|

시장보고서

상품코드

2062471

상업용 분산형 에너지 발전 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Commercial Distributed Energy Generation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

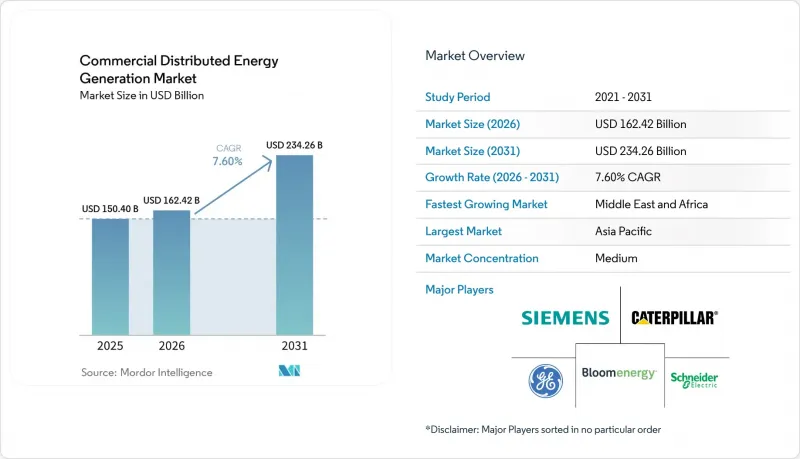

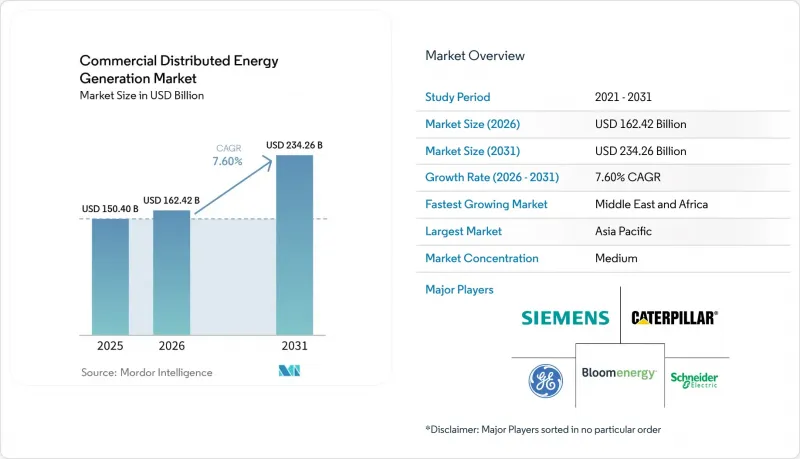

Mordor Intelligence에 의하면, 상업용 분산형 에너지 발전 시장 규모는 2025년에 1,504억 달러로 평가되었습니다. 2026년 1,624억 2,000만 달러에서 2031년까지 2,342억 6,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 7.60%를 나타낼 전망입니다.

본 보고서는 기술별(태양광 발전, 풍력 터빈, 연료전지, 열병합 발전, 축전지와 결합된 분산형 에너지 자원, 기타), 용도별(사무실 건물, 소매 시설, 데이터센터, 교육 기관, 병원, 창고, 공항, 기타), 지역별(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망치는 금액(달러) 단위로 제시되어 있습니다.

세계의 상업용 분산형 에너지 발전 시장 동향 및 인사이트

태양광 발전 및 풍력 발전의 LCOE 하락

2025년에는 대규모 태양광 발전의 LCOE가 1MWh당 29달러에 달했으며, 일조량이 많은 지역에서는 상업용 옥상 시스템이 1MWh당 50-70달러를 실현하고 있어, 미국 23개 주에서 소매 전기 요금을 밑돌고 있습니다. 중국의 폴리실리콘 공급 과잉으로 인해 모듈의 현물 가격은 1와트당 0.10달러 아래로 떨어졌으나, 급속 차단 전자 장치의 도입으로 설치 작업에 드는 노동력이 30% 감소했습니다. 따라서 기업은 고정 가격 전력 구매 계약(PPA)과 4-6년 내에 투자 회수가 예상되는 자체 자금으로 태양광 발전 시스템을 도입하는 것 중 하나를 선택하게 됩니다. 비용 절감이야말로 태양광 발전이 상업용 분산형 에너지 발전 시장에서 가장 빠르게 성장하고 있는 분야인 이유를 설명해 줍니다.

기업의 재생에너지 PPA와 탄소중립 목표

2025년 말까지 전 세계 기업 대상 재생에너지 전력구매계약(PPA)의 누적 규모는 50GW에 달했으며, 그중 60%는 북미와 유럽에서 체결되었습니다. 구글과 토탈에너지(TotalEnergies) 간의 1GW 계약이나 마이크로소프트와 브룩필드(Brookfield) 간의 10.5GW 파트너십과 같은 대규모 포트폴리오 거래에서는 여러 기술이 결합되어 있으며, 개발업체는 2-4시간 분량의 배터리 저장 설비를 설치해야 합니다. 24시간 체제로 청정 전력을 공급해야 하는 의무로 인해 간헐성 위험이 구매자에게 전가되므로, PPA는 프로젝트의 자금 조달 가능성을 높이고 상업시설 내 분산형 자산의 보급을 촉진합니다.

막대한 초기 설비 투자와 긴 회수 기간

미국 내 상업용 태양광 발전 비용은 여전히 1와트당 1.57달러이며, 연료전지 열병합발전(CHP)은 1와트당 6달러에 달할 전망입니다. 이는 수백만 달러 규모의 투자에 해당하며, 중소기업이 자체 자금으로 충당하는 경우는 드뭅니다. EaaS(Energy-as-a-service) 계약은 자본 측면의 장벽을 해소해 주지만, 투자 적격 등급의 신용도를 갖추지 못한 고객은 대상에서 제외되기 때문에 잠재 구매자의 60%가 이 서비스를 이용하지 못하고 있습니다.

부문별 분석

2025년, 연료전지는 상업용 분산형 에너지 발전 시장 점유율의 37.6%를 차지했습니다. 이는 끊김 없는 열과 전력이 필요한 병원, 데이터센터 및 산업 시설에서 이 기술이 지닌 가치를 반영하고 있습니다. Bloom Energy는 Equinix 시설에 100MW 이상을 도입하고, 와이오밍주에서 900MW 규모의 수소 관련 계약을 수주했습니다. 이러한 움직임은 해당 회사의 리더십을 입증하는 것입니다. 태양광 발전 부문은 더욱 빠르게 성장하고 있으며, 모듈 가격이 1와트당 0.10달러 아래로 떨어짐에 따라 2031년까지 연평균 성장률(CAGR) 14.4%로 성장할 전망입니다. 옥상 태양광 발전과 2-4시간 분량의 축전지를 결합함으로써, 저녁 피크 시간대의 전력망 의존도를 대폭 낮추고 수요 요금을 절감할 수 있어, 투자 회수 기간이 5-6년으로 단축됩니다.

풍력 터빈은 여전히 틈새 시장 수준에 머물러 있습니다. 이는 구역 지정 규제로 인해 100-500kW급 설비가 충분한 세트백(부지 경계로부터의 거리)을 확보할 수 있는 산업단지로만 제한되어 있기 때문입니다. 한편, 마이크로터빈이나 왕복 엔진과 결합된 하이브리드 시스템은 Off-grid 광업 및 농업 사업 분야의 활용 사례에서 여전히 주류를 이루고 있습니다. 2025년에 배터리 가격이 kWh당 120달러까지 하락함에 따라, 단독 시스템이 아닌 추가 설비로서 1-2시간 분량의 축전 시스템 도입이 촉진될 것이며, 상업용 분산형 에너지 발전 시장에서 태양광 발전이 기본적인 성장 동력으로서의 입지를 강화하게 될 것입니다. 이와 동시에, 수소 혼합형 CHP(열전병급)는 조절성을 희생하지 않으면서도 대폭적인 탈탄소화를 실현할 수 있는 방안을 제시하고 있으며, 이러한 특징 덕분에 예측 기간 동안에도 연료전지의 중요성이 유지될 가능성이 있습니다.

지역별 분석

2025년에는 아시아태평양이 매출의 45.3%를 차지하며 시장을 주도했습니다. 중국에서만 2025년에 18GW 규모의 상업용 옥상 태양광 발전 시설이 도입되었으며, 신규 산업단지에 재생에너지 발전 시설을 현장 설치할 비율을 20-30%로 의무화했습니다. 인도의 개방형 접근 개혁으로 인해 기업들은 배전 회사를 거치지 않고도 전력을 공급할 수 있게 되었으며, 이에 따라 인도의 상업용 분산형 에너지 발전 시장은 2025년에 연평균 35%의 성장률을 기록했습니다. 아세안(ASEAN) 국가들은 옥상 태양광 발전의 잠재력을 극대화하기 위해 현지 은행 및 개발 금융 기관을 활용하여 160억 달러 규모의 자금 격차를 메우고 있습니다.

중동 및 아프리카은 2031년까지 연평균 성장률(CAGR) 13.1%를 나타낼 것으로 예측되며, 이는 세계에서 가장 빠른 성장 속도입니다. 만안 국가들은 천연가스를 수출용으로 확보하기 위해 태양광 발전과 전력 저장을 결합한 시스템을 도입하고 있습니다. 한편, 남아프리카공화국, 케냐, 나이지리아에서는 산업용 전력 공급이 60% 미만에 그치는 송전망 환경에서 가동 시간을 유지하기 위해 디젤 발전과 태양광 발전을 결합한 하이브리드 시스템에 의존하고 있습니다.

북미는 2025년에도 상업용 분산형 에너지 발전 시장에서 큰 점유율을 유지했으나, 최대 3년에 달하는 계통 연계 대기 기간의 장기화와 2027년 이후 연방 세액 공제의 단계적 폐지가 시장의 성장세를 둔화시키고 있습니다. 유럽에서는 독일과 스페인의 저전압 배전선로가 포화 상태에 이르고, 막대한 비용이 소요되는 송전망 업그레이드를 피할 수 없는 실정입니다. 남미에서는 브라질과 칠레를 제외하고는 아직 발전 단계에 있지만, 2025년 아르헨티나에서 시행된 규제 완화 개혁에 따라 2027년 이후 도입이 가속화될 가능성이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the commercial distributed energy generation market size was valued at USD 150.40 billion in 2025 and is estimated to grow from USD 162.42 billion in 2026 to reach USD 234.26 billion by 2031, at a CAGR of 7.60% during the forecast period (2026-2031).

This report is Segmented by Technology (Solar PV, Wind Turbines, Fuel Cells, CHP, Battery-Storage-Coupled DER, Others), Application (Office Buildings, Retail, Data Centers, Educational Institutions, Hospitals, Warehouses, Airports, Others), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). Market Forecasts are Provided in Value (USD).

Global Commercial Distributed Energy Generation Market Trends and Insights

Declining LCOE of Solar PV & Wind

Utility-scale solar reached USD 29 per MWh in 2025, and commercial rooftop systems now deliver USD 50-70 per MWh in high-insolation zones, undercutting retail tariffs in 23 U.S. states. Chinese polysilicon oversupply pushed spot module prices below USD 0.10 per watt, while rapid-shutdown electronics trimmed installation labor by 30%. Companies, therefore, face a choice between fixed-rate PPAs and self-financed arrays with four-to-six-year paybacks. The fall in costs explains why solar is the fastest-growing slice of the commercial distributed energy generation market.

Corporate Renewable PPAs & Net-Zero Targets

Cumulative corporate renewable PPAs reached 50 GW worldwide by end-2025, 60% of which originated in North America and Europe. Portfolio-scale deals such as Google's 1 GW contract with TotalEnergies and Microsoft's 10.5 GW partnership with Brookfield bundle multiple technologies and oblige developers to add two-to-four-hour batteries. Because the obligation to deliver round-the-clock clean power shifts intermittency risk away from the buyer, PPAs accelerate project bankability and drive deeper penetration of distributed assets on commercial sites.

High Upfront CAPEX & Long Payback Period

Commercial solar still costs USD 1.57 per watt in the United States, and fuel-cell CHP reaches USD 6.00 per watt, translating to multi-million-dollar investments that small businesses rarely self-finance. Energy-as-a-service contracts remove capital barriers but exclude customers lacking investment-grade credit, leaving 60% of potential offtakers unserved.

Other drivers and restraints analyzed in the detailed report include:

- Extension of Net-Metering & ITC-Type Incentives

- Resilience Demand Amid Rising Grid Outage Risks

- Distribution-Grid Hosting-Capacity Saturation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fuel cells captured 37.6% of the commercial distributed energy generation market share in 2025, reflecting their value in hospitals, data centers, and industrial sites that need uninterrupted heat and power. Bloom Energy deployed more than 100 MW at Equinix facilities and lined up a 900 MW hydrogen-ready contract in Wyoming, moves that underpin its leadership. The solar segment is scaling faster, expanding at a 14.4% CAGR to 2031 as module prices dip below USD 0.10 per watt. Coupling rooftop PV with two-to-four-hour batteries slashes dependence on grid imports during evening peaks and trims demand charges, hastening payback to five to six years.

Wind turbines remain niche because zoning rules restrict 100-500 kW machines to industrial campuses with generous setbacks, while microturbine and reciprocating-engine hybrids continue to dominate off-grid mining and agribusiness use cases. Battery prices falling to USD 120 per kWh in 2025 spur adoption of one-to-two-hour storage as an add-on rather than a standalone system, reinforcing solar's position as the default growth engine in the commercial distributed energy generation market context. In parallel, hydrogen-blended CHP offers a pathway to deep decarbonization without sacrificing dispatchability, a feature that could preserve fuel-cell relevance during the forecast period.

Geography Analysis

Asia-Pacific dominated with 45.3% revenue in 2025. China alone installed 18 GW of commercial rooftop solar in 2025 and mandates 20-30% on-site renewables within new industrial parks. India's open-access reforms let corporations bypass distribution companies and have propelled the commercial distributed energy generation market in the country to 35% annual growth during 2025. ASEAN economies are filling a USD 16 billion financing gap with local banks and development finance institutions to unlock rooftop potential.

The Middle East and Africa are forecast to grow at 13.1% CAGR to 2031, the fastest worldwide. Gulf states deploy solar-plus-storage to free natural gas for export, while South Africa, Kenya, and Nigeria rely on diesel-solar hybrids to maintain uptime amid grids that serve industry less than 60% of the time.

North America retained a significant share of the commercial distributed energy generation market in 2025, but interconnection queues stretching up to three years and the scheduled sunset of federal tax credits after 2027 weigh on momentum. Europe's saturation of low-voltage feeders in Germany and Spain forces costly grid upgrades. South America remains nascent outside Brazil and Chile, though Argentina's liberalizing reforms in 2025 could accelerate adoption after 2027.

- Siemens AG

- Schneider Electric

- Caterpillar Inc.

- General Electric (GE Vernova)

- Bloom Energy

- Sunnova Energy

- Enel X

- Aggreko Ltd

- Eaton Corporation

- Tesla Energy

- ABB Ltd.

- Johnson Controls

- Engie SA

- Cummins Inc.

- Wartsila Corporation

- Capstone Green Energy

- Generac Power Systems

- Vicinity Energy

- Veolia (Microgrids)

- NextEra Energy Resources

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Declining LCOE of Solar PV & Wind

- 4.2.2 Corporate renewable PPAs & net-zero targets

- 4.2.3 Extension of net-metering & ITC-type incentives

- 4.2.4 Resilience demand amid rising grid outage risks

- 4.2.5 AI-enabled DER orchestration platforms

- 4.2.6 Hydrogen-ready micro-cogeneration with fuel cells

- 4.3 Market Restraints

- 4.3.1 High upfront CAPEX & long payback period

- 4.3.2 Evolving interconnection & tariff complexity

- 4.3.3 Distribution-grid hosting-capacity saturation

- 4.3.4 ESG traceability scrutiny for PV & wind supply chains

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Solar PV

- 5.1.2 Wind Turbines

- 5.1.3 Fuel Cells

- 5.1.4 Combined Heat and Power (CHP)

- 5.1.5 Battery-Storage-Coupled DER

- 5.1.6 Others

- 5.2 By Application

- 5.2.1 Office Buildings

- 5.2.2 Retail Stores

- 5.2.3 Data Centers

- 5.2.4 Educational Institutions

- 5.2.5 Hospitals

- 5.2.6 Warehouses and Logistics Centres

- 5.2.7 Airports and Transport Hubs

- 5.2.8 Others (incl campuses, hotels)

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Spain

- 5.3.2.5 Nordic Countries

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 ASEAN Countries

- 5.3.3.6 Australia and New Zealand

- 5.3.3.7 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 South Africa

- 5.3.5.4 Egypt

- 5.3.5.5 Rest of Middle East and Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Siemens AG

- 6.4.2 Schneider Electric

- 6.4.3 Caterpillar Inc.

- 6.4.4 General Electric (GE Vernova)

- 6.4.5 Bloom Energy

- 6.4.6 Sunnova Energy

- 6.4.7 Enel X

- 6.4.8 Aggreko Ltd

- 6.4.9 Eaton Corporation

- 6.4.10 Tesla Energy

- 6.4.11 ABB Ltd.

- 6.4.12 Johnson Controls

- 6.4.13 Engie SA

- 6.4.14 Cummins Inc.

- 6.4.15 Wartsila Corporation

- 6.4.16 Capstone Green Energy

- 6.4.17 Generac Power Systems

- 6.4.18 Vicinity Energy

- 6.4.19 Veolia (Microgrids)

- 6.4.20 NextEra Energy Resources

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment