|

시장보고서

상품코드

2062462

도메인 네임 시스템(DNS) 방화벽 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Domain Name System Firewall - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

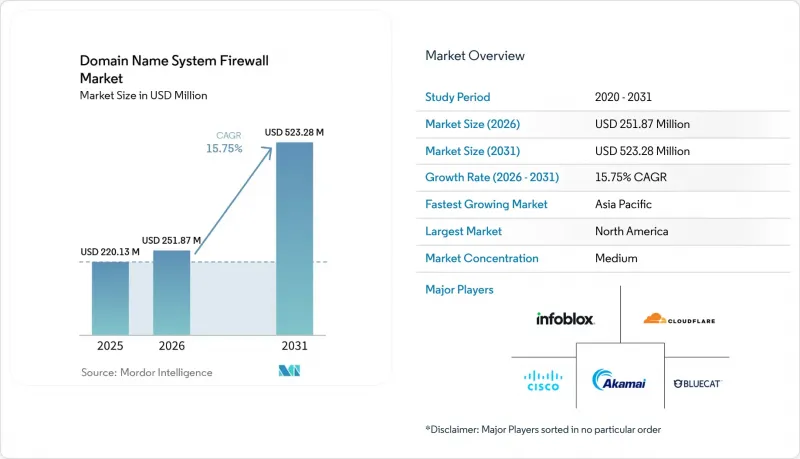

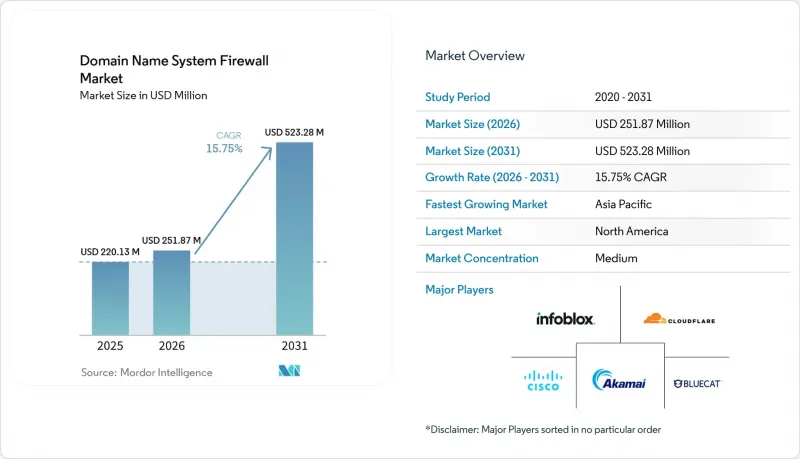

Mordor Intelligence에 의하면, 도메인 네임 시스템(DNS) 방화벽 시장 규모는 2025년에 2억 2,013만 달러로 평가되었고, 2026년 2억 5,187만 달러로 추정되고, 2031년까지 5억 2,328만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 15.75%를 나타낼 전망입니다.

본 보고서는 배포 모델별(온프레미스, 클라우드 기반, 하이브리드), DNS 서버 유형별(재귀적 리졸버 방화벽, 권한 DNS 방화벽 등), 기업 규모별(대기업, 중견기업, 중소기업), 업종별(은행, 금융서비스 및 보험(BFSI), IT 및 통신, 정부 및 국방 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 도메인 네임 시스템(DNS) 방화벽 시장 동향 및 인사이트

DNS 계층에 대한 공격이 증가함에 따라 보안 투자가 필수화되고 있습니다.

대규모 정찰, 피싱 및 분산 서비스 거부(DDoS) 공격으로 인해 기업의 보안 예산은 리졸버를 중심으로 한 대책으로 전환되고 있습니다. 2025년 3월 미국 사이버보안·인프라보안청(CISA)과 국가안보국(NSA)이 공동으로 발표한 권고안에서는 끊임없이 변화하는 IP 주소 뒤에 공격자의 인프라를 숨겨 정적 차단 목록을 무력화시키는 ‘패스트플럭스(Fast Flux)’ 도메인 로테이션이 지적되었습니다. 이 기법은 2024년 초 연방수사국(FBI)이 100만 대 이상의 소규모 사무실용 라우터를 장악한 러시아의 봇넷을 적발함에 따라 그 시급성이 더욱 커졌습니다. 이는 어디에나 존재하는 DNS 트래픽이 어떻게 무기로 활용될 수 있는지를 보여줍니다. Infoblox의 ‘2025년 DNS 위협 보고서’에 따르면, 터널링 사건이 37% 증가한 것으로 기록되었으며, 이는 공격자들이 현재 DNS를 장벽이 적은 명령 및 제어 경로로 간주하고 있음을 뒷받침합니다. 이사회 차원의 사이버 위험 관련 논의에서 방어적인 DNS 대책이 사이버 보험 인수 요건으로 간주되는 사례가 증가하고 있으며, 조달 주기가 수년 단위에서 분기 단위로 단축되고 있습니다.

멀티클라우드 및 하이브리드 IT 아키텍처로의 급속한 전환

Amazon Web Services, Microsoft Azure, Google Cloud 및 코로케이션 사이트를 아우르며 워크로드를 운영하는 기업들은 일관된 도메인 정책을 유지하는 데 어려움을 겪고 있습니다. IBM의 NS1 Connect 백서에 따르면, 금융 기업들은 단일 장애 지점을 제거하기 위해 최소 두 곳의 외부 DNS 공급자를 운영하고 있으며, 2024년 중반 주요 플랫폼에서 6시간에 걸친 재귀적 장애가 발생했을 때 이러한 관행의 타당성이 입증되었습니다. 알고리즘 트레이딩에서 실시간 환자 원격 모니터링에 이르기까지, 성능이 중요한 용도는 여전히 로컬 리졸버에 의존하고 있기 때문에 조직들은 온프레미스형 어플라이언스와 클라우드 오케스트레이션을 융합한 하이브리드 설계를 선호하고 있습니다. 시스코는 2026년 4월, 걸프협력회의(GCC) 시장을 위해 현지화된 DNS 방화벽 어플라이언스를 출시하는 동시에, 통합된 정책 적용을 실현하기 위해 이를 자사의 Umbrella 클라우드 레이어와 연동함으로써 이러한 지연 및 주권 관련 우려를 해소했습니다. 아키텍처가 복잡해짐에 따라, 서로 다른 리졸버 인스턴스 간에 위협 피드 및 대응 정책 영역을 거의 실시간으로 배포할 수 있는 관리 콘솔에 대한 수요가 증가하고 있습니다. 쿼리 성능을 저하시키지 않으면서 이러한 연동을 자동화할 수 있는 벤더들이 시장 점유율을 크게 확대되고 있습니다.

대형 기존 기업에서 레거시 재귀 서버를 교체하는 데 드는 높은 비용

BIND 등 오픈소스 리졸버를 표준화해 온 금융 및 통신 대기업들은 상용 방화벽으로 전환함에 따라 50만 달러가 넘는 자본 지출을 감수해야할 것입니다. 가용성을 확보하기 위해 구축된 지리적 클러스터에는 수백 개의 애니캐스트 노드가 포함되어 있으며, 이를 단순히 새로운 하드웨어로 ‘그대로 이전’할 수는 없습니다. NIST 특별 간행물 800-81 개정판 3에서는 기존 환경에서 DNSSEC 및 관련 정책 영역을 도입하는 데 12-18개월이 소요될 수 있다고 경고하고 있습니다. 전환 기간 동안 팀은 기존 인프라와 새로운 인프라를 병행하여 유지 관리해야 하므로 인건비가 증가하고, 변경 관리 기간도 길어집니다. 예산 측면에서의 타격은 제조업 및 소매업에서 특히 심각합니다. 이러한 업계에서는 영업이익률이 낮아, 7자리 규모의 보안 프로젝트에 투자할 여유가 거의 없기 때문입니다.

부문별 분석

하이브리드 구성은 2025년 지출의 상당 부분을 차지했으며, 연평균 성장률(CAGR) 16.43%로 성장하고 있어 도메인 네임 시스템(DNS) 방화벽 시장 전체의 성장률을 상회하고 있습니다. 기업들은 당초, 즉각적인 효과를 기대하며 클라우드 기반 방화벽을 선호하여 2025년 지출의 58.91%를 차지했으나, 쿼리의 홉이 증가함에 따라 지연 시간이 10-20밀리초 늘어났고, 이는 거래 알고리즘이나 임상 영상 시스템에 있어 용납할 수 없는 지연으로 판명되었습니다. 그 결과, 구매자들은 현재 정책 제어를 일원화하면서도 서브밀리초 단위의 응답 속도를 유지하기 위해 경량 온프레미스형 리졸버와 클라우드 오케스트레이션을 결합하고 있습니다. EfficientIP의 2025년 조사에 따르면, 직원 수 1만 명 이상의 기업 중 62%가 이미 이러한 듀얼 아키텍처를 도입하고 있으며, NIS2의 복원력 요건이 이러한 추세를 뒷받침하고 있습니다. 도메인 네임 시스템(DNS) 방화벽 시장 규모는 구매자가 구독형 서비스와 어플라이언스 하드웨어 중 하나만 선택하는 것이 아니라, 두 가지 모두를 도입함으로써 혜택을 보고 있습니다.

두 번째 성장 요인은 주권 클라우드에 관한 규제입니다. 사우디아라비아의 ‘Salam Secure DNS’는 공급업체의 클라우드에서 전송되는 위협 정보를 수신하면서도 모든 로그를 국내에 보관하고 있어, 다른 걸프 지역 시장들에게 모범이 되고 있습니다. 반면, Cloudflare Gateway는 그 정반대의 모습을 보여줍니다. 2025년에는 레거시 장비를 보유하지 않은 15,000개 이상의 기업이 순수 클라우드 DNS로 직접 전환했습니다. 그렇긴 하지만, 엣지 사이트가 증가함에 따라 대역폭이 제한된 지사에서는 캐싱 포워더가 여전히 필수적일 것입니다. 중앙에서 오케스트레이션되든, 독립형으로 운영되든 상관없이, 리졸버의 다양성은 더 이상 아키텍처상의 선호 사항이 아니라 규정 준수 요건이 되었습니다.

2025년에도 재귀형 리졸버 엔진은 여전히 주력 제품이었으며, 모든 엔드포인트의 쿼리가 여기서 시작되기 때문에 도메인 네임 시스템(DNS) 방화벽 시장의 38.45%를 차지했습니다. 그러나 SaaS 공급업체와 CDN이 테라비트 규모의 리플렉션 공격을 방어하려는 움직임에 힘입어, 권한 서버 계층의 방어 시장은 연평균 성장률(CAGR) 15.95%로 확대되고 있습니다. Akamai는 2025년 상반기에 이러한 공격이 71% 급증한 것으로 기록했으며, 이로 인해 사업자들은 존의 최상위에서 속도 제한 및 DNSSEC 검증을 도입할 수밖에 없게 되었습니다. 새로운 아키텍처 청사진에서는 리졸버와 오소리티의 필터를 공유 정책 메쉬 내에서 결합하는 것이 권장되고 있으며, 도메인 네임 시스템(DNS) 방화벽 시장은 통합된 제어 플레인 비전에 한 걸음 더 가까워지고 있습니다.

VeriSign의 하루 1,830억 건에 달하는 쿼리 부하는 오소리티 엔진이 오감지 없이 충족해야 하는 처리량 요건을 여실히 보여주고 있습니다. Neustar와 F5는 비정상적인 트래픽 급증이나 지리적 이상 현상을 1초 미만의 간격으로 감지하는 머신러닝 분류기를 도입하여 이에 대응하고 있습니다. 인터넷 기술 태스크포스(IETF)의 ‘Protective DNS’ 프레임워크 초안은 기능의 균일성에 관한 지침을 한층 더 강화하여, 벤더 간의 차별화가 기본적인 차단 및 허용 목록이 아닌 분석의 심도 측면으로 전환되도록 보장하고 있습니다. SaaS 도입이 여전히 증가하는 가운데, 재귀형 DNS에 대한 지출이 견조한 추세를 보이는 반면, 권한 서버용 방화벽은 향후 10년 동안 그 성장 프리미엄을 유지할 것으로 보입니다.

지역별 분석

미국의 프로텍티브 DNS 이니셔티브를 통해 위협 정보를 활용한 리졸버 서비스가 101개 연방 기관에 도입된 결과, 2025년 매출의 42.56%를 북미가 차지했습니다. 충실한 사이버 보안 예산에 더해, 하이퍼스케일 클라우드 및 관리형 보안 분야의 혁신 기업들과의 근접성 덕분에, 이 지역은 절대적인 지출 규모 측면에서 계속해서 우위를 점하고 있습니다. 캐나다 사이버보안센터는 2025년, 주 정부 의료 시스템에 대해 재귀적 인프라 강화를 권고함으로써 이러한 움직임에 동참했으며, 멕시코 규제 당국은 2024년 발생한 해킹 사건을 계기로 은행들에 DNS 모니터링을 의무화했습니다.

아시아태평양은 연평균 성장률(CAGR) 15.92%를 기록하며, 성장 속도 순위에서 1위를 차지하고 있습니다. 일본은 대학 및 유틸리티용 리졸버 도입에 49억 3,000만 엔(3,300만 달러)을 책정한 반면, 인도의 CERT-In은 2025년에 294만 4,000건의 사고를 처리했으며, AI를 활용한 악성 도메인 감지 그리드에 대한 투자를 두 배로 늘렸습니다. 한국의 KISA는 2025년 감시 시스템에 EU 및 미국의 위협 정보를 통합하여, 지역을 초월한 데이터 공유 확대를 시사했습니다. 아세안 전역에서는 ICANN의 지역 계획에 따라 DNSSEC 워크숍이 활성화되면서 공공 부문에서의 도입이 가속화되고 있습니다.

유럽의 동향은 DNS를 공급망 감사의 핵심으로 삼는 NIS2 및 DORA에 의해 형성되고 있습니다. 독일의 BSI, 영국의 국가사이버보안센터(NCSC), 그리고 사우디아라비아와 아랍에미리트(UAE)의 주권 클라우드 이니셔티브는 리졸버 정책이 방화벽 정책과 마찬가지로 전략적이라는 관점을 뒷받침하고 있습니다. 아프리카와 남미에서는 여전히 투자가 부진한 상황이지만, 관리형 보안 서비스 제공업체들이 종량제 기반 리졸버 보호 서비스를 도입함에 따라 향후 5년 동안 그 격차가 줄어들 가능성이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the domain name system firewall market size was valued at USD 220.13 million in 2025 and estimated to grow from USD 251.87 million in 2026 to reach USD 523.28 million by 2031, at a CAGR of 15.75% during the forecast period (2026-2031).

This report is Segmented by Deployment Model (On-Premises, Cloud-Based, and Hybrid), DNS Server Type (Recursive Resolver Firewall, Authoritative DNS Firewall, and More), Enterprise Size (Large Enterprises, Mid-Sized Enterprises, and SMEs), Industry Vertical (BFSI, IT and Telecommunications, Government and Defense, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Domain Name System Firewall Market Trends and Insights

Increasing DNS-Layer Attacks Driving Mandatory Security Investments

High-volume reconnaissance, phishing, and distributed denial-of-service assaults are shifting corporate security budgets toward resolver-centric countermeasures. A joint advisory from the U.S. Cybersecurity and Infrastructure Security Agency and the National Security Agency in March 2025 flagged "fast flux" domain rotation that hides attacker infrastructure behind constantly changing IP addresses, rendering static blocklists obsolete. The technique gained urgency after the Federal Bureau of Investigation dismantled a Russian botnet that hijacked more than one million small-office routers in early 2024, illustrating how ubiquitous DNS traffic can be weaponized. Infoblox's 2025 DNS Threat Report logged a 37% rise in tunneling events, confirming that adversaries now view DNS as a low-friction command-and-control pathway. Board-level cyber-risk discussions increasingly treat protective DNS as a prerequisite for cyber-insurance underwriting, compressing procurement cycles from years to quarters.

Rapid Migration to Multi-Cloud and Hybrid IT Architectures

Enterprises juggling workloads across Amazon Web Services, Microsoft Azure, Google Cloud, and colocation sites struggle to keep consistent domain policies. IBM's NS1 Connect white paper documented that financial firms maintain at least two external DNS providers to eliminate single points of failure, a practice vindicated when a major platform suffered a six-hour recursive outage in mid-2024. Performance-critical apps, from algorithmic trading to real-time patient telemetry, still depend on local resolvers, so organizations favor hybrid designs that blend on-premises appliances with cloud orchestration. Cisco addressed those latency and sovereignty concerns in April 2026 by rolling out localized DNS firewall appliances for Gulf Cooperation Council markets while tying them back to its Umbrella cloud layer for a unified policy push. The architectural sprawl fuels demand for management consoles that broadcast threat feeds and response-policy zones across disparate resolver instances in near real time. Vendors that can automate this federation without degrading query performance are winning disproportionate wallet share.

High Replacement Cost for Legacy Recursive Servers in Large Incumbents

Financial and telecom giants that standardized on open-source resolvers such as BIND face capital outlays topping USD 500,000 when migrating to commercial firewalls. Geographic clusters built for redundancy house hundreds of anycast nodes that cannot simply be "forklifted" into new hardware. NIST's Special Publication 800-81 Revision 3 cautions that retrofitting DNSSEC and response-policy zones can drag on for 12-18 months in brownfield environments. During the transition window, teams must dual-maintain old and new infrastructure, inflating labor costs and elongating change-control windows. The budgetary shock is especially acute in manufacturing and retail, where thin operating margins leave minimal headroom for seven-figure security projects.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Mandates for Zero-Trust and Secure Access Service Edge Frameworks

- Growing Use of DNS Tunneling for Command-and-Control in Edge IoT Fleets

- Lack of Skilled DNS Security Professionals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid setups accounted for a material slice of 2025 spending and are growing at 16.43% CAGR, outpacing the broader Domain Name System Firewall market. Organizations first gravitated to cloud-based firewalls for quick wins, 58.91% of outlays in 2025, but discovered that added query hops inflate latency by 10-20 milliseconds, an unacceptable drag on trading algorithms and clinical imaging systems. Consequently, buyers now mesh lightweight on-premises resolvers with cloud orchestration to retain sub-millisecond response while centralizing policy control. EfficientIP's 2025 survey found that 62% of firms above 10,000 employees already run such dual architectures, and NIS2 resilience mandates reinforce the trend. The Domain Name System Firewall market size benefits because buyers procure both subscriptions and appliance hardware instead of choosing one or the other.

A second growth lever is sovereign-cloud regulation. Saudi Arabia's Salam Secure DNS keeps all logs within national borders while still accepting threat-feed pushes from vendor clouds, providing a playbook for other Gulf markets. Cloudflare Gateway illustrates the opposite end of the spectrum: more than 15,000 enterprises without legacy gear leaped straight into pure cloud DNS in 2025. Still, as edge sites proliferate, caching forwarders will remain indispensable for branch offices where bandwidth is scarce. Whether orchestrated centrally or run stand-alone, resolver diversity is now a compliance requirement rather than an architectural preference.

Recursive resolver engines remained the workhorse in 2025, controlling 38.45% of the Domain Name System Firewall market share because every endpoint query begins there. Yet authoritative-layer defenses are climbing at a 15.95% CAGR, propelled by SaaS vendors and CDNs fending off terabit-scale reflection floods. Akamai logged a 71% spike in such assaults during 1H 2025, forcing operators to deploy rate limiting and DNSSEC validation at the zone apex. New architectural blueprints now recommend pairing resolver and authoritative filters in a shared policy mesh, moving the Domain Name System Firewall market closer to a unified control-plane vision.

VeriSign's daily query load of 183 billion illustrates the throughput requirement that authoritative engines must satisfy without false positives. Neustar and F5 have responded with machine-learning classifiers that flag anomalous volume bursts or geo anomalies in sub-second intervals. The Internet Engineering Task Force's draft Protective DNS framework further cements feature parity guidelines, ensuring vendor differentiation skews toward analytics depth rather than basic block-and-allow lists. With SaaS adoption still climbing, authoritative firewalls should preserve their growth premium well into the next decade even as recursive spending stays robust.

Geography Analysis

North America generated 42.56% of 2025 receipts after the U.S. Protective DNS initiative funneled threat-fed resolver services into 101 federal agencies. Mature cyber budgets, plus proximity to hyperscale clouds and managed security innovators, keep the region ahead on absolute spend. Canada's Center for Cyber Security echoed the push in 2025 by advising provincial health systems to harden recursive infrastructure, and Mexico's regulators compelled banks to monitor DNS following 2024 hijacking incidents.

Asia-Pacific, tracking a 15.92% CAGR, tops the velocity charts. Japan earmarked JPY 4.93 billion (USD 33 million) for university and utility resolver rollouts, while India's CERT-In processed 2.944 million incidents in 2025 and doubled down on an AI-driven malicious-domain detection grid. South Korea's KISA plugged EU and U.S. threat intel into its 2025 monitoring stack, illustrating growing cross-regional data sharing. Across ASEAN, ICANN's regional plan boosted DNSSEC workshops, accelerating public-sector adoption.

Europe's trajectory is shaped by NIS2 and DORA, which pull DNS into the core of supply-chain audits. Germany's BSI, the U.K.'s National Cyber Security Center, and sovereign-cloud initiatives in Saudi Arabia and the UAE reinforce the view that resolver policy is now as strategic as firewall policy. Africa and South America still lag in spending, but managed security providers are introducing pay-as-you-go resolver protection that may compress the gap over the next five years.

- Infoblox Inc.

- Cloudflare, Inc.

- Cisco Systems, Inc.

- Akamai Technologies, Inc.

- BlueCat Networks, Inc.

- EfficientIP SAS

- Neustar Security Solutions, LLC

- F5, Inc.

- Men & Mice ehf

- VeriSign, Inc.

- DNSFilter, Inc.

- Comodo Security Solutions, Inc.

- Enea AB

- Huawei Technologies Co., Ltd.

- Palo Alto Networks, Inc.

- Quad9 Foundation

- Technitium Solutions Pvt. Ltd.

- FlashStart S.r.l.

- Secure64 Software Corporation

- Zscaler, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing DNS-Layer Attacks Driving Mandatory Security Investments

- 4.2.2 Rapid Migration to Multi-Cloud and Hybrid IT Architectures

- 4.2.3 Regulatory Mandates for Zero-Trust and Secure Access Service Edge (SASE) Frameworks

- 4.2.4 Growing Use of DNS Tunneling for Command-and-Control in Edge IoT Fleets

- 4.2.5 Rise of "Everything over HTTPS" Accelerating Encrypted DNS Adoption

- 4.2.6 Telecom Operators Monetising DNS Threat-Intel Feeds to Enterprises

- 4.3 Market Restraints

- 4.3.1 High Replacement Cost for Legacy Recursive Servers in Large Incumbents

- 4.3.2 Lack of Skilled DNS Security Professionals

- 4.3.3 Performance Trade-Offs with Encrypted DNS over Satellite Back-Haul Links

- 4.3.4 Fragmentation of National Root-Server Policies in Sovereign Clouds

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 On-premises

- 5.1.2 Cloud-based

- 5.1.3 Hybrid

- 5.2 By DNS Server Type

- 5.2.1 Recursive Resolver Firewall

- 5.2.2 Authoritative DNS Firewall

- 5.2.3 Caching Forwarder Firewall

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises (>=1,000 employees)

- 5.3.2 Mid-sized Enterprises (100-999 employees)

- 5.3.3 SMEs (<100 employees)

- 5.4 By Industry Vertical

- 5.4.1 BFSI

- 5.4.2 IT and Telecommunications

- 5.4.3 Government and Defense

- 5.4.4 Healthcare and Lifesciences

- 5.4.5 Retail and e-Commerce

- 5.4.6 Manufacturing

- 5.4.7 Other Industry Vertical

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of the Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Infoblox Inc.

- 6.4.2 Cloudflare, Inc.

- 6.4.3 Cisco Systems, Inc.

- 6.4.4 Akamai Technologies, Inc.

- 6.4.5 BlueCat Networks, Inc.

- 6.4.6 EfficientIP SAS

- 6.4.7 Neustar Security Solutions, LLC

- 6.4.8 F5, Inc.

- 6.4.9 Men & Mice ehf

- 6.4.10 VeriSign, Inc.

- 6.4.11 DNSFilter, Inc.

- 6.4.12 Comodo Security Solutions, Inc.

- 6.4.13 Enea AB

- 6.4.14 Huawei Technologies Co., Ltd.

- 6.4.15 Palo Alto Networks, Inc.

- 6.4.16 Quad9 Foundation

- 6.4.17 Technitium Solutions Pvt. Ltd.

- 6.4.18 FlashStart S.r.l.

- 6.4.19 Secure64 Software Corporation

- 6.4.20 Zscaler, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment