|

시장보고서

상품코드

2062442

항공 클라우드 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Aviation Cloud - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

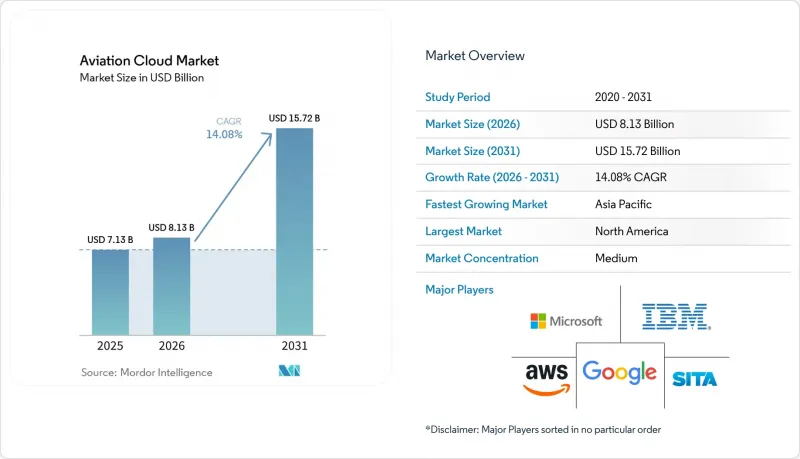

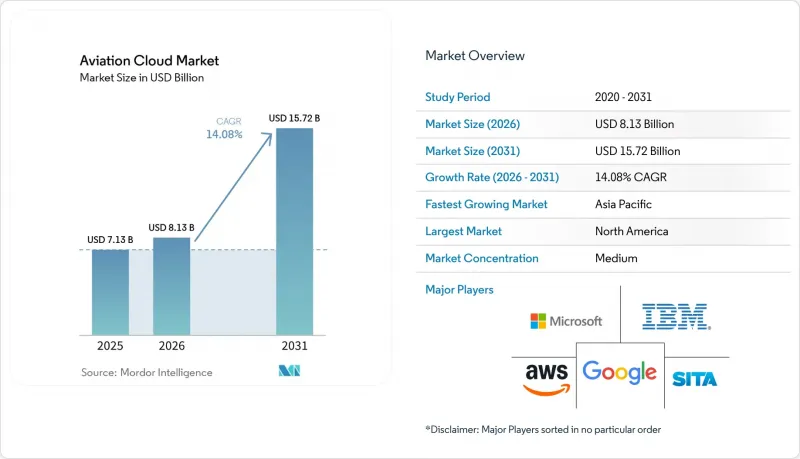

Mordor Intelligence에 의하면, 항공 클라우드 시장 규모는 2025년 71억 3,000만 달러로 평가되었고, 2026년에는 81억 3,000만 달러로 추정되고, 2026-2031년 CAGR 14.08%로 성장을 지속할 전망이며, 2031년까지 157억 2,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 도입 모델별(퍼블릭 클라우드, 프라이빗 클라우드, 하이브리드 클라우드, 커뮤니티 클라우드), 서비스 모델별(IaaS, PaaS, SaaS, FaaS), 용도별(운항 업무, 여객 서비스 등), 최종 사용자별(항공사, 공항, MRO 제공업체, ANS, OEM, 규제 당국 등), 지역별(북미, 아시아태평양 등)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

세계의 항공 클라우드 시장 동향 및 인사이트

항공사의 디지털 전환 예산이 폭발적으로 증가

각 항공사는 승객 경험의 혁신과 운항 회복탄력성을 가속화하기 위한 클라우드 플랫폼에 신조기 프로그램 자금을 재배정하고 있습니다. 이러한 변화는 SITA가 발표한 2025년 IT 지출액 508억 달러라는 수치에서도 드러나며, 클라우드 전환의 성장률은 다른 어떤 분야보다 가파르게 나타났습니다. 구체적인 예로, 버진 애틀랜틱 항공이 2026년에 시작할 예정인 위성 통신을 활용한 스트리밍 서비스를 들 수 있습니다. 이는 실시간 로열티 정보 업데이트에 클라우드 백엔드를 활용하는 것입니다. 또한, 동남아시아의 여러 저비용 항공사에서는 완전히 서버리스 방식의 예약 시스템을 운영하고 있습니다. 각 항공사가 리스 부담이 큰 데이터센터를 폐지하고 IT 부서 인력을 감축함에 따라 투자 회수 기간이 단축되었으며, 항공 클라우드 시장은 항공사의 디지털 전략의 핵심 축으로 자리 잡고 있습니다.

실시간 항공편 데이터 분석에 대한 수요 증가

이벤트 주도형 플랫폼은 현재 난기류 보고, 기체 상태 모니터링 텔레메트리, 레이더 플롯을 수 초 이내에 처리하여 연료비 및 유지보수 비용을 절감하고 있습니다. 루프트한자의 'Turbulence Aware' 도입과 제트블루의 에어버스 'Skywise'와의 예측 유지보수 연계는 모두 2025년에 실시간 센서 데이터를 1초 미만의 운영 판단으로 전환했습니다. EUROCONTROL의 2025년 개념 검증(PoC)은 이 모델을 항공 교통 관제 서비스 제공업체로까지 확대하고 있으며, 실시간 처리가 항공 클라우드 업계 전반에 걸쳐 필수 요소로 자리 잡고 있음을 보여줍니다.

사이버 주권과 데이터 소재지 규제의 준수 비용

법규의 파편화로 인해 항공사들은 여러 관할 구역에 걸쳐 인프라를 중복 구축할 수밖에 없게 되었으며, 그 결과 자본 수요는 단일 지역 내 구축에 비해 15-25% 증가했습니다. 유럽연합(EU)의 2025년 프레임워크에서는 승객 명단(PNR)의 국내 처리가 의무화되어 있으나, 카타르항공은 2026년 각국의 규제를 충족하기 위해 프라이빗 클라우드 모델을 선택했습니다. 중국과 인도에서 발생하는 유사한 제약으로 인해, 항공사들은 별도의 데이터 레이크와 감사 추적을 유지할 수밖에 없으며, 전 세계 네트워크 전반에 걸친 통일된 거버넌스 구축이 과제로 대두되고 있습니다.

부문별 분석

하이브리드 클라우드는 2031년까지 연평균 16.9%의 성장률을 보일 것으로 예상되며, 이는 하이퍼스케일러의 확장성을 희생하지 않으면서도 데이터에 대한 주권적 통제를 원하는 항공사들 수요를 반영한 것입니다. 델타항공은 승객 정보를 프라이빗 노드에 저장하는 한편, 수요 예측 모델 훈련을 퍼블릭 GPU에서 수행하고 있으며, 이는 항공 클라우드 시장을 주도하는 2층 구조의 패턴을 보여줍니다. 예약이나 승무원 스케줄링과 같은 멀티테넌트형 SaaS의 경우 여전히 퍼블릭 클라우드 도입이 선호되지만, 명확한 국가 지침에 구속되는 국적 항공사들 사이에서는 프라이빗 클라우드 사용이 계속되고 있습니다. 커뮤니티 클라우드는 규모는 작지만, 지역 연합이 공동 거버넌스 하에서 슬롯 및 정비 데이터를 공유할 수 있도록 함으로써 일방적인 정보 공개를 방지하고 있습니다.

선도적인 도입 사례에서는 현재 프라이빗 인스턴스와 공항 내 에지 존을 상호 연결하여, 승객 흐름, 수하물 추적, 생체 인증을 통한 탑승 수속 과정에서 발생하는 지연을 최소화하고 있습니다. 이러한 구조를 통해 항공사는 기밀성이 높은 비행 계획에 대한 규정 준수를 로컬에서 관리하는 동시에, 내결함성이 뛰어난 퍼블릭 클러스터에서 대량의 분석 작업을 실행할 수 있게 됩니다. 규제 당국이 클라우드 감사 기준을 명확히 함에 따라, 항공사들은 항공 클라우드 시장 전망 성장을 뒷받침할 하이브리드 모델을 포기하기보다는 워크로드 배치 정책을 더욱 정교하게 다듬어 나갈 것으로 예측됩니다.

Platform-as-a-Service(PaaS)는 차별화가 어려운 번거로운 작업을 대신 처리해 주는 관리형 데이터 레이크 및 이벤트 스트리밍 엔진을 제공함으로써, 15.7%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 2025년까지 200개 항공사에 서비스를 제공할 예정인 Airbus Skywise는 항공사가 운항, 정비, 기상 데이터를 공유 데이터 레이크에 업로드하여, 별도의 서버 프로비저닝 없이 자체 신뢰성 모델을 실행할 수 있도록 지원합니다. SaaS는 메인프레임에서 멀티테넌트형 클라우드로 이전된 여객 서비스, 출발 관리, 수익 관리 제품군의 성장에 힘입어 2025년 매출의 41.5%를 차지한 것으로 평가되었습니다. 항공사가 모놀리식 코드를 단계적으로 리팩토링할 때, 컴퓨팅 리소스를 프로비저닝하기 위해 IaaS(Infrastructure as a Service)는 이 두 계층 모두의 기반이 됩니다.

Function-as-a-Service(FaaS)는 아직 틈새 시장 수준이지만, 경쟁사가 가격을 인하했을 때의 자동 운임 변경이나 기상 악화 시의 자동 재예약 로직과 같이 특정 트리거에 대응하는 형태로 점차 주목받고 있습니다. 이 실행 단위 과금 모델은 자원 유휴화를 방지할 수 있어, 불규칙한 운항 환경에서 매력적입니다. 항공사가 기술적 과제를 가장 비용 효율적인 추상화 계층과 결합함으로써, 이러한 서비스 모델의 시너지 효과가 항공 클라우드 시장의 성장을 뒷받침하고 있습니다.

지역별 분석

2025년 매출의 36.3%를 차지한 북미 시장은 미국 연방항공청(FAA)의 클라우드 네이티브 항공 교통 시스템에 대한 조기 승인 및 항공사들의 다년간에 걸친 전환 프로그램의 혜택을 받고 있습니다. 델타 항공, 유나이티드 항공, 아메리칸 항공은 온프레미스 페일오버 기능을 유지하면서 휴가철 성수기에 컴퓨팅 리소스를 확장할 수 있는 하이브리드 아키텍처를 활용하고 있습니다. 캐나다의 NAV CANADA 역시 마찬가지로, 비행 데이터 처리를 하이브리드 Azure 스택으로 이전하고 있으며, 이는 규제 당국이 관리형 퍼블릭 플랫폼에 신뢰를 두고 있음을 보여줍니다. 멕시코의 공항 운영사는 대기열 분석 SaaS를 도입하여, 지역적인 파급 효과가 나타나고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 15.1%를 기록할 전망이며, 항공 클라우드 시장 규모에서 가장 큰 절대적 증가를 이끌 것으로 예측됩니다. 인도의 'Digi Yatra'나 중국이 모든 신규 공항에 클라우드 리소스 시스템 도입을 의무화한 것은 3급 공항에서도 도입을 가속화하고 있습니다. 인도네시아, 일본, 호주의 항공사들은 정비, 재고 관리, 승객 경험과 관련된 업무 부하를 클라우드로 이전하고 있으며, 많은 경우 기존의 데이터센터 단계를 완전히 건너뛰고 있습니다. 싱가포르 항공의 대륙 간 노선에서 위성 통신 연결이 이루어지고 있는 것은 클라우드 기반 스트리밍 및 로열티 앱에 대한 수요가 증가하고 있음을 보여줍니다.

유럽의 동향은 2025년 클라우드 주권 프레임워크에 따라 형성되었으며, 이 프레임워크에서는 승객 기록을 회원국 내에 보관할 것을 요구하고 있습니다. 이 규정에 따라 항공사들은 프라이빗 클라우드나 커뮤니티 클라우드로의 전환을 강요받고 있으며, 지역 인프라 구축이 촉진되고 있습니다. 카타르항공 등 중동 항공사들은 자국 내 프라이빗 클라우드 도입을 선호하는 한편, 세계 배분 시스템(GDS)과의 연동도 유지하고 있습니다. 남미에서는 도입 현황에 차이가 나타나고 있으며, 브라질과 칠레에서는 처리 시간 단축과 자원 배분의 최적화를 실현하는 클라우드 플랫폼을 통해 공항 운영의 현대화가 진행되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the aviation cloud market size is expected to grow from USD 7.13 billion in 2025 to USD 8.13 billion in 2026 and is forecast to reach USD 15.72 billion by 2031 at a 14.08% CAGR over 2026-2031.

This report is Segmented by Deployment Model (Public Cloud, Private Cloud, Hybrid Cloud, Community Cloud), Service Model (IaaS, Paas, Saas, and FaasS, Application (Flight Operations, Passenger Services, and More)), End User (Airlines, Airports, MRO Providers, Ansps, Oems, Regulators, and More), and Geography (North America, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Aviation Cloud Market Trends and Insights

Explosive Growth in Airline Digital-Transformation Budgets

Airlines are diverting capital from new-aircraft programs to cloud platforms that accelerate passenger experience innovation and operational resilience. The shift is visible in SITA's USD 50.8 billion 2025 IT-spend figure, where cloud migration rose faster than any other category. Examples include Virgin Atlantic's 2026 launch of satellite-enabled streaming that relies on cloud back-ends for real-time loyalty updates, while several low-cost carriers in Southeast Asia run entirely serverless reservation stacks. Payback periods have shortened as carriers retire lease-heavy data centers and trim IT headcount, making the aviation cloud market a core pillar of airline digital strategy.

Rising Demand for Real-Time Flight-Data Analytics

Event-driven platforms now process turbulence reports, health-monitoring telemetry, and radar plots within seconds, unlocking fuel and maintenance savings. Lufthansa's Turbulence Aware deployment and JetBlue's predictive-maintenance tie-in to Airbus Skywise both converted raw sensor feeds into sub-second operational decisions in 2025. EUROCONTROL's 2025 proof-of-concept extended the model to air navigation service providers, indicating that real-time processing is becoming mandatory across the aviation cloud industry.

Cyber-Sovereignty and Data-Residency Compliance Costs

Fragmented laws force carriers to replicate infrastructure across multiple jurisdictions, lifting capital needs 15-25% above single-region setups. The European Union's 2025 framework requires in-country processing of passenger name records, while Qatar Airways chose a private-cloud model in 2026 to satisfy national mandates. Comparable constraints in China and India compel airlines to maintain separate data lakes and audit chains, challenging uniform governance across global networks.

Other drivers and restraints analyzed in the detailed report include:

- Cloud Cost-Optimization Over Legacy Airline IT

- IaaS Expansion by Hyperscalers into Tier-2 Airports

- Skill Shortages in Aviation-Grade Cloud DevSecOps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid cloud is slated to grow 16.9% annually to 2031, reflecting airline demand for sovereign data control without forgoing hyperscaler elasticity. Delta Air Lines stores passenger information on private nodes while training demand-forecasting models on public GPUs, illustrating the two-tier pattern driving the aviation cloud market. Public deployments remain preferred for multi-tenant SaaS, such as reservations or crew scheduling, while private cloud lingers among flag carriers bound by explicit state directives. Community clouds, though small, enable regional alliances to share slots and maintenance data under joint governance, avoiding unilateral exposure.

Forward-looking deployments now interconnect private instances with edge zones inside airports to minimize latency for passenger flow, baggage tracking, and biometric boarding. The structure allows airlines to manage compliance for sensitive flight plans locally while executing high-volume analytics jobs in burstable public clusters. As regulators clarify cloud audit standards, carriers are expected to refine workload-placement policies rather than abandon the hybrid model that will anchor future growth of the aviation cloud market.

Platform-as-a-service should log the fastest 15.7% CAGR because it offers managed data lakes and event-streaming engines that eliminate the undifferentiated heavy lifting. Airbus Skywise, serving 200 airlines by 2025, lets carriers inject flight, maintenance, and weather feeds into a shared lake, then run custom reliability models without provisioning servers. SaaS still accounts for 41.5% of 2025 revenue, driven by passenger service, departure control, and revenue management suites migrated from mainframes to multi-tenant clouds. Infrastructure as a service underlies both layers, as airlines provision compute when lifting monolithic code for gradual refactoring.

Function-as-a-service, while niche, is emerging for discrete triggers such as automatic fare changes when competitors cut prices or auto-rebook logic during weather disruptions. This pay-per-execution model avoids idle resources, making it attractive for irregular operations. The cumulative effect of these service models underpins the expansion of the aviation cloud market, as carriers match technical tasks with the most cost-efficient abstraction layer.

Geography Analysis

North America, which accounted for 36.3% of 2025 revenue, benefits from early FAA endorsement of cloud-native air-traffic systems and multi-year airline migration programs. Delta, United, and American leverage hybrid blueprints that maintain on-premise failover while scaling compute for holiday peaks. Canada's NAV CANADA likewise shifted flight-data processing to a hybrid Azure stack, illustrating regulator confidence in controlled public platforms. Mexico's airport operators adopted queue analytics SaaS, signaling regional spill-over.

Asia-Pacific is expected to post a 15.1% CAGR through 2031 and drive the largest absolute gain in the aviation cloud market size. India's Digi Yatra and China's mandate that all new airports embed cloud resource systems accelerate adoption even at tier-3 facilities. Airlines in Indonesia, Japan, and Australia migrate maintenance, inventory, and passenger-experience workloads to the cloud, often skipping legacy data centers entirely. Satellite-enabled connectivity on Singapore Airlines' intercontinental routes demonstrates growing demand for cloud-hosted streaming and loyalty apps.

Europe's trajectory is shaped by the 2025 Cloud Sovereignty Framework, which requires passenger records to remain within member states. The rule steers carriers toward private or community clouds and stimulates local infrastructure builds. Middle East airlines such as Qatar Airways prefer private deployments inside national borders yet still integrate with global distribution systems. South America shows mixed adoption, with Brazil and Chile modernizing airport operations through cloud platforms that cut turnaround times and enhance resource allocation.

- Amazon Web Services Inc.

- Microsoft Corporation

- Google LLC

- International Business Machines Corporation (IBM)

- SITA

- Amadeus IT Group SA

- Sabre Corporation

- Lufthansa Systems GmbH

- Collins Aerospace (ARINC)

- Honeywell International Inc.

- Oracle Corporation

- Tata Consultancy Services Limited

- Unisys Corporation

- Raytheon Technologies Corporation

- Hexaware Technologies Limited

- HCL Technologies Limited

- Accenture plc

- Capgemini SE

- Indra Sistemas S.A.

- Salesforce Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive Growth in Airline Digital-Transformation Budgets

- 4.2.2 Rising Demand for Real-Time Flight-Data Analytics

- 4.2.3 Cloud Cost-Optimization Over Legacy Airline IT

- 4.2.4 IaaS Expansion by Hyperscalers into Tier-2 Airports

- 4.2.5 Sovereign-Cloud Mandates for Aviation Data

- 4.2.6 Satellite-Edge Fusion for Oceanic Route Coverage

- 4.3 Market Restraints

- 4.3.1 Cyber-Sovereignty and Data-Residency Compliance Costs

- 4.3.2 Skill Shortages in Aviation-Grade Cloud DevSecOps

- 4.3.3 Volatile Jet-Fuel Economics Delaying IT Refresh

- 4.3.4 Stratospheric Spectrum-Sharing Uncertainty

- 4.4 Industry Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Deployment Model

- 5.1.1 Public Cloud

- 5.1.2 Private Cloud

- 5.1.3 Hybrid Cloud

- 5.1.4 Community Cloud

- 5.2 By Service Model

- 5.2.1 Infrastructure as a Service (IaaS)

- 5.2.2 Platform as a Service (PaaS)

- 5.2.3 Software as a Service (SaaS)

- 5.2.4 Function as a Service (FaaS)

- 5.3 By Application

- 5.3.1 Flight Operations

- 5.3.2 Passenger Services

- 5.3.3 Airport Operations

- 5.3.4 Maintenance Repair and Overhaul (MRO)

- 5.3.5 Crew and Workforce Management

- 5.3.6 Other Applications

- 5.4 By End User

- 5.4.1 Airlines

- 5.4.2 Airports

- 5.4.3 MRO Providers

- 5.4.4 Air Navigation Service Providers (ANSP)

- 5.4.5 Aircraft OEMs and Integrators

- 5.4.6 Aviation Regulators

- 5.4.7 Other End Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 South Korea

- 5.5.3.4 India

- 5.5.3.5 Australia

- 5.5.3.6 Indonesia

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Chile

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Saudi Arabia

- 5.5.5.1.4 Israel

- 5.5.5.1.5 Qatar

- 5.5.5.1.6 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Kenya

- 5.5.5.2.4 Egypt

- 5.5.5.2.5 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 Amazon Web Services Inc.

- 6.4.2 Microsoft Corporation

- 6.4.3 Google LLC

- 6.4.4 International Business Machines Corporation (IBM)

- 6.4.5 SITA

- 6.4.6 Amadeus IT Group SA

- 6.4.7 Sabre Corporation

- 6.4.8 Lufthansa Systems GmbH

- 6.4.9 Collins Aerospace (ARINC)

- 6.4.10 Honeywell International Inc.

- 6.4.11 Oracle Corporation

- 6.4.12 Tata Consultancy Services Limited

- 6.4.13 Unisys Corporation

- 6.4.14 Raytheon Technologies Corporation

- 6.4.15 Hexaware Technologies Limited

- 6.4.16 HCL Technologies Limited

- 6.4.17 Accenture plc

- 6.4.18 Capgemini SE

- 6.4.19 Indra Sistemas S.A.

- 6.4.20 Salesforce Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment