|

시장보고서

상품코드

2062453

금속 공기 배터리 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Metal-Air Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

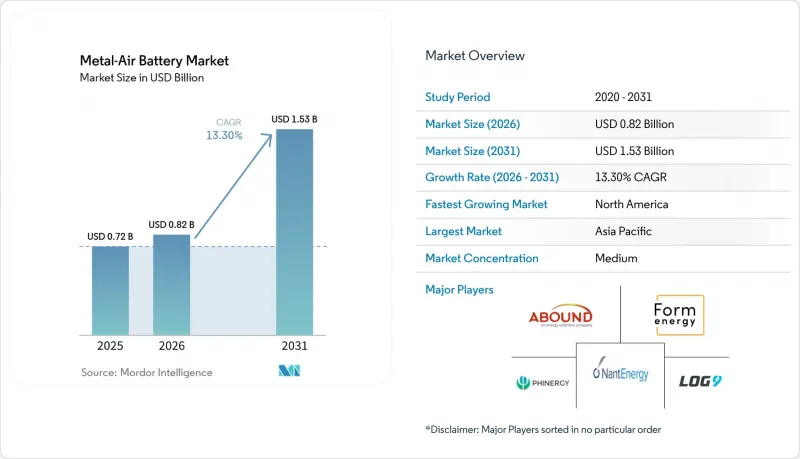

Mordor Intelligence에 의하면, 금속 공기 배터리 시장 규모는 2026년 8억 2,000만 달러로 추정되고, 2031년까지 15억 3,000만 달러로 확대될 전망이며, 2026-2031년 CAGR 13.3%를 나타낼 것으로 예측됩니다.

본 보고서는 금속 유형별(아연-공기, 알루미늄-공기, 리튬-공기, 철-공기 및 기타 금속), 배터리 유형별(1차 전지, 2차 전지), 전압별(저전압, 중전압, 고전압), 용도별(전기자동차, 고정형 에너지 저장, 군 및 방위용 전자기기, 소비자용 및 의료용 전자기기 및 기타 용도) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 금속 공기 배터리 시장 동향 및 분석

충전식 아연 공기 및 리튬 공기 배터리의 화학 기술 발전

2025년과 2026년에 보고된 획기적인 이중 기능성 촉매 덕분에 아연 공기 배터리의 수명이 10,000시간 이상으로 연장되었으며, 충전 시와 방전 시의 전압 차가 줄어들었습니다. 이러한 개선을 통해 열 관리 부담이 줄어들었고, 고정형 에너지 저장 시스템 분야에서 총비용 측면에서 리튬 이온 배터리에 필적하는 2차 아연 공기 배터리 팩의 길이 열렸습니다. 또한, 연구진은 보호된 리튬 음극을 갖춘 고체 전해질에 대한 관심을 높이고 있으며, 리튬 공기 배터리의 상용화를 위한 확실한 로드맵이 제시되고 있습니다. 이러한 발전들이 맞물리면서, 며칠에 걸친 방전 솔루션이 보증 요건을 충족할 수 있다는 전력 회사와 데이터센터 운영자들의 확신을 강화시켜, 조달 프로젝트 증가를 촉진하고 있습니다.

전기차의 급속한 보급이 요구하는 초고에너지 밀도 배터리 팩

세계 전기차 판매 대수는 2024년에 1,400만 대를 돌파하며 계속 증가하고 있습니다. 자동차 제조업체들은 배터리 팩의 무게를 늘리지 않으면서도 한 번 충전으로 500km의 주행 거리를 실현할 수 있는 화학 기술을 모색하고 있습니다. 금속 공기 배터리는 리튬 이온 전지에 비해 3배에서 5배 더 높은 이론적 비에너지를 기대할 수 있습니다. Phinergy, Hindalco, Indian Oil 등 3사가 체결한 양해각서는 몇 분 만에 알루미늄 플레이트를 교체할 수 있는 알루미늄-공기 배터리 팩 개발을 목표로 하고 있으며, 이는 전력 공급 물류 체계를 혁신할 것입니다. 중국과 인도에서는 시범 차량을 활용한 레인지 익스텐더 모듈 시험이 진행 중이며, 배기가스 제로화를 위한 규제상의 인센티브가 상용 플랫폼의 상용화 일정을 앞당기고 있습니다.

성숙된 리튬 이온 화학 기술에 비해 제한적인 사이클 수명

실험실 환경에서 철-공기 시스템은 최대 1,696시간의 가동 시간을 기록했으며, 충전식 아연 공기 배터리도 최상의 조건에서는 10,000시간을 넘게 되었지만, 둘 다 리튬 이온 배터리의 표준인 3,000-5,000회 사이클에는 미치지 못하는 상황입니다. 따라서 주파수 조정이나 승용차 등 매일 주기적으로 작동하는 용도에서는 여전히 리튬 이온 배터리가 주류를 이루고 있습니다. Form Energy사는 철 공기 배터리를 주간 또는 월간 주기로 100시간 동안 방전하는 용도로 설정하여, 가장 가혹한 사용 조건을 피하고 있습니다. 전해액 내 이산화탄소 발생 억제 및 덴드라이트 제어 분야의 지속적인 발전은 여전히 더 광범위한 도입을 위한 전제조건으로 남아 있습니다.

부문별 분석

아연 공기 배터리는 2025년에도 금속 공기 배터리 시장에서 55.47%의 점유율을 유지한 것으로 평가되었습니다. 이는 주로 보청기나 의료용 전자기기에서 지속적으로 사용되기 때문이며, 이러한 기기에서는 1차 전지로서 높은 신뢰성을 갖춘 성능이 요구되기 때문입니다. Form Energy사의 광범위한 다중 프로젝트 파이프라인에 힘입어 철 공기 배터리 부문은 금속 공기 배터리 시장에서 더 큰 점유율을 차지할 것으로 예측됩니다. 이 부문은 다양한 용도로의 채택 확대에 힘입어, 2026-2031년 예측 기간 동안 13.86%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다.

계통 연계 및 데이터센터 백업 운영에서 수일에 걸친 방전 계약 증가는 철 공기 배터리의 경제적 실현 가능성을 입증하고 있습니다. 이러한 배터리는 kW시당 저장 비용을 낮게 유지하는 대신, 사이클 수명과 왕복 효율 간의 절충이 허용되는 용도에 특히 적합합니다. 한편, 알루미늄 공기 배터리를 개발하는 기업들은 풍부한 알루미늄 원료와 금속 플레이트의 신속한 교체 가능성을 활용하고 있습니다. 이 접근 방식은 특히 상용 차량 운영에 있어 주행 거리 부족에 대한 우려나 연료 보급으로 인한 가동 중단 시간과 같은 중대한 문제점을 해결하기 위한 것입니다. 한편, 리튬 공기 배터리 기술은 고체 전지 프로토타입 개발에서 진전을 보이고 있지만, 해당 기술이 초기 단계에 있고 상용화를 위한 과제가 여전히 남아 있어, 현재 예측 기간 내에는 주류로 채택될 것으로 예상되지 않습니다.

2025년 기준으로, 금속 공기 배터리 시장 중 1차 전지가 60.19%를 차지했습니다. 이는 보청기 등의 의료기기나 소비자용 전자 기기에서 확립된 용도에 힘입은 결과입니다. 이러한 전지는 안정적인 성능이 요구되는 분야에서 그 신뢰성과 높은 비용 효율성 덕분에 여전히 시장을 주도하고 있습니다. 한편, 두 기능성 촉매의 발전으로 2차 아연 공기 배터리의 수명이 대폭 연장되어 약 10,000시간 동안 작동할 수 있게 되었습니다. 이러한 발전은 고정형 에너지 저장 시스템 및 모빌리티 분야에서의 새로운 활용 기회를 열어줄 것으로 보이며, 예측 기간 동안 충전식 아연 공기 배터리의 연평균 성장률(CAGR)이 13.92%를 나타낼 것으로 전망됩니다.

듀라셀, 파나소닉, GP 배터리스와 같은 기존 기업들은 광범위한 유통망과 브랜드 인지도를 바탕으로 버튼형 전지 부문에서 확고한 입지를 유지하고 있습니다. 그러나 EnZinc나 Zinc8과 같은 신생 기업들은 지역 마이크로그리드나 상업용 빌딩 등의 용도를 위한 모듈형 아연 공기 배터리 팩의 규모 확대를 향해 꾸준히 나아가고 있습니다. 미국 및 유럽 등지에서 제조 능력이 연간 기가와트시 규모로 확대됨에 따라, 금속 공기 배터리 시장의 2차 전지 구성으로의 전환이 가속화될 것으로 예상되며, 이는 해당 분야의 혁신과 보급을 더욱 촉진할 것입니다.

지역별 분석

2025년 금속 공기 배터리 시장에서 아시아태평양은 53.79%를 차지했습니다. 이는 중국의 방대한 제조 역량, 인도의 전략적 알루미늄 공기 배터리 협력, 그리고 일본의 촉매 과학 분야의 발전에 힘입은 결과입니다. 중국은 CATL의 'Choco-Swap' 생태계를 통해 배터리 교체 인프라를 구축하고 있습니다. 이 시스템은 2024년 12월에 가동을 시작하여, 2025년까지 1,000곳, 중기 목표로는 10,000곳의 스테이션을 구축할 계획이며, 알루미늄 공기 배터리 및 아연 공기 배터리에 적용 가능한 금속 슬러리 급전 시스템 모델을 구축하고 있습니다. 해당 지역은 현지 공급망 개발을 촉진하는 정책과 야심 찬 운송 부문 전기화 목표의 혜택을 받고 있어, 시장 성장에 유리한 환경이 조성되어 있습니다. 또한, 주요 기업들의 존재와 연구 개발에 대한 지속적인 투자가 아시아태평양 시장에서의 우위를 더욱 공고히 하고 있습니다.

북미는 2026-2031년 14.08%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 이러한 성장은 장기간에 걸친 주 차원의 에너지 저장 의무화 정책, 에너지부의 자금 지원 이니셔티브, 그리고 웨스트버지니아주에 Form Energy의 생산 시설이 설립된 데 힘입은 것입니다. 이러한 요인들은 기초 조사부터 대규모 현장 도입에 이르기까지를 아우르는 견고한 국내 생태계 구축에 기여하고 있습니다. 또한, 캐나다가 ELYSIS 사업을 통해 저탄소 알루미늄 생산에 주력하고 있는 것은 해당 지역의 원료 지속가능성을 높이고, 시장 확대를 더욱 촉진하고 있습니다.

유럽은 '호라이즌 유럽' 프로그램 하에서 산학 협력 촉진에 지속적으로 주력하고 있으며, 아연 공기 배터리의 상용화를 위해 1,500만 유로(약 1,620만 달러)를 배정했습니다. 독일과 영국 등 각국의 송전망 운영 사업자들은 용량 입찰에 며칠 단위의 에너지 저장 솔루션을 점점 더 많이 도입하고 있습니다. 이러한 전략적 중점을 통해 유럽은 주요 실증 단계의 달성을 전제로, 향후 수요의 급격한 증가에 대비한 체제를 갖추고 있습니다. 해당 지역에서의 혁신 및 규제 측면 지원에 대한 집중적인 노력은 금속 공기 배터리 기술의 발전을 지속적으로 이끌고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the metal-air battery market size is expected to increase from USD 0.82 billion in 2026 to USD 1.53 billion by 2031, growing at a CAGR of 13.3% over 2026-2031.

This report is Segmented by Metal Type (Zinc-Air, Aluminum-Air, Lithium-Air, Iron-Air, and Other Metal Type), Battery Type (Primary, and Secondary), Voltage (Low, Medium, and High), Application (Electric Vehicles, Stationary Energy Storage, Military and Defence Electronics, Consumer and Medical Electronics, and Other Application), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Metal-Air Battery Market Trends and Insights

Advances in Rechargeable Zinc-Air and Lithium-Air Chemistries

Breakthrough bifunctional catalysts reported during 2025 and 2026 increased zinc-air cycle life above 10,000 hours and narrowed the voltage gap between charge and discharge. These improvements reduce thermal management loads and pave the way for secondary zinc-air packs that can rival lithium-ion on total cost in stationary storage. Research groups are also converging on solid-state electrolytes with protected lithium anodes, placing lithium-air on a credible path toward commercialization. The combined progress strengthens confidence among utilities and data-center operators that multi-day discharge solutions can meet warranty requirements, stimulating procurement pipelines.

Rapid Electric-Vehicle Adoption Requiring Ultra-High Energy Density Packs

Global electric-vehicle sales surpassed 14 million units in 2024 and continue to climb. Automakers seek chemistries delivering 500 km per charge without heavier packs. Metal-air batteries promise three-to-five-fold higher theoretical specific energy compared with lithium-ion. Memoranda of understanding between Phinergy, Hindalco, and Indian Oil target aluminum-air packs that swap aluminum plates in minutes, reshaping refueling logistics. Pilot fleets in China and India are testing range-extender modules, and regulatory incentives for zero-tailpipe emissions accelerate the timeline for commercial platforms.

Limited Cycle Life Compared with Mature Lithium-Ion Chemistries

Laboratory iron-air systems have logged up to 1,696 hours, and rechargeable zinc-air cells now exceed 10,000 hours in the best cases, yet both remain below lithium-ion norms of 3,000-5,000 cycles. Daily-cycling applications, such as frequency regulation or passenger vehicles, therefore still default to lithium-ion. Form Energy positions iron-air for 100-hour discharge at weekly or monthly cycling intervals, sidestepping the heaviest duty profiles. Continued advances in electrolyte carbonation suppression and dendrite control remain prerequisites for broader deployment.

Other drivers and restraints analyzed in the detailed report include:

- Declining Zinc and Aluminum Prices Versus Lithium and Cobalt

- Government Funding for Long-Duration Storage Pilots

- Air-Cathode Carbon Dioxide Poisoning and Catalyst Degradation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Zinc-air batteries are projected to retain a 55.47% share of the metal-air battery market in 2025, primarily due to their continued use in hearing aids and medical electronics, which rely on these batteries for their dependable performance as primary cells. The iron-air segment, supported by Form Energy's extensive multiproject pipeline, is expected to gain a larger share of the metal-air battery market. This segment is expected to register the highest compound annual growth rate (CAGR) of 13.86% during the forecast period of 2026-2031, driven by increasing adoption in various applications.

The growing number of multi-day discharge contracts in grid balancing and data center backup operations underscores the economic viability of iron-air batteries. These batteries are particularly suited for applications where trade-offs between cycle life and round-trip efficiency are acceptable in exchange for a lower cost per stored kilowatt-hour. Concurrently, aluminum-air battery developers are capitalizing on the abundance of aluminum feedstock and the ability to quickly swap metal plates. This approach addresses critical concerns such as range anxiety and refueling downtime, especially in commercial fleet operations. On the other hand, while lithium-air battery technology has shown progress in solid-state prototype development, its mainstream adoption remains outside the current forecast window due to its early-stage nature and ongoing challenges in commercialization.

Primary cells accounted for 60.19% of the metal-air battery market in 2025, driven by their established use in healthcare devices, such as hearing aids, and consumer electronics. These cells continue to dominate due to their reliability and cost-effectiveness in applications requiring consistent performance. Meanwhile, advancements in bifunctional catalysts have significantly extended the lifespan of secondary zinc-air batteries, enabling them to operate for nearly 10,000 hours. This development has opened up new opportunities for their use in stationary energy storage systems and mobility applications, contributing to a projected 13.92% compound annual growth rate (CAGR) for rechargeable zinc-air batteries during the forecast period.

Established players like Duracell, Panasonic, and GP Batteries maintain their stronghold in the button-cell segment, leveraging their extensive distribution networks and brand recognition. However, emerging companies such as EnZinc and Zinc8 are making strides toward scaling modular zinc-air battery packs for applications including community microgrids and commercial buildings. The shift in the metal-air battery market toward secondary configurations is expected to accelerate as manufacturing capacities in regions like the United States and Europe expand to gigawatt-hour annual output levels, further driving innovation and adoption in this segment.

Geography Analysis

Asia-Pacific accounted for 53.79% of the 2025 metal-air battery market, driven by China's extensive manufacturing capabilities, India's strategic aluminum-air collaborations, and Japan's advancements in catalyst science. China is advancing battery-swapping infrastructure through CATL's Choco-Swap ecosystem, which launched in December 2024 with plans to reach 1,000 stations by 2025 and a mid-term target of 10,000 stations, creating a template for metal-slurry refueling systems applicable to aluminum-air and zinc-air batteries. The region benefits from policies that promote local supply chain development and ambitious transportation electrification goals, creating a conducive environment for market growth. Additionally, the presence of key players and ongoing investments in research and development further solidify Asia-Pacific's dominance in the market.

North America is projected to exhibit the highest 14.08% forecast CAGR for 2026-2031. This growth is supported by state-level mandates for long-duration energy storage, funding initiatives from the Department of Energy, and the establishment of Form Energy's manufacturing facility in West Virginia. These factors contribute to a robust domestic ecosystem that spans from foundational research to large-scale field deployment. Furthermore, Canada's focus on low-carbon aluminum production through the ELYSIS venture enhances the region's feedstock sustainability, providing additional support for market expansion.

Europe remains committed to fostering academic-industry collaborations under the Horizon Europe program, allocating EUR 15 million (approximately USD 16.2 million) toward the commercialization of zinc-air batteries. National grid operators in countries like Germany and the United Kingdom are increasingly incorporating multi-day storage solutions into capacity auctions. This strategic focus positions Europe for a significant surge in demand in the future, contingent on achieving key demonstration milestones. The region's emphasis on innovation and regulatory support continues to drive advancements in metal-air battery technologies.

- Arotech Corporation

- Duracell Inc.

- E-Stone Batteries B.V.

- Electric Fuel Battery Corporation

- EnZinc Inc.

- e-Zinc Corporation

- Fuji Pigment Co., Ltd.

- GP Batteries International Limited

- Log9 Materials Scientific Private Limited

- Maxell Holdings, Ltd.

- NantEnergy Inc.

- Panasonic Holdings Corporation

- Phinergy Ltd.

- PolyPlus Battery Company

- Renata SA

- Sunergy Battery Co., Ltd.

- ZAF Energy Systems Inc.

- Zhuhai Zhi Li Battery Co., Ltd. (ZeniPower)

- Zinc8 Energy Solutions Inc.

- Form Energy, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Advances in Rechargeable Zinc- and Lithium-Air Chemistries

- 4.2.2 Rapid EV Adoption Requiring Ultra-High Energy Density Packs

- 4.2.3 Declining Zinc and Aluminum Prices Versus Lithium and Cobalt

- 4.2.4 Government Funding for Long-Duration Storage Pilots

- 4.2.5 Swappable Metal-Slurry Refuel Stations for Commercial EV Fleets

- 4.2.6 National Defense Push for Silent, Lightweight Soldier Power

- 4.3 Market Restraints

- 4.3.1 Limited Cycle Life Compared with Mature Li-ion Chemistries

- 4.3.2 Air-Cathode CO2 Poisoning and Catalyst Degradation

- 4.3.3 Immature Large-Scale Manufacturing Supply Chain

- 4.3.4 Competition for Decarbonised High-Purity Aluminium Feedstock

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Metal Type

- 5.1.1 Zinc-air

- 5.1.2 Aluminum-air

- 5.1.3 Lithium-air

- 5.1.4 Iron-air

- 5.1.5 Other Metal Type

- 5.2 By Battery Type

- 5.2.1 Primary (Non-rechargeable)

- 5.2.2 Secondary (Rechargeable)

- 5.3 By Voltage

- 5.3.1 Low (less than 12 V)

- 5.3.2 Medium (12-36 V)

- 5.3.3 High (greater than 36 V)

- 5.4 By Application

- 5.4.1 Electric Vehicles

- 5.4.2 Stationary Energy Storage

- 5.4.3 Military and Defence Electronics

- 5.4.4 Consumer and Medical Electronics

- 5.4.5 Other Application

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Arotech Corporation

- 6.4.2 Duracell Inc.

- 6.4.3 E-Stone Batteries B.V.

- 6.4.4 Electric Fuel Battery Corporation

- 6.4.5 EnZinc Inc.

- 6.4.6 e-Zinc Corporation

- 6.4.7 Fuji Pigment Co., Ltd.

- 6.4.8 GP Batteries International Limited

- 6.4.9 Log9 Materials Scientific Private Limited

- 6.4.10 Maxell Holdings, Ltd.

- 6.4.11 NantEnergy Inc.

- 6.4.12 Panasonic Holdings Corporation

- 6.4.13 Phinergy Ltd.

- 6.4.14 PolyPlus Battery Company

- 6.4.15 Renata SA

- 6.4.16 Sunergy Battery Co., Ltd.

- 6.4.17 ZAF Energy Systems Inc.

- 6.4.18 Zhuhai Zhi Li Battery Co., Ltd. (ZeniPower)

- 6.4.19 Zinc8 Energy Solutions Inc.

- 6.4.20 Form Energy, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment