|

시장보고서

상품코드

2062475

에너지 개보수 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Energy Retrofit - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

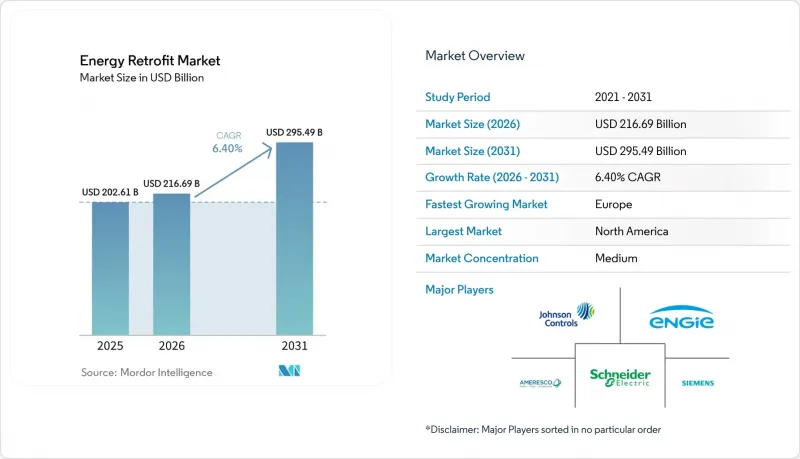

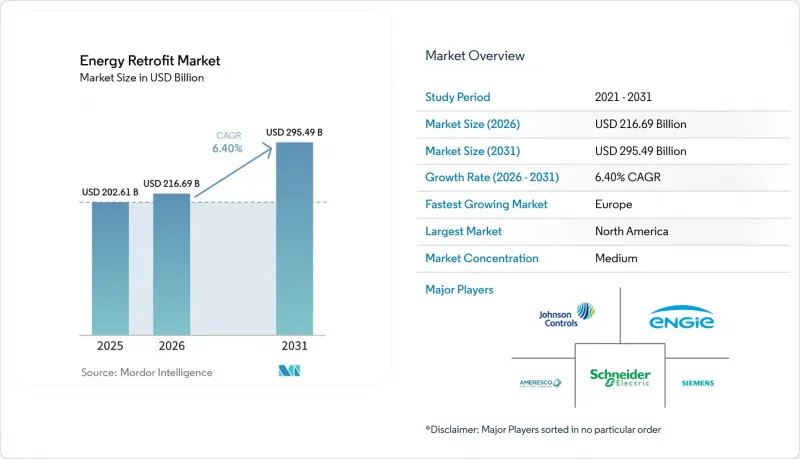

Mordor Intelligence에 의하면, 에너지 개보수 시장 규모는 2025년 2,026억 1,000만 달러로 평가되었습니다. 2026년에는 2,166억 9,000만 달러로 확대되어 2031년까지 2,954억 9,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR은 6.40%를 나타낼 전망입니다.

본 보고서는 개보수 규모(대규모 에너지 개보수, 소규모/경미한 에너지 개보수), 기술(HVAC 시스템, 조명 시스템, 건축 외피 등), 용도(주택, 상업용 건물 등) 및 지역(북미, 유럽, 아시아·태평양, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 에너지 개보수 시장 동향 및 인사이트

정부의 에너지 효율화 의무화 및 인센티브

유럽연합(EU)의 개정된 ‘건축물의 에너지 성능에 관한 지침’은 2024년에 회원국별로 국내법으로 제정되어, 자발적인 개보수를 법적 의무로 전환하는 법정 개보수 요건을 규정하고 있습니다. 독일은 2024년, BEG 프로그램의 일환으로 에너지 개보수 공사에 135억 유로를 지출했습니다. 또한, 프랑스의 ‘MaPrimeRenov’는 히트펌프 설치 지원금으로 26억 유로를 추가로 배정했습니다. 미국에서는 ‘인플레이션 억제법’ 제179D조에 따라, 에너지 소비량을 50% 감축하는 프로젝트에 대해 1제곱피트당 5달러의 세액 공제가 제공되게 되었습니다. 한편, ‘초당파 인프라법’을 통해 에너지 효율 및 에너지 절약 블록 보조금으로 35억 달러가 투입되었습니다. 일본에서는 2025년 4월에 시행된 개정 건축물 에너지 절약법에 따라 모든 신규 비주거용 건물에 에너지 절약 기준이 의무화됨에 따라, 선제적인 개보수 열풍이 일고 있습니다. 한국에서는 2025년 6월부터 제로에너지빌딩(ZEB) 의무 적용 대상이 500제곱미터 이상의 모든 공공건축물로 확대되며, 이에 더해 서울에서는 개보수 비용의 최대 50%를 지원하는 제도가 마련되어 있습니다.

기업의 탄소중립·ESG 약속이 리모델링 수요를 가속화

대기업들은 과학에 기반한 배출 감축 로드맵에 개조 비용을 직접 반영하고 있습니다. 이케아는 2030년까지 자사가 소유한 모든 매장을 탄소 중립화할 것을 목표로 하고 있으며, 2024년 말까지 400곳에 총 1.7GW 규모의 옥상 태양광 발전 설비를 설치했습니다. 리바이스 스트라우스는 2027년까지 시설의 90%를 개보수하고, 에너지 집약도를 40% 감축하겠다고 약속했습니다. 샌프란시스코 연방준비은행의 2024년 조사에 따르면, 과학에 기반한 목표를 공개한 기업들은 동종 업계의 다른 기업들에 비해 에너지 효율화 프로젝트에 23% 더 많은 자본을 투자하고 있는 것으로 나타났습니다. 이에 따라 자금 조달 수단도 발전하고 있습니다. HSBC는 2024년, 유럽의 REIT(부동산 투자 신탁)을 대상으로 5억 달러 규모의 지속가능성 연계형 대출을 구성하여, 검증된 포트폴리오의 에너지 집약도가 낮아짐에 따라 차입 비용을 절감할 수 있도록 했습니다.

기술 비용이 낮아졌음에도 불구하고, 초기 설비 투자(CAPEX)는 여전히 고액입니다.

종합적인 개보수 공사에서는 건물 외피 개보수, 공조 설비 교체, 제어 시스템 통합 등이 하나의 프로젝트로 묶이는 경우가 많으며, 그로 인해 일반적인 지출 규모는 6자리에서 7자리 수에 달할 전망입니다. 2024년 브리티시컬럼비아주에서 실시된 메타분석에 따르면, 대규모 개보수 비용의 중앙값은 1제곱피트당 150-250캐나다 달러(110-185달러)이며, 보조금을 받더라도 단순 회수 기간은 15년을 초과하여 많은 투자자의 보유 기간보다 훨씬 더 길어집니다. 유럽연합 집행위원회는 2030년 개보수 목표 달성을 위해 필요한 연간 자금 부족액을 950억 유로로 추산하고 있습니다. 인도에서도 이와 같은 자금 부족이 우려되고 있으며, 조사 대상 소유자의 68%가 행동을 가로막는 주요 요인으로 초기 비용을 꼽았습니다. 그린뱅크나 온빌 파이낸스 같은 새로운 방식은 유망하지만, 여전히 일부 미국 주와 EU 국가들로 한정되어 있습니다.

부문별 분석

2025년 에너지 개보수 시장 규모의 64.4%를 차지한 것은 ‘소규모 개보수’였으며, 이는 LED 조명으로의 교체, 스마트 온도 조절기 설치, 저비용 단열재 추가와 같이 최소한의 불편함으로 15%-25%의 절감 효과를 가져오고 투자 회수 기간이 짧은 대책이 소유주들에게 선호되고 있음을 반영합니다. 대규모 개보수는 자본 집약적이긴 하지만, 넷제로 규제로 인해 포트폴리오의 에너지 집약도를 50% 이상 감축해야 하는 상황에서 연평균 성장률(CAGR) 8.6%로 확대되고 있습니다. 미국의 ‘베터 빌딩 이니셔티브(Better Building Initiative)’ 프로젝트에서 나타난 38%라는 중앙값의 에너지 절감 효과는 이 프로젝트의 잠재적 이점을 입증하며, 효율 연계형 금융 하에서의 장기 상환 일정을 정당화하는 근거가 됩니다.

업계의 밸류체인은 양극화되어 있습니다. 전기 공사업체는 대규모 및 소규모 공사를 주도하는 한편, 대규모 개보수 프로젝트의 경우 성과 연계형 계약 하에 외피 재설계, 기계 설비 업그레이드, 재생에너지 설비 설치를 통합할 수 있는 전문 엔지니어링 기업이 참여하고 있습니다. 패시브하우스 인증은 신뢰성의 지표로 부상하고 있으며, 2024년에는 전 세계적으로 1,840건의 리모델링 프로젝트가 인증을 받았는데, 이는 2022년 대비 64% 증가한 수치입니다. 유럽투자은행이 폴란드와 루마니아의 공동주택 대규모 개보수를 위해 제공한 2억 유로 규모의 대출 한도는 에너지 절감 효과를 기반으로 한 부채 구조에 대한 투자자들의 관심이 높아지고 있음을 보여줍니다.

지역별 분석

북미는 미국 연방 정부의 적극적인 세제 혜택과 주 차원의 그린뱅크 대출 프로그램의 지원을 받아, 2025년 에너지 개보수 시장 매출의 38.9%를 차지했습니다. 캘리포니아주가 2026년부터 신축 상업용 건물에 의무화할 예정인 ‘태양광 발전 + 에너지 저장’ 요건이 개보수 공사 분야로도 확대됨에 따라, 해당 지역의 규제 강화 추세는 더욱 가속화될 전망입니다.

연평균 성장률(CAGR) 9.0%의 성장이 예상되는 유럽은 EPBD(에너지 성능에 관한 건축물 지침)의 엄격한 준수 기한과 독일의 BEG(에너지 효율화법), 영국의 공공 부문 탈탄소화 보조금 등 수십억 유로 규모의 보조금 제도의 혜택을 받고 있습니다. 그러나 유럽집행위원회는 연간 950억 유로의 자금 부족을 경고하고 있으며, 이에 따라 리모델링용 주택담보대출 포트폴리오나 EU가 지원하는 보증 제도와 같은 혁신적인 금융 상품이 개발되고 있습니다.

아시아·태평양 지역의 동향은 다양합니다. 중국의 제14차 5개년 계획에서는 2025년까지 3억 5,000만 제곱미터의 개보수를 목표로 했지만, 그 이행 상황은 성마다 크게 달랐습니다. 일본에서는 2025년 4월부터 건축물 에너지 기준이 강화됨에 따라, 상업시설을 중심으로 리모델링 열풍이 일고 있습니다. 한편, 한국에서는 적극적인 제로에너지 의무화가 공공시설의 개보수 시 절반을 보조하는 제도를 통해 이를 촉진하고 있습니다. 라틴아메리카 및 중동 및 아프리카에서는 브라질의 PROCEL이나 UAE의 Estidama와 같은 주요 프로그램들이 향후 규모 확대를 위한 규제 기반을 마련하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the energy retrofit market size is expected to increase from USD 202.61 billion in 2025 to USD 216.69 billion in 2026 and reach USD 295.49 billion by 2031, growing at a CAGR of 6.40% over 2026-2031.

This report is Segmented by Retrofit Depth (Deep Energy Retrofits, Shallow/Light Energy Retrofits), Technology (HVAC Systems, Lighting Systems, Building Envelope, and More), Application (Residential Buildings, Commercial Buildings, and More), and Geography Geography (North America, Europe, Asia-Pacific, South America and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Energy Retrofit Market Trends and Insights

Government Energy-Efficiency Mandates & Incentives

The European Union's recast Energy Performance of Buildings Directive, transposed by member states in 2024, sets statutory renovation requirements that convert optional upgrades into legal obligations. Germany disbursed EUR 13.5 billion for efficiency upgrades under its BEG program during 2024, and France's MaPrimeRenov' added EUR 2.6 billion to subsidize heat-pump installations. In the United States, Section 179D of the Inflation Reduction Act now offers a USD 5 per-square-foot deduction for projects achieving 50% energy cuts, while the Bipartisan Infrastructure Law funneled USD 3.5 billion through Energy Efficiency and Conservation Block Grants. Japan's revised Building Energy Conservation Law, effective April 2025, imposed mandatory savings standards on all new non-residential properties, prompting a wave of pre-emptive retrofits. South Korea's Zero Energy Building mandate was extended to all public buildings above 500 square meters in June 2025, complemented by a Seoul subsidy that covers up to 50% of retrofit costs.

Corporate Net-Zero/ESG Commitments Accelerating Retrofit Demand

Large enterprises are writing retrofit spending directly into science-based emission-reduction roadmaps. IKEA aims to upgrade every owned store to net-zero energy by 2030, installing 1.7 GW of rooftop solar across 400 sites by end-2024. Levi Strauss has committed to retrofit 90% of its facilities by 2027 to slash energy intensity 40%. The Federal Reserve Bank of San Francisco's 2024 study showed that firms with public science-based targets devote 23% more capital to efficiency projects compared with peers. Financing tools are evolving in tandem: HSBC arranged a USD 500 million sustainability-linked loan for a European REIT in 2024, reducing borrowing costs as verified portfolio energy intensity falls.

High Upfront CAPEX Despite Falling Tech Costs

Comprehensive retrofits often group envelope upgrades, HVAC replacements, and controls integration into one project, pushing typical spends into six- or seven-figure territory. A 2024 British Columbia meta-analysis found median deep-retrofit costs of CAD 150-250 per square foot (USD 110-185), with simple payback exceeding 15 years even after subsidies, far longer than many investors' hold periods. The European Commission pegs the annual funding gap for its 2030 renovation target at EUR 95 billion. Similar gaps loom in India, where 68% of surveyed owners cited upfront cost as the primary deterrent to action. Emerging tools such as green banks and on-bill financing are promising but remain limited to select U.S. states and a handful of EU nations.

Other drivers and restraints analyzed in the detailed report include:

- Ageing Building Stock in OECD Economies Requiring Upgrades

- Volatile Electricity & Gas Prices Prompting Payback-Driven Retrofits

- Landlord-Tenant Split-Incentive Dilemma

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Shallow retrofits captured 64.4% of the 2025 Energy Retrofit Market size, reflecting owners' preference for quick-payback measures such as LED relamping, smart thermostats, and low-cost insulation top-ups that deliver 15%-25% savings with minimal disruption. Deep retrofits, though capital-intensive, are expanding at an 8.6% CAGR as net-zero mandates push portfolios toward more than 50% cuts in energy intensity. Median savings of 38% in U.S. Better Buildings Initiative projects underscore the upside, justifying long amortization schedules under efficiency-linked financing.

Industry value chains are bifurcating. Electrical contractors dominate high-volume shallow works, while deep projects attract specialist engineering firms that can integrate envelope redesign, mechanical upgrades, and renewable installations under outcome-based contracts. Passive House certification is emerging as a credibility marker, with 1,840 certified retrofit projects worldwide in 2024, up 64% from 2022. The European Investment Bank's EUR 200 million facility for multifamily deep retrofits in Poland and Romania demonstrates growing investor appetite for savings-backed debt structures.

Geography Analysis

North America captured 38.9% of the 2025 Energy Retrofit Market revenue, buoyed by generous U.S. federal tax incentives and state-level green-bank financing programs. The region's regulatory push will intensify as California's 2026 solar-plus-storage mandate for new commercial buildings spills over into retrofit scopes.

Europe, forecast to grow at 9.0% CAGR, benefits from the EPBD's hard compliance deadlines and multi-billion-euro subsidy pools such as Germany's BEG and the U.K.'s Public Sector Decarbonisation grants. Yet the European Commission warns of a EUR 95 billion annual financing gap, spurring creative instruments like renovation mortgage portfolios and EU-backed guarantee schemes.

Asia-Pacific trends are heterogeneous. China's 14th Five-Year Plan targets 350 million m2 of retrofits by 2025, but enforcement differs widely by province. Japan's April 2025 building-energy code stiffening is triggering a wave of upgrades in the commercial core, while South Korea's aggressive zero-energy mandate is catalyzing half-subsidized retrofits in public stock. Latin America and the Middle East-Africa, though flagship programs, Brazil's PROCEL and the UAE's Estidama, are laying regulatory foundations for future scale.

- Johnson Controls

- Ameresco

- Siemens AG

- Schneider Electric

- ENGIE

- Honeywell International

- ABB

- Daikin Industries

- Trane Technologies

- Carrier Global

- Bouygues Energies & Services

- Veolia Energy

- Enel X

- Rockwool Group

- Kingspan Group

- NORESCO

- Cenergistic

- Eaton Corporation

- Comfort Systems USA

- EMCOR Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government energy-efficiency mandates & incentives

- 4.2.2 Corporate net-zero/ESG commitments accelerating retrofit demand

- 4.2.3 Ageing building stock in OECD economies requiring upgrades

- 4.2.4 Volatile electricity & gas prices prompting payback-driven retrofits

- 4.2.5 AI-enabled building-twin analytics uncovering hidden savings

- 4.2.6 Growing adoption of outcome-based financing & ESG-linked loans

- 4.3 Market Restraints

- 4.3.1 High upfront CAPEX despite falling tech costs

- 4.3.2 Landlord-tenant split-incentive dilemma

- 4.3.3 Shortage of deep-retrofit skilled labor & project managers

- 4.3.4 Performance-risk perception & measurement uncertainty

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Investment & Funding Trends

5 Market Size & Growth Forecasts

- 5.1 By Retrofit Depth

- 5.1.1 Deep Energy Retrofits

- 5.1.2 Shallow/Light Energy Retrofits

- 5.2 By Technology

- 5.2.1 HVAC Systems

- 5.2.2 Lighting Systems

- 5.2.3 Building Envelope (Insulation and Glazing)

- 5.2.4 Renewable Integration (Solar PV, Solar Thermal)

- 5.2.5 Smart Building Controls and IoT

- 5.2.6 Water Heating and Plumbing

- 5.3 By Application

- 5.3.1 Residential Buildings

- 5.3.2 Commercial Buildings

- 5.3.3 Industrial Facilities

- 5.3.4 Public and Institutional Buildings

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 Nordic Countries

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 ASEAN Countries

- 5.4.3.6 Australia and New Zealand

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Johnson Controls

- 6.4.2 Ameresco

- 6.4.3 Siemens AG

- 6.4.4 Schneider Electric

- 6.4.5 ENGIE

- 6.4.6 Honeywell International

- 6.4.7 ABB

- 6.4.8 Daikin Industries

- 6.4.9 Trane Technologies

- 6.4.10 Carrier Global

- 6.4.11 Bouygues Energies & Services

- 6.4.12 Veolia Energy

- 6.4.13 Enel X

- 6.4.14 Rockwool Group

- 6.4.15 Kingspan Group

- 6.4.16 NORESCO

- 6.4.17 Cenergistic

- 6.4.18 Eaton Corporation

- 6.4.19 Comfort Systems USA

- 6.4.20 EMCOR Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment