|

시장보고서

상품코드

2062444

스마트 커넥티드 자산 및 운영 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Smart Connected Assets And Operations - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

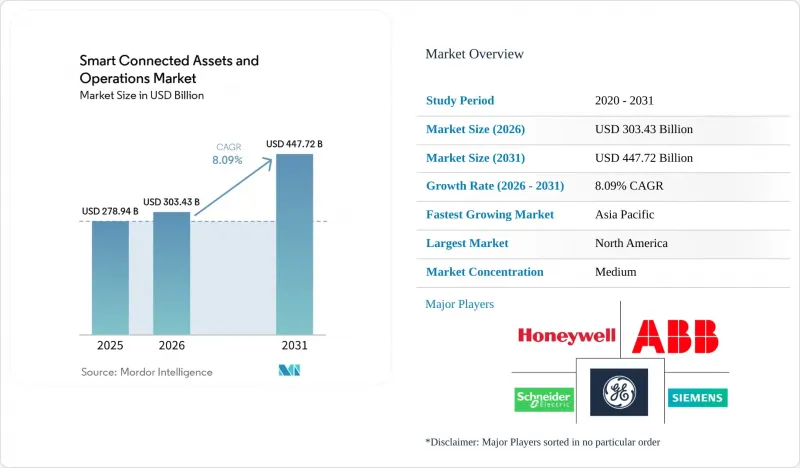

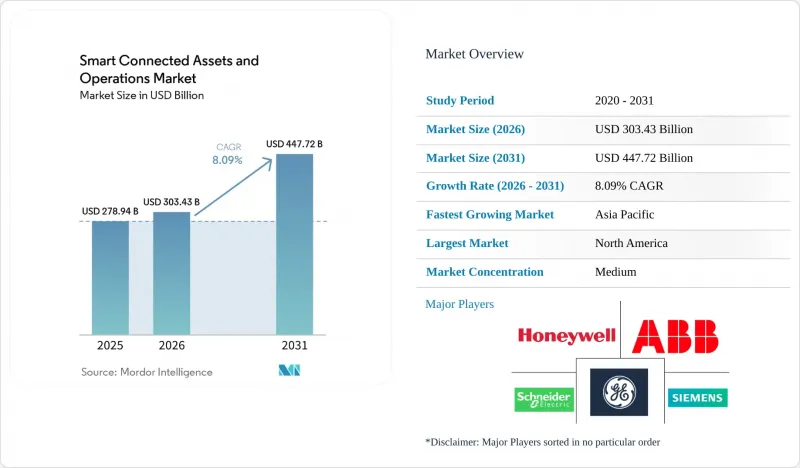

Mordor Intelligence에 의하면, 스마트 커넥티드 자산 및 운영 시장 규모는 2025년에 2,789억 4,000만 달러로 평가되었고, 2026년 3,034억 3,000만 달러로 추정되고, 2031년까지 4,477억 2,000만 달러에 이를 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR)은 8.09%를 나타낼 전망입니다.

본 보고서는 구성 요소별(하드웨어, 소프트웨어, 서비스), 연결 기술별(유선, 무선, 위성), 배포 방식별(온프레미스, 클라우드, 하이브리드), 산업 분야별(제조, 에너지 및 유틸리티, 석유 및 가스, 광업, 운송 및 물류, 의료 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 스마트 커넥티드 자산 및 운영 시장 동향과 인사이트

자산 성과 관리를 통합한 산업용 IoT 플랫폼의 급속한 보급

세계의 제조업체들은 센서 데이터, 히스토리안 로그 및 기업 기록을 예측 유지보수 대시보드에 통합하는 통합 산업용 IoT 플랫폼으로 개별 도구를 통합하고 있습니다. Amazon Web Services는 2025년에 SiteWise Edge를 출시하여, 클라우드와 요약 데이터를 동기화하면서도 100밀리초 미만의 로컬 지연 시간을 실현했습니다. 이러한 설계를 통해 제어 네트워크를 일반 트래픽으로부터 격리하고 있습니다. PTC의 2025년 투자자 제출 자료에 따르면, ThingWorx 도입 건수는 전년 대비 40% 증가했으며, 자동차 부품 공급업체들은 CAD와 PLM의 긴밀한 통합을 통해 근본 원인 분석에 소요되는 시간을 며칠에서 몇 시간으로 단축할 수 있었습니다고 밝혔습니다. Rockwell Automation은 전 세계 50만 대 이상의 장치를 연결하는 ‘FactoryTalk Hub’를 원동력으로 삼아, 2025년에 구독형 소프트웨어 매출이 10억 달러를 돌파했다고 보고했습니다. GE Digital은 Predix를 수평 계층으로 재정의하고, 현재 각 분야의 전문가들과 협력하여 터빈 점검 주기를 최대 20% 연장하는 풍력 발전소 및 발전소용 턴키 최적화 솔루션을 제공합니다.

가동 중단 시간을 최소화하기 위한 예측 유지보수로의 전환이 진전되고 있습니다.

예측 유지보수는 비용 절감 효과가 확고해짐에 따라 시범 단계에서 기업 차원으로 확대되고 있습니다. 쉘은 2025년 지속가능성 보고서에서 예기치 못한 가동 중단 시간이 35% 감소하고 유지보수 비용이 20% 절감되었다고 보고했으며, 그 결과 연간 2억 달러 이상의 비용 절감을 달성했습니다. 2025년, Factory AI는 12개 자동차 공장에서 베어링 열화가 발생하기 14일 전에 92%의 정확도로 고장을 예측하는 데 성공했습니다. Emerson의 AspenTech V15에는 유지보수 시기를 생산 일정에 맞출 수 있는 생성형 AI 모델이 탑재되어 있어, 화학 플랜트의 예기치 못한 가동 중단을 15% 줄이는 데 기여하고 있습니다. 국제에너지기구(IEA)의 추산에 따르면, 도입률이 60%에 도달할 경우 2030년까지 발전 업계 전체에서 500억 달러의 중단 비용을 피할 수 있을 것으로 보입니다. Augury와 같은 관리형 서비스 제공업체는 센서, 분석 기능, 가동률 보장을 하나의 패키지로 제공하므로, 중규모 공장은 설비 투자를 피하면서도 성능 관련 위험을 공급업체에 전가할 수 있습니다.

기존 설비에 대한 막대한 초기 투자 비용과 통합의 복잡성

기존 기계 설비에 센서나 게이트웨이를 사후에 도입하는 경우, 신규 도입에 비해 비용이 몇 배나 더 드는 경우가 종종 있습니다. 슈나이더 일렉트릭의 보고서에 따르면, 정유시설에 EcoStruxure를 도입하는 데는 평균 18-24개월이 소요됩니다. 이는 엔지니어가 분석 기능을 추가하기 전에, 수십년전의 프로그래머블 로직 컨트롤러(PLC)의 로직을 리버스 엔지니어링해야 하기 때문입니다. 에머슨은 자산 성과 개선 프로젝트의 40%에서 Modbus, Profibus, Foundation Fieldbus를 연동하기 위한 맞춤형 미들웨어가 필요하며, 이로 인해 사이트당 20만-50만 달러의 추가 비용이 발생한다고 밝혔습니다. 2024년에 최종 확정된 IEC 62443 사이버 보안 규격은 네트워크 세분화과 암호화를 의무화하고 있지만, 많은 기존 설비(브라운필드)의 운영 사업자들은 이러한 요소가 부족하여 인프라를 병행하여 업그레이드할 수밖에 없는 실정입니다. 요금 개정 주기에 제약을 받는 규제 대상 유틸리티자는 안전 및 규정 준수 기관에서 의무화하지 않는 한, 이러한 자본 집약적인 프로그램을 미루는 경우가 많습니다.

부문별 분석

하드웨어는 2025년 매출의 49.19%를 차지했으나, 기업들이 사후 대응형 자산 소유 방식에서 성과 기반 계약으로 전환함에 따라 소프트웨어 및 관리형 서비스 분야의 스마트 커넥티드 자산 운영 시장 규모는 연평균 성장률(CAGR) 8.72%로 확대될 것으로 전망됩니다. 반도체 공급업체들이 아날로그-디지털 변환, 신호 조정, 무선 기능을 단일 칩에 집적함에 따라 센서와 액추에이터는 상품화가 진행되고 있으며, 단가는 연간 최대 20% 하락하고 있습니다. NVIDIA Jetson Orin과 같은 엣지 게이트웨이는 15와트의 전력 소비로 275 TOPS를 구현하여, 클라우드와의 왕복 통신 없이도 장치 자체에서 이상 감지가 가능하게 합니다.

벤더들이 영구 라이선스에서 종량제 과금 방식으로 전환함에 따라, 소프트웨어는 높은 이익률을 확보하고 있습니다. IBM Maximo나 SAP Intelligent Asset Management와 같은 자산 성능 관리 제품군에는 작업 지시서를 자동으로 작성하고 예비 부품 조달을 제안하는 생성형 AI가 통합되어 있어, 기획 담당자의 업무 부담을 40% 줄이고 있습니다. 3-5년 단위의 매니지드 서비스 계약이 중견 제조업체들 사이에서 점차 확산되고 있으며, 서비스 제공업체는 가동 시간 보장을 대가로 센서 교정, 모델 재학습, 사이버 보안 패치 적용 등의 책임을 지고 있습니다. 그 결과, 가치 창출은 단순한 하드웨어가 아닌, 분석, 서비스, 지속적인 개선을 종합적으로 제공하는 벤더로 이동하고 있습니다.

2025년에는 이더넷이 스마트 커넥티드 자산 운영 시장에서 76.73%의 점유율을 차지하며 지배적인 위치를 차지했으나, 프라이빗 5G, NB-IoT, LoRaWAN이 모바일 및 원격지 자산에 대한 커버리지를 확대함에 따라 무선 연결은 연평균 성장률(CAGR) 8.95%로 성장하고 있습니다. 산업용 이더넷은 Cisco, Hirschmann, Moxa의 스위치에 내장된 IEEE 802.1 타임 센시티브 네트워킹(TSN) 확장 기능을 활용하여 1밀리초 미만의 결정론적 제어를 지속적으로 지원하고 있습니다. 무선 옵션은 대역폭이 넓은 공장 내 이동성과 장거리 및 저전력 원격 측정이라는 두 가지로 나뉩니다.

지멘스가 2026년 2월에 발표한 바와 같이, 제조 현장에서 10밀리초 미만의 지연 시간은 자율 주행 로봇 및 증강현실(AR) 워크플로우에서 5G의 적합성을 입증하고 있습니다. NB-IoT는 통신 사업자와의 원활한 통합을 통해 전 세계 저전력 광역 네트워크(LPWA) 도입의 58%를 차지하고 있습니다. 한편, LoRaWAN은 중국 이외 지역에서 면허가 필요 없는 주파수 대역의 구축 분야에서 40%의 점유율을 기록하며 주도적인 위치를 차지하고 있습니다. 이리듐 및 신흥 저궤도 위성 군집에 의한 위성 링크는 지상 네트워크 도입이 여전히 현실적이지 않은 해상 시추 시설이나 외딴 지역의 광산에서 발생하는 텔레메트리 데이터를 백홀하고 있습니다.

지역별 분석

북미는 2025년 매출의 37.63%를 차지했으며, 제조업체들이 생산 능력을 국내로 되돌리고, 유틸리티자들이 노후화된 송전 자산을 디지털화함에 따라 연평균 성장률(CAGR) 8.87%로 성장하고 있습니다. 미국 에너지부의 추산에 따르면, 캘리포니아주와 텍사스주에서는 재생에너지 보급률이 40%를 넘어섰으며, 이는 송전망 현대화의 시급성을 여실히 보여주고 있습니다. Rockwell Automation은 공급망의 병목 현상을 완화하기 위해 PLC 및 엣지 디바이스의 국내 생산에 20억 달러를 배정했습니다. 캐나다 온타리오주와 브리티시컬럼비아주의 전력 회사들은 정전 대응 시간을 단축하기 위해 첨단 계량 인프라(AMI) 도입을 가속화하고 있습니다. 멕시코는 자동차 전자기기 분야에 대한 외국인 투자를 유치하고 있으며, 3개국에 걸친 공급망을 연계하기 위해 커넥티드 자산 플랫폼의 도입을 촉진하고 있습니다.

유럽에서는 EU의 CSRD(기업 지속가능성 보고 지침)에 따라 에너지 효율이 우선시되고 있으며, 기업들은 설비 단위의 배출량을 정량화해야 할 의무가 있습니다. Severn Trent는 2025년 9월 Netmore와 제휴하여 100만 대의 LoRaWAN 지원 수도 계량기를 도입함으로써, 미수금 손실을 10% 줄일 계획입니다. 지멘스, 슈나이더 일렉트릭, ABB는 전 세계적인 확대에 앞서 독일, 프랑스, 영국에서 디지털 트윈 공장의 시범 운영을 진행하고 있습니다. 지정학적 제재로 인해 러시아의 현대화 속도가 둔화되면서, 지역 내 수요는 국내 자동화 업체들로 쏠리고 있습니다.

중국, 일본, 인도, 한국이 스마트 제조 정책을 정착시켜 나가는 가운데, 아시아태평양은 절대적인 성장률에서 1위를 기록하고 있습니다. 중국의 ‘중국 제조 2025’ 로드맵은 스마트 팩토리를 우선시하고 있는 반면, 일본의 ‘사회 5.0’은 노동력 고령화를 보완하기 위해 사이버-물리 시스템을 통합하고 있습니다. 인도의 ‘스마트 시티 미션’은 100개 도시권에서 교통, 폐기물, 수자원 관리를 위한 IoT 기반 네트워크 구축을 지원하고 있습니다. 호주의 한 광산 기업은 수천 킬로미터 떨어진 도시 지역에서 제어되는 자율 주행 차량 군을 운영하고 있으며, 원격 환경에서의 엣지 분석의 실현 가능성을 입증하고 있습니다. 중동에서는 석유 수입을 사우디아라비아의 NEOM과 같은 다양한 스마트 시티 프로젝트에 투자하고 있어, 견고한 자산 성과 관리 체계가 요구되고 있습니다. 남아프리카공화국과 나이지리아에서는 식량 안보와 전력망의 신뢰성을 높이기 위해 정밀 농업 및 스마트 계량 솔루션의 시범 운영이 진행되고 있습니다. 남미에서는 브라질과 아르헨티나가 주도하여 수출 시장의 지속가능성 인증 요건을 충족하기 위해 농업 분야에서 커넥티드 자산 프레임워크를 도입하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the smart connected assets and Operations market size was valued at USD 278.94 billion in 2025 and is estimated to grow from USD 303.43 billion in 2026 to reach USD 447.72 billion by 2031, at a CAGR of 8.09% during 2026-2031.

This report is Segmented by Component (Hardware, Software, and Services), Connectivity Technology (Wired, Wireless, and Satellite), Deployment Mode (On-Premise, Cloud, and Hybrid), Industry Vertical (Manufacturing, Energy and Utilities, Oil and Gas, Mining, Transportation and Logistics, Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Smart Connected Assets And Operations Market Trends and Insights

Rapid Adoption of Industrial IoT Platforms Integrating Asset Performance Management

Global manufacturers are consolidating point tools into unified industrial IoT platforms that stream sensor data, historian logs, and enterprise records into prescriptive-maintenance dashboards. Amazon Web Services shipped SiteWise Edge in 2025, offering sub-100 ms local latency while synchronizing summaries with the cloud, a design that keeps control networks isolated from public traffic.PTC's 2025 investor filing showed ThingWorx deployments rising 40% year over year as automotive suppliers cited tight CAD and PLM integration that cuts root-cause analysis from days to hours. Rockwell Automation reported subscription software revenue surpassing USD 1 billion in 2025, driven by FactoryTalk Hub, which connects more than 500,000 devices worldwide. GE Digital repositioned Predix as a horizontal layer and now partners with domain specialists to deliver turnkey wind-farm and power-plant optimizations that extend turbine inspection intervals by up to 20%.

Increasing Shift Towards Predictive Maintenance to Minimise Downtime

Predictive maintenance has moved from pilot to enterprise scale as the savings case hardens. Shell documented a 35% drop in unplanned downtime and a 20% reduction in maintenance spend in its 2025 sustainability report, resulting in annual savings above USD 200 million. Factory AI achieved a 92% bearing-failure forecast accuracy 14 days before degradation across 12 automotive plants in 2025. Emerson's AspenTech V15 embeds generative AI models that align maintenance windows with production schedules, helping chemical plants reduce unplanned outages by 15%. The International Energy Agency calculates that similar techniques could avert USD 50 billion in outage costs across power generation by 2030 if adoption reaches 60%. Managed-service providers such as Augury bundle sensors, analytics, and uptime guarantees so mid-size factories can avoid capital expense while transferring performance risk to the vendor.

High Upfront Capital and Integration Complexity for Brownfield Assets

Retrofitting legacy machinery with sensors and gateways often costs multiple times as much as greenfield deployments. Schneider Electric reported average EcoStruxure rollouts at refineries lasting 18-24 months because engineers must reverse-engineer decades-old programmable-logic-controller logic before layering analytics. Emerson disclosed that 40% of asset-performance projects require custom middleware to bridge Modbus, Profibus, and Foundation Fieldbus, adding USD 200,000-500,000 per site. IEC 62443 cybersecurity standards finalized in 2024 compel network segmentation and encryption that many brownfield operators lack, driving parallel infrastructure upgrades. Regulated utilities, constrained by rate-case cycles, often defer such capital-heavy programs unless mandated by safety or compliance bodies.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of 5G Private Networks Enabling Real-Time Analytics at Edge

- Regulatory Push for Sustainability and Energy-Efficiency Reporting

- Cyber-Security Vulnerabilities Across Expanded Attack Surfaces

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware retained 49.19% of 2025 revenue, yet the Smart Connected Assets and Operations market size for software and managed services is projected to expand at an 8.72% CAGR as enterprises migrate from reactive asset ownership to outcome-based contracts. Sensors and actuators are commoditizing as semiconductor vendors collapse analog-to-digital conversion, signal conditioning, and radios onto single chips, lowering unit prices by up to 20% annually. Edge gateways such as NVIDIA Jetson Orin deliver 275 TOPS in a 15-watt envelope, enabling on-device anomaly detection without cloud round-trips.

Software commands premium margins as vendors shift from perpetual licenses to consumption pricing. Asset performance suites like IBM Maximo and SAP Intelligent Asset Management embed generative AI that auto-drafts work orders and suggests spare-parts procurement, trimming planner workload by 40%. Managed-services contracts spanning 3-5 years are gaining traction among mid-size manufacturers, with providers assuming responsibility for sensor calibration, model retraining, and cybersecurity patching in exchange for uptime guarantees. Consequently, value capture is tilting toward vendors that bundle analytics, services, and continuous improvement rather than stand-alone hardware.

Ethernet dominated the Smart Connected Assets and Operations market with 76.73% market share in 2025, but wireless links are growing at an 8.95% CAGR as private 5G, NB-IoT, and LoRaWAN extend coverage to mobile and remote assets. Industrial Ethernet continues to anchor sub-1 ms deterministic control using IEEE 802.1 time-sensitive networking extensions built into Cisco, Hirschmann, and Moxa switches. Wireless options bifurcate between high-bandwidth intra-plant mobility and long-range, low-power telemetry.

Siemens' February 2026 announcement of sub-10 ms production-floor latency underscores 5G's suitability for autonomous mobile robots and augmented-reality workflows. NB-IoT accounts for 58% of low-power wide-area deployments globally due to seamless carrier integration, while LoRaWAN leads unlicensed spectrum rollouts outside China with 40% share. Satellite links from Iridium and emerging low-earth-orbit constellations backhaul telemetry from offshore rigs and remote mines where terrestrial networks remain impractical.

Geography Analysis

North America generated 37.63% of 2025 revenue and is advancing at an 8.87% CAGR as manufacturers reshore capacity and utilities digitize aging transmission assets. The U.S. Department of Energy estimates that renewable penetration exceeded 40% in California and Texas, underscoring the urgency of grid modernization. Rockwell Automation earmarked USD 2 billion for domestic production of PLCs and edge devices to mitigate supply chain bottlenecks. Canada's utilities in Ontario and British Columbia accelerate advanced-metering infrastructure deployments to shorten outage response times. Mexico attracts foreign investment in automotive electronics, spurring the adoption of connected-asset platforms to sync tri-national supply chains.

Europe prioritizes energy efficiency under the EU CSRD, compelling firms to quantify equipment-level emissions. Severn Trent partnered with Netmore in September 2025 to roll out 1 million LoRaWAN water meters to cut non-revenue water losses by 10%. Siemens, Schneider Electric, and ABB are piloting digital twin factories in Germany, France, and the United Kingdom before global scaling. Geopolitical sanctions slow Russia's modernization, steering regional demand toward domestic automation vendors.

Asia-Pacific posts the fastest absolute growth as China, Japan, India, and South Korea embed smart-manufacturing policies. China's Made in China roadmap prioritizes intelligent factories, while Japan's Society 5.0 aligns cyber-physical systems to offset workforce aging. India's Smart Cities Mission supports IoT-enabled networks for traffic, waste, and water in 100 urban centers. Australia's miners operate autonomous fleets controlled from urban centers thousands of kilometers away, validating the viability of edge analytics in remote environments. The Middle East channels oil revenues into diversified smart-city projects, such as Saudi Arabia's NEOM, and demands robust asset-performance layers. South Africa and Nigeria are piloting precision agriculture and smart metering solutions to improve food security and grid reliability. South America, led by Brazil and Argentina, applies connected-asset frameworks in agribusiness to meet export-market sustainability certification requirements.

- Siemens AG

- General Electric Company

- Schneider Electric SE

- ABB Ltd.

- Honeywell International Inc.

- Rockwell Automation, Inc.

- Emerson Electric Co.

- Mitsubishi Electric Corporation

- Robert Bosch GmbH

- Hitachi, Ltd.

- Yokogawa Electric Corporation

- PTC Inc.

- Cisco Systems, Inc.

- IBM Corporation

- Microsoft Corporation

- SAP SE

- Oracle Corporation

- Fujitsu Limited

- Aspen Technology, Inc.

- AVEVA Group plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Adoption of Industrial IoT Platforms Integrating Asset Performance Management

- 4.2.2 Increasing Shift Towards Predictive Maintenance to Minimise Downtime

- 4.2.3 Demand for Remote Operations and Worker Safety in Hazardous Environments

- 4.2.4 Proliferation of 5G Private Networks Enabling Real-Time Analytics at Edge

- 4.2.5 Regulatory Push for Sustainability and Energy-Efficiency Reporting

- 4.2.6 Convergence of Digital-Twin Technology with AI-Driven Asset Modelling

- 4.3 Market Restraints

- 4.3.1 High Upfront Capital and Integration Complexity for Brownfield Assets

- 4.3.2 Cyber-Security Vulnerabilities Across Expanded Attack Surfaces

- 4.3.3 Interoperability Challenges Due to Proprietary Legacy Protocols

- 4.3.4 Shortage of Cross-Disciplinary OT-IT-Analytics Talent

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter''s Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.1.1 Sensors and Actuators

- 5.1.1.2 Gateways and Edge Devices

- 5.1.2 Software

- 5.1.2.1 Asset Performance Management (APM)

- 5.1.2.2 Manufacturing Execution System (MES)

- 5.1.2.3 SCADA and HMI

- 5.1.2.4 Analytics and AI Platforms

- 5.1.3 Services

- 5.1.3.1 Professional Services

- 5.1.3.2 Managed Services

- 5.1.1 Hardware

- 5.2 By Connectivity Technology

- 5.2.1 Wired

- 5.2.1.1 Ethernet

- 5.2.1.2 Industrial Fieldbus

- 5.2.2 Wireless

- 5.2.2.1 Wi-Fi and Bluetooth

- 5.2.2.2 5G / Private LTE

- 5.2.2.3 LPWAN (LoRa, NB-IoT, Sigfox)

- 5.2.3 Satellite / Remote

- 5.2.1 Wired

- 5.3 By Deployment Mode

- 5.3.1 On-Premise

- 5.3.2 Cloud

- 5.3.3 Hybrid

- 5.4 By Industry Vertical

- 5.4.1 Manufacturing

- 5.4.2 Energy and Utilities

- 5.4.3 Oil and Gas

- 5.4.4 Mining

- 5.4.5 Transportation and Logistics

- 5.4.6 Healthcare

- 5.4.7 Agriculture

- 5.4.8 Smart Cities and Infrastructure

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.2 Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Siemens AG

- 6.4.2 General Electric Company

- 6.4.3 Schneider Electric SE

- 6.4.4 ABB Ltd.

- 6.4.5 Honeywell International Inc.

- 6.4.6 Rockwell Automation, Inc.

- 6.4.7 Emerson Electric Co.

- 6.4.8 Mitsubishi Electric Corporation

- 6.4.9 Robert Bosch GmbH

- 6.4.10 Hitachi, Ltd.

- 6.4.11 Yokogawa Electric Corporation

- 6.4.12 PTC Inc.

- 6.4.13 Cisco Systems, Inc.

- 6.4.14 IBM Corporation

- 6.4.15 Microsoft Corporation

- 6.4.16 SAP SE

- 6.4.17 Oracle Corporation

- 6.4.18 Fujitsu Limited

- 6.4.19 Aspen Technology, Inc.

- 6.4.20 AVEVA Group plc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment