|

시장보고서

상품코드

2062472

군발 두통 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Cluster Headache - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

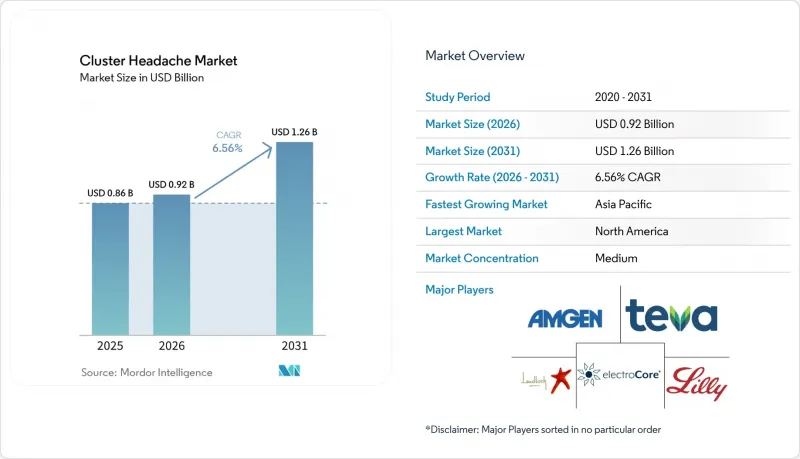

Mordor Intelligence에 의하면, 군발 두통 시장 규모는 2025년 8억 6,000만 달러로 평가되었습니다. 2026년에는 9억 2,000만 달러로 확대되어 2031년까지 12억 6,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR 6.56%로 성장할 전망입니다.

본 보고서는 진단 유형(임상 평가 등), 치료 유형(급성기 등), 약물 분류(트립탄 계열, 기타), 투여 경로(경구, 주사, 기타), 유통 채널(병원, 소매, 온라인, 기타), 환자 유형(발작성, 만성), 지역(북미, 유럽, 아시아태평양, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

세계의 군발 두통 시장 동향 및 인사이트

표적형 생물학적 제제 및 신약의 확대

발작성 군발 두통 치료제로 승인된 유일한 CGRP 단일클론 항체인 갈카네즈마브는 주요 임상시험에서 3주 시점에서 71.4%의 반응률을 보였습니다. Organon은 2024년, 2,250만 달러 규모의 계약을 통해 11개 신규 시장으로의 상용화를 확대했습니다. 이는 희귀질환 적응증에 대한 보험 급여 지급에 대한 지급 주체의 의지를 반영한 것입니다. 에프티네주맙을 대상으로 한 2025년 ALLEVIATE 임상시험은 주요 평가 변수를 달성하지는 못했으나, 지연된 효능의 가능성을 시사하고 있으며, 이는 보험 지급 기관들이 지속적인 반응이라는 평가 기준으로 전환하고 있음을 시사합니다. 플레마네즈맙의 무효성으로 인한 임상시험 중단은 생물학적 제제의 유효성 편차를 여실히 드러내며, 발작 빈도에 따른 환자군 선별 중요성을 재확인시켜 줍니다. 2026년 메타분석을 통해 발작성 질환에 대한 단기적 유효성의 우월성이 확인됨에 따라, 향후 임상시험 설계는 아형별 계층화로 나아갈 것입니다.

가정용 비침습적 미주신경 자극 요법의 보급

GammaCore는 2017년에 급성기 치료용으로, 2018년에 예방용으로 미국 승인을 획득한 후, 2019년에는 비용 절감 효과가 인정되어 환자 1인당 연간 450파운드(570달러)의 비용이 절감되었습니다. PREVA 임상시험에서는 위약군에서 주당 2.1회였던 발작 횟수가 5.9회 감소한 것으로 나타났으며, 동반 발작 치료제 사용도 57% 감소했습니다. Salvia BioElectronics는 2025년, AI 제어 방식의 자극 기능을 갖춘 초박형 임플란트 개발을 위해 6,000만 달러를 조달하고, ‘획기적인 의료기기(Breakthrough Device)’ 지정을 획득했습니다. 유럽의 CLUSTERSENSE 이니셔티브는 바이오센서와 폐쇄 루프 자극 장치를 통합하여 증상 완화까지 걸리는 시간을 5분 미만으로 단축하는 것을 목표로 하고 있습니다. 한국에서는 보험 적용을 받으려면 여전히 12개월간의 경구 예방약 치료가 실패해야 한다는 조건이 적용되고 있어, 신경조절요법에 대한 접근이 지연되고 있습니다.

두통 전문의 부족과 진단 지연

미국에서는 인증을 받은 두통 전문의가 고작 564명에 불과하여, 필요한 3,700명에서 4,500명에 비해 심각한 부족 현상을 겪고 있습니다. 이러한 부족으로 인해 성인의 평균 대기 시간은 30일, 소아 환자의 경우 최대 6개월의 지연이 발생하고 있습니다. 오진은 환자의 거의 절반에게 영향을 미치며, 치료까지 걸리는 기간을 6년이나 늘리고, 응급실 방문을 증가시키고 있습니다. 이동 거리가 먼 지방에 거주하는 미국인들은 전문의 진료를 받기 위해 70-81마일(약 113-130킬로미터)이나 이동하는 경우가 많아, 기존의 사회경제적 격차를 더욱 심화시키고 있습니다. 'HEADACHE법'은 원격의료에 대한 자금 지원을 강화하는 것을 목적으로 하고 있지만, 주마다 다른 보상 정책이 법안 도입의 걸림돌이 되고 있습니다. 지불자 측의 개혁이나 지속적인 교육 프로그램이 병행되지 않는 한, 의료 종사자 증원만으로는 CGRP 단일클론 항체의 도입을 촉진하기에는 불충분할 수 있습니다.

부문별 분석

2025년, 이차적 원인을 배제하기 위한 MRI 및 CT 스캔의 보급에 힘입어 영상 진단이 군발 두통 시장의 41.23%를 차지했습니다. 단 32분 만에 결과를 확인할 수 있는 초고속 CGRP 검사에 기반한 바이오마커 검사는 2031년까지 연평균 8.10%의 성장률을 보일 것으로 예상되며, 이로 인해 진단 지연 시간을 대폭 단축할 것으로 전망됩니다. ICHD-3 기준에 따른 임상 평가가 여전히 주요 진단 방법인 반면, 49%에 달하는 오진율은 객관적인 바이오마커의 필요성을 여실히 보여주고 있습니다. 눈물 검사법은 전분석 단계에서의 분해에 대해 높은 내성을 보이지만, 유전자 패널은 침투율이 낮고 치료에의 응용도 제한적이기 때문에 여전히 연구 단계에 머물러 있습니다.

2025년에는 산소 요법이나 피하 투여용 수마트립탄으로 대표되는 급성기 치료가 매출의 65.44%를 차지했습니다. CGRP 단일클론항체(mAb)가 임상적 접근 방식을 장기적인 발작 억제로 전환함에 따라, 예방 요법은 2031년까지 연평균 성장률(CAGR) 7.60%를 나타낼 것으로 예측됩니다. 코르티코스테로이드를 이용한 브리지 요법이나 후두신경 차단술은 일시적인 해결책으로 작용하지만, 급성기 및 예방 단계만큼의 효과는 나타나지 않습니다. GammaCore가 급성기 치료와 예방 치료 모두에서 효과를 발휘하는 이중 특성은 하이브리드 치료 전략에 대한 관심을 높이고 있습니다.

지역별 분석

북미의 군발 두통 시장은 갈카네주맙 및 감마코어와 같은 치료법에 대해 메디케어 및 민간 보험이 제공하는 광범위한 보장 범위의 혜택을 누리고 있습니다. 이러한 장점은 대도시권에 구축된 전문의 네트워크에 의해 더욱 뒷받침되고 있습니다. 그러나 지방 지역에서는 여전히 의료 접근성 측면에서 큰 과제에 직면해 있습니다. HEADACHE법의 시행으로 텔레헬스(원격의료) 사업에 자금이 배정됨에 따라, 이러한 지역 간 격차 해소와 치료 접근성 개선이 이루어질 가능성이 있습니다. 또한, 게판 계열 약물에 초점을 맞춘 다수의 연구자 주도 임상시험이 진행되고 있는 점에서도 알 수 있듯이, 미국은 혁신을 적극적으로 추진하고 있습니다. 이러한 동향은 치료 선택지의 확대와 시장 내 미충족 의료 수요에 대응하기 위한 해당 지역의 노력을 여실히 보여주고 있습니다.

유럽에서는 통일된 임상 지침과 비용 대비 효과에 대한 강한 중시가 시장의 원동력이 되고 있습니다. 규제 당국의 미주신경 자극 요법 승인은 독일, 프랑스, 북유럽 국가들을 포함한 주요 시장의 보험 급여 정책에 영향을 미치고 있습니다. 또한, 유럽은 AI를 활용한 폐쇄 루프 신경 조절 시스템 개발 등의 노력을 통해 첨단 의료 기술의 선도자로서의 입지를 확고히 다지고 있습니다. 이러한 발전은 치료 성과 향상, 환자 관리 개선, 그리고 지역 전체에 걸친 혁신적인 솔루션 도입을 촉진할 것으로 기대됩니다.

아시아태평양에서는 단편적인 규제 체계에서 벗어나, 아세안(ASEAN) 및 ICH 지침에 기반한 통일된 기준으로의 전환이 진행되고 있습니다. 한국의 단계적 승인(스텝 에디트) 정책은 생물학적 제제의 즉각적인 도입에 걸림돌이 되고 있지만, 반면 일본의 엄격한 2년간의 시판 후 조사 절차는 확고한 안전성 데이터를 도출함으로써 이러한 치료법의 장기 사용에 대한 신뢰를 높이고 있습니다. 중국에서는 CGRP 단일클론 항체가 아직 국가 보험 의약품 목록에 포함되지 않았지만, 일부 도시에서는 시범 프로그램을 통해 혁신적인 가치 기반 계약 모델을 모색하고 있습니다. 이러한 노력은 첨단 치료법의 보다 광범위한 도입과 통합의 길을 열어, 해당 지역의 성장을 가속하고 환자의 치료 성과를 향상시킬 가능성이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the cluster headache market size is expected to increase from USD 0.86 billion in 2025 to USD 0.92 billion in 2026 and reach USD 1.26 billion by 2031, growing at a CAGR of 6.56% over 2026-2031.

This report is Segmented by Diagnosis Type (Clinical Assessment, and More), Treatment Type (Acute, and More), Drug Class (Triptans, and More), Route of Administration (Oral, Injectable, and More), Distribution Channel (Hospital, Retail, Online, and More), Patient Type (Episodic, Chronic), and Geography (North America, Europe, Asia-Pacific, and More). Market Forecasts are Provided in Terms of Value (USD).

Global Cluster Headache Market Trends and Insights

Expansion of Targeted Biologics & Novel Therapeutics

Galcanezumab, the only CGRP monoclonal antibody approved for episodic cluster headaches, demonstrated a 71.4% responder rate by week 3 in pivotal studies. Organon expanded its commercialization efforts to 11 new markets in 2024 through a USD 22.5 million deal, reflecting payers' willingness to reimburse orphan indications.' The 2025 ALLEVIATE trial for eptinezumab did not meet its primary endpoint but indicated potential delayed benefits, suggesting a shift by payers toward sustained-response benchmarks. Fremanezumab's futility stop highlights the variability in biologics, reinforcing the importance of attack-frequency-based enrichment arms. A 2026 meta-analysis confirmed superior short-term efficacy in episodic diseases, guiding future trial designs toward subtype stratification.

Home-Use Non-Invasive Vagus Nerve Stimulation Uptake

GammaCore, after receiving U.S. clearance for acute use in 2017 and preventive use in 2018, was endorsed in 2019 for its cost-saving potential, with projected annual savings of GBP 450 (USD 570) per patient. The PREVA study demonstrated a reduction of 5.9 attacks per week compared to 2.1 with a sham, along with a 57% decrease in abortive medication usage. Salvia BioElectronics secured USD 60 million in 2025 to develop ultra-thin implants with AI-controlled stimulation, achieving Breakthrough Device status. Europe's CLUSTERSENSE initiative is integrating biosensors with closed-loop stimulators to reduce time-to-relief to under five minutes.In South Korea, reimbursement policies still require 12 months of failed oral prevention before coverage, delaying access to neuromodulation solutions.

Scarcity of Headache Specialists & Diagnostic Delays

With only 564 board-certified headache specialists available, the U.S. faces a significant shortfall compared to the required 3,700 to 4,500. This shortage results in average wait times of 30 days for adults and delays of up to six months for pediatric patients. Misdiagnosis affects nearly half of the patients, extending their care pathway by six years and increasing emergency department visits. Rural Americans, facing longer travel distances, often journey 70 to 81 miles for specialist consultations, exacerbating existing socioeconomic disparities. While the HEADACHE Act aims to enhance telehealth funding, inconsistent reimbursement policies across states limit its adoption. Expanding the workforce alone may not be sufficient to drive CGRP mAb adoption without concurrent payer reforms and continuous education initiatives.

Other drivers and restraints analyzed in the detailed report include:

- AI-Powered Wearable Headache-Diary Analytics

- Orphan-Drug Reimbursements & Rising Healthcare Spend

- Cardiovascular Safety Flags for Long-Acting CGRP mAbs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, imaging captured 41.23% of the cluster headache market, driven by the widespread use of MRI and CT scans to eliminate secondary causes. Biomarker assays, supported by ultra-rapid CGRP tests delivering results in just 32 minutes, are expected to grow at an annual rate of 8.10% through 2031, significantly reducing diagnostic delays. While clinical evaluations based on ICHD-3 criteria remain the primary diagnostic method, a 49% misdiagnosis rate highlights the critical need for objective biomarkers. Tear-fluid assays demonstrate resilience against preanalytical degradation, while genetic panels remain confined to research due to low penetrance and limited therapeutic applications.

In 2025, acute treatments, led by oxygen and subcutaneous sumatriptan, accounted for 65.44% of the revenue. Preventive therapies are projected to grow at a 7.60% CAGR through 2031, as CGRP mAbs shift the clinical approach toward long-term attack suppression. Corticosteroid bridges and occipital nerve blocks serve as transitional solutions but lack the scale of acute and preventive segments. GammaCore's dual functionality in both acute and preventive treatment is driving interest in hybrid therapeutic strategies.

Geography Analysis

North America's cluster headache market benefits from extensive Medicare and commercial coverage for treatments such as galcanezumab and gammaCore. This advantage is further supported by a well-established network of specialists in metropolitan areas. However, rural regions continue to face significant challenges in accessing care. The implementation of the HEADACHE Act could allocate funding to telehealth initiatives, aiming to address these geographic disparities and improve access to treatment. Additionally, the United States is actively fostering innovation, as evidenced by the numerous investigator-initiated trials focusing on gepants. These developments highlight the region's commitment to advancing treatment options and addressing unmet needs in the market.

In Europe, the market is driven by harmonized clinical guidelines and a strong emphasis on cost-effectiveness. The endorsement of vagus-nerve stimulation by regulatory bodies has influenced reimbursement policies across key markets, including Germany, France, and Nordic countries. Moreover, Europe is positioning itself as a leader in advanced medical technologies, with initiatives such as the development of AI-enabled closed-loop neuromodulation systems. These advancements are expected to enhance treatment outcomes, improve patient care, and drive the adoption of innovative solutions across the region.

The Asia-Pacific region is undergoing a transition from fragmented regulatory frameworks to unified standards under ASEAN and ICH guidelines. While South Korea's step-edit policies present barriers to the immediate adoption of biologics, Japan's stringent two-year post-marketing surveillance process generates robust safety data, fostering greater confidence in the long-term use of these treatments. In China, although CGRP monoclonal antibodies are not yet included in the National Reimbursement Drug List, pilot programs in select cities are exploring innovative value-based contracting models. These initiatives could pave the way for broader adoption and integration of advanced therapies, driving growth and improving patient outcomes in the region.

- Abbvie

- Amgen

- AstraZeneca

- Cipla

- Dr. Reddy's Laboratories

- electroCore, Inc.

- Eli Lilly and Company

- Endo International

- GE HealthCare Technologies Inc.

- Hikma Pharmaceuticals

- Impel NeuroPharma, Inc.

- Johnson & Johnson

- Koninklijke Philips

- Lundbeck A/S

- Magstim Company Ltd.

- Nevro

- Novartis

- Otsuka

- Pfizer

- Salvia BioElectronics B.V.

- Satsuma Pharmaceuticals, Inc.

- Siemens Healthineers

- Teva Pharmaceutical Industries

- UCB

- Upsher-Smith Laboratories

- WraSer Pharmaceuticals, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Diagnosed Patient Population

- 4.2.2 Expansion of Targeted Biologics & Novel Therapeutics

- 4.2.3 Orphan-Drug Reimbursements & Rising Healthcare Spend

- 4.2.4 CGRP Point-of-Care Biomarker Assays Accelerate Diagnosis

- 4.2.5 Home-Use Non-Invasive Vagus Nerve Stimulation Uptake

- 4.2.6 AI-Powered Wearable Headache-Diary Analytics

- 4.3 Market Restraints

- 4.3.1 High Therapy Cost Burden on Payers & Patients

- 4.3.2 Scarcity of Headache Specialists & Diagnostic Delays

- 4.3.3 Cardiovascular Safety Flags for Long-Acting CGRP Mabs

- 4.3.4 Limited Neuromodulation Reimbursement Outside NA/EU5

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Diagnosis Type

- 5.1.1 Clinical Assessment

- 5.1.2 Imaging

- 5.1.2.1 MRI

- 5.1.2.2 CT

- 5.1.3 Biomarker Assays

- 5.1.4 Wearable Neuro-physiological Monitoring

- 5.1.5 Genetic Testing

- 5.2 By Treatment Type

- 5.2.1 Acute Treatment

- 5.2.2 Preventive Treatment

- 5.2.3 Transitional Therapy

- 5.3 By Drug Class

- 5.3.1 Triptans

- 5.3.2 CGRP Monoclonal Antibodies

- 5.3.3 Ergot Alkaloids

- 5.3.4 Calcium-Channel Blockers (Verapamil)

- 5.3.5 Lithium Carbonate & Miscellaneous

- 5.4 By Route of Administration

- 5.4.1 Oral

- 5.4.2 Injectable

- 5.4.3 Intranasal

- 5.4.4 Inhalation (Medical Oxygen)

- 5.4.5 Neuromodulation Device

- 5.5 By Distribution Channel

- 5.5.1 Hospital Pharmacies

- 5.5.2 Retail Pharmacies

- 5.5.3 Online Pharmacies

- 5.5.4 Specialty Clinics

- 5.5.5 Home Healthcare Providers

- 5.6 By Patient Type

- 5.6.1 Episodic Cluster Headache

- 5.6.2 Chronic Cluster Headache

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 Australia

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East & Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East and Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 Amgen Inc.

- 6.3.3 AstraZeneca plc

- 6.3.4 Cipla Ltd.

- 6.3.5 Dr. Reddy's Laboratories Ltd.

- 6.3.6 electroCore, Inc.

- 6.3.7 Eli Lilly & Co.

- 6.3.8 Endo International plc

- 6.3.9 GE HealthCare Technologies Inc.

- 6.3.10 Hikma Pharmaceuticals PLC

- 6.3.11 Impel NeuroPharma, Inc.

- 6.3.12 Johnson & Johnson (Janssen)

- 6.3.13 Koninklijke Philips N.V.

- 6.3.14 Lundbeck A/S

- 6.3.15 Magstim Company Ltd.

- 6.3.16 Nevro Corp.

- 6.3.17 Novartis AG

- 6.3.18 Otsuka Pharmaceutical Co., Ltd.

- 6.3.19 Pfizer Inc.

- 6.3.20 Salvia BioElectronics B.V.

- 6.3.21 Satsuma Pharmaceuticals, Inc.

- 6.3.22 Siemens Healthineers AG

- 6.3.23 Teva Pharmaceutical Industries Ltd.

- 6.3.24 UCB S.A.

- 6.3.25 Upsher-Smith Laboratories, LLC

- 6.3.26 WraSer Pharmaceuticals, LLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment