|

시장보고서

상품코드

2062457

다기능 디스플레이 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Multi-Function Display - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

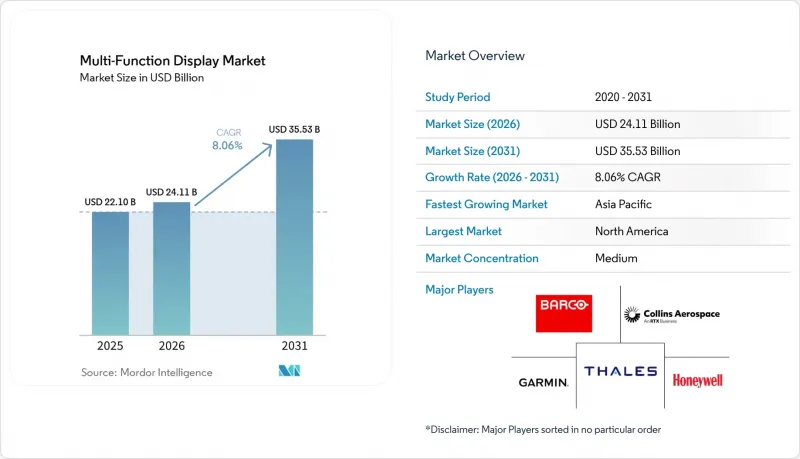

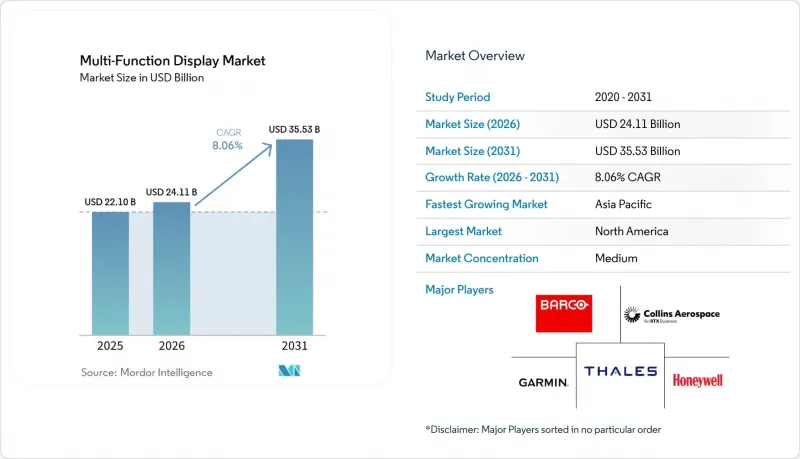

Mordor Intelligence에 의하면, 다기능 디스플레이 시장 규모는 2025년 221억 달러로 평가되었습니다. 2026년 241억 1,000만 달러에서 2031년까지 355억 3,000만 달러로 확대되고 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 8.06%를 나타낼 것으로 예측됩니다.

본 보고서는 플랫폼(항공기, 지상, 해군, 우주 및 무인항공기), 기술(LCD/AMLCD, LED/TFT 등), 최종 이용 산업(항공우주 및 방위, 자동차, 기타), 디스플레이 크기(5인치 미만, 5-10인치, 10-15인치, 15인치 이상과), 시스템 유형(헤드업 디스플레이, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 다기능 디스플레이 시장 동향 및 인사이트

민간 및 군용 항공기의 지속적인 인도

에어버스와 보잉의 사상 최대 수주 잔고로 인해 향후 10년 동안 생산 일정이 계속 채워질 전망이며, 이는 단일 통로형 조종실에 적합한 10-15인치 크기의 주 비행 패널 및 다기능 패널에 대한 수요를 뒷받침하고 있습니다. 미국 공군의 C-17 글라스 콕핏 개조나 인도의 테자스 Mk2 시리즈 등, 리드타임이 긴 전투기 업그레이드 프로젝트는 기체 1대당 전시 가치를 높이고 있습니다. 이는 각 개보수 작업에서 노후화된 브라운관 모니터가 소프트웨어의 확장성을 고려하여 설계된 모듈식 LCD 시스템으로 교체되기 때문입니다. 오픈 시스템 표준 덕분에 항공기 제조업체는 하드웨어 조달과 임무용 소프트웨어 개발을 분리할 수 있게 되었으며, 이로 인해 조달처가 더 폭넓은 공급업체 기반으로 분산되는 한편, 신규 제조 주기를 넘어 다기능 디스플레이 시장이 유지됨에 따라 독립 공급업체들도 혜택을 보고 있습니다.

자동차 운전석의 급속한 디지털화

고급 자동차 브랜드와 전기차(EV) 스타트업 기업들은 현재 광활한 곡면 클러스터를 핵심 브랜드 정체성으로 삼고 있으며, 아날로그 계기판, 인포테인먼트, 운전 보조 그래픽을 베젤이 없는 단일 OLED 또는 TFT 화면에 통합하고 있습니다. 이러한 통합을 통해 배선의 복잡성이 줄어들고, 무선(OTA) 업데이트 가능성이 높아지며, 모델 변경에 소요되는 리드타임이 단축됩니다. 15인치를 초과하는 곡면 패널은 유럽의 프리미엄 차량과 중국의 신에너지 차량의 계기판에 채택되고 있으며, 패널 제조업체들은 자동차용 OLED 생산 능력을 확대하고 다기능 디스플레이 시장을 강화하도록 촉구받고 있습니다. ISO 26262 및 UNECE R155에 기반한 기능 안전 및 사이버 보안 검증은 개발 비용을 증가시키지만, 궁극적으로는 새로운 문서화 요건을 충족할 수 있는 공급업체를 확보하는 결과를 가져옵니다.

OLED 및 MicroLED 패널의 높은 BOM 비용

유기 발광 및 마이크로 발광 기술은 타의 추종을 불허하는 명암비와 저전력 소비를 보장하지만, 박막 형성 수율의 저하, 복잡한 밀봉 공정, 엄격한 결함 허용 한도로 인해 여전히 AMLCD보다 40-60% 높은 제조 비용이 소요됩니다. 자동차 양산 제조업체들은 프리미엄 등급을 제외한 모델에 OLED를 채택하는 데 소극적인 반면, 산업용 구매자들은 설비 투자를 억제하기 위해 LCD를 유지하고 있습니다. 최근 중국 내 8.6세대 공장의 수율 개선으로 격차는 점차 좁혀지고 있지만, 2028년 이전에 가격이 동등해질 가능성은 낮아, 이로 인해 다기능 디스플레이 시장에서 발광형 기판으로의 단기적인 전환이 억제되고 있습니다.

부문별 분석

2025년, 항공기용 프로그램은 다기능 디스플레이 시장 점유율의 46.18%를 차지했습니다. 이는 민간 제트기의 미수주 물량과 전투기 현대화 사업이 조달을 주도하고 있기 때문입니다. C-17의 항공전자 장비 교체와 같은 기체 유지 관리 계획 덕분에, 신규 생산 대수가 감소하더라도 기존 기체를 위한 다기능 디스플레이 시장 규모는 유지되고 있습니다. 이와 함께 성장이 예상되는 분야는 UAV(무인 항공기)의 지상 관제소 및 우주 지휘 콘솔입니다. 이 제품들은 텔레메트리 데이터를 실시간으로 전송하는 내구성이 뛰어나고 저전력 소비의 AMLCD 또는 OLED 모듈을 주로 채택하고 있습니다. 플랫폼의 다양성으로 인해 인증 기준은 세분화되어 있습니다. 항공기용 모듈은 DO-160을 준수하고, 해군용 장비는 MIL-STD-461을 충족하며, 자동차용 계기판은 ISO 26262를 준수하기 때문입니다.

우주선, 위성, 드론의 경우, 내방사선 패널이 틈새 조사 분야에서 주류인 저궤도 위성군으로 전환됨에 따라, 플랫폼 중 가장 높은 연평균 성장률(CAGR) 8.68%를 나타낼 것으로 전망됩니다. 디스플레이 설계에서는 색 심도보다 저전력성과 열적 안정성이 더 중요시되고 있지만, 발사가 예정된 위성 버스(플랫폼)의 수가 방대함에 따라 다기능 디스플레이 시장은 확대되고 있습니다. 한편, 지상 차량 분야에서는 국방 및 민간 규격이 뒤죽박죽으로 혼재되어 있어 플랫폼 간 규모의 경제 효과는 둔화되고 있지만, 의무화된 노후화 관리 계약을 통해 안정적인 애프터마켓 수익이 확보되고 있습니다.

LCD 및 AMLCD는 성숙한 제조 설비, 안정적인 백라이트 공급, 그리고 10인치 항공기용 패널 시장 가격이 50달러라는 점 등을 배경으로, 2025년에도 다기능 디스플레이 시장에서 51.37%의 점유율을 유지했습니다. 양자점 및 미니LED 백라이트는 밝기와 조광 구역을 단계적으로 향상시켜, 완전 발광형 기판으로의 전환을 원활하게 하고 있습니다. 자동차 제조업체와 전투기 프로그램이 베젤이 없고 명암비가 높은 인터페이스를 요구하는 가운데, OLED, QD-OLED 및 신기술인 마이크로 LED는 연평균 성장률(CAGR) 8.91%를 나타낼 전망입니다. 비용과 차별화의 균형을 잘 맞춘 곡면 OLED 계기판이 중형차에 채택됨에 따라, 발광형 패널이 차지하는 다기능 디스플레이 시장 점유율은 더욱 확대될 전망입니다.

중국의 8.6세대 생산 라인에서는 2025년에 수율이 85%를 넘어섰으며, AMLCD와 OLED 간의 비용 격차가 줄어들었습니다. 방위 분야 구매자들은 OLED의 무한한 명암비를 활용해 야간 투시 기능과의 호환성을 높이고, 조종석 주변을 감싸는 듯한 유연한 형태를 채택하고 있습니다. MiniLED는 LCD 공정의 익숙한 방식을 유지하면서 로컬 디밍 기능을 제공하는 과도기적인 솔루션으로 기능하고 있습니다. 기술 간 경쟁으로 인해 패널 제조업체들은 화소 불량 보정 알고리즘이나 저전력 구동 방식을 통해 차별화를 꾀하고 있으며, 이로 인해 다기능 디스플레이 시장에서 독자적으로 개발한 드라이버 IC의 가치가 높아지고 있습니다.

지역별 분석

북미는 2025년에도 미국 국방부의 지속적인 플랫폼 유지 관리와 FAA(연방항공청)의 개조 규정 준수 주기에 힘입어 34.98%라는 최고 점유율을 유지했습니다. C-17의 조종석 개편 및 미 해군의 슈퍼호넷 중간 수명 연장 업그레이드 프로젝트에서는 모두 소프트웨어와 하드웨어를 분리된 개방형 아키텍처의 디스플레이가 규정되어 있으며, 이를 통해 경쟁이 촉진되는 동시에, 실적이 입증되고 사이버 보안 대책이 마련된 제품을 제공하는 기존 제조업체의 가치도 유지되고 있습니다. 캐나다의 북극권 감시 활동에서 우선순위가 높아짐에 따라, CP-140 순찰기를 위한 내한 사양 패널에 대한 수요가 증가하고 있습니다. 한편, 멕시코의 자동차 수출 모델에는 미국과 유럽 시장의 인포테인먼트에 대한 기대에 부응하기 위해 디지털 계기판이 탑재되어 있습니다.

중국의 민간 항공기 보유 대수가 두 배로 증가하고 국산 전투기 생산 라인이 성숙함에 따라, 아시아태평양은 2031년까지 연평균 성장률(CAGR) 8.61%라는 가장 높은 성장률을 나타낼 것으로 전망됩니다. COMAC의 C919 및 ARJ21 제트기는 수입 의존도를 낮추기 위해 현지에서 조달된 AMLCD 시스템을 통합하고 있으며, 이를 통해 국내 공급망의 성숙도를 높이고 있습니다. 인도의 ‘테자스 Mk2’ 및 ‘첨단 중형 전투기(AMCA)’의 헤드업 디스플레이와 헬멧 시스템은 고대비 OLED 바이저의 현지 생산을 확대되고 있습니다. 일본 해상자위대의 장비 현대화와 한국의 KF-21 개발은 해군 및 항공우주 분야에서 안정적인 수요를 창출하고 있는 반면, 호주의 헌터급 호위함은 국방·해사 분야의 통합을 활기차게 유지하고 있습니다. 동남아시아 전역에서는 ADS-B 및 ICAO 규격에 따른 개조로 인해 노후화된 협폭기 기종의 조종실 디스플레이 수요가 점차 확대되면서, 다기능 디스플레이 시장 규모가 커지고 있습니다.

유럽에서는 데이터 링크 항공전자 장비와 첨단 감시 기능을 결합한 SESAR(단일 유럽 항공 공간 관리)의 요구 사항에 맞추어 기체 현대화가 진행되고 있습니다. 툴루즈, 함부르크, 세비야에 위치한 에어버스의 최종 조립 거점은 AMLCD 유닛의 기본 생산량을 보장하고 있는 반면, 영국의 ‘템페스트’와 프랑스의 항공모함 탑재 전투기 프로그램에서는 파노라마형 OLED 또는 대면적 디스플레이가 규정되어 있습니다. 중동, 주로 사우디아라비아와 아랍에미리트연합(UAE)의 지출은 현지 조립에 대한 상쇄 조항이 포함된 전투기 및 해군 장비 조달을 대상으로 하며, 전 세계 공급업체들에게 이 지역 내 제조 체계 구축을 과제로 제시하고 있습니다. 남미와 아프리카는 절대 수치상으로는 뒤처져 있지만, 해상 에너지 시설이나 철도 관제 센터에서는 내환경성 패널이 채택되고 있으며, 이것이 다기능 디스플레이 시장에서 롱테일 기회를 창출하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the multi-function display market size is projected to expand from USD 22.10 billion in 2025 and USD 24.11 billion in 2026 to USD 35.53 billion by 2031, registering a CAGR of 8.06% between 2026 and 2031.

This report is Segmented by Platform (Airborne, Land-Based, Naval, and Space and UAV), Technology (LCD/AMLCD, LED/TFT, and More), End-Use Industry (Aerospace and Defense, Automotive, and More), Display Size (Less Than 5 Inches, 5-10 Inches, 10-15 Inches, and Greater Than 15 Inches), System Type (Head-Up Displays, and More, and Geography. The Market Forecasts are Provided in Terms of Value (USD)).

Global Multi-Function Display Market Trends and Insights

Ongoing Commercial and Military Aircraft Deliveries

Record order backlogs at Airbus and Boeing keep production slots filled through the decade, anchoring demand for 10-15 inch primary flight and multi-function panels that fit single-aisle cockpits. Long-lead fighter upgrades such as the U.S. Air Force C-17 glass-cockpit retrofit and India's Tejas Mk2 line elevate per-airframe display value, because each retrofit replaces aging cathode-ray tubes with modular LCD suites designed for software extensibility. Independent suppliers benefit as open-system standards let airframers decouple hardware sourcing from mission software development, which diffuses procurement across a wider vendor base while sustaining the multi-function display market beyond new-build cycles.

Rapid Digitization of Automotive Cockpits

Luxury marques and electric-vehicle startups now position expansive curved clusters as core brand identifiers, compressing analog gauges, infotainment, and driver-assistance graphics into a single bezel-free OLED or TFT surface. This consolidation reduces wiring complexity, enhances the potential for over-the-air upgrades, and shortens model-refresh timelines. Curved panels exceeding 15 inches are used on instrument panels across European premium and Chinese new-energy vehicles, encouraging panel makers to scale automotive-grade OLED capacity and to reinforce the multi-function display market. Functional-safety and cybersecurity validations, guided by ISO 26262 and UNECE R155, add development overhead but ultimately lock in suppliers capable of meeting the new documentation load.

High BOM Cost of OLED and MicroLED Panels

Organic-emissive and micro-emissive technologies promise unmatched contrast and power thrift, yet they still command 40-60% higher manufacturing costs than AMLCDs due to low deposition yields, complex encapsulation, and tight defect tolerances. Automotive volume builders hesitate to specify OLED outside premium trims, while industrial buyers retain LCD to contain capital expenditure. Yield improvements at recent 8.6-generation Chinese fabs are narrowing the gap, but price parity is unlikely before 2028, tempering the multi-function display market's near-term tilt toward emissive substrates.

Other drivers and restraints analyzed in the detailed report include:

- Defense Modernization Programmes in Asia and Middle East

- Regulatory Mandates, ADS-B, NextGen, SESAR

- Display Burn-In and Reliability Certification Hurdles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Airborne programs secured 46.18% of the multi-function display market share in 2025, as commercial jet backlogs and fighter modernization dominate procurement. Fleet sustainment initiatives, such as the C-17 avionics refresh, replenish the multi-function display market size for existing aircraft even when new-build rates soften. Parallel growth stems from UAV ground-control stations and space-command consoles, which favor rugged, low-power AMLCD or OLED modules that communicate telemetry in real time. Platform diversity splinters qualification regimes, because airborne modules follow DO-160, naval installations meet MIL-STD-461, and automotive clusters adhere to ISO 26262.

Spacecraft, satellites, and drones are projected to register an 8.68% CAGR, the fastest among platforms, as radiation-hardened panels migrate from niche research to mainstream low-Earth-orbit constellations. Screen designs emphasize power thrift and thermal stability over color depth, but the sheer volume of satellite buses scheduled for launch broadens the market for multi-function displays. Meanwhile, land-vehicle applications follow a patchwork of defense and civil standards, slowing cross-platform economies of scale yet ensuring stable aftermarket revenues through mandatory obsolescence-management contracts.

LCD and AMLCD kept 51.37% multi-function display market share in 2025 on the back of mature tooling, stable backlight supply, and USD 50 street pricing for 10-inch aeronautical-grade panels. Quantum-dot and miniLED backlights add incremental brightness and dimming zones, smoothing the transition to fully emissive substrates. OLED, QD-OLED, and emerging micro-LED variants will climb at an 8.91% CAGR as carmakers and fighter programs demand bezel-free, high-contrast interfaces. The multi-function display market share allocated to emissive panels is poised to expand further as mid-range automobiles adopt curved OLED clusters that balance cost with differentiation.

China's 8.6-generation lines improved yields beyond 85% in 2025, compressing the AMLCD-OLED cost gap. Defense buyers exploit OLED's infinite contrast to boost night-vision compatibility and adopt flexible form factors that wrap around cockpit perimeters. MiniLED serves as a transitory solution, preserving LCD process familiarity while furnishing local dimming. Inter-technology competition is prompting panel makers to differentiate through pixel-failure compensation algorithms and low-power drive schemes, reinforcing the value of proprietary driver ICs in the multi-function display market.

Geography Analysis

North America maintained the highest 34.98% multi-function display market share in 2025, anchored by the United States Department of Defense's ongoing platform sustainment and the FAA's retrofit compliance cycles. The C-17 cockpit refresh and the U.S. Navy Super Hornet mid-life upgrade both stipulate open-architecture displays that keep software decoupled from hardware, thereby fostering competition while preserving value for incumbents with proven, cyber-secure offerings. Canadian Arctic surveillance priorities add demand for cold-weather-rated panels in CP-140 patrol aircraft, while Mexico's automotive exports embed digital clusters to meet infotainment expectations in the United States and Europe.

Asia-Pacific will progress at the fastest 8.61% CAGR through 2031 as China's civil fleet doubles and indigenous fighter lines mature. COMAC's C919 and ARJ21 jets integrate locally sourced AMLCD suites to reduce import dependency, thereby boosting domestic supply-chain maturity. India's Tejas Mk2 and Advanced Medium Combat Aircraft head-up and helmet systems amplify regional production of high-contrast OLED visors. Japan's maritime upgrades and South Korea's KF-21 development furnish steady naval and aerospace pull, whereas Australia's Hunter-class frigates keep defense-marine integration buoyant. Across Southeast Asia, ADS-B and ICAO compliance retrofits unlock incremental cockpit-display demand in aging narrow-body fleets, multiplying the multi-function display market footprint.

Europe embraces fleet refreshes tied to SESAR mandates that couple datalink avionics with advanced surveillance. Airbus final-assembly hubs in Toulouse, Hamburg, and Seville guarantee base-load production of AMLCD units, while the UK's Tempest and France's carrier-borne fighter programs stipulate panoramic OLED or large-area displays. Middle Eastern outlays, primarily from Saudi Arabia and the United Arab Emirates, target fighter and naval procurements that carry local-assembly offset clauses, challenging global suppliers to embed regional manufacturing. South America and Africa trail in absolute numbers, yet offshore energy installations and rail control centers adopt ruggedized panels that seed long-tail opportunities within the multi-function display market.

- Aspen Avionics Inc.

- Avidyne Corporation

- Barco NV

- Collins Aerospace (RTX Corporation)

- Curtiss-Wright Corporation

- Dynon Avionics Inc.

- Elbit Systems Ltd.

- Esterline Technologies LLC (TransDigm Group)

- Garmin Ltd.

- Honeywell International Inc.

- L3Harris Technologies Inc.

- Mercury Systems Inc.

- Mid-Continent Instruments and Avionics Inc.

- Northrop Grumman Corporation

- Samtel Avionics Ltd.

- SAAB AB

- Thales Group

- Transas (Wartsila Voyage Ltd.)

- Universal Avionics Systems Corporation

- BAE Systems plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ongoing Commercial and Military Aircraft Deliveries

- 4.2.2 Rapid Digitization of Automotive Cockpits

- 4.2.3 Defense Modernization Programmes in Asia and Middle East

- 4.2.4 Regulatory Mandates, ADS-B, NextGen, SESAR

- 4.2.5 China's Low-Cost AMLCD Capacity Expansion

- 4.2.6 AR-Ready Marine Navigation Displays

- 4.3 Market Restraints

- 4.3.1 High BOM Cost of OLED and MicroLED Panels

- 4.3.2 Display Burn-In and Reliability Certification Hurdles

- 4.3.3 Semiconductor and Specialty-Glass Supply Chain Risks

- 4.3.4 Escalating Cockpit-HMI Cybersecurity Requirements

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Platform

- 5.1.1 Airborne

- 5.1.2 Land-Based (Ground and Automotive)

- 5.1.3 Naval

- 5.1.4 Space and UAV

- 5.2 By Technology

- 5.2.1 LCD / AMLCD

- 5.2.2 LED / TFT

- 5.2.3 OLED / QD-OLED

- 5.2.4 MiniLED and MicroLED

- 5.3 By End-Use Industry

- 5.3.1 Aerospace and Defense

- 5.3.2 Automotive

- 5.3.3 Maritime

- 5.3.4 Industrial and Energy

- 5.3.5 Other End-Use Industries

- 5.4 By Display Size

- 5.4.1 Less Than 5 Inches

- 5.4.2 5-10 Inches

- 5.4.3 10-15 Inches

- 5.4.4 Greater Than 15 Inches

- 5.5 By System Type

- 5.5.1 Electronic Flight Displays

- 5.5.2 Head-Up Displays

- 5.5.3 Helmet-Mounted Displays

- 5.5.4 Portable / Hand-Held MFDs

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East

- 5.6.4.1 Saudi Arabia

- 5.6.4.2 United Arab Emirates

- 5.6.4.3 Rest of Middle East

- 5.6.5 Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Egypt

- 5.6.5.3 Rest of Africa

- 5.6.6 South America

- 5.6.6.1 Brazil

- 5.6.6.2 Argentina

- 5.6.6.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Aspen Avionics Inc.

- 6.4.2 Avidyne Corporation

- 6.4.3 Barco NV

- 6.4.4 Collins Aerospace (RTX Corporation)

- 6.4.5 Curtiss-Wright Corporation

- 6.4.6 Dynon Avionics Inc.

- 6.4.7 Elbit Systems Ltd.

- 6.4.8 Esterline Technologies LLC (TransDigm Group)

- 6.4.9 Garmin Ltd.

- 6.4.10 Honeywell International Inc.

- 6.4.11 L3Harris Technologies Inc.

- 6.4.12 Mercury Systems Inc.

- 6.4.13 Mid-Continent Instruments and Avionics Inc.

- 6.4.14 Northrop Grumman Corporation

- 6.4.15 Samtel Avionics Ltd.

- 6.4.16 SAAB AB

- 6.4.17 Thales Group

- 6.4.18 Transas (Wartsila Voyage Ltd.)

- 6.4.19 Universal Avionics Systems Corporation

- 6.4.20 BAE Systems plc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment