|

시장보고서

상품코드

2062474

5PL(Fifth-party Logistics) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Fifth-party Logistics (5PL) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

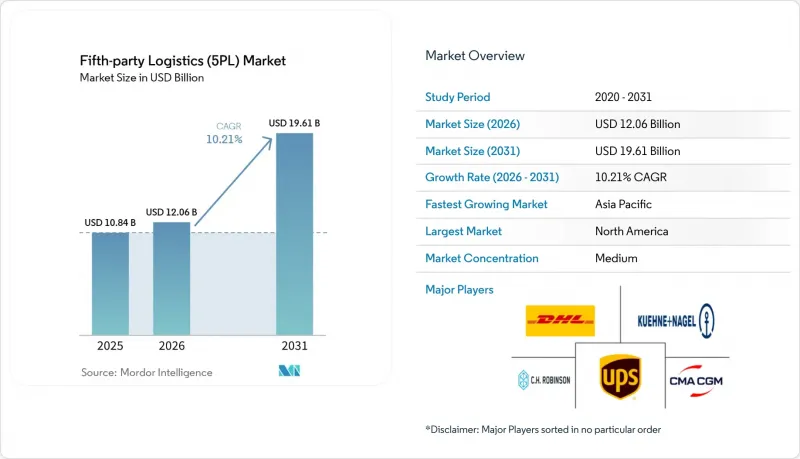

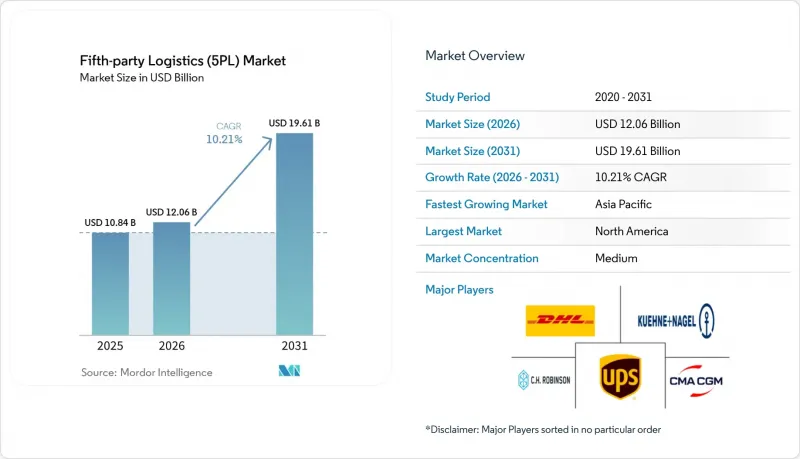

Mordor Intelligence에 의하면, 5PL(Fifth-party Logistics) 시장 규모는 2025년 108억 4,000만 달러로 평가되었습니다. 2026년 120억 6,000만 달러로 확대되어 2031년까지 196억 1,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR은 10.21%를 나타낼 전망입니다.

본 보고서는 서비스 모델(운송 서비스 등), 최종 사용자 산업(전자상거래·소매 등), 비즈니스 모델(전자상거래 직결형, 3PL/4PL용 애그리게이터/인테그레이터 등), 기업 규모(대기업 등) 및 지역(북미, 남미 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 5PL(Fifth-party Logistics) 시장 동향과 인사이트

D2C 브랜드의 확장이 턴키형 풀필먼트 수요를 견인하고 있습니다.

디지털 퍼스트 브랜드들은 창고 관리, 배송, 반품을 단일 계약으로 포괄하는 원스톱 물류 서비스를 요구함으로써 조달 전략을 재구축하고 있습니다. 학술 연구에 따르면, 옴니채널 소매업체는 오프라인 매장, 온라인 주문, 픽업 지점을 동시에 처리할 수 있는 재고 관리 알고리즘이 필요하며, 이러한 복잡성이 5PL(Fifth-party Logistics) 시장 공급업체들에게 유리하게 작용하고 있습니다. 이러한 브랜드들이 독자적으로 네트워크를 구축할 수 있는 규모를 갖춘 경우는 드물기 때문에 턴키 방식의 5PL 솔루션을 통해 수년에 걸치는 인프라 구축 기간이 수 주일로 단축됩니다. 아시아태평양에서 소셜 커머스의 확산은 결제, 재고 가시화, 당일 배송을 통합한 플랫폼에 대한 수요를 더욱 높이고 있습니다. 탁월한 주문 처리 능력은 현재 고객 확보 비용에 직접적인 영향을 미치기 때문에 통합된 5PL 파트너십은 전략적인 마케팅 수단이 되고 있습니다.

팬데믹 이후 옴니채널 재고 관리의 복잡화

팬데믹으로 인해 소매업체들은 오프라인 매장과 디지털 채널을 병행하여 운영할 수밖에 없게 되었으며, 재고 배치와 관련된 의사결정 건수가 두 배로 늘어났습니다. 조사 결과에 따르면, 기업은 운전자금을 늘리지 않으면서 서비스 목표를 달성하기 위해 다수의 물류 거점을 동기화해야 하는 것으로 확인되었습니다. 기존 도구만으로는 계절성, 프로모션, 실시간 수요 파악 간의 균형을 맞추기에는 부족합니다. 5PL(제5자 물류) 시장의 선도 기업들은 상품을 지속적으로 재배치하는 컨트롤 타워 내에 머신러닝 엔진을 통합함으로써 이 과제를 해결하고 있습니다. 소매업체들은 서비스 수준 향상과 안전 재고 감축이라는 이점을 바탕으로, 물류 최적화를 이익률 향상의 원동력으로 삼고 있습니다.

전 세계 마이크로 풀필먼트 네트워크의 자본 집약적 구축

당일 배송을 위해서는 인구 밀집 도시 지역에 소규모 창고가 필요하지만, 지가 급등과 자동화 설비 비용으로 인해 자본 요건이 소규모 신규 진출기업이 감당하기 어려운 수준까지 치솟고 있습니다. 손익분기점 분석에 따르면, 수익성은 주문 밀도에 달려 있지만, 많은 지역에서 이는 불확실한 변수입니다. 또한, 여러 고객을 위한 재고 분리 역시 간접비를 증가시키고 가동률을 저하시키고 있습니다. 이러한 경제적 요인으로 인해, 자금력이 풍부한 사업자들이 유리한 입지를 확보하기 위해 경쟁사를 인수하는 등 업계 재편이 진행되고 있습니다. 초기 투자가 성장세를 둔화시켜 업계 전체의 연평균 성장률(CAGR)을 끌어내리고 있습니다.

부문별 분석

2025년 기준으로 운송 서비스는 제3자 물류 시장의 49.83%를 차지했으나, 상품화 압력으로 인해 지출이 부가가치 서비스로 이동하고 있으며, 해당 서비스는 2031년까지 연평균 성장률(CAGR) 15.59%로 확대되고 있습니다. 고객들은 화물 운송을 점점 더 기본적인 요건으로 간주하며, 컨설팅, 분석, 블록체인 통합을 하나의 패키지로 제공할 수 있는 능력을 바탕으로 계약을 결정하고 있습니다. 이러한 구조의 변화로 인해, 과거에는 물류 핵심 예산 범위에 포함되지 않았던 자문 기능을 포함한 5PL(Fifth-party Logistics) 시장 규모가 확대되고 있습니다. 소포의 밀도가 높아 빈번한 배송 노선을 유지할 수 있기 때문에 라스트 마일 배송에서는 여전히 도로 운송이 주류를 이루고 있지만, 복합 운송 최적화 도구를 통해 긴급성이 낮은 화물은 해상 운송으로 전환되면서 탄소 발자국 감축이 진행되고 있습니다.

‘Robotics-as-a-Service(RaaS)’의 도입은 이러한 변화를 여실히 보여주고 있습니다. DHL 등의 물류 업체들은 변동비 기반 계약을 통해 Locus사의 자율 주행 로봇 군을 통합함으로써, 화주의 자본 지출 없이도 수거율을 높이고 있습니다. 재고 관리 모듈에는 유럽의 ‘디지털 제품 여권’ 요건을 충족하기 위해 블록체인이 점점 더 많이 도입되고 있습니다. 이러한 기능 덕분에 고객 1인당 교차 판매 수익이 향상되며, 기존의 요금 기반 관계에서 발생하는 것보다 훨씬 더 높은 이탈 비용이 발생합니다. 컨설팅 및 기술 부문 매출이 트럭 운송 부문의 매출을 앞지르는 속도로 성장하고 있기 때문에 현재 시장 가치는 지적 재산권과 데이터 분석의 심도 여부에 따라 좌우되고 있습니다.

2025년, 전자상거래 및 소매 업계는 D2C(소비자 직접 판매)의 성장세에 힘입어 5PL(Fifth-party Logistics) 시장에서 37.97%의 점유율을 유지했으나, 의료 및 제약 업계는 연평균 성장률(CAGR) 13.35%로 확대될 것으로 예측되어 가장 빠르게 성장하는 최종 사용자층이 될 전망입니다. 백신 온도 관리 요건 및 위조 방지 규제로 인해 완벽한 추적성이 요구되고 있으며, 블록체인과 IoT 센서를 융합한 5PL 플랫폼은 이 분야에서 뛰어난 성능을 발휘합니다. 취급량 면에서는 소매업이 여전히 지배적이지만, 의약품은 특수한 포장과 규정 준수 조치가 필요하기 때문에 단위당 수익은 높은 임베디드니다. 아시아태평양에서 소셜 커머스와 라이브 스트리밍 쇼핑의 융합으로 인해 국경 간 소포 발송량이 증가하고 있으며, 이에 따라 통합된 통관 서류 및 관세 납부 자동화에 대한 수요가 높아지고 있습니다.

식품 및 음료 기업들 역시 변동하는 레스토랑 및 식료품점 수요에 맞추어 재고를 조정할 수 있는 콜드체인 최적화를 추구하며, 5PL(Fifth-party Logistics) 시장공급업체들로 몰리고 있습니다. 제조업체는 5PL 컨트롤 타워를 활용하여 입고되는 부품과 출하되는 완제품의 조정을 통해 체류 시간을 단축하고 있습니다. 모든 산업 분야에서 도입 기업들을 하나로 묶는 공통된 요인은 사내의 소규모 팀만으로는 쉽게 관리하기 어려울 정도로 공급망이 점점 더 복잡해지고 있다는 점입니다.

지역별 분석

북미는 2025년, 성숙한 전자상거래 생태계와 창고 운영사의 자동화 도입 비용을 절감해 주는 ‘Robotics-as-a-Service(RaaS)’의 조기 도입에 힘입어 5PL(Fifth-party Logistics) 시장 매출의 36.72%를 차지했습니다. 운송업체 배정 알고리즘의 편향성에 대한 규제 당국의 감독은 미국과 캐나다에서 가장 엄격하며, 주요 업체들은 경로 설정 엔진에 공정성 감사 및 설명 가능한 AI 요소를 도입하도록 권고받고 있습니다. D2C(Direct-to-Consumer) 브랜드의 급증으로 소포 물동량이 증가함에 따라, 이는 지방 도시에서의 마이크로 풀필먼트 확장을 정당화하는 한편, 물류 플랫폼에 통합된 금융 서비스는 대안적인 자금 조달 수단을 모색하는 소규모 판매자들 사이에서 지지를 얻고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR)이 11.97%로, 가장 빠르게 성장하고 있는 지역입니다. 중국, 동남아시아, 호주를 연결하는 크로스보더 전자상거래 회랑은 소포 유통을 빈번하게 발생시키고 있으며, 통일된 통관 절차와 관세 선납 기능의 혜택을 누리고 있습니다. 인도 및 인도네시아에서 공급망 디지털화를 위한 정부 보조금은 중견 제조업체들이 운영 조정을 ‘제5자 물류(5PL)’ 시장 플랫폼에 위탁하도록 장려하고 있습니다. 중국 주요 도시에서 도시 정체 요금제가 도입됨에 따라, 창고 운영 업체들은 더 좁은 공간에서도 운용 가능한 자율 주행 로봇을 도입해야 하는 상황에 놓여 있으며, 이로 인해 RaaS(Robot-as-a-Service)의 보급이 가속화되고 있습니다. 또한, 니어쇼어링의 동향 역시 브랜드들이 단일 국가에서의 조달에서 벗어나 다각화를 모색하는 가운데, 베트남과 태국의 물류 허브에 대한 투자를 촉진하고 있습니다.

유럽에서는 광범위한 지속가능성 규제의 영향으로 꾸준한 성장을 이어가고 있습니다. ‘탄소 국경 조정 메커니즘(CBAM)’은 상세한 배출량 보고를 의무화하고 있으며, 수입업체들은 인증된 산정 엔진을 갖춘 5PL 제공업체를 이용해야 합니다. ‘디지털 제품 여권’ 프로그램은 패션 및 전자제품 공급망 전반에 걸쳐 블록체인 도입을 가속화하고 있습니다. 컴플라이언스 대응과 주문 처리 서비스를 하나로 묶어 제공하는 사업자는 운송에만 주력하는 자산 집약형 경쟁사들에 비해 우위를 점하고 있습니다. 남미 및 중동 및 아프리카는 인프라 면에서 뒤처져 있지만, 일부 도시 지역에서는 공유형 마이크로 풀필먼트 시범 프로젝트가 진행되고 있어, 자금이 확보된다면 향후 격차를 좁힐 가능성이 있음을 시사하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the fifth-Party logistics market size is expected to increase from USD 10.84 billion in 2025 to USD 12.06 billion in 2026 and reach USD 19.61 billion by 2031, growing at a CAGR of 10.21% over 2026-2031.

This report is Segmented by Service Model (Transportation Services, and More), by End-User Industry (E-Commerce & Retail, and More), by Business Model (Direct To E-Commerce, Aggregator/Integrator for 3PL/4PL, and More), by Enterprise Size (Large Enterprises, and More), and by Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Fifth-party Logistics (5PL) Market Trends and Insights

Direct-to-Consumer Brand Expansion Fueling Turnkey Fulfillment Demand

Digital-first brands are reshaping procurement strategies by insisting on single-source logistics that cover warehousing, shipping, and returns under a single contract. Academic studies show that omnichannel retailers need inventory algorithms that can serve storefronts, online orders, and pickup points simultaneously, a complexity that favors Fifth-Party Logistics market providers. These brands rarely have the scale to build networks on their own, so turnkey 5PL solutions collapse multi-year infrastructure timelines into weeks. Social commerce adoption in the Asia-Pacific further amplifies demand for platforms that blend payments, inventory visibility, and same-day delivery. Superior fulfillment now directly influences customer acquisition costs, making integrated 5PL partnerships a strategic marketing lever.

Heightened Omnichannel Inventory Complexity Post-Pandemic

The pandemic pushed retailers to run physical stores and digital channels in parallel, multiplying the number of stock-placement decisions. Research confirms companies must synchronize many fulfillment nodes to hit service targets without inflating working capital. Off-the-shelf tools are inadequate for balancing seasonality, promotions, and real-time demand sensing. Fifth-Party Logistics market leaders solve this by embedding machine-learning engines inside control towers that continuously reposition goods. Retailers benefit from higher service levels and reduced safety stocks, turning logistics optimization into a margin driver.

Capital-Heavy Build-Out of Global Micro-Fulfillment Networks

Same-day delivery requires micro-warehouses in dense urban areas, but high land prices and the cost of automation equipment push capital requirements beyond the reach of smaller entrants. Break-even analysis shows profitability hinges on high order density, an uncertain variable in many locales. Inventory segregation for multiple clients also drives overhead, eroding utilization rates. These economics encourage consolidation as well-funded providers purchase rivals to secure prime sites. Up-front spending slows expansion pace, trimming overall industry CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Supply-Chain Resilience Needs Amid Geopolitical Disruptions

- Plug-and-Play Robotics-as-a-Service Bundled into 5PL Contracts

- Ocean-Freight Capacity Volatility Weakening Optimization Accuracy

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation Services controlled 49.83% of the Fifth-Party Logistics market share in 2025, yet commoditization pressures are redirecting spending toward Value-Added Services that are accelerating at a 15.59% CAGR through 2031. Clients increasingly view freight movement as a baseline requirement and award contracts based on the provider's ability to deliver consulting, analytics, and blockchain integration in one bundle. This mix change is expanding the Fifth-Party Logistics market size for advisory functions that once sat outside core logistics budgets. Road transport still dominates last-mile delivery because parcel density supports frequent routes, while multimodal optimization tools shift non-urgent volumes to sea lanes to shrink carbon footprints.

Robotics-as-a-service deployments underscore the pivot. Providers such as DHL integrate fleets of Locus autonomous mobile robots under variable-cost arrangements, improving pick rates for shippers without capital expense. Inventory management modules increasingly embed blockchain to meet Digital Product Passport mandates in Europe. These capabilities boost cross-sell revenue per customer and raise switching costs well above those in traditional rate-based relationships. As advisory and tech income grow faster than trucking revenue, market valuations now hinge on intellectual property and depth of data analytics.

E-commerce & Retail retained 37.97% share of the Fifth-Party Logistics market in 2025 thanks to direct-to-consumer momentum, yet Healthcare & Pharma is projected to climb at a 13.35% CAGR, making it the fastest-growing end-user bloc. Vaccine temperature-control mandates and anti-counterfeit regulations compel full traceability, an area where 5PL platforms that marry blockchain and Internet-of-Things sensors excel. Retailers still dominate by volume, but pharmaceuticals deliver higher revenue per unit because of specialized packaging and compliance tasks. The convergence of social commerce and livestream shopping in the Asia-Pacific increases cross-border parcel counts, reinforcing demand for unified customs documentation and duty-payment automation.

Food & Beverage companies also gravitate to Fifth-Party Logistics market providers for cold-chain orchestration that aligns inventory with fluctuating restaurant and grocery demand. Industrial manufacturers leverage 5PL control towers to coordinate inbound parts with outbound finished goods, reducing dwell times. Across sectors, the thread that unites adopters is rising supply-chain complexity that small internal teams cannot easily master.

Geography Analysis

North America held 36.72% of the Fifth-Party Logistics market revenue in 2025, underpinned by mature e-commerce ecosystems and early adoption of robotics-as-a-service, which lowers automation entry costs for warehouse operators. Regulatory scrutiny over algorithmic bias in carrier allocation is strongest in the United States and Canada, prompting leading providers to embed fairness audits and explainable-AI components in their routing engines. Direct-to-consumer brand proliferation is adding parcel density that justifies micro-fulfillment rollout in secondary cities, while embedded finance on logistics platforms is gaining traction among small sellers seeking alternative credit.

Asia Pacific is the fastest-growing region with an 11.97% CAGR through 2031. Cross-border e-commerce corridors linking China, Southeast Asia, and Australia generate high-frequency parcel flows that benefit from unified customs clearance and duty pre-payment features. Government grants for supply-chain digitalization in India and Indonesia encourage mid-tier manufacturers to outsource orchestration to the Fifth-Party Logistics market platforms. Urban congestion fees in major Chinese cities are pushing warehouse operators to adopt autonomous mobile robots that can work in tighter footprints, accelerating RaaS uptake. Nearshoring trends also spur investment in Vietnamese and Thai fulfillment hubs as brands diversify away from single-country sourcing.

Europe maintains steady growth driven by far-reaching sustainability regulations. The Carbon Border Adjustment Mechanism demands granular emissions reporting, prompting importers to enlist 5PL providers with certified calculation engines. The Digital Product Passport program accelerates blockchain deployment across fashion and electronics supply chains. Providers offering packaged compliance plus fulfillment gain an advantage over asset-heavy rivals focused solely on transport. Although South America and the Middle East & Africa lag in infrastructure, select urban centers see pilot projects for shared micro-fulfillment, signaling future catch-up potential as capital becomes available.

- DHL Supply Chain (DHL Group)

- CEVA Logistics (CMA CGM Group)

- Kuehne + Nagel International AG

- UPS Supply Chain Solutions

- C.H. Robinson Worldwide

- DSV A/S

- DB Schenker

- Maersk Logistics and Services

- GXO Logistics

- GEODIS

- Ryder System, Inc.

- Nippon Express Holdings (NX Group)

- Toll Group

- Amazon Global Logistics

- Cainiao Smart Logistics Network (Alibaba Group)

- JD Logistics

- Uber Freight

- Flexport Inc.

- Sennder Technologies

- ShipBob

- Expeditors International of Washington, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Direct-to-consumer brand expansion fuelling turnkey fulfilment demand

- 4.2.2 Heightened Omni-Channel Inventory Complexity Post-Pandemic

- 4.2.3 Blockchain Provenance Mandates Enhancing Outsourcing Appeal

- 4.2.4 Supply-Chain Resilience Needs Amid Geopolitical Disruptions

- 4.2.5 Plug-and-Play Robotics-as-a-Service Bundled into 5Pl Contracts

- 4.2.6 Embedded Finance Services Within 5Pl Control-Tower Platforms

- 4.3 Market Restraints

- 4.3.1 Capital-Heavy Build-Out of Global Micro-Fulfilment Networks

- 4.3.2 Ocean-Freight Capacity Volatility Weakening Optimisation Accuracy

- 4.3.3 Regulatory Scrutiny of Algorithmic Bias In Carrier Allocation

- 4.3.4 Carbon Border Adjustment Compliance Burden on 5Pl Providers

- 4.4 Porter's Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Competitive Rivalry

- 4.5 Value / Supply-Chain Analysis

- 4.6 Technological Innovations in the Industry

- 4.7 Government Regulations and Policies

- 4.8 Impact of Geopolitical Events on the Market

5 Market Size & Growth Forecasts

- 5.1 By Service Model

- 5.1.1 Transportation Services

- 5.1.1.1 Road

- 5.1.1.2 Air

- 5.1.1.3 Sea

- 5.1.1.4 Multimodal

- 5.1.2 Warehousing & Fulfillments

- 5.1.3 Inventory Mangement

- 5.1.4 Value Added Services (tech, analytics, consulting, etc.)

- 5.1.1 Transportation Services

- 5.2 By End-user Industry

- 5.2.1 E-commerce & Retail

- 5.2.2 Consumer Packaged Goods

- 5.2.3 Food & Beverage (incl. Cold-chain)

- 5.2.4 Healthcare & Pharma

- 5.2.5 Industrial & Manufacturing

- 5.2.6 Others

- 5.3 By Business Model / Client Type

- 5.3.1 Direct to E-commerce

- 5.3.2 Aggregator/Integrator for 3PL/4PL

- 5.3.3 Custom Supply Chain Orchestration for Enterprises

- 5.3.4 Platform-based, Technology-driven Outsourcing

- 5.3.5 Others (Government/public sector, alliance-based logistics orchestration, project based events/exhibitions)

- 5.4 By Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small & Medium Enterprises (SMEs)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Southeast Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 Europe

- 5.5.4.1 United Kingdom

- 5.5.4.2 Germany

- 5.5.4.3 France

- 5.5.4.4 Spain

- 5.5.4.5 Italy

- 5.5.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.4.8 Rest of Europe

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 DHL Supply Chain (DHL Group)

- 6.4.2 CEVA Logistics (CMA CGM Group)

- 6.4.3 Kuehne + Nagel International AG

- 6.4.4 UPS Supply Chain Solutions

- 6.4.5 C.H. Robinson Worldwide

- 6.4.6 DSV A/S

- 6.4.7 DB Schenker

- 6.4.8 Maersk Logistics and Services

- 6.4.9 GXO Logistics

- 6.4.10 GEODIS

- 6.4.11 Ryder System, Inc.

- 6.4.12 Nippon Express Holdings (NX Group)

- 6.4.13 Toll Group

- 6.4.14 Amazon Global Logistics

- 6.4.15 Cainiao Smart Logistics Network (Alibaba Group)

- 6.4.16 JD Logistics

- 6.4.17 Uber Freight

- 6.4.18 Flexport Inc.

- 6.4.19 Sennder Technologies

- 6.4.20 ShipBob

- 6.4.21 Expeditors International of Washington, Inc.