.4.1.19 Matrikon (OPC Training)

- 6.4.1.20 B&R Industrial Automation (Training)

- 6.4.1.21 Pilz (Safety Automation Training)

- 6.4.1 Siemens (SITRAIN)

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment