|

시장보고서

상품코드

2062466

해상 계류 시스템 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Offshore Mooring System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

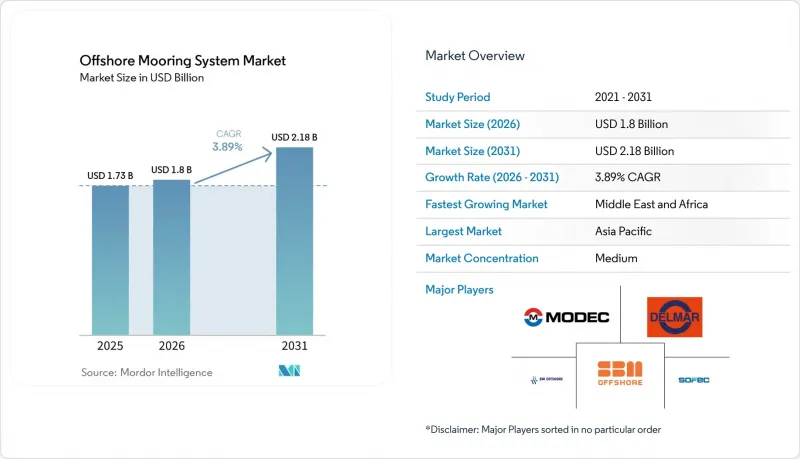

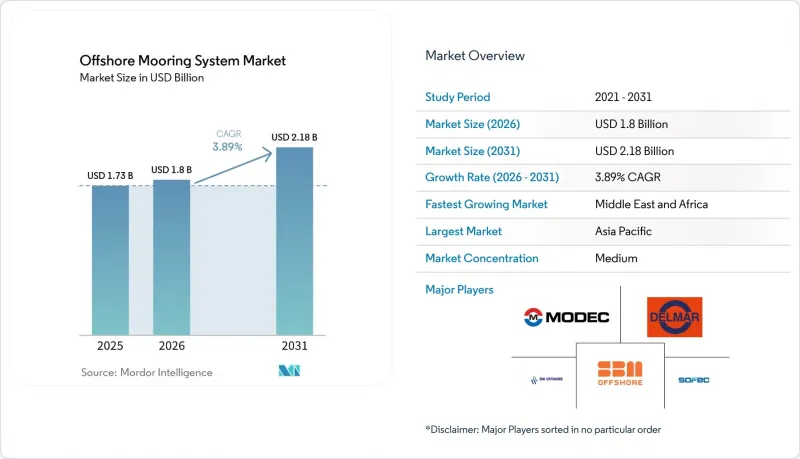

Mordor Intelligence에 의하면, 해상 계류 시스템 시장 규모는 2025년에 17억 3,000만 달러로 평가되었습니다. 2026년에 18억 달러에 달하고, 2031년까지 21억 8,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR은 3.89%를 나타낼 전망입니다.

본 보고서는 계류 유형(스프레드 계류 등), 구성 부품(앵커 등), 수심(얕은 바다, 심해, 초심해), 설치 유형(영구형, 일시형), 용도(부유식 생산·저장·하역 설비 등), 지역(북미, 유럽, 아시아·태평양, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 단위로 제시되어 있습니다.

세계의 해상 계류 시스템 시장 동향 및 인사이트

브라질 및 가이아나에서의 FPSO 수주 잔고 증가

브라질의 프레솔트층과 가이아나의 스태블록 블록에서는 하루 총 90만 배럴 이상의 생산이 이루어지고 있으며, 첨단 카테너리형 및 타우트레그형 계류 시스템에 의존하는 전용 FPSO에 대한 수요가 사상 최고 수준에 달하고 있습니다. SBM Offshore 및 MODEC과 같은 운영사들은 계류 하드웨어와 해저 구조물의 통합에 있어 새로운 기준을 제시하고 있으며, 이는 하중 관리, 부식 방지, 디지털 모니터링에 관한 전 세계적인 사양 체계에 영향을 미치고 있습니다. 2030년까지 해당 지역의 가동 중인 FPSO 수가 10척에 가까워짐에 따라, 앵커 단조 및 체인 제조에 대한 공급망의 압박이 커지고 있으며, 이는 해상 계류 시스템 시장 수요 증가를 뒷받침하고 있습니다. 또한, 이 지역의 클러스터는 강한 유속과 높은 피로도가 발생하는 환경에서 점검 기간을 단축하고 고장 위험을 줄이기 위한 예측 유지보수 분석의 실증 현장으로도 기능하고 있습니다. 이러한知見은 전 세계의 신조 프로젝트에 파급되어, 안전 여유를 훼손하지 않으면서 설계상의 유지보수성을 완화할 수 있을 것으로 기대됩니다.

동지중해 및 모잠비크의 심해 가스 개발에 대한 설비 투자 확대

아프로디테, 레비아탄 2단계, 코랄 사우스 FLNG를 합산하면 2024년부터 2025년에 걸쳐 확정된 총 지출액은 120억 달러를 초과하며, LNG 인수 하중 및 긴급 차단 시나리오를 견딜 수 있는 맞춤형 계류 설계를 필요로 했습니다. 수심 1,500m를 초과하는 초심해 환경에서는 해저 접촉 구간에 고강도 체인을 사용하여 상부 구조물의 움직임을 억제하면서도 수직 방향의 처짐을 유지하기 위해, 경량 HMPE 섹션을 조합한 하이브리드 구조가 필요합니다. 가스 시장에 대한 조기 공급을 중시하는 규제 당국의 입장에 따라 조기 조달이 필요해졌으며, 계류 시스템의 사양 수립이 기본 설계(FEED) 단계로 앞당겨졌습니다. 그 결과, 프로젝트 개발자들은 선박 부족 위험을 피하기 위해 로드셀, 위치 기준 센서, 퀵 릴리스 커넥터의 표준화를 중시하고 있습니다. 이러한 추세에 따라 향후 부유식 LNG(FLNG) 건설 프로젝트 간에 상호 호환 가능한 모듈식 설계가 도입될 것으로 예상되며, 이에 따라 해상 계류 시스템 시장의 성장 전망이 더욱 밝아질 것입니다.

리드타임이 긴 체인 및 앵커의 단조 능력에 대한 병목 현상

직경 120mm를 초과하는 앵커 체인의 리드타임이 12-15개월에서 18-24개월로 길어지고 있으며, 재고가 없는 앵커의 납품량이 1회당 200톤을 초과함에 따라, 피크 시 생산 능력에 가까운 수준으로 가동 중인 아시아태평양의 단조 제조업체들에 부담이 가중되고 있습니다. 미결 주문은 프로젝트 일정 조정의 유연성을 제한하고, 조기 자재 확보를 불가피하게 만들며, 제조업체의 운전자금 수요를 증가시키고 있습니다. 사이펨 7과 같은 통합형 도급업체는 현재 체인 공급업체의 소수 지분을 취득함으로써 위험을 헤지하고 있으며, 이는 위험 완화 방안으로서의 수직 통합의 한 사례를 보여줍니다. 일회성 조달에 의존하는 소규모 엔지니어링 전문 기업들은 경쟁력 약화에 직면해 있으며, 이는 단기적으로 해외 계류 시스템 시장 전체의 성장을 둔화시킬 가능성이 있습니다.

부문별 분석

2025년에는 카테너리 시스템이 4.3%의 성장률을 기록하며, 해상 계류 시스템 시장의 성장률을 상회했습니다. 이는 부유식 풍력 발전 프로젝트가 더 낮은 설비 투자(CAPEX)와 단순한 하드웨어를 특징으로 하는 카테너리 시스템으로 기울고 있기 때문입니다. FPSO의 위치 유지 용도로 2025년 매출의 25.5%를 스프레드 계류 방식이 차지했으나, 서아프리카에서는 풍향 변화에 따라 라인 하중을 30%까지 줄일 수 있는 싱글 포인트 방식이 선호되고 있습니다.

세미타우트 설계는 해저에 미치는 영향이 적다는 점에서 높이 평가받고 있으며, 부유식 풍력 발전 분야에서 도입되고 있습니다. 운영사들은 서로 다른 유형을 조합하는 경향이 점점 더 강해지고 있으며, 트렐보르그(Trelleborg)사의 앙골라에 위치한 3기의 FPSO에서 채택된 탠덤 방식은 스프레드의 무결성을 유지한 채 하역 작업을 가능하게 하고 있습니다. 재설계 없이 카테너리, 세미타우트, 타우트 레그 옵션 간에 전환이 가능한 모듈식 스프레드를 판매하는 공급업체는 상업적 우위를 점하고 있습니다.

앵커는 2025년 매출의 34.9%를 차지했으나, 로프는 연평균 5.4%의 성장률을 기록하며 합성 소재 부품 부문의 해상 계류 시스템 시장 규모를 끌어올리고 있습니다. Vryhof사의 STEVPRIS 및 VLA 앵커는 콩고와 트리니다드에서 수주한 프로젝트에서 연약한 점토 지반에서 1,500톤 이상의 지지 능력을 입증했습니다. 하이브리드 스프레드로 인해 체인 전체의 길이가 짧아지는 가운데, 시장의 하위 부문에서는 여전히 스틸 체인이 주류를 이루고 있습니다.

커넥터 시장은 HMPE 로프와 결합되는 파단 하중 2,000톤의 샤클 수요에 힘입어 성장하고 있습니다. 통합이 차별화 요소로 작용하고 있습니다. Cortland사의 AeroLock은 로프와 커넥터를 일체형으로 설계하여 선박의 작업 시간을 단축하고 공급업체의 이익률을 높이고 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 37.8%를 차지했으며, 중국의 원통형 FPSO, 한국의 KF Wind 컨세션, 일본의 JERA 텐션 레그 시범 프로젝트가 이를 주도했습니다. 2025년에는 시난위 및 나크월 풍력발전소가 80-120m 길이의 카테너리 설계를 검증함으로써, 지역 보조금이 어떻게 시제품을 상업적 규모로 전환시킬 수 있는지를 입증했습니다. 인도 타밀나두주와 구자라트주의 연안 지역에서는 수심 40-60m 해역에서도 부유식 발전의 경제성이 입증되면서, 공급업체들의 사업 파이프라인이 석유 프로젝트의 범위를 넘어 확대되고 있습니다.

중동 및 아프리카는 연평균 성장률(CAGR) 4.7%를 기록하며 가장 빠르게 성장하고 있는 지역으로, 카타르의 노스 필드, 동지중해 가스, 그리고 모잠비크의 코랄 노스 FLNG 프로젝트 덕분에 활기를 띠고 있습니다. 이 프로젝트의 2,000m 폴리에스터 타우트레그는 해당 지역에서 디지털 피로 모델에 대한 수요를 높였습니다. 사우디 아람코의 90m 마르잔 유전 확장 프로젝트에서는 해저 점유 면적을 줄이기 위해 심해용 계류 기술을 얕은 해역에 적용했습니다. 앙골라와 나이지리아에서는 탠덤식 하역 시스템의 도입이 진행되고 있어, 앵커 및 커넥터에 대한 수요를 뒷받침하고 있습니다.

덴마크의 본홀름과 벨기에의 프린세스 엘리자베스 에너지 아일랜드는 2030년까지 총 6.5GW 규모의 하이브리드 계류식 발전 단지를 추가할 예정입니다. 노르웨이가 2025년에 강화한 규정에 따라, 사업자는 철거 보증금을 예치해야 할 의무가 부과되었으며, 철거 비용을 30% 절감할 수 있는 경량 합성 로프로의 설계 전환이 진행되고 있습니다. 유럽에서는 2028년에 부유식 풍력 발전 설비의 설치 수가 석유 및 가스용 계류 설비를 넘어설 것으로 예상되며, 전환점을 맞이할 것으로 전망됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the offshore mooring system market size is projected to be USD 1.73 billion in 2025, USD 1.8 billion in 2026, and reach USD 2.18 billion by 2031, growing at a CAGR of 3.89% from 2026 to 2031.

This report is Segmented by Mooring Type (Spread Mooring, and More), Component (Anchors, and More), Depth (Shallow Water, Deep Water, and Ultra-Deep Water), Installation Type (Permanent, and Temporary), Application (Floating Production Storage and Offloading, and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). Market Forecasts are Provided in Value (USD).

Global Offshore Mooring System Market Trends and Insights

Rising FPSO Backlog in Brazil & Guyana

Brazil's pre-salt provinces and Guyana's Stabroek Block collectively host more than 900,000 bpd of production, creating record demand for purpose-built FPSOs that rely on advanced catenary and taut-leg mooring systems. Operators such as SBM Offshore and MODEC are setting new benchmarks for integrating mooring hardware with subsea architecture, which influences global specification frameworks for load management, corrosion protection, and digital monitoring. As FPSO counts in the region climb toward ten units in service by 2030, supply-chain pressure on anchor forging and chain manufacturing is intensifying, underpinning a positive demand trajectory for the offshore mooring systems market. The regional cluster also acts as a live testbed for predictive-maintenance analytics that shorten inspection campaigns and mitigate failure risk in high-current, high-fatigue environments. These learnings are expected to cascade into newbuild projects worldwide and relax design conservatism without compromising safety margins.

Growing CAPEX on Deep-water Gas in East Med & Mozambique

Total 2024-2025 committed expenditure exceeds USD 12 billion across Aphrodite, Leviathan Phase 2, and Coral South FLNG, prompting bespoke mooring designs able to withstand LNG off-take loads and emergency disconnection scenarios. Ultra-deep settings above 1,500 m require hybrid arrangements that combine high-grade chain in touch-down zones with low-weight HMPE sections to maintain vertical compliance while curbing topside motion. Regulatory focus on rapid gas-to-market schedules compels early procurement, pushing mooring system specification to front-end engineering design (FEED). Consequently, project developers emphasize standardization of load cells, position reference sensors, and quick-release connectors to hedge against vessel scarcity. This dynamic is expected to introduce transferable module designs across future floating LNG builds, reinforcing growth prospects for the offshore mooring systems market.

Long-lead Chain & Anchor Forging Capacity Bottlenecks

Anchor chain lead times have widened from 12-15 months to 18-24 months for diameters above 120 mm, and stockless anchor deliveries exceed 200 tons each, stressing Asia-Pacific forges operating near peak capacity. The backlog constrains project scheduling flexibility, compels early material reservations, and inflates working capital needs for fabricators. Integrated contractors such as Saipem7 now hedge risk by acquiring minority stakes in chain suppliers, illustrating vertical integration as a mitigation pathway. Smaller engineering boutiques dependent on spot procurement face erosion of competitiveness, which could slow overall expansion of the offshore mooring systems market in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Pre-commercial Floating Wind Arrays (>=50 MW)

- Rapid Uptake of Polyester & HMPE Ropes to Cut Weight

- Cost Overruns from Subsea Installation Vessel Scarcity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Catenary systems expanded at 4.3% in 2025, overtaking the offshore mooring system market growth rate as floating-wind projects gravitate toward their lower CAPEX and simpler hardware. Spread moorings held 25.5% of 2025 revenue for FPSO station-keeping, yet single-point variants are preferred in West Africa, where weathervaning trims line loads by 30%.

Semi-taut designs surface in floating wind, valued for a smaller seabed footprint. Operators increasingly combine types; Trelleborg's tandem scheme on three Angola FPSOs allows offloading while preserving spread integrity. Suppliers marketing modular spreads that pivot among catenary, semi-taut, and taut-leg choices without redesign gain a commercial edge.

Anchors captured 34.9% of 2025 revenue, yet ropes are advancing 5.4% per year, lifting the offshore mooring system market size for synthetic components. Vryhof's STEVPRIS and VLA anchors proved holding capacities above 1,500 t in soft clay across Congo and Trinidad awards. Steel chain still rules the lower catenary in the market as hybrid spreads shorten overall chain length.

Connectors fueled by demand for 2,000 t break-load shackles that pair with HMPE ropes. Integration is a differentiator: Cortland's AeroLock bundles rope and connector, cutting vessel time and boosting supplier margin.

Geography Analysis

Asia-Pacific commanded 37.8% of 2025 revenue, led by China's cylindrical FPSOs, South Korea's KF Wind concession, and Japan's JERA tension-leg pilot. Shinan-Ui and Nakwol wind farms validated 80-120 m catenary designs in 2025, demonstrating how local subsidies transform prototypes into commercial scale. India's Tamil Nadu and Gujarat coastlines show floating economics even in 40-60 m, expanding supplier pipelines beyond oil projects.

The Middle East and Africa are the fastest-growing regions at 4.7% CAGR, energized by Qatar's North Field, East Med gas, and Mozambique's Coral North FLNG, whose 2,000 m polyester taut-legs raised regional demand for digital fatigue models. Saudi Aramco's 90 m Marjan field expansion applied deep-water mooring tech in shallow water to shrink seabed footprint. Angola and Nigeria continue tandem offloading adoption, reinforcing anchor-connector demand.

Denmark's Bornholm and Belgium's Princess Elisabeth energy islands together add 6.5 GW of hybrid mooring scope by 2030. Norway's tightened 2025 rules oblige operators to post decommissioning security, steering designs toward lighter synthetic lines that trim removal cost by 30%. Europe is forecast to cross an inflection in 2028 when floating-wind installations eclipse oil and gas moorings.

- SBM Offshore

- MODEC Inc.

- Delmar Systems

- Bluewater Holding

- SOFEC Inc.

- BW Offshore

- Mampaey Offshore Industries

- NOV AqualisBraemar LOC

- Bexco

- Vryhof Anchors

- Deep Sea Mooring (OEG)

- First Subsea

- Lankhorst Ropes

- Franklin Offshore

- Trelleborg Marine & Infrastructure

- Parker Hannifin (Parker Polyflex)

- Cortland Company

- Kongsberg Maritime

- MacGregor (Cargotec)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising FPSO back-log in Brazil & Guyana

- 4.2.2 Growing CAPEX on deep-water gas in East Med & Mozambique

- 4.2.3 Surge in pre-commercial floating wind arrays (>=50 MW)

- 4.2.4 Rapid uptake of polyester & HMPE ropes to cut weight

- 4.2.5 Digital twins for mooring fatigue monitoring (AI-enabled)

- 4.2.6 Multipurpose energy-island hubs needing hybrid moorings

- 4.3 Market Restraints

- 4.3.1 Long-lead chain & anchor forging capacity bottlenecks

- 4.3.2 Cost overruns from subsea installation vessel scarcity

- 4.3.3 Insurance premiums rising after recent mooring failures

- 4.3.4 End-of-life decommissioning liability uncertainty

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Mooring Type

- 5.1.1 Spread Mooring

- 5.1.2 Single Point Mooring

- 5.1.3 Dynamic Positioning

- 5.1.4 Catenary

- 5.1.5 Taut Leg

- 5.1.6 Semi-taut

- 5.1.7 Others

- 5.2 By Component

- 5.2.1 Anchors

- 5.2.2 Connectors

- 5.2.3 Chains

- 5.2.4 Synthetic Fiber Ropes

- 5.2.5 Buoys

- 5.2.6 Others

- 5.3 By Depth

- 5.3.1 Shallow Water (Up to 400 m)

- 5.3.2 Deep Water (400 to 1 500 m)

- 5.3.3 Ultra-Deep Water (Above 1 500 m)

- 5.4 By Installation Type

- 5.4.1 Permanent

- 5.4.2 Temporary

- 5.5 By Application

- 5.5.1 Floating Production Storage and Offloading (FPSO)

- 5.5.2 Tension Leg Platforms (TLP)

- 5.5.3 Semi-submersibles

- 5.5.4 Spar Platforms

- 5.5.5 Floating Wind Turbines

- 5.5.6 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Spain

- 5.6.2.5 Nordic Countries

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 ASEAN Countries

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Colombia

- 5.6.4.4 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Qatar

- 5.6.5.4 South Africa

- 5.6.5.5 Egypt

- 5.6.5.6 Nigeria

- 5.6.5.7 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 SBM Offshore

- 6.4.2 MODEC Inc.

- 6.4.3 Delmar Systems

- 6.4.4 Bluewater Holding

- 6.4.5 SOFEC Inc.

- 6.4.6 BW Offshore

- 6.4.7 Mampaey Offshore Industries

- 6.4.8 NOV AqualisBraemar LOC

- 6.4.9 Bexco

- 6.4.10 Vryhof Anchors

- 6.4.11 Deep Sea Mooring (OEG)

- 6.4.12 First Subsea

- 6.4.13 Lankhorst Ropes

- 6.4.14 Franklin Offshore

- 6.4.15 Trelleborg Marine & Infrastructure

- 6.4.16 Parker Hannifin (Parker Polyflex)

- 6.4.17 Cortland Company

- 6.4.18 Kongsberg Maritime

- 6.4.19 MacGregor (Cargotec)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment