|

시장보고서

상품코드

2062456

High K 및 CVD ALD 금속 전구체 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)High-K And CVD ALD Metal Precursors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

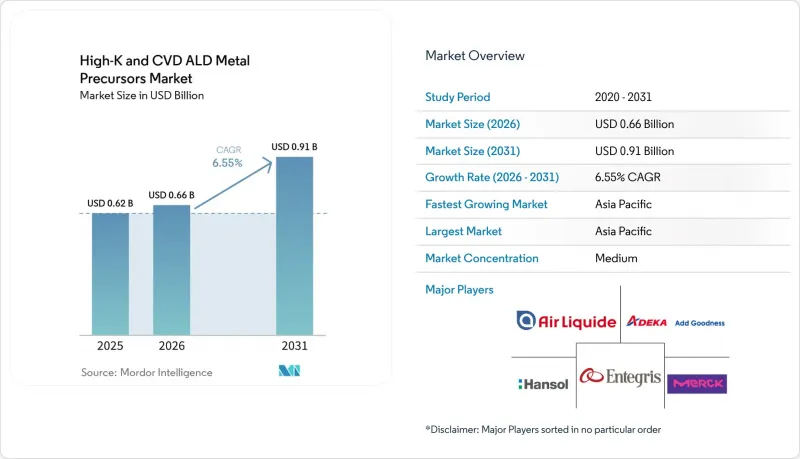

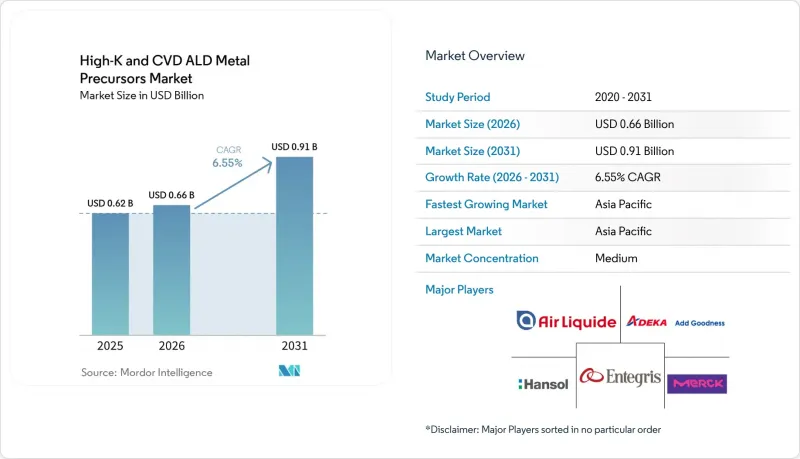

Mordor Intelligence에 의하면, High K 및 CVD ALD 금속 전구체 시장 규모는 2025년 6억 2,000만 달러로 평가되었고, 2026년에는 6억 6,000만 달러로 추정되고, 2031년까지 9억 1,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 6.55%로 성장할 전망입니다.

본 보고서는 금속 유형별(하프늄, 지르코늄, 알루미늄, 코발트, 텅스텐 등), 성막 방법별(열 ALD, 플라즈마 강화 ALD 등), 형태별(액체 전구체, 고체 전구체, 기체 전구체), 최종 용도별(로직 디바이스 FinFET/GAA, 메모리 DRAM, 메모리 3D NAND 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 High K 및 CVD ALD 금속 전구체 시장 동향과 인사이트

3nm 미만의 로직 노드로의 주류 미세화

2나노미터 노드의 게이트 올 어라운드(GAA) 나노시트 설계에서는 랩어라운드 게이트와 후면 전원 네트워크로 인해 필요한 ALD 사이클 수가 2배로 증가하므로, 3나노미터 FinFET에 비해 웨이퍼당 35-50% 더 많은 고유전율 절연체가 소비됩니다. 2025년 하반기부터 양산이 시작될 TSMC의 N2 로직에서는 디바이스 스택의 양면에 하프늄 산화물을 증착하는 반면, 인텔의 18A PowerVia 공정에서는 전구체 부품 목록에 텅스텐으로 만든 실리콘 관통 비아가 추가됩니다. 그 결과 발생하는 전구체 사용량의 급증은 초기 양산 확대 단계에서 팹이 재료를 과잉 조달할 수밖에 없게 되는 ‘수율 학습에 따른 초과’로 인해 더욱 증폭됩니다.

뒷면 전원 공급을 위한 층별 제어

뒷면 전원 배선에는 직경 500나노미터 미만의 실리콘 관통 비아(TSV) 위에 루테늄 또는 텅스텐의 원자층 증착(ALD)이 필요합니다. 이러한 재료들은 이처럼 미세한 규모에서도 성능을 유지할 수 있기 때문에 매우 중요합니다. 인텔의 18A 노드에서는 에너지 손실을 최소화하는 낮은 저항률과, 높은 전류 밀도 하에서 내구성을 높이는 뛰어난 전기이동 저항성을 이유로 특히 루테늄이 선정되었습니다. 또한, Imec의 조사에 따르면, 후면 전원 배선을 채택함으로써 온칩 전압 강하를 약 25% 줄일 수 있으며, 전반적인 전력 공급 효율을 향상시킬 수 있는 것으로 밝혀졌습니다. 그러나 이 레이아웃은 IR 드롭을 대폭 줄이는 반면, 웨이퍼당 전구체 재료 비용을 추정치로 40% 증가시키기 때문에 성능 향상과 제조 비용 사이에서 상충 관계가 발생합니다.

하프늄 금속공급 제약과 가격 변동

지르코늄 채굴과 밀접한 관련이 있는 하프늄의 생산량은 2025년에도 80-90톤에 그쳤습니다. 그러나 하프늄 전구체 수요는 2028년까지 120톤을 넘어설 것으로 예상되어, 큰 수급 격차가 발생할 것으로 보입니다. 이러한 불균형으로 인해 현물 가격이 급등하여 2026년 1분기에는 1Kg당 1,400달러에 달했습니다. 가격 급등으로 인해 반도체 파브는 공급 리스크를 줄이기 위해 재고를 늘리고, 더 많은 안전 재고를 유지하지 않을 수 없게 되었습니다. 서호주주의 새로운 분리 생산 능력 덕분에 2027년까지 15-20톤이 추가될 것으로 예상되지만, 이러한 증가분으로는 예상되는 공급 부족의 극히 일부만 충당할 수 있을 뿐이며, 수요 증가에 대응하기 위한 시장의 압박은 계속될 전망입니다.

부문별 분석

2025년 시장 규모에서 텅스텐계 화학 약품이 45.74%로 가장 큰 점유율을 차지하고 있으며, 이러한 우위는 낮은 저항률과 높은 탄성률이 필수적인 콘택트 플러그 및 워드라인 분야에서 확고한 역할을 수행하고 있다는 점에 기인합니다. 텅스텐 용도의 High-K 및 화학기상증착(CVD), 원자층 증착(ALD)용 금속 전구체 시장은 2025년에 총 매출의 거의 절반을 차지할 것으로 예상되며, 이는 이 소재들이 로직 및 메모리 스택 모두에 광범위하게 통합되고 있음을 반영합니다. 한편, 루테늄은 두께가 5나노미터 미만이어도 우수한 저항률을 유지하고 있으며, 새로운 액체 전구체가 100톨 이상의 안정적인 증기압을 실현하고 있다는 점에서 주목을 받고 있습니다. 지르코늄의 연평균 성장률(CAGR) 6.98%는 강유전체 HfZrO 유전체가 임베디드 메모리 흐름을 어떻게 변화시키고 있는지를 보여줍니다.

앞으로 파운드리 각사가 마이크로컨트롤러 노드 전반에 FeFET를 도입함에 따라, 지르코늄 시장 점유율 확대가 텅스텐의 영역을 위협할 가능성이 있습니다. 하프늄은 7나노미터 이하의 모든 게이트 유전체가 이에 의존하고 있기 때문에 여전히 전략적 금속이지만, 그 공급망은 구조적으로逼迫하고 있습니다. PowerVia의 위험 생산을 통해 입증된, 후면 전원 레일 라이너에서 루테늄의 부상은 파괴적인 재료 구성의 변화를 시사합니다. 코발트와 몰리브덴은 배리어 라이너의 대체 소재로서 틈새 시장이지만 점차 그 역할이 확대되고 있는 반면, 산화알루미늄은 성숙기에 접어든 아날로그 및 파워 디바이스 분야에서 여전히 중요한 위치를 차지하고 있습니다.

열 ALD는 그 간편함 덕분에 2025년 시점에서 48.19%라는 최대 시장 점유율을 유지했으나, 플라즈마 강화 ALD의 연평균 성장률(CAGR) 7.11%는 종횡비 제약이 장비 로드맵을 재편하고 있음을 여실히 보여주고 있습니다. 플라즈마 강화 공정을 위한 High K 및 CVD ALD 금속 전구체 시장 규모는 DRAM 트렌치와 후면 비아 모두에서 원격 플라즈마 화학 공정이 요구됨에 따라, 예측 기간 후반에는 열 공정의 매출을 넘어설 것으로 전망됩니다. 초고주파 플라즈마 소스는 13.56 MHz 시스템에 비해 이온 손상을 절반으로 줄여주며, 감도가 낮은 저유전율 스택의 공정 범위를 확대합니다.

금속 유기 CVD는 분당 5-10 나노미터의 증착 속도를 통해 대량 생산 구조에서 웨이퍼당 비용을 낮게 유지할 수 있기 때문에 두꺼운 텅스텐 충진 및 알루미늄 패드의 기판으로서 여전히 중요한 역할을 하고 있습니다. 공간 ALD 및 하이브리드 ALD-CVD 공정은 여전히 소수이지만, 연속 작동 및 순차적 핵생성의 이점을 중시하는 디스플레이, 태양전지 및 첨단 패키징 분야의 사용자들로부터 주목을 받고 있습니다. 인텔이 18A 비아를 위해 하이브리드 ALD 시드 + CVD 벌크 텅스텐 공정을 공개한 것은 이러한 혼합 공정의 보급이 확대되고 있음을 시사합니다.

지역별 분석

아시아태평양은 한국, 대만, 중국의 막대한 웨이퍼 생산 능력을 반영하여 2025년에는 60.28%의 점유율을 차지했으며, 시장 규모 면에서 압도적인 존재감을 보이고 있습니다. 2024-2026년 해당 지역 내 팹 투자액이 2,000억 달러를 넘어설 것으로 예상에 따라, 2031년까지의 연평균 성장률(CAGR)은 7.21%를 나타낼 것으로 전망됩니다. Samsung Electronics가 재개한 P5 프로젝트와 SK하이닉스의 용인 공장 건설 일정이 앞당겨짐에 따라, 공급업체들은 현지에서 재고를 확보해야 하는 상황에 처해 있습니다. 한편, YMTC와 CXMT는 수출 규제에 대응하기 위해 확장 속도를 높이고 있습니다. 강력한 정책 지원, 노동력 확보, 그리고 확립된 생태계 덕분에 아시아태평양은 현지 임금 수준이 상승했음에도 불구하고 비용 우위를 유지하고 있습니다.

북미는 2025년 매출의 19% 가까이를 차지했으며, CHIPS법에 따른 인센티브가 최소 23개의 신규 팹 건설 또는 확장을 촉진함에 따라 연평균 성장률(CAGR) 약 7%의 궤도에 올라 있습니다. TSMC의 애리조나 공장, 인텔의 오하이오 공장, 삼성의 텍사스 공장은 국내 조달 요건을 충족하기 위해 현지에서 하프늄 및 텅스텐 정제 공장을 공동으로 구축해야 합니다. 에어 리퀴드(Air Liquide), 엔테그리스(Entegris), SK 머티리얼즈(SK Materials)는 이러한 메가 프로젝트 인근에 가스 및 전구체 생산 거점을 건설하기 위해 이미 공사에 착수했습니다.

유럽은 인텔 마그데부르크(Intel Magdeburg)와 ST마이크로일렉트로닉스 크롤레(STMicroelectronics Crolles)의 확장 계획에 힘입어 2025년 지출의 약 11%를 차지하고 있습니다. 자동차 수요와 자국 조달 이니셔티브를 통해 보조금이 확보되는 가운데, 해당 지역의 성장률은 연평균 성장률(CAGR) 6% 전후로 유지되고 있습니다. 중동 및 아프리카와 남미의 합계는 여전히 5% 미만에 그치고 있지만, 브라질의 자동차용 생산 시설과 이스라엘의 방위 관련 거점에서는 고수익률을 자랑하는 특수 제품 분야에서 비즈니스 기회가 예상됩니다. 모든 지역에서 듀얼 소싱과 리드타임 단축을 통해, 여러 개의 ISO 인증 공장을 운영하는 공급업체로 경쟁 우위가 이동하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the high-K and CVD ALD metal precursors market size is expected to increase from USD 0.62 billion in 2025 to USD 0.66 billion in 2026 and reach USD 0.91 billion by 2031, growing at a CAGR of 6.55% over 2026-2031.

This report is Segmented by Metal Type (Hafnium, Zirconium, Aluminum, Cobalt, Tungsten, and More), Deposition Method (Thermal ALD, Plasma-Enhanced ALD, and More), Form (Liquid Precursors, Solid Precursors, and Gas Precursors), End-Use Application (Logic Devices FinFET/GAA, Memory DRAM, Memory 3D NAND, and More ), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global High-K And CVD ALD Metal Precursors Market Trends and Insights

Mainstream Scaling to Sub-3 nm Logic Nodes

Gate-all-around nanosheet designs at 2-nanometer nodes consume 35-50% more high-k dielectric per wafer than 3-nanometer FinFETs because wrap-around gates and backside power networks double the number of ALD cycles required. TSMC's N2 logic, in volume production since late 2025, deposits hafnium oxide on both sides of the device stack, while Intel's 18A PowerVia flow adds tungsten through-silicon vias to the precursor bill of materials. The resulting spike in precursor intensity is magnified by yield-learning overruns that force fabs to over-provision materials during early ramps.

Layer-by-Layer Control for Backside Power Delivery

Backside power routes require ruthenium or tungsten atomic layer deposition (ALD) on through-silicon vias (TSVs) with diameters less than 500 nanometers. These materials are critical because they can maintain performance at such small scales. Intel's 18A node specifically selected ruthenium because of its low resistivity, which minimizes energy loss, and its superior electromigration resistance, which enhances durability under high current densities. Additionally, research from Imec highlights that adopting backside power routing can reduce on-chip voltage droop by approximately 25%, improving overall power delivery efficiency. However, while this layout significantly reduces IR drop, it also increases the cost of per-wafer precursor materials by an estimated 40%, presenting a trade-off between performance gains and manufacturing expenses.

Hafnium Metal Supply Constraints and Price Volatility

Hafnium output, which is intrinsically linked to zirconium mining, remained limited to only 80-90 metric tons in 2025. However, the demand for hafnium precursors is projected to exceed 120 metric tons by 2028, creating a significant supply-demand gap. This imbalance has driven spot prices to surge, reaching USD 1,400 per kilogram in the first quarter of 2026. The rising prices have compelled semiconductor fabs to increase their inventories and maintain higher safety stocks to mitigate supply risks. Although new separation capacity in Western Australia is expected to add 15-20 metric tons by 2027, this increase will address only a fraction of the anticipated shortfall, leaving the market under pressure to meet growing demand.

Other drivers and restraints analyzed in the detailed report include:

- 3D NAND Stacks Above 500 Layers

- EUV-Patterned High-Aspect-Ratio DRAM Capacitors

- Escalating EHS Regulations on Alkyl-Amide and PFAS Ligand Chemistries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tungsten-based chemistries accounted for the largest share with 45.74% in 2025 value, and that dominance rests on their entrenched role in contact plugs and word-lines, where low resistivity and high modulus are vital. The High-K and Chemical Vapor Deposition (CVD) Atomic Layer Deposition (ALD) metal precursors market for tungsten applications accounted for nearly half of overall revenue in 2025, reflecting widespread integration in both logic and memory stacks. Ruthenium, however, is gaining mindshare because its resistivity remains favorable at sub-5-nanometer thicknesses, and new liquid precursors now deliver stable vapor pressures above 100 torr. Zirconium's 6.98% CAGR shows how ferroelectric HfZrO dielectrics are reshaping embedded memory flows.

Looking forward, zirconium's share acceleration could edge into tungsten territory as foundries deploy FeFETs across microcontroller nodes. Hafnium remains a strategic metal because every sub-7 nanometer gate dielectric relies on it, yet its supply chain is structurally tight. Ruthenium's emergence in backside power rail liners, validated by PowerVia risk production, points to a disruptive mix shift. Cobalt and molybdenum occupy niche but growing roles as barrier-liner substitutes, while aluminum oxide stays relevant for mature analog and power devices.

Thermal ALD retained the largest market share at 48.19% in 2025, thanks to its simplicity, but plasma-enhanced ALD's 7.11% CAGR highlights how aspect-ratio pressures are rewriting tool roadmaps. The High-K and CVD ALD metal precursors market size for plasma-enhanced processes is on track to overtake thermal revenue late in the forecast window as DRAM trenches and backside vias both demand remote-plasma chemistries. Very-high-frequency plasma sources cut ion damage in half compared with 13.56 MHz systems, broadening the process window for sensitive low-k stacks.

Metal-organic CVD still underpins thick tungsten fills and aluminum pads because its 5-10 nanometer-per-minute deposition rates keep the cost-per-wafer low for high-volume structures. Spatial ALD and hybrid ALD-CVD flows remain minority shares but are attracting display, solar, and advanced packaging users who value the advantages of continuous motion or sequential nucleation. Intel's public disclosure of a hybrid ALD-seed plus CVD-bulk tungsten approach for 18A vias signals broader acceptance of these mixed regimes.

Geography Analysis

Asia-Pacific dominates value with a 60.28% hold in 2025, reflecting massive wafer capacity across Korea, Taiwan, and China. Regional fab investments exceeding USD 200 billion between 2024-2026 underpin a 7.21% CAGR to 2031. Samsung's restarted P5 project and SK hynix's advanced Yongin timeline force suppliers to pre-position inventory on site, while YMTC and CXMT accelerate expansions to counter export controls. Strong policy support, labor availability, and entrenched ecosystems allow the Asia-Pacific to maintain cost advantages despite a rising local wage base.

North America accounted for close to 19% of 2025 revenue and is on track for roughly a 7% CAGR as CHIPS Act incentives trigger at least 23 new fabs or expansions. TSMC Arizona, Intel Ohio, and Samsung Texas collectively require localized hafnium and tungsten purification plants to satisfy domestic-content mandates. Air Liquide, Entegris, and SK Materials are already breaking ground on gas and precursor campuses adjacent to these megaprojects.

Europe controls about 11% of 2025 spend, buoyed by Intel Magdeburg and STMicroelectronics Crolles expansions. Regional growth hovers near 6% CAGR as automotive demand and sovereignty initiatives lock in subsidies. The Middle East, Africa, and South America remain sub-5% combined, yet Brazilian automotive fabs and Israeli defense nodes present high-margin specialty opportunities. Across all regions, dual sourcing and shorter lead-times shift competitive advantage toward suppliers operating multiple ISO-certified plants.

- Air Liquide S.A.

- ADEKA Corporation

- Merck KGaA

- Entegris Inc.

- Hansol Chemical Co., Ltd.

- DNF Co., Ltd.

- Soulbrain Co., Ltd.

- UP Chemical Co., Ltd.

- Tanaka Kikinzoku Kogyo K.K.

- Strem Chemicals, Inc.

- Versum Materials LLC

- SK Trichem Co., Ltd.

- SK Materials Co., Ltd.

- Gelest, Inc.

- Air Products and Chemicals, Inc.

- Jiangsu Yoke Technology Co., Ltd.

- Solvay S.A.

- Nanmat Technology Co., Ltd.

- Mecaro Co., Ltd.

- EpiValence Ltd.

- American Elements

- Botai Electronic Material Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mainstream Scaling to Sub-3 nm Logic Nodes

- 4.2.2 Layer-by-Layer Atomic-Scale Control Enabling Backside Power Delivery

- 4.2.3 3D-NAND Stacks Above 500 Layers Multiplying ALD Precursor Volumes

- 4.2.4 EUV-Patterned High-Aspect-Ratio DRAM Trench Capacitors

- 4.2.5 Rapid Build-Out of Chinese, Korean and US Fab Clusters Post-CHIPS Acts

- 4.2.6 Ferroelectric HfZrO Devices for Embedded Non-Volatile Memory in IoT Edge

- 4.3 Market Restraints

- 4.3.1 Hafnium Metal Supply Constraints and Price Volatility

- 4.3.2 Escalating EHS Regulations on Alkyl-Amide and PFAS Ligand Chemistries

- 4.3.3 Capex Intensity of Solid-Precursor Sublimation and Delivery Systems

- 4.3.4 Plasma Damage-Induced Defectivity Narrowing PE-ALD Process Windows

- 4.4 Industry Value-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Metal Type

- 5.1.1 Hafnium

- 5.1.2 Zirconium

- 5.1.3 Aluminum

- 5.1.4 Cobalt

- 5.1.5 Tungsten

- 5.1.6 Ruthenium

- 5.1.7 Other Metal Type

- 5.2 By Deposition Method

- 5.2.1 Thermal ALD

- 5.2.2 Plasma-Enhanced ALD

- 5.2.3 Metal-Organic CVD

- 5.2.4 Spatial ALD

- 5.2.5 Hybrid ALD-CVD

- 5.3 By Form

- 5.3.1 Liquid Precursors

- 5.3.2 Solid Precursors

- 5.3.3 Gas Precursors

- 5.4 By End-Use Application

- 5.4.1 Logic Devices, FinFET/GAA

- 5.4.2 Memory, DRAM

- 5.4.3 Memory, 3D NAND

- 5.4.4 Emerging Memory (RRAM, MRAM, Fe-FET)

- 5.4.5 Interconnects and Metallization

- 5.4.6 Analog, Power and Specialty Devices

- 5.5 By Geography

- 5.5.1 North America

- 5.5.2 South America

- 5.5.3 Europe

- 5.5.4 Asia-Pacific

- 5.5.5 Middle East

- 5.5.6 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Air Liquide S.A.

- 6.4.2 ADEKA Corporation

- 6.4.3 Merck KGaA

- 6.4.4 Entegris Inc.

- 6.4.5 Hansol Chemical Co., Ltd.

- 6.4.6 DNF Co., Ltd.

- 6.4.7 Soulbrain Co., Ltd.

- 6.4.8 UP Chemical Co., Ltd.

- 6.4.9 Tanaka Kikinzoku Kogyo K.K.

- 6.4.10 Strem Chemicals, Inc.

- 6.4.11 Versum Materials LLC

- 6.4.12 SK Trichem Co., Ltd.

- 6.4.13 SK Materials Co., Ltd.

- 6.4.14 Gelest, Inc.

- 6.4.15 Air Products and Chemicals, Inc.

- 6.4.16 Jiangsu Yoke Technology Co., Ltd.

- 6.4.17 Solvay S.A.

- 6.4.18 Nanmat Technology Co., Ltd.

- 6.4.19 Mecaro Co., Ltd.

- 6.4.20 EpiValence Ltd.

- 6.4.21 American Elements

- 6.4.22 Botai Electronic Material Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment