|

시장보고서

상품코드

2062459

고빈도 거래 서버 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)High Frequency Trading Server - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

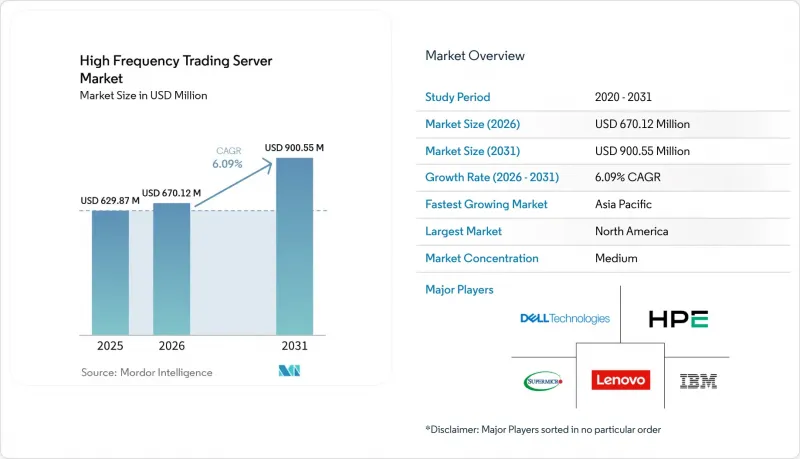

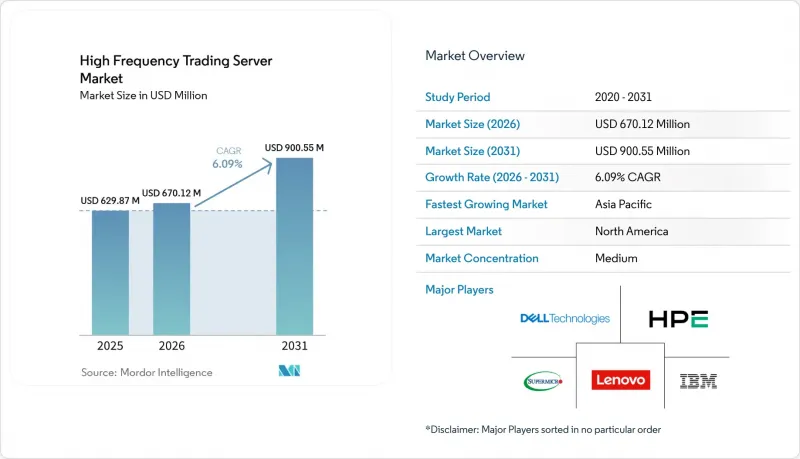

Mordor Intelligence에 의하면, 고빈도 거래용 서버 시장 규모는 2025년에 6억 2,987만 달러로 평가되었고, 2026년 6억 7,012만 달러로 추정되고, 2031년까지 9억 55만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 6.09%를 나타낼 전망입니다.

본 보고서는 프로세서 아키텍처별(x86 기반 서버, ARM 기반 서버 등), 폼 팩터별(랙 서버, 블레이드 서버 등), 용도별(주식 거래, 외환 등), 최종 사용자별(자사 거래 회사 및 시장 조성자, 투자 은행 및 증권사 등), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 고빈도 거래 서버 시장 동향 및 분석

알고리즘 및 AI 주도 거래량의 급증

선진국의 거래 시장에서 알고리즘에 의한 체결은 주식 주문 흐름의 70% 이상을 차지하고 있으며, 현재는 강화 학습 에이전트가 FPGA 패브릭에 직접 통합되어 티크에서 거래까지의 주기를 나노초 단위로 단축하고 있습니다. 2026년 2월 유럽증권시장감독청(ESMA)이 발표한 지침에 따르면, 마이크로초 단위의 거래 전 점검이 의무화되었으며, 클라우드 엔드포인트보다 온프레미스 컴퓨팅이 우선시되고 있습니다. 100억 달러 이상의 자산을 운용하는 퀀트 펀드는 거래소 엔진에 인접한 곳에 추론 기능을 갖춘 서버를 도입하여, 마이크로초 단위의 처리 시간 단축을 수백만 달러 규모의 슬리피지 감소로 연결하고 있습니다. 메모리 대역폭에 대한 수요가 증가함에 따라, 초당 1테라바이트의 코히런트 대역폭을 제공하는 NVIDIA Grace와 같은 ARM 설계의 도입이 가속화되고 있습니다. 그 결과, 주요 콜로케이션 거점 전반에 걸쳐 이종 서버의 출하 대수가 구조적으로 증가하고 있습니다.

초저지연 인프라에 대한 수요

거래소 인근 호스트는 10기가비트에서 400기가비트 이더넷으로 업그레이드되어 왕복 시간을 1마이크로초 미만으로 단축했으며, 네트워크 인터페이스 카드의 최소 사양을 새롭게 설정했습니다. 크라켄은 2026년 4월, Equinix LD5에 런던 케이지를 개설하여 유럽 거래소까지 1밀리초 미만의 접속 시간을 실현함으로써, 결정론적 흐름을 필요로 하는 암호화폐 시장 조성자들을 유치하고 있습니다. CME Aurora는 Google Cloud와 제휴하여 428,000제곱피트 규모의 고가 바닥 공간을 증설했습니다. 이를 통해 듀얼 소켓 블레이드 노드 및 FPGA 가속기를 지원하는 17kW 캐비닛을 제공합니다. DPDK나 RDMA와 같은 커널 바이패스 스택은 현재 거래용 NIC의 필수 기능이 되었으며, 서버 설계와 네트워크 토폴로지의 연계가 더욱 강화되고 있습니다.

콜로케이션 및 전용 냉각 시스템에 대한 막대한 설비 투자

Tier 1 거래소 인접 캐비닛은 10기가비트 연결 기준으로 월 6,000-9,600달러, 프리미엄 케이지는 월 1만 5,000달러이며, 크로스 커넥트를 포함하면 랙당 연간 15만 달러가 넘는 비용이 발생합니다. 액체 냉각으로의 업그레이드에는 초기 비용으로 5만-10만 달러가 소요되므로, 중견 헤지펀드는 지연 시간 개선 효과와 예산 제약을 저울질할 수밖에 없습니다. 냉수 순환 시스템이 없는 구형 홀에서는 고밀도 블레이드 서버로 개조하는 것이 불가능하며, 이로 인해 신축 시설로의 전환이 촉진되고 투자 회수 기간이 길어지고 있습니다. 일부 기업은 가상 사설 서버로의 전환을 선택하여 20마이크로초의 지연 시간을 감수하는 대신월2,000달러 미만의 비용을 실현하고 있으며, 이로 인해 최첨단 하드웨어에 대한 수요가 세분화되고 있습니다.

부문별 분석

기업들이 에너지 효율과 메모리 대역폭을 우선시하는 가운데, ARM 기반 서버는 2026년부터 2031년까지 연평균 성장률(CAGR) 8.43%라는 가장 높은 성장률을 기록했습니다. 72개의 Arm Neoverse V2 코어와 초당 1테라바이트의 대역폭을 갖춘 NVIDIA Grace CPU가 2025년에 출시됨에 따라, 과거에는 듀얼 소켓 x86 시스템이 필요했던 실시간 위험 시뮬레이션이 가능해졌습니다. x86 시스템은 인텔 및 AMD 마이크로우코드에 최적화된 수십 년간 축적된 사전 컴파일된 거래 로직에 힘입어, 2025년 고빈도 거래 서버 시장 점유율의 74.32%를 차지하며 여전히 지배적인 위치를 유지하고 있습니다.

ARM의 전력 밀도 측면에서의 우위는 대부분의 경우 30-40%에 달하며, 이는 kW당 수익을 추구하는 코로케이션 사업자에게 유리한 점입니다. 재컴파일 과정의 난관이나 ARM 네이티브 FPGA 툴의 부족으로 인해 중소기업의 전환이 지연되고 있지만, 2026년 3월 후지쯔·Arrcus·1Finity간의 제휴 등은 차세대 케이지용 ARM 설계에 대한 신뢰가 높아지고 있음을 보여줍니다.

블레이드 서버 시장은 2031년까지 연평균 성장률(CAGR) 7.84%를 나타낼 것으로 예측되며, 신규 구축 시장에서 랙 시스템을 앞지를 전망입니다. 시스코의 UCS XE9305 섀시는 10U 섀시에 16대의 듀얼 소켓 노드를 탑재하여, 랙 상단 스위치의 지연을 제거함과 동시에 평방피트당 연산 성능을 극대화합니다. 2025년, 랙 서버는 고빈도 거래 서버 시장에서 63.47%의 점유율을 유지했으며, 이는 저전력 환경으로의 사이트 개편에 있어 뛰어난 유연성을 반영한 것입니다.

수냉식 블레이드 섀시는 대규모 개조 없이 17kW 캐비닛을 유지할 수 있어, 거래소 호스트들이 밀도 한계를 높여가는 상황에서 이는 큰 장점이 됩니다. 슈퍼마이크로가 2026년 3월에 발표한 40노드 MicroBlade는 노드당 설치 면적을 50% 줄임으로써, 바닥 면적에 대한 경제적 부담을 부각시켰습니다. 개조 작업의 제약으로 인해 랙 서버의 보급은 유지되겠지만, 신규 도입에서는 블레이드 서버가 점점 더 표준이 될 것입니다.

지역별 분석

2025년, 북미는 고빈도 거래 서버 시장의 36.51%를 차지했으며, CME Aurora, NYSE Mahwah, Nasdaq Carteret이 이를 주도했습니다. CME와 Google Cloud의 제휴를 통해 428,000제곱피트의 추가 레이즈드 플로어가 제공됨에 따라, 블레이드와 FPGA 하이브리드 구성에 적합한 17kW 캐비닛을 도입할 수 있게 되었습니다. ICE 마호와는 2026년 1월, 28메가와트의 전력 공급과 1마이크로초 미만의 정밀도를 자랑하는 타임 프로토콜을 통해 Tier 4 수준의 중복성을 실현함으로써, 타사가 따라올 수 없는 벤치마크를 확립했습니다.

아시아태평양은 2026-2031년 연평균 성장률(CAGR) 7.58%를 나타낼 것으로 예측되며, 지역별로는 가장 빠른 성장이 전망됩니다. 2026년 개장 예정인 Equinix HK6는 홍콩을 중국 본토의 거래소를 연결하는 국경 간 차익거래의 허브로 자리매김할 것입니다. 일본거래소그룹과 한국거래소는 100기가비트 이더넷을 지원하는 케이지를 도입하여 지역 내 독점 기업들을 유치하고 있습니다. 싱가포르 거래소는 여전히 결정론적 접근 방식을 제공하고 있지만, 인도의 국립증권거래소는 고빈도 거래에 대한 유인을 억제하기 위해 무작위 지연 방식을 도입했습니다.

유럽, 중동 및 아프리카에서는 동향에 차이가 나타나고 있습니다. 유렉스 프랑크푸르트와 유로넥스트 암스테르담에서는 수요가 견조한 추세를 보이고 있으며, 유렉스에서는 캐비닛 1대 당 월 6,000-9,600유로(6,780-10,848달러)의 요금을 책정하고 있습니다. 유로넥스트가 2024년 7월에 구축한 마이크로파 네트워크 덕분에 런던-베르가모 구간의 지연 시간이 4밀리초 미만으로 단축되었으며, 이는 광섬유 우회 경로를 활용한 서버 배치와 일치합니다. 중동의 정부계 펀드는 신생 디지털 자산 거래소에 자금을 지원하고 있지만, 남미에서는 도입이 초기 단계에 머물러 있으며 B3 상파울루의 코로케이션 서비스로 한정되어 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the high frequency trading server market size was valued at USD 629.87 million in 2025 and estimated to grow from USD 670.12 million in 2026 to reach USD 900.55 million by 2031, at a CAGR of 6.09% during the forecast period (2026-2031).

This report is Segmented by Processor Architecture (x86-Based Servers, ARM-Based Servers, and More), Form Factor (Rack Servers, Blade Servers, and More), Application (Equity Trading, Foreign Exchange, and More), End-User (Proprietary Trading Firms and Market Makers, Investment Banks and Brokerage Houses, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global High Frequency Trading Server Market Trends and Insights

Surge in Algorithmic and AI-Driven Trading Volumes

Algorithmic execution accounts for more than 70% of equity order flow in developed venues, and reinforcement-learning agents are now being embedded directly into FPGA fabric to shave nanoseconds off tick-to-trade cycles. The European Securities and Markets Authority guidance issued in February 2026 requires microsecond-level pre-trade checks that favor on-premises compute over cloud endpoints. Quantitative funds managing more than USD 10 billion in assets deploy inference-capable servers next to exchange engines, converting microsecond gains into multi-million-dollar slippage savings. Memory-bandwidth demands widen, accelerating the adoption of ARM designs such as NVIDIA Grace that deliver 1 terabyte per second of coherent bandwidth. The result is a structural lift in unit shipments of heterogeneous servers across major colocation hubs.

Demand for Ultra-Low-Latency Infrastructure

Exchange proximity hosts are upgrading from 10-gigabit to 400-gigabit Ethernet, compressing round-trip times to sub-microsecond territory and setting new floor specifications for network interface cards. Kraken opened a London cage at Equinix LD5 in April 2026 that delivers sub-millisecond access to European venues, drawing crypto market makers that require deterministic flows. CME Aurora added 428,000 square feet of raised floor in partnership with Google Cloud, providing 17-kilowatt cabinets that accommodate dual-socket blade nodes and FPGA accelerators. Kernel-bypass stacks such as DPDK and RDMA are now mandatory features on trading NICs, further intertwining server design with network topology.

High CAPEX for Colocation and Specialized Cooling

Tier-1 exchange-adjacent cabinets range from USD 6,000 to USD 9,600 per month for 10-gigabit connectivity, and premium cages attract USD 15,000 monthly, pushing annual spend beyond USD 150,000 per rack after cross-connects. Liquid-cooling upgrades add USD 50,000-100,000 upfront, forcing mid-tier hedge funds to weigh latency gains against budget limits. Legacy halls lacking chilled-water loops cannot retrofit high-density blades, driving migrations to new builds and elongating payback periods. Some firms downshift to virtual private servers, trading 20 microseconds of latency for monthly bills under USD 2,000, fragmenting demand for cutting-edge hardware.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Cryptocurrency and Digital-Asset Exchanges

- Evolution of x86 Multi-core and FPGA-accelerated Processors

- Rising Regulatory Scrutiny and Speed-Bump Initiatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

ARM-based servers logged the fastest 8.43% CAGR forecast for 2026-2031 as firms prioritize energy efficiency and memory bandwidth. NVIDIA Grace CPUs with 72 Arm Neoverse V2 cores and 1 terabyte per second of bandwidth shipped in 2025, enabling real-time risk simulations that once demanded dual-socket x86 rigs. x86 systems still dominated with 74.32% of high frequency trading server market share in 2025, underpinned by decades of compiled trading logic optimized for Intel and AMD microcode.

The power-density edge for ARM is frequently 30-40%, a benefit that aligns with colocation operators chasing revenue per kilowatt. Recompilation hurdles and limited ARM-native FPGA tooling slow migration for smaller firms, yet partnerships such as Fujitsu-Arrcus-1Finity in March 2026 reveal growing confidence in ARM designs for next-generation cages.

Blade servers are projected to expand at 7.84% CAGR to 2031, eclipsing rack systems in new builds. Cisco's UCS XE9305 chassis hosts 16 dual-socket nodes in 10U, eliminating top-of-rack switch latency and maximizing compute per square foot. Rack servers maintained 63.47% share of the high-frequency trading server market in 2025, reflecting their flexibility in retrofitting sites with lower power envelopes.

Liquid-cooling-ready blade chassis sustain 17-kilowatt cabinets without disruptive retrofits, an advantage as exchange hosts lift density ceilings. Supermicro's March 2026 40-node MicroBlade reduced per-node footprint by 50%, underscoring the economic pressure on square footage. Retrofit constraints will preserve rack prevalence, but greenfield deployments increasingly default to blade.

Geography Analysis

North America anchored 36.51% of the high frequency trading server market in 2025, supported by CME Aurora, NYSE Mahwah, and Nasdaq Carteret. CME's partnership with Google Cloud delivered 428,000 square feet of additional raised floor, enabling 17-kilowatt cabinets that favor blade and FPGA hybrids. ICE Mahwah reached Tier 4 redundancy with 28 megawatts and sub-1 microsecond precision time protocol in January 2026, cementing a benchmark others emulate.

Asia-Pacific is projected to log a 7.58% CAGR over 2026-2031, the fastest regional climb. Equinix HK6, opening in 2026, positions Hong Kong as a cross-border arbitrage hub linking mainland exchanges. Japan Exchange Group and Korea Exchange rolled out 100-gigabit Ethernet cages, drawing regional proprietary firms. Singapore Exchange continues to offer deterministic access, yet India's National Stock Exchange introduced randomized delays that temper high-frequency incentives.

Europe, the Middle East, and Africa show divergent trends. Eurex Frankfurt and Euronext Amsterdam sustain steady demand, with Eurex charging EUR 6,000-9,600 (USD 6,780-10,848) per cabinet each month. Euronext's July 2024 microwave network lowered London-Bergamo latency below 4 milliseconds, aligning with server placements that exploit fiber bypass. Middle Eastern sovereign wealth funds fund nascent digital-asset exchanges, while South America remains in early adoption, limited to B3 Sao Paulo colocation offerings.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Super Micro Computer, Inc.

- Lenovo Group Limited

- International Business Machines Corporation

- Cisco Systems, Inc.

- Fujitsu Limited

- NEC Corporation

- Inspur Group Co., Ltd.

- Gigabyte Technology Co., Ltd.

- ASUSTeK Computer Inc.

- Quanta Computer Inc.

- Wistron Corporation

- MiTAC Holdings Corporation

- Penguin Computing, Inc.

- LDA Technologies Ltd.

- Silicom Ltd.

- XENON Pty Ltd.

- Broadberry Data Systems Limited

- Arista Networks, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Algorithmic and AI-Driven Trading Volumes

- 4.2.2 Demand for Ultra-Low-Latency Infrastructure

- 4.2.3 Expansion of Cryptocurrency and Digital-Asset Exchanges

- 4.2.4 Evolution of x86 Multi-Core and FPGA-Accelerated Processors

- 4.2.5 Microwave and Free-Space Optical Links Co-Optimizing Servers

- 4.2.6 Edge Colocation in Emerging Financial Hubs

- 4.3 Market Restraints

- 4.3.1 Rising Regulatory Scrutiny and Speed-Bump Initiatives

- 4.3.2 High CAPEX for Colocation and Specialized Cooling

- 4.3.3 Supply-Chain Constraints for NIC / FPGA Components

- 4.3.4 Carbon-Intensity Reporting Limiting Ultra-Dense Halls

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Processor Architecture

- 5.1.1 x86-based Servers

- 5.1.2 ARM-based Servers

- 5.1.3 Other Processor Architectures

- 5.2 By Form Factor

- 5.2.1 Rack Servers

- 5.2.2 Blade Servers

- 5.2.3 Tower Servers

- 5.2.4 Micro Servers

- 5.3 By Application

- 5.3.1 Equity Trading

- 5.3.2 Foreign Exchange (Forex)

- 5.3.3 Commodity Trading

- 5.3.4 Derivatives and Cryptoassets

- 5.4 By End-User

- 5.4.1 Proprietary Trading Firms and Market Makers

- 5.4.2 Investment Banks and Brokerage Houses

- 5.4.3 Hedge Funds and Asset Managers

- 5.4.4 Stock and Derivatives Exchanges

- 5.4.5 Ancillary Systems (CRM, Treasury, HR)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of the Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Dell Technologies Inc.

- 6.4.2 Hewlett Packard Enterprise Company

- 6.4.3 Super Micro Computer, Inc.

- 6.4.4 Lenovo Group Limited

- 6.4.5 International Business Machines Corporation

- 6.4.6 Cisco Systems, Inc.

- 6.4.7 Fujitsu Limited

- 6.4.8 NEC Corporation

- 6.4.9 Inspur Group Co., Ltd.

- 6.4.10 Gigabyte Technology Co., Ltd.

- 6.4.11 ASUSTeK Computer Inc.

- 6.4.12 Quanta Computer Inc.

- 6.4.13 Wistron Corporation

- 6.4.14 MiTAC Holdings Corporation

- 6.4.15 Penguin Computing, Inc.

- 6.4.16 LDA Technologies Ltd.

- 6.4.17 Silicom Ltd.

- 6.4.18 XENON Pty Ltd.

- 6.4.19 Broadberry Data Systems Limited

- 6.4.20 Arista Networks, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment