|

시장보고서

상품코드

2062441

유체 센서 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Fluid Sensor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

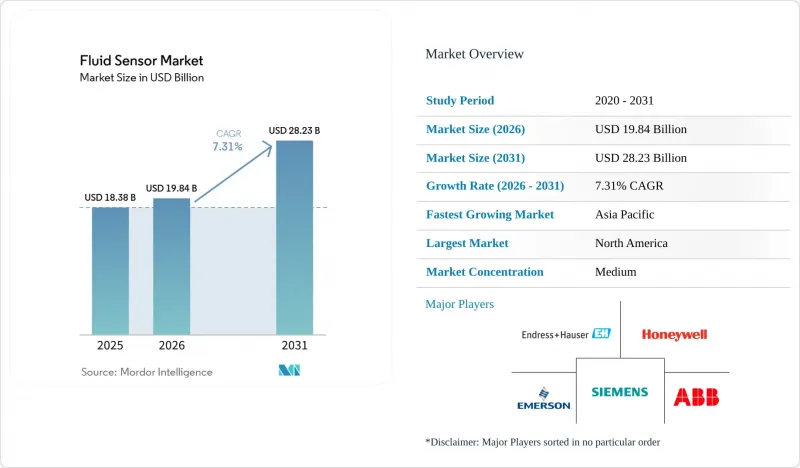

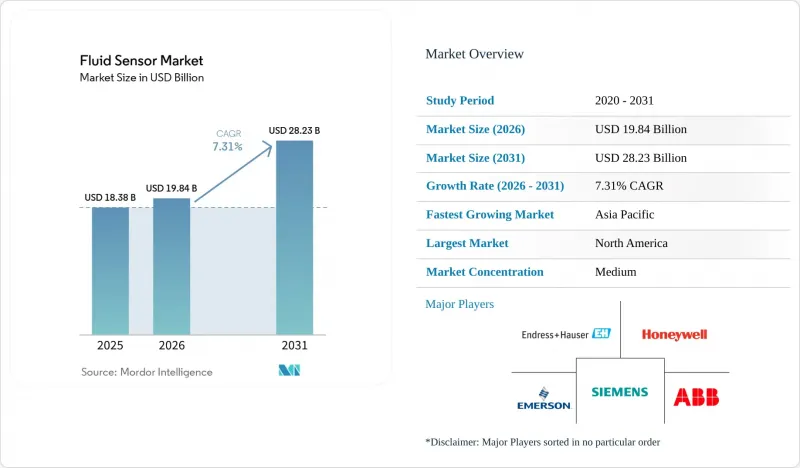

Mordor Intelligence에 의하면, 유체 센서 시장 규모는 2025년 183억 8,000만 달러로 평가되었습니다. 2026년 198억 4,000만 달러에서 2031년까지 282억 3,000만 달러로 확대되고 2026년부터 2031년에 걸쳐 CAGR은 7.31%를 나타낼 것으로 예측됩니다.

본 보고서는 센서 유형(압력 센서, 유량 센서 등), 감지 매체(액체, 기체), 측정 원리(접촉식, 비접촉식), 최종 사용 산업(석유 및 가스, 상하수도, 화학제품 및 석유화학제품, 식품 및 음료, 의약품·생명공학, 발전 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 유체 센서 시장 동향과 인사이트

IIoT를 통한 실시간 모니터링에 대한 수요

지속적인 원격 측정 기술이 정기적인 수동 순찰을 대체함으로써, 이상 감지 시간을 몇 시간에서 몇 초로 단축하고 있습니다. 2025년 인도에서 진행된 12대의 CNC 공작기계 개조 프로젝트에서는 저비용 마이크로컨트롤러와 데이터를 전송하는 압력·유량 프로브를 결합함으로써 예기치 못한 가동 중지 시간을 95% 줄였으며, 3개월도 채 되지 않아 투자 비용을 회수했습니다. 이러한 시계열 데이터 스트림을 기반으로 구축된 예측 모델은 현재 펌프 씰의 고장을 최대 2주 전에 예측하고 있으며, 공정 플랜트에 건당 5만-20만 달러의 비용이 드는 긴급 정지를 방지하고 있습니다. LoRaWAN 및 셀룰러 협대역 IoT를 통해 통신 범위가 외딴 지역의 우물 부지까지 확대되고 있습니다. 4G 게이트웨이 1대로 50-100대의 기기를 통합할 수 있으며, 노드당 연간 통신 비용은 200-800달러입니다. 요코가와 전기 등공급업체는 분산된 자산에 SCADA 수준의 가시화 기능을 적용함으로써, 노후화를 조기에 감지하고 생산에 차질이 생기기 전에 예비 부품을 배치할 수 있도록 하고 있습니다.

엄격한 물 및 폐수 규제

미국 환경보호청(EPA)은 현재 퍼플루오로알킬 물질(PFAS) 및 폴리플루오로알킬 물질(PFAS)의 농도를 2-5 ng/L로 제한하고 있으며, 이로 인해 상수도 유틸리티자들은 실험실 등급의 크로마토그래피 장비나 고해상도 센서를 도입할 수밖에 없는 실정입니다. 또한, 2027년까지 단계적으로 시행될 예정인 유사한 규정이 라인 지침을 통해 부과되고 있어, 기존 수처리 시설의 경우, 흩어진 시료 채취 방식에서 pH, 탁도, 용존산소의 연속 원격 측정 방식으로의 전환이 시급히 요구되고 있습니다. 나노 소재 기반의 전기화학 프로브와 머신러닝 필터를 결합함으로써, 기존 셀에서는 IEC.CH가 포화 상태에 이르렀던 탁한 매트릭스에서도 ppb 미만의 농도를 측정할 수 있게 되었습니다. 소규모 지방 상수도 시스템은 대규모 상수도 유틸리티자에 비해 1인당 설비 비용이 3-5배 높기 때문에 현장에서 유지보수가 가능한 유닛이나 사용량 기반 클라우드 분석을 선호하는 저비용 부문이 호황을 누리고 있습니다.

첨단 센서의 높은 초기 비용

ATEX 및 IECEx 인증을 획득한 위험 지역용 압력 트랜스미터는 표준 유닛보다 비용이 3배 더 들 수 있습니다. 또한, 가격이 1만 달러를 넘는 레이저 레벨미터는 3,000달러 전후의 초음파식 대체 제품을 훨씬 능가합니다. 통합, 보정, 클라우드 호스팅, 유지보수를 포함하면 총 소유 비용이 크게 증가합니다. 인도에서 IoT 기기 10대를 도입하는 데는 평균 80만 루피(9,600 달러)가 소요되며, 연간 최대 1만 5,000 달러의 지속적인 클라우드 이용료가 발생합니다. ROI가 2년을 초과할 경우, 중소기업은 자금 면에서 제약을 받게 됩니다. 대량 주문으로 인해 단가는 최대 40%까지 절감되지만, 분산된 최종 사용자의 경우 팔레트 단위의 주문 기준량에 도달하는 경우는 드뭅니다.

부문별 분석

2025년 매출액 기준으로 유량 센서가 유체 센서 시장 점유율의 38.68%를 차지하며 1위를 차지했습니다. 이는 계량 거래 및 에너지 균형 조정 분야에서 유량 센서의 보급 현황을 뒷받침하는 것입니다. 그럼에도 불구하고, 레이더식 및 초음파식 레벨 센서는 주요 카테고리 중 가장 높은 연평균 성장률(CAGR) 8.11%를 나타낼 것으로 전망됩니다. 이러한 추세는 비접촉식 설계 덕분에 플로트식 센서의 고질적인 문제인 마모와 오염을 피할 수 있어, 결과적으로 유지보수 비용을 절감할 수 있기 때문입니다. WIKA가 2026년 3월에 출시한 소형 레이더식 레벨 센서는 공간이 제한된 제약용 용기를 대상으로 하는 반면, OndoSense의 70미터 대응 솔루션은 광업용 사일로로의 적용 범위를 확대되고 있습니다. 압력 프로브는 현재 6,000바의 정격이 일반화된 유정 입구 및 수소 용도 분야에서 여전히 필수적입니다. 이러한 센서에 디지털 온도 소자를 결합함으로써 밀도 보정이 가능해지며, 다중 파라미터 측정의 정확도가 향상됩니다.

예측 기간 동안 전체 수명 주기 비용을 산정해 보면, 비접촉 방식의 도입이 가속화될 것입니다. 액체와 접촉하는 프로브를 분기마다 교정하는 작업은 많은 노력이 필요하고 오염 위험을 초래하기 때문에 무균 제조 과정에서 과제로 대두되고 있습니다. 레이더식 유닛은 유지보수 빈도를 연 1회로 줄여주며, 초기 비용은 높지만 운영 비용을 절감합니다. 안전 기준 또한 상황을 완전히 바꿔놓고 있습니다. IEC 61511을 준수하는 오버필 시스템에서는 SIL 인증을 받은 레이더 장치가 점점 더 많이 지정되고 있습니다. 따라서 각 공급업체들은 침전물 축적을 감지하고, 장비 상태를 확인하며, 내압 시험 데이터를 자산 관리 시스템으로 전송하는 자가 진단 기능을 강조하고 있습니다. 이를 통해 운영자는 침습적인 점검을 실시하지 않아도 규정 준수 여부를 입증할 수 있게 됩니다.

2025년 매출액 중 액체 계측 부문은 여전히 64.24%를 차지하며, 물, 연료, 용제 등을 포함했습니다. 한편, 정부의 대기 오염 물질 규제 강화에 따라 가스 감지 시장은 연평균 성장률(CAGR) 8.05%를 기록하며 더욱 빠르게 성장하고 있습니다. 하네웰의 4 시리즈 비분산형 적외선 모듈은 교정 주기를 2배로 연장하여 정유시설의 고정식 안전 시스템 총 비용을 절감합니다. 에머슨의 QX1000 연속 분석기는 배기가스 내의 SO₂, NOx, CO를 ppb 수준으로 검출하여, 점점 더 엄격해지는 발전소 배출 허가 기준을 충족합니다. 상업용 건물에서는 개정된 국제 기계 규정(IMC)에 따라 주차장에 일산화탄소 및 이산화질소 감지기를 설치해야 합니다.

그럼에도 불구하고, 액체 계량 분야에서는 코리올리식 및 초음파식 유량계가 ±0.1%의 정확도를 실현함으로써, 석유 계량 거래와 같은 고수익 분야의 기반이 되고 있습니다. 제약용 바이오리액터에서는 무균 상태를 유지하기 위해 일회용 pH, 전도도, 용존산소 프로브가 사용되고 있습니다. 한편, 수소 인프라 분야에서는 티타늄이나 금 도금 등 취화에 강한 소재가 틈새 시장을 형성하고 있습니다. 이 제품들은 스테인리스 모델보다 30-50% 비싸지만, 고압 수소 환경에서 미세한 균열이 발생하는 것을 방지할 수 있습니다. 규제상의 차이로 인해 공급업체의 로드맵이 복잡해지고 있으며, 장비는 전 세계적으로 ATEX 및 IECEx 인증을 취득한 데 이어 북미 시장용으로는 UL 또는 CSA 인증도 추가로 취득해야 하므로, 이로 인해 시험 주기가 길어지고 비용도 증가합니다.

지역별 분석

아시아태평양은 2025년에 전 세계 매출의 36.82%를 차지했으며, 연평균 성장률(CAGR) 7.83%를 나타낼 것으로 전망됩니다. 중국의 벙부(蚌埠) 센서 밸리는 8인치 MEMS 생산 라인을 기반으로, 2027년까지 생산액 300억 위안(41억 달러)을 달성하는 것을 목표로 하고 있습니다. 인도의 ‘센서 우수 센터(Sensor Centre of Excellence)’는 자동차 및 IoT 프로그램을 원동력으로 삼아, 2027년까지 국내 시장 규모가 31,000 카롤 루피(37억 달러)에 달할 것으로 전망하고 있습니다. 일본과 한국은 극자외선(EUV) 리소그래피의 장벽을 극복하기 위해 칩렛 아키텍처에 보조금을 지원하고 있는 반면, 호주는 외딴 지역의 광산에 무선 프로브를 도입하고 있습니다.

2025년 매출의 약 절반은 북미와 유럽이 차지했습니다. 2024년 말, 미국의 중국산 반도체에 대한 제301조 관세가 50%로 두 배로 인상됨에 따라 부품 원가가 15-30% 상승했고, 이에 OEM 각사는 멕시코, 베트남, 동유럽으로 조립 생산을 전환했습니다. 엔드리스 하우저사가 인디애나주 그린우드에 건설한 5,090만 달러 규모의 공장은 2025년 중반부터 출하를 시작했으며, 리드타임을 6주로 단축했습니다. ‘유럽 그린딜’은 재생에너지와 탄소 포집에 대한 자금 배분을 촉진하고 있으며, ST마이크로일렉트로닉스는 아그라테 공장의 생산 능력을 주당 4,000 웨이퍼로 확대하고 있으며, 온세미는 체코에 19억 1,000만 달러 규모의 실리콘 카바이드 제조 거점을 건설하고 있습니다.

남미, 중동 및 아프리카는 규모는 작지만 특정 분야에서 유망한 기회를 제공합니다. 브라질과 아르헨티나에서는 도시 지역의 수처리 시설이 현대화되면서, 농약과 중금속을 감지하는 분석용 센서에 대한 수요가 증가하고 있습니다. 중동의 사업자들은 사워 가스전 및 수소 파이프라인용으로 ATEX 인증 프로브를 지정하고 있으며, 사우디아라비아의 해수 담수화 플랜트에서는 내식성 수준 및 유량 측정 장치가 채택되고 있습니다. 아프리카에서는 남아프리카공화국의 광산에서 심부 갱도에 진동 발전 방식의 무선 노드가 도입되고 있는 반면, 나이지리아의 파이프라인에서는 통신 인프라가 제한적임에도 불구하고 누출 감지 시스템이 추가되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the fluid sensor market size is projected to expand from USD 18.38 billion in 2025 and USD 19.84 billion in 2026 to USD 28.23 billion by 2031, registering a CAGR of 7.31% between 2026 and 2031.

This report is Segmented by Sensor Type (Pressure Sensors, Flow Sensors, and More), Detection Medium (Liquid, and Gas), Measurement Principle (Contact, and Non-Contact), End-Use Industry (Oil and Gas, Water and Wastewater, Chemicals and Petrochemicals, Food and Beverage, Pharmaceuticals and Biotechnology, Power Generation, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Fluid Sensor Market Trends and Insights

IIoT-Driven Demand for Real-Time Monitoring

Continuous telemetry is replacing periodic manual rounds, cutting anomaly-detection time from hours to seconds. A 2025 retrofit on twelve CNC machines in India trimmed unplanned downtime by 95% and paid back in under three months by pairing low-cost microcontrollers with pressure and flow probes that publish data over. Predictive models built on these time-series streams now forecast pump seal failures up to two weeks in advance, averting emergency shutdowns that cost process plants USD 50,000-200,000 per event. LoRaWAN and cellular narrowband IoT extend coverage to remote well sites, with a single 4G gateway aggregating 50-100 devices at annual connectivity costs of USD 200-800 per node. Vendors such as Yokogawa overlay SCADA-grade visualizations atop distributed assets, surfacing degradation early and enabling spare-part staging before production is threatened.

Stringent Water and Wastewater Regulations

The United States Environmental Protection Agency now caps per- and polyfluoroalkyl substances at 2-5 ng/L, forcing utilities to adopt lab-grade chromatography and high-resolution sensors on line directives impose similar rules with phased enforcement through 2027, pressuring legacy plants to move from grab sampling to continuous pH, turbidity, and dissolved-oxygen telemetry.Nanomaterial-based electrochemical probes combined with machine-learning filters resolve sub-ppb concentrations in turbid matrices where older cells saturated IEC.CH. Smaller rural systems face 3-5 times higher per-capita capital cost than large utilities, energizing a low-cost segment that favors field-serviceable units and pay-as-you-go cloud analytics.

High Upfront Cost of Advanced Sensors

Hazardous-area pressure transmitters certified to ATEX and IECEx can cost triple a standard unit, while laser level meters priced above USD 10,000 dwarf ultrasonic alternatives that sit near USD 3,000. Total cost of ownership balloons once integration, calibration, cloud hosting, and maintenance are included; a 10-machine IoT roll-out in India averages INR 800,000 (USD 9,600) with recurring cloud fees up to USD 15,000 per year. SMEs grapple with capital constraints when ROI stretches past two years. Volume orders cut unit pricing by up to 40%, but dispersed end users rarely hit pallet-scale thresholds.

Other drivers and restraints analyzed in the detailed report include:

- Pipeline Integrity Mandates in Oil and Gas

- Process-Industry Need for Hygienic Sensors

- Accuracy Drift Under Extreme Conditions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flow sensors led 2025 revenue with 38.68% of the fluid sensor market share, underscoring their ubiquity in custody transfer and energy balancing. Nonetheless, radar and ultrasonic level sensors are forecast to post an 8.11% CAGR, the fastest among major categories. This momentum stems from maintenance avoidance, as non-contact designs sidestep wear and fouling that plague floats. WIKA's compact radar launch in March 2026 targets cramped pharmaceutical vessels, while OndoSense's 70-meter solution broadens reach to mining silos. Pressure probes remain essential in wellhead and hydrogen applications where 6,000-bar ratings are now routine. Bundling digital temperature elements with these sensors enables density compensation, advancing multiparameter accuracy.

Across the forecast horizon, non-contact adoption accelerates once the total lifecycle cost is tallied. Quarterly calibrations on wetted probes consume labor and pose contamination risk, a pain point for sterile manufacturing. Radar units slash maintenance visits to an annual cadence, trimming operating expenditure despite a higher upfront ticket. Safety standards also tilt the table; IEC 61511-compliant overfill systems increasingly specify SIL-rated radar devices. Vendors thus emphasize self-diagnostics that flag buildup, verify health, and feed proof-test data to asset management suites, helping operators demonstrate compliance without intrusive checks.

Liquid measurement still accounts for 64.24% of 2025 sales, covering water, fuels, and solvents, while gas sensing is growing faster at an 8.05% CAGR as governments crack down on air pollutants. Honeywell's 4-Series nondispersive infrared module doubles calibration intervals, lowering total cost for fixed safety systems in refineries. Emerson's QX1000 continuous analyzer brings ppb detection to SO2, NOx, and CO stacks, aligning with tightening power-plant permits. In commercial buildings, updated International Mechanical Code rules require carbon monoxide and nitrogen dioxide detectors in parking garages.

Liquid lines nonetheless anchor high-revenue verticals such as fiscal oil custody transfer, where Coriolis and ultrasonic meters deliver +-0.1% accuracy. Pharmaceutical bioreactors rely on single-use pH, conductivity, and dissolved-oxygen probes to maintain sterility. Meanwhile, hydrogen infrastructure creates a niche for embrittlement-resistant elements, such as titanium or gold plating. These units are priced 30-50% above stainless versions but avoid micro-cracking under high-pressure H2 service. Regulatory divergence complicates vendor roadmaps, devices must clear ATEX and IECEx globally, then layer UL or CSA for North America, which extends test cycles and costs.

Geography Analysis

Asia-Pacific accounted for 36.82% of global revenue in 2025 and is forecast to expand at a 7.83% CAGR. China's Bengbu Sensor Valley aims to reach CNY 30 billion (USD 4.1 billion) in output by 2027, backed by an 8-inch MEMS line. India's Sensor Center of Excellence projects a domestic market of INR 31,000 crore (USD 3.7 billion) by 2027, fueled by automotive and IoT programs. Japan and South Korea channel subsidies into chiplet architectures to sidestep barriers to extreme-ultraviolet lithography, while Australia deploys wireless probes across remote mines.

North America and Europe together accounted for roughly half of the 2025 turnover. United States Section 301 tariffs that doubled to 50% on Chinese semiconductors in late 2024 inflated bill-of-material costs 15-30%, prodding OEMs toward Mexican, Vietnamese, and Eastern European assembly. Endress and Hauser's USD 50.9 million Greenwood, Indiana, plant began shipping in mid-2025, shrinking lead times to six weeks. The European Green Deal steers funding toward renewables and carbon capture, with STMicroelectronics scaling its Agrate fab to 4,000 wafers per week and onsemi building a USD 1.91 billion silicon-carbide site in the Czech Republic.

South America, the Middle East, and Africa, though smaller, present focused opportunities. Brazil and Argentina upgrade municipal water treatment, demanding analytical sensors that sniff pesticides and heavy metals. Middle Eastern operators specify ATEX-rated probes for sour-gas fields and hydrogen pipelines, while desalination plants in Saudi Arabia adopt corrosion-resistant level and flow devices. In Africa, South African mines deploy vibration-powered wireless nodes in deep shafts, whereas Nigerian pipelines add leak-detection strings despite limited telecoms backbones.

- Honeywell International Inc.

- Siemens AG

- Emerson Electric Co.

- ABB Ltd

- Endress+Hauser Group

- Schneider Electric SE

- Yokogawa Electric Corp.

- Flowserve Corp.

- Xylem Inc.

- Danfoss A/S

- Keyence Corporation

- Sick AG

- TE Connectivity

- First Sensor AG

- Parker Hannifin Corp.

- Gems Sensors and Controls

- Bosch Sensortec GmbH

- Badger Meter Inc.

- Dwyer Instruments

- Omega Engineering

- Sensirion AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 IIoT-driven demand for real-time monitoring

- 4.2.2 Stringent water and wastewater regulations

- 4.2.3 Pipeline integrity mandates in oil and gas

- 4.2.4 Process-industry need for hygienic sensors

- 4.2.5 AI-enabled self-calibrating sensors

- 4.2.6 Micro-fluidic lab-on-chip diagnostics

- 4.3 Market Restraints

- 4.3.1 High upfront cost of advanced sensors

- 4.3.2 Accuracy drift under extreme conditions

- 4.3.3 Tariff-driven silicon wafer shortages

- 4.3.4 Cyber-security risks in wireless devices

- 4.4 Industry Ecosystem Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Sensor Type

- 5.1.1 Pressure Sensors

- 5.1.2 Flow Sensors

- 5.1.3 Level Sensors

- 5.1.4 Temperature and Others

- 5.2 By Detection Medium

- 5.2.1 Liquid

- 5.2.2 Gas

- 5.3 By Measurement Principle

- 5.3.1 Contact

- 5.3.2 Non-contact

- 5.4 By End-use Industry

- 5.4.1 Oil and Gas

- 5.4.2 Water and Wastewater

- 5.4.3 Chemicals and Petrochemicals

- 5.4.4 Food and Beverage

- 5.4.5 Pharmaceuticals and Biotechnology

- 5.4.6 Automotive and Transportation

- 5.4.7 Power Generation

- 5.4.8 Other End-Use Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Honeywell International Inc.

- 6.4.2 Siemens AG

- 6.4.3 Emerson Electric Co.

- 6.4.4 ABB Ltd

- 6.4.5 Endress+Hauser Group

- 6.4.6 Schneider Electric SE

- 6.4.7 Yokogawa Electric Corp.

- 6.4.8 Flowserve Corp.

- 6.4.9 Xylem Inc.

- 6.4.10 Danfoss A/S

- 6.4.11 Keyence Corporation

- 6.4.12 Sick AG

- 6.4.13 TE Connectivity

- 6.4.14 First Sensor AG

- 6.4.15 Parker Hannifin Corp.

- 6.4.16 Gems Sensors and Controls

- 6.4.17 Bosch Sensortec GmbH

- 6.4.18 Badger Meter Inc.

- 6.4.19 Dwyer Instruments

- 6.4.20 Omega Engineering

- 6.4.21 Sensirion AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment