|

시장보고서

상품코드

2062440

AI코드 툴 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI Code Tools - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

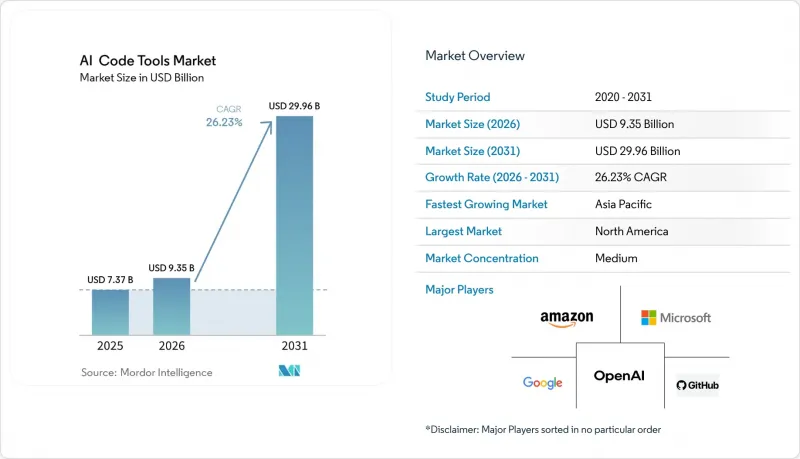

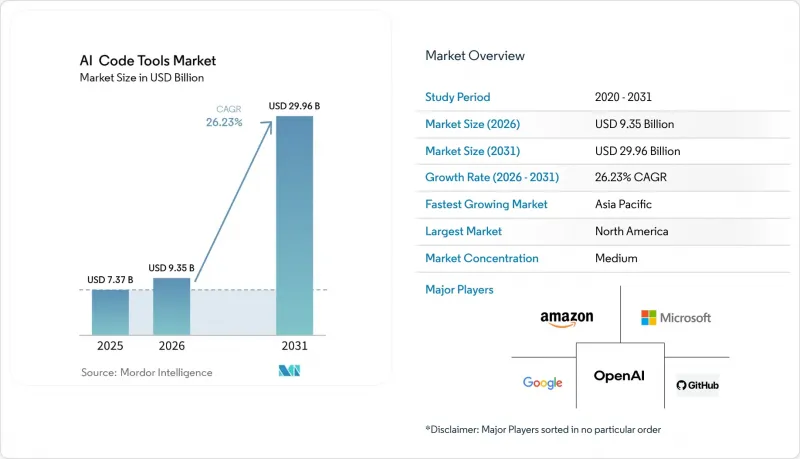

Mordor Intelligence에 의하면, 인공지능(AI) 코드 툴 시장 규모는 2025년에 73억 7,000만 달러로 평가되었고, 2026년에 93억 5,000만 달러로 추정되고, 2031년까지 299억 6,000만 달러에 이를 것으로 예측됩니다.

2026-2031년 연평균 성장률(CAGR) 26.23%로 성장할 것으로 전망됩니다.

본 보고서는 도입 형태별(클라우드 기반 등), 툴 기능별(코드 완성, 코드 생성, 코드 검토 및 최적화 등), 최종 사용자 산업 분야별(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 헬스케어 및 생명과학, 소매 및 전자상거래 등), 조직 규모별(대기업, 중소기업) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 AI 코드 툴 시장 동향 및 인사이트

LLM의 정확도가 비약적으로 향상됨에 따라, 코드 생성에 대한 기업의 신뢰도가 높아지고 있습니다.

2025년, HumanEval에서 기초 모델의 정확도는 90%를 넘어섰으며, OpenAI의 o1-mini와 Anthropic의 Claude 3.5 Sonnet은 모두 92.4%를 기록하여, 표준화된 과제에서 숙련된 개발자의 성과에 실질적으로 필적하게 되었습니다. 예전에는 두 자릿수의 오류율을 이유로 AI 생성 코드를 거부하던 기업들도, 현재는 수동으로 한 줄씩 검토하지 않고도 에이전트가 수행한 리팩토링을 수용하고 있습니다. Moonshot AI의 Kimi K2는 정확도 상한선을 94.5%까지 끌어올리며, 여전히 급격한 개선 추세를 보이고 있음을 입증했습니다. NatWest의 운영 데이터에 따르면, 정확도가 90%를 넘어서자 AI 코드 어시스턴트는 섀도 테스트 단계에서 본 생산 파이프라인으로 전환되었습니다. 정밀도가 향상됨에 따라, 여러 에이전트가 협력하여 리포지토리 전반에 걸쳐 코드 계획, 리팩토링, 컴파일을 수행하는 워크플로우도 가능해졌습니다. 다만, Anthropic의 2026년 조사에 따르면 엔지니어들이 업무의 0-20%만 완전히 위임하고 있는 것으로 나타나, 여전히 인간의 감독이 필요함을 시사하고 있습니다.

IDE 플러그인의 보급으로 인해 AI가 개발자의 일상 업무에 통합되고 있습니다.

AI 어시스턴트는 더 이상 독립된 사이드바가 아니라, Visual Studio Code나 JetBrains의 IDE 내에 기본 기능으로 통합되어 있습니다. Google Cloud의 Gemini Code Assist는 2025년 10월, 코드 검토 주기가 1일을 초과하는 팀의 60.2%를 대상으로 엔터프라이즈급 GitHub 통합 기능을 추가했습니다. VS Code의 AI 네이티브 포크인 Cursor는 2025년 중반까지 연간 반복 매출(ARR) 5억 달러에 도달할 것으로 예상되며, 여러 파일에 걸친 추론이 필수적인 경우 컨텍스트 인식형 AI 에디터가 플러그인 방식의 접근법을 능가한다는 사실을 입증했습니다. 마이크로소프트는 2026년 3월, Word, Excel, Outlook에 에이전트 기능을 탑재하며 본격적으로 나서면서, 생성형 코딩이 더 이상 개발자만의 전유물이 아님을 보여주었습니다. 개발자 1인당 트랜잭션 처리 시간을 40분 단축하고, 전체적으로는 50만 시간 이상을 절약한 것으로 나타났는데, 이는 플러그인의 보급을 통해 실제로 확보된 시간을 여실히 보여주고 있습니다.

지적재산권 및 저작권에 대한 책임 우려가 기업의 도입을 지연시키고 있습니다.

2025년에는 저작권 분쟁이 격화되면서, 보상 조항을 마련해야 하는 CIO들의 불확실성이 커졌습니다. 뉴욕 남부 연방지방법원 판사는 OpenAI를 상대로 한 집단소송의 진행을 허용하고, 실질적 유사성에 대한 주장에는 증거개시 절차가 필요하다고 판단했습니다. GitHub Copilot은 출처 표기를 삭제했다는 이유로 DMCA 위반 혐의로 제9순회항소법원에 항소되었습니다. 뉴스 코프가 Perplexity AI를 상대로 제기한 소송에서 검색 강화 생성(RAG) 기술이 유료 구독 장벽을 우회함으로써 출판사에 피해를 주고 있다고 주장하고 있습니다. 이처럼 주목을 끄는 소송들로 인해, 구매자들은 코드를 커밋하기 전에 라이선스 상의 충돌을 감지할 수 있는 중복 감지 툴를 도입할 수밖에 없게 되었습니다. EU AI법은 서비스 제공업체에 훈련 데이터 요약본을 공개하고 권리자의 불만 사항에 대응할 것을 의무화하고 있으며, 2026년 8월부터 시행됨에 따라 관련 리스크를 더욱 증대시키고 있습니다.

부문별 분석

인공지능(AI) 코드 툴 시장에서 클라우드 기반 분야가 총 매출의 72.47%를 차지했으며, 나머지는 온프레미스 배포가 차지했습니다. 은행, 의료 시스템, 국방 기관이 주권 관련 규정을 위반할 가능성이 있는 제3자에 의한 데이터 처리를 피하려는 경향이 있기 때문에 온프레미스형 솔루션은 연평균 성장률(CAGR) 26.55%로 성장할 전망입니다. Vault의 200대 서버 규모 인프라와 Anaconda의 Llama 2 미세 조정 키트는 자체 호스팅형 스택에 대한 수요가 증가하고 있음을 보여줍니다. EU AI법의 투명성 관련 제재 조항은 특히 코드 주석에 기밀성이 높은 개인 식별 정보가 포함된 경우, 모델을 기업의 방화벽 내부에 보관해야 한다는 주장을 더욱 강화시키고 있습니다.

클라우드 제공업체는 속도와 다양성 면에서 여전히 우위를 점하고 있습니다. 2026년 3월 Google Cloud가 출시한, 100만 토큰 규모의 윈도우를 갖춘 Gemini 3.1 Pro는 온프레미스 환경에서 재현하려면 막대한 비용이 소요되는 혁신의 한 예입니다. Microsoft의 Frontier Suite는 Anthropic과 OpenAI 모델 간에 프롬프트를 동적으로 라우팅하지만, 이 기능은 싱글 테넌트 클러스터에서는 구현하기 어렵습니다. 로드맵에서는 하이브리드 전략이 주류를 이루고 있으며, 기밀성이 높은 리포지토리는 온프레미스에 남겨두고 중요도가 낮은 작업에는 SaaS API를 활용함으로써, 기업은 규정 준수 프레임워크를 준수하면서도 기능을 최대한 활용할 수 있게 되었습니다. 그 결과, AI 코드 툴 시장은 클라우드 네이티브의 편의성과 온프레미스의 제어성이라는 양극화가 진행되고 있습니다.

2025년 매출 중 코드 자동 완성 기능이 38.19%를 차지했으나, 현재 가장 빠르게 성장하고 있는 분야는 보안 지원 분야로, 연평균 성장률(CAGR)은 26.83%에 달할 전망입니다. 자동 스캐너는 생성된 개요을 취약점 데이터베이스와 대조하여, 병합 전에 호환되지 않는 라이선스를 표시함으로써 감사 부담을 줄여줍니다. Anthropic사의 2026년 이용 데이터에 따르면, 개발자들은 에이전트형 세션의 42%에서 보안 검사를 수행하고 있으며, 이는 2025년 초의 18%에서 증가한 수치입니다. 이러한 가속화는 훈련 데이터 및 거버넌스 관리의 문서화를 의무화하는 EU 규정에 부합합니다.

문서 작성 봇이나 AI를 활용한 시험 문제 생성 툴도 그 직후에 이어지고 있습니다. 지속적 통합(CI) 파이프라인은 불안정한 테스트를 감지하고 커버리지 분석을 LLM에 맡김으로써 릴리스 주기를 두 자릿수 비율로 단축하고 있습니다. 코드 리뷰 봇 분야의 AI 코드 툴 시장 점유율은 여전히 견조한 모습을 보이고 있습니다. 이는 많은 팀이 AI를 자율적인 승인자가 아닌, 또 하나의 '눈'으로 여기고 있기 때문입니다. 컴플라이언스 자동화가 도입을 촉진함에 따라, 기능의 우선순위는 생산성에서 리스크 관리로 이동하고 있으며, 보안이 새로운 '킬러 기능'으로 자리 잡아가고 있습니다.

지역별 분석

북미는 2025년 매출의 41.89%를 차지했으며, 이는 하이퍼스케일러의 투자, 벤처 자금 조달의 활발함, 그리고 기업들의 조기 도입을 반영한 것입니다. 미국의 은행과 캐나다의 통신 사업자들은 프롬프트 라이브러리와 리스크 관리를 표준화하는 AI 거버넌스 부서를 구성하고, 챗봇을 안전한 소프트웨어 개발 라이프사이클에 깊이 통합하고 있습니다. 지적재산권 관련 소송은 여전히 지역적으로 불리한 여건을 보이고 있지만, 미국 법원에서는 법적 확실성을 더 신속하게 확보할 수 있는 경우가 많아, 선구자들의 시도를 뒷받침하고 있습니다.

유럽에서는 규제 체계를 준수하는 것을 중시하는 '컴플라이언스 퍼스트' 접근 방식에 따라 진전이 이루어지고 있습니다. 2025년 7월에 도입된 '범용 AI 행동 강령'은 저작권 준수 및 투명성 등 중요한 측면을 중심으로, 서비스 제공업체를 대상으로 일련의 자율적 점검 목록을 제공합니다. 이 이니셔티브는 2026년 8월 발효 예정인 EU AI법의 시행에 대비하기 위해 마련되었습니다. 이러한 규제 동향을 반영하여 은행과 보험사는 엄격한 데이터 상주 요건을 준수하기 위해 온프레미스형 클러스터 도입을 가속화하고 있습니다. 이러한 변화는 유럽 전역의 AI 코드 툴 시장 성장을 주도하는 한편, 변화하는 규제 환경에 대한 준수를 보장하기 위해 거버넌스 관련 기능에 대한 지출 우선순위를 재조정하고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 26.68%를 기록하며 두드러진 성장 동력으로 자리매김하고 있습니다. 알리바바의 Qwen과 같은 중국 공급업체들은 현재 미국 비용의 6분의 1 수준에 멀티모달 및 에이전트 지원 모델을 제공하고 있어, 인도 아웃소싱 업체와 동남아시아 스타트업들의 도입을 촉진하고 있습니다. 싱가포르와 한국에서는 정부의 지원금을 통해 중소기업을 대상으로 GPU 사용료를 면제해 주는 국내 액셀러레이터가 운영되고 있습니다. 가격 대비 성능의 우위 덕분에 지출은 비용 최적화된 스택으로 이동하고 있습니다. 한편, 영어 실력 향상으로 인해 대상 개발자의 기반은 확대되고 있습니다. 남미, 중동 및 아프리카는 AI 도입의 초기 단계에 있지만, 정부의 디지털 전환(DX) 추진 정책과 해외 지원 거점을 통해 AI 코딩 툴가 공공 조달 및 현지 기술 생태계에 도입되기 시작하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the artificial intelligence (AI) code tools market size is projected to be USD 7.37 billion in 2025, USD 9.35 billion in 2026, and reach USD 29.96 billion by 2031, growing at a CAGR of 26.23% from 2026 to 2031.

This report is Segmented by Deployment Mode (Cloud-Based, and More), Tool Functionality (Code Completion, Code Generation, Code Review and Optimization, and More), End-User Industry (IT and Telecom, BFSI, Healthcare and Life Sciences, Retail and E-Commerce, and More), Organization Size (Large Enterprises, and Small and Medium Enterprises), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global AI Code Tools Market Trends and Insights

Exploding LLM Accuracy Drives Enterprise Confidence in Code Generation

Foundation-model accuracy surged past 90% on HumanEval in 2025, with OpenAI's o1-mini and Anthropic's Claude 3.5 Sonnet both hitting 92.4%, effectively matching senior-developer performance on standardized tasks. Enterprises that once rejected AI-generated code at double-digit error rates now accept agentic refactors without manual, line-by-line review. Moonshot AI's Kimi K2 pushed the ceiling to 94.5%, proving the improvement arc is still steep. NatWest's operational data shows that once accuracy exceeded 90%, AI code assistants moved from shadow testing into production pipelines. Higher accuracy also unlocks multi-agent workflows in which models plan, refactor, and compile code across repositories, though Anthropic's 2026 survey notes that engineers delegate only 0-20% of tasks fully, signaling persistent human oversight.

IDE Plug-in Proliferation Embeds AI into Daily Developer Workflows

AI assistants are now native features inside Visual Studio Code and JetBrains IDEs rather than standalone sidebars. Google Cloud's Gemini Code Assist added enterprise-grade GitHub integrations in October 2025, targeting the 60.2% of teams whose code-review cycles exceed a day. Cursor, an AI-native fork of VS Code, reached USD 500 million ARR by mid-2025, proving that context-aware AI editors can outpace plug-in approaches when multi-file reasoning is essential. Microsoft doubled down in March 2026 by embedding agentic features across Word, Excel, and Outlook, signaling that generative coding is no longer a developer-only phenomenon. Citing 40 minutes saved per developer transaction and more than 500,000 hours saved overall, the move highlights the tangible hours freed by plug-in ubiquity.

IP and Copyright Liability Concerns Slow Enterprise Procurement

Copyright disputes intensified in 2025, creating uncertainty for CIOs drafting indemnity clauses. A Southern District of New York judge let class-action claims against OpenAI proceed, ruling that substantial-similarity arguments merited discovery. GitHub Copilot faces a Ninth Circuit appeal over alleged DMCA violations for stripping attribution. News Corp's suit against Perplexity AI claims retrieval-augmented generation harms publishers by bypassing paywalls. These high-profile cases push buyers to demand duplication-detection tools that flag license conflicts before committing code. The EU AI Act compounds risks by requiring providers to publish summaries of their training data and to handle rights-holder complaints, with enforcement starting in August 2026.

Other drivers and restraints analyzed in the detailed report include:

- Vendor-Bundled Cloud Credits and Free Tiers Expand Access

- 75% of Enterprise Developers to Use AI Assistants by 2028

- Model Hallucination and Security Vulnerabilities Constrain Production Deployment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The cloud-based slice of the Artificial Intelligence (AI) code tools market accounted for 72.47% of overall revenue, while on-premises deployments accounted for the balance. On-premises options are set to grow at a 26.55% CAGR as banks, health systems, and defense agencies shun third-party data processing that might breach sovereignty rules. Vault's 200-server footprint and Anaconda's Llama 2 fine-tuning kits exemplify the appetite for self-hosted stacks. The EU AI Act's transparency fines strengthen the case for keeping models behind corporate firewalls, especially where sensitive personally identifiable information appears in code comments.

Cloud providers retain an edge in speed and diversity. Google Cloud's March 2026 rollout of Gemini 3.1 Pro with a 1-million-token window illustrates innovations that would be costly to replicate on-site. Microsoft's Frontier Suite dynamically routes prompts among Anthropic and OpenAI models, a feature that single-tenant clusters struggle to match. Hybrid strategies dominate roadmaps, sensitive repositories remain on-premises while low-criticality tasks use SaaS APIs, enabling firms to maximize capabilities without breaching compliance guardrails. As a result, the AI code tools market continues to bifurcate into cloud-native convenience and on-premises control.

Code completion accounted for 38.19% of 2025 revenue, yet the security-assistant niche is now the fastest-growing at a 26.83% CAGR. Automated scanners cross-reference generated snippets against vulnerability databases and flag incompatible licenses before merge, easing audit fatigue. Anthropic's 2026 usage data shows that developers invoke security checks in 42% of agentic sessions, up from 18% in early 2025. This acceleration aligns with EU mandates that require documentation of training data and governance controls.

Documentation bots and AI-powered test generators follow close behind. Continuous-integration pipelines pass off flaky test detection and coverage analysis to LLMs, shortening release cycles by double-digit percentages. The AI code tools market share for code-review bots remains sticky because many teams treat AI as a second pair of eyes rather than an autonomous approver. As compliance automation drives adoption, the functionality hierarchy is shifting from productivity to risk management, cementing security as the new killer feature.

Geography Analysis

North America accounted for 41.89% of 2025 revenue, reflecting hyperscaler investments, venture funding density, and early enterprise adoption. US banks and Canadian telcos have institutionalized AI governance offices that standardize prompt libraries and risk controls, embedding assistants deeply into secure software development lifecycles. Intellectual property litigation remains a regional headwind, but legal certainty often arrives more quickly in US courts, encouraging first-mover experimentation.

Europe is progressing under a compliance-first approach, emphasizing adherence to regulatory frameworks. The General-Purpose AI Code of Practice, introduced in July 2025, offers providers a set of voluntary checklists focusing on critical aspects such as copyright compliance and transparency. This initiative is designed to prepare the region for the enforcement of the EU AI Act, which is scheduled to come into effect in August 2026. In response to these regulatory developments, banks and insurers are increasingly adopting on-premises clusters to comply with stringent data-residency requirements. This shift is driving growth in the AI code tools market across the continent, while also redirecting spending priorities toward governance-related features to ensure compliance with the evolving regulatory landscape.

Asia-Pacific is the standout growth engine, with a 26.68% CAGR. Chinese vendors like Alibaba's Qwen now offer multimodal, agent-ready models at one-sixth the US cost, unlocking adoption among Indian outsourcers and Southeast-Asian startups. Government grants in Singapore and South Korea fund in-country accelerators that waive GPU fees for SMEs. The price-performance edge tilts spending toward cost-optimized stacks, even as English-language proficiency broadens addressable developer bases. South America, the Middle East, and Africa sit at earlier stages of AI adoption, but government digital-transformation agendas and offshore support hubs are beginning to pull AI code tools into public tenders and local tech ecosystems.

- GitHub, Inc.

- Amazon.com, Inc. (Amazon Web Services, Inc.)

- Google LLC

- Microsoft Corporation

- International Business Machines Corporation

- JetBrains s.r.o.

- Tabnine Ltd.

- Sourcegraph, Inc.

- OpenAI OpCo, LLC

- Anthropic PBC

- Meta Platforms, Inc.

- DeepSeek Inc.

- Alibaba Cloud Computing Co., Ltd.

- Tencent Cloud Computing (Beijing) Co., Ltd.

- Replit, Inc.

- Anysphere, Inc.

- Magic AI, Inc.

- Qodo, Inc.

- Phind, Inc.

- salesforce.com, inc.

- Harness Inc.

- CodeRabbit, Inc.

- Cohere Inc.

- BigCode Project (Software Heritage and Hugging Face)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Exploding LLM Accuracy (>90% HumanEval)

- 4.2.2 Soaring IDE Plug-in Adoption (VS Code, JetBrains)

- 4.2.3 Vendor-Bundled Cloud Credits and Free Tiers

- 4.2.4 75% of Enterprise Developers to Use AI Assistants by 2028

- 4.2.5 Shift to Private or Local Models for IP Control

- 4.2.6 Edge-Optimized LLMs Reducing Latency for AR, VR Coding

- 4.3 Market Restraints

- 4.3.1 IP and Copyright Liability Concerns

- 4.3.2 Model Hallucination and Security-Bug Risk

- 4.3.3 Rising GPU or ASIC Shortages for On-Prem Clusters

- 4.3.4 Developer-Skill Erosion (Prompt-Engineer Paradox)

- 4.4 Industry Value-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Technological Outlook

- 4.7 Regulatory Landscape

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-Based

- 5.1.2 On-Premises

- 5.2 By Tool Functionality

- 5.2.1 Code Completion

- 5.2.2 Code Generation

- 5.2.3 Code Review and Optimization

- 5.2.4 Automated Testing

- 5.2.5 Security and Compliance Assistants

- 5.2.6 Documentation and Commenting

- 5.3 By End-User Industry

- 5.3.1 IT and Telecom

- 5.3.2 BFSI

- 5.3.3 Healthcare and Life Sciences

- 5.3.4 Retail and E-Commerce

- 5.3.5 Media and Entertainment

- 5.3.6 Government and Public Sector

- 5.3.7 Others End-User Industry

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 GitHub, Inc.

- 6.4.2 Amazon.com, Inc. (Amazon Web Services, Inc.)

- 6.4.3 Google LLC

- 6.4.4 Microsoft Corporation

- 6.4.5 International Business Machines Corporation

- 6.4.6 JetBrains s.r.o.

- 6.4.7 Tabnine Ltd.

- 6.4.8 Sourcegraph, Inc.

- 6.4.9 OpenAI OpCo, LLC

- 6.4.10 Anthropic PBC

- 6.4.11 Meta Platforms, Inc.

- 6.4.12 DeepSeek Inc.

- 6.4.13 Alibaba Cloud Computing Co., Ltd.

- 6.4.14 Tencent Cloud Computing (Beijing) Co., Ltd.

- 6.4.15 Replit, Inc.

- 6.4.16 Anysphere, Inc.

- 6.4.17 Magic AI, Inc.

- 6.4.18 Qodo, Inc.

- 6.4.19 Phind, Inc.

- 6.4.20 salesforce.com, inc.

- 6.4.21 Harness Inc.

- 6.4.22 CodeRabbit, Inc.

- 6.4.23 Cohere Inc.

- 6.4.24 BigCode Project (Software Heritage and Hugging Face)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment