|

시장보고서

상품코드

2062477

타이트가스 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Tight Gas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

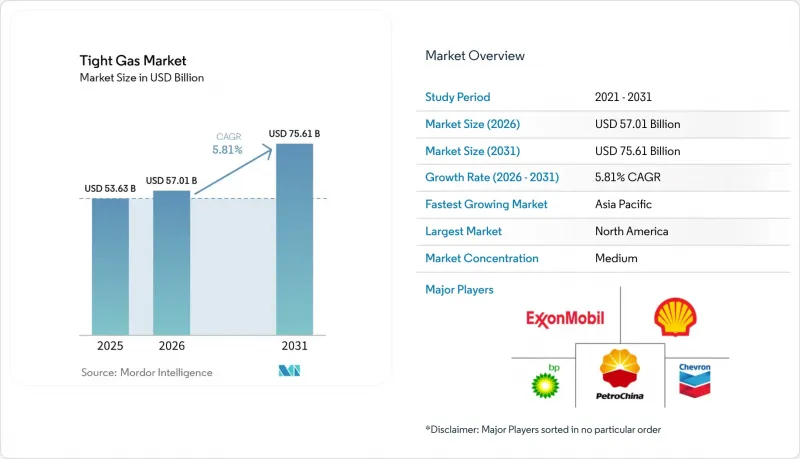

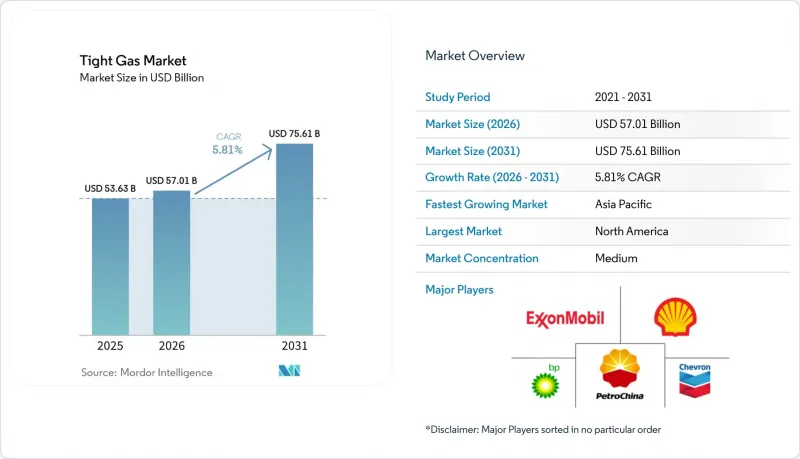

Mordor Intelligence에 의하면, 타이트가스 시장 규모는 2025년에 536억 3,000만 달러로 평가되었습니다. 2026년에 570억 1,000만 달러에서 2031년까지 756억 1,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR은 5.81%를 나타낼 전망입니다.

본 보고서는 자원 유형(사암, 석회암, 기타), 유정 유형(전통형, 비전통형), 입지(해양, 육상), 최종 사용자(대형 석유 및 가스 기업, 유틸리티체, 독립 생산자, 정부·국영 석유 회사, 기타), 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 타이트가스 시장 동향 및 인사이트

기존 가스 매장량의 감소

기존의 해양 및 육상 재래형 가스전은 현재 전 세계적으로 연간 6.8%의 속도로 생산량이 감소하고 있으며, 생산자들은 연간 약 5,000억 달러에 달하는 업스트림 부문 지출을 비재래형 매장지로 전환할 수밖에 없는 상황입니다. 1970년대에 가동을 시작한 홋카이도의 시설은 당초 최대 생산량의 30% 미만으로 운영되고 있는 반면, 미국 멕시코만 연안의 얕은 해역에서의 생산량은 2015년 이후 절반으로 줄었습니다. 헤인즈빌의 수평정 건설 비용은 약 800만 달러인 반면, 새로운 해양 플랫폼 건설에는 5,000만-1억 달러가 소요되므로, 사이클 중반의 가격 수준에서도 타이트가스 투자의 회수 속도는 빠릅니다. 중국석유천연가스그룹(CNPC)은 2025년에 쓰촨 분지의 타이트가스 생산량이 400억 m³를 넘어설 것이라고 보고했으며, 이는 다칭과 승리의 감산분을 상쇄하는 데 도움이 될 것입니다. 유럽 기업들도 마찬가지로 사업 구조를 재편하고 있으며, 토탈에너지스는 2024년에 성숙기에 접어든 북해 자산에서 철수하고, 아르헨티나 바카 무에르타 지역의 타이트가스 개발에 필요한 투자 자금을 확보했습니다.

전 세계 가스 화력 발전 수요 증가

2025년 전 세계 가스 화력 발전 용량이 85GW 증가한은 아시아·태평양 지역의 석탄에서 가스로의 전환과 북미의 급성장하는 데이터센터 전력 수요에 기인합니다. 미국의 드라이 가스 생산량은 2026년 하루 120.8억 입방피트(Bcf/d)에서 2027년에는 122.3억 입방피트(Bcf/d)로 증가할 전망이며, 그 증가분의 60%는 타이트층에서 공급될 것으로 보입니다. 장기 LNG 판매 계약이 업스트림 부문의 수익성을 뒷받침하고 있으며, 2025년에 승인된 미국 프로젝트를 통해 연간 800억 입방미터(bcm/yr) 이상의 액화 능력이 추가되었습니다. 카타르의 노스 필드 2단계 프로젝트는 2028년까지 하루 1.2 Bcf의 타이트 카보네이트 원료를 공급할 전망입니다. 인도는 2025년까지 12 GW 규모의 가스 피킹 발전소 건설을 승인했으나, 이 발전소들은 크리슈나-고다바리 지역의 타이트가스에 의존하게 될 것입니다.

환경 및 물 이용을 둘러싼 반대

콜로라도주의 타이트가스 유정 1개당 평균 물 사용량은 2024년에 1,717만 갤런으로 4배 증가했으며, 저수량이 부족한 시기에는 허가 일시 정지를 초래했습니다. 뉴멕시코주의 페코스강 협정은 산업용수 취수를 제한하고 있으며, 대규모 시추 우물의 수를 연간 15개 이하로 제한하고 있습니다. 현재 페르미안 분지에서 수압파쇄용 유체의 65%를 재생 생산수가 차지하고 있으며, 이로 인해 배럴당 0.50-0.80달러의 비용이 증가하고 있습니다. 프랑스와 독일에서는 여전히 수압 파쇄법이 금지되어 있어, 이로 인해 유럽에서 기술적으로 회수 가능한 타이트가스의 약 15조 입방피트가 개발되지 못하고 있습니다. 영국은 2024년에 모라토리엄을 해제했으나, 진도 0.5라는 기준을 유지하고 있어, 이로 인해 신규 유정 시추가 정체되고 있습니다.

부문별 분석

2025년, 사암은 타이트가스 시장 점유율의 64.2%를 차지했으며, 천연 파쇄 네트워크의 이점을 누리고 있는 메사바데와 헤인즈빌의 생산량이 그 기반을 이루고 있습니다. 석회암 시장은 산성 겔 처리 기술의 발전으로 인해 유정당 생산성이 약 30% 향상됨에 따라, 2031년까지 연평균 6.4%의 성장률을 기록하며 사암 시장을 추월할 것으로 전망됩니다. ADNOC이 2026년 1월에 승인한 SARB 심부 가스 개발 계획은 수심 4,500미터라는 깊은 깊이에도 불구하고, 쿠프층의 심부 탄산염암에 대한 업계의 열의를 입증하고 있습니다. 타이트 탄층 가스나 셰일·타이트층 혼합층 등 다른 자원 유형들도 2025년 시장 수익에 크게 기여했습니다.

비용 곡선은 암석의 유형에 따라 크게 달라집니다. 미국 중부 대륙의 사암 유정 시추 비용은 600만-800만 달러인 반면, 중동의 탄산염암 유정은 고온 완공 처리가 필요하기 때문에 1,500만 달러를 초과하는 경우가 많습니다. 그러나 석회암의 경우, 학습 곡선에 따른 이익 증가세가 더 가파릅니다. 카타르 에너지는 산 겔 시스템으로 전환한 후, 2025년에 유정당 생산성을 22% 향상시켰습니다. 호주에서는 퀸즐랜드 LNG 수요를 충족하기 위해 탄층 가스와 타이트가스의 수입을 균형 있게 조정하고 있으며, 하이브리드형 울프캠프층 유정은 원유 대 가스 비율이 확대될 경우 사업자에게 상품 선택의 여지를 제공합니다. 전반적으로, 타이트가스 시장은 북미 이외의 지역에서는 탄산염암으로 서서히 전환되는 추세를 보이고 있지만, 미국의 분지에서는 여전히 사암이 주류를 이루고 있습니다.

다단 수압 파쇄를 수반하는 수평 시추공은 2025년 매출의 78.7%를 차지했으며, 2031년까지 연평균 6.1%의 성장률을 나타낼 것으로 전망됩니다. 헤인즈빌의 수평 유정의 평균 초기 생산량은 하루 2,500만 입방피트인 반면, 수직 유정은 1,000만-2,000만 입방피트에 그치기 때문에 3-4배에 달하는 높은 설비 투자 비용이 정당화됩니다. 지표면의 제약으로 인해 수평 시추가 어려운 기존 유전에서는 여전히 기존 방식의 수직 시추가 주류를 이루고 있습니다.

아시아태평양에서는 도입이 가속화되고 있습니다. 중국석유화학(Sinopec)은 2025년에 푸링(Fuling)에서 85개의 수평 유정을 완공할 예정이며, 인도의 ONGC는 2026년 말까지 10개의 시범 유정을 시추할 계획입니다. 남미에서는 YPF가 2025년에 수직 시추 장비를 15대로 줄이는 한편, 현지 조달이 가능한 공급망 덕분에 수평 시추 장비를 180대로 확대했습니다. 앨버타주의 유정 간격에 관한 규제는 여전히 밀집된 타운십에서 수직 시추를 우선시하고 있으며, 규제, 지질 조건, 지상권이 복합적으로 작용하여 타이트가스 시장의 유정 유형 구성을 결정하고 있음을 보여줍니다.

지역별 분석

북미는 2025년에 45.3%의 점유율로 타이트가스 시장을 주도했으며, 퍼미안 분지에서 하루 15 Bcf, 헤인즈빌에서 하루 12 Bcf를 생산했습니다. LNG 수요에 대응하기 위해 시추가 건식 가스로 전환됨에 따라 성장률은 5.2%로 둔화되고 있습니다. 캐나다 몬토니와 듀버네이의 생산량은 2024년 코스트 가스링크의 가동에 힘입어 서쪽 방향의 LNG 수송 경로가 개통되었습니다. 페멕스가 해상 전통형 프로젝트를 우선시함에 따라 멕시코 부르고스의 생산량은 정체되었으며, 그 결과 미국으로의 파이프라인 수입량은 하루 6.8 Bcf에 달했습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 6.5%를 기록하며 가장 높은 성장세를 보일 전망입니다. 중국석유천연가스그룹(CNPC)은 2025년에 오르도스 분지의 생산량을 50억 입방미터 확대했으며, 쓰촨성의 생산량은 연간 400억 입방미터를 넘어 베이징의 석탄 소비를 대체했습니다. 인도는 크리슈나-고다바리 지역의 타이트가스에 의존하는 12기가와트 규모의 가스 피크 발전소를 승인했습니다. 호주의 쿠퍼 분지는 사업자들이 석탄층 가스를 우선시하는 한편, LNG 공급 계약을 위한 타이트가스 수입에 주력한 결과, 생산량이 보합세를 보였습니다.

유럽에서는 독일과 프랑스에서 수압 파쇄법이 금지됨에 따라 여러 과제에 직면해 있습니다. 영국은 모라토리엄을 해제했으나, 지진 위험 기준치가 상업적 생산에 걸림돌이 되고 있습니다. 에퀴노르는 북해 해저 타이백 프로젝트를 추진하고 있으며, 가즈프롬의 아치모프 타이트가스 매장량은 유럽 파이프라인으로공급을 계속하고 있지만, 제재로 인해 기술 유입은 제한되고 있습니다.

남미에서의 성장은 주로 아르헨티나의 바카 무에르타가 주도하고 있으며, YPF는 2025년까지 일일 생산량을 6,000만 입방미터로 늘렸으며, 파이프라인 건설 자금으로 30억 달러를 확보했습니다. 쉘과 에퀴놀은 2029년까지 LNG 수출을 목표로, 현지 타이트가스 프로젝트에 25억 달러를 투자하기로 결정했습니다. 브라질은 산토스 분지의 경제성을 평가하고 있는 반면, 볼리비아는 5억 달러 규모의 차코 프로그램을 시작했습니다.

중동 및 아프리카에서는 ADNOC가 SARB 심층 가스 프로젝트를 승인했으며, 2029년까지 일일 2억 표준 입방피트(MMscf/d)의 최대 생산량을 목표로 하고 있습니다. 카타르 에너지는 2026년부터 2030년까지의 1,500억 달러 예산 중 40%를 비전통적 가스 개발에 배정하고 있습니다. 사우디 아람코의 자프라 시범 프로젝트는 2030년까지 일일 20억 입방피트(Bcf/d)의 생산 달성을 목표로 하고 있습니다. 한편, 남아프리카의 카루 분지에서는 환경 심사 및 물 부족 문제로 인해 개발이 지연되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the tight gas market size is projected to be USD 53.63 billion in 2025, USD 57.01 billion in 2026, and reach USD 75.61 billion by 2031, growing at a CAGR of 5.81% from 2026 to 2031.

This report is Segmented by Resource Type (Sandstone, Limestone, Others), Well Type (Conventional, Unconventional), Location (Offshore, Onshore), End-User (Oil & Gas Majors, Utilities, Independent Producers, Government & NOCs, Others), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Tight Gas Market Trends and Insights

Declining Conventional Gas Reserves

Legacy offshore and onshore conventional gas fields now decline 6.8% per year globally, forcing producers to redirect roughly USD 500 billion of annual upstream spending toward unconventional deposits . North Sea facilities commissioned in the 1970s operate below 30% of their original plateau rates, while U.S. shallow-water Gulf of Mexico output has halved since 2015. A Haynesville horizontal well costs near USD 8 million versus USD 50-100 million for a new offshore platform, giving tight gas a rapid payback even at mid-cycle prices. CNPC reported Sichuan Basin tight-gas output topping 40 billion m3 in 2025, helping offset declines at Daqing and Shengli. European players are rebalancing similarly; TotalEnergies exited mature North Sea assets in 2024 to fund Argentina's Vaca Muerta tight-gas push.

Rising Global Gas-Fired Power Demand

Global additions of 85 GW of gas-fired capacity in 2025 stemmed from coal-to-gas switching in Asia-Pacific and fast-growing data-center loads in North America . U.S. dry-gas production is set to rise from 120.8 Bcf/d in 2026 to 122.3 Bcf/d in 2027, with tight formations supplying 60% of the increase. Long-dated LNG offtake contracts underwrite upstream economics; U.S. projects sanctioned in 2025 added more than 80 bcm/yr of liquefaction. Qatar's North Field Phase 2 will contribute 1.2 Bcf/d of tight-carbonate feedstock by 2028. India cleared 12 GW of gas-peaking plants in 2025 that will lean on Krishna-Godavari tight gas.

Environmental and Water-Use Opposition

Average water use per Colorado tight-gas well quadrupled to 17.17 million gal in 2024, prompting permit pauses during low-reservoir months . New Mexico's Pecos River Compact restricts industrial withdrawal, capping large-scale completions below 15 wells per year. Recycled produced water now covers 65% of Permian fracture fluid but adds USD 0.50-0.80/bbl to cost. France and Germany still ban hydraulic fracturing, blocking roughly 15 Tcf of technically recoverable European tight gas . The U.K. lifted its moratorium in 2024, yet keeps a magnitude-0.5 threshold that has stalled new wells.

Other drivers and restraints analyzed in the detailed report include:

- Technology Cost Deflation

- Tight-Gas / CCS Integration Unlocking Green Finance

- Gas-price volatility vs LNG & shale

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sandstone held 64.2% of the tight gas market share in 2025, anchored by Mesaverde and Haynesville outputs that benefit from natural fracture networks. The limestone market is projected to grow at an annual rate of 6.4% through 2031, surpassing sandstone, as advancements in acid-gel treatments enhance per-well productivity by approximately 30%. ADNOC's January 2026 SARB Deep Gas sanction underscores industry appetite for deep Khuff carbonates despite 4,500 m depths. Other resource types, such as tight coal-seam gas and hybrid shale-tight plays, significantly contributed to market revenue in 2025.

Cost curves vary sharply across rock types. Sandstone wells in the U.S. Mid-Continent drill for USD 6-8 million, while Middle East carbonate wells often exceed USD 15 million due to high-temp completions. Yet limestone offers steeper learning-curve gains; QatarEnergy lifted well productivity 22% in 2025 after switching to acid-gel systems. Australia balances coal-seam gas with tight imports to satisfy Queensland LNG, and hybrid Wolfcamp wells grant operators commodity optionality when oil-to-gas ratios widen. Overall, the tight gas market registers a gradual pivot toward carbonates outside North America, while sandstones remain dominant in U.S. basins.

Horizontal wells with multi-stage hydraulic fracturing accounted for 78.7% of 2025 revenue and are projected to expand at 6.1% through 2031. A Haynesville horizontal averages 25 MMcf/d initial output versus 1-2 MMcf/d for a vertical well, justifying the 3-4X capex premium. Conventional vertical wells persist in legacy fields where surface constraints discourage horizontals.

Asia-Pacific is accelerating adoption; Sinopec completed 85 horizontals at Fuling in 2025, and India's ONGC will drill 10 pilot wells by end-2026. In South America, YPF dropped vertical rigs to 15 in 2025 while boosting horizontals to 180, thanks to localized supply chains. Alberta's spacing rules still favor verticals in dense townships, demonstrating that regulation, geology, and surface rights collectively determine well-type mix within the tight gas market.

Geography Analysis

North America led the tight gas market with 45.3% share in 2025, producing 15 Bcf/d from the Permian and 12 Bcf/d from the Haynesville. Growth moderates to 5.2% as drilling migrates toward drier gas for LNG outlets. Canada's Montney and Duvernay flows benefited from the 2024 Coastal GasLink start-up, unlocking westward LNG pathways. Mexico's Burgos output stagnated as Pemex favored offshore conventional projects, leading U.S. pipeline imports to reach 6.8 Bcf/d.

Asia-Pacific posts the fastest 6.5% CAGR to 2031. CNPC expanded Ordos output by 5 bcm in 2025, and Sichuan exceeded 40 bcm/yr, displacing Beijing coal burn. India approved 12 GW of gas-peaking plants that will rely on Krishna-Godavari tight gas. Australia's Cooper Basin stayed flat as operators prioritized coal-seam gas while eyeing tight imports for LNG commitments.

Europe faces challenges due to the fracturing bans in Germany and France. While the United Kingdom has lifted its moratorium, seismic thresholds have hindered commercial operations. Equinor is advancing North Sea subsea tieback projects, and Gazprom's Achimov tight reserves continue to supply European pipelines, although sanctions have restricted technology inflow.

Growth in South America is primarily driven by Argentina's Vaca Muerta, where YPF plans to increase output to 60 MM m3/d by 2025 and has secured USD 3 billion in pipeline funding. Shell and Equinor have committed USD 2.5 billion to local tight gas projects, targeting LNG exports by 2029. Brazil is assessing the margins of the Santos Basin, while Bolivia has launched a USD 500 million Chaco program.

In the Middle East and Africa, ADNOC has approved the SARB Deep Gas project, targeting a plateau of 200 MMscf/d by 2029. QatarEnergy has allocated 40% of its USD 150 billion budget for 2026-2030 to unconventional gas development. Saudi Aramco's Jafurah pilot aims to achieve 2 Bcf/d by 2030. Meanwhile, South Africa's Karoo Basin faces delays due to environmental reviews and water scarcity issues.

- ExxonMobil Corporation

- Chevron Corporation

- Shell PLC

- bp p.l.c.

- TotalEnergies SE

- China National Petroleum Corp. (CNPC)

- ConocoPhillips

- Eni S.p.A.

- China Petroleum and Chemical Corporation

- Chesapeake Energy Corporation

- PetroChina Company Limited

- Equinor ASA

- Occidental Petroleum Corporation

- CNOOC Ltd

- Gazprom PJSC

- Woodside Energy Group Ltd

- QatarEnergy

- Repsol S.A.

- Ecopetrol S.A.

- Santos Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Declining conventional gas reserves

- 4.2.2 Rising global gas-fired power demand

- 4.2.3 Technology cost deflation (HZ drilling & frac)

- 4.2.4 Government incentives to monetise stranded gas

- 4.2.5 Tight-gas/CCS integration unlocking green finance

- 4.2.6 National energy-security mandates boosting domestic output

- 4.3 Market Restraints

- 4.3.1 Environmental & water-use opposition

- 4.3.2 Gas-price volatility vs LNG & shale

- 4.3.3 Induced-seismicity moratoria in emerging plays

- 4.3.4 Proppant-supply bottlenecks in remote basins

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Resource Type

- 5.1.1 Sandstone

- 5.1.2 Limestone

- 5.1.3 Others

- 5.2 By Well Type

- 5.2.1 Conventional

- 5.2.2 Unconventional

- 5.3 By Location

- 5.3.1 Offshore

- 5.3.2 Onshore

- 5.4 By End-user

- 5.4.1 Oil & Gas Majors

- 5.4.2 Utilities

- 5.4.3 Independent Producers

- 5.4.4 Government and NOCs

- 5.4.5 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 NORDIC Countries

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN Countries

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 ExxonMobil Corporation

- 6.4.2 Chevron Corporation

- 6.4.3 Shell PLC

- 6.4.4 bp p.l.c.

- 6.4.5 TotalEnergies SE

- 6.4.6 China National Petroleum Corp. (CNPC)

- 6.4.7 ConocoPhillips

- 6.4.8 Eni S.p.A.

- 6.4.9 China Petroleum and Chemical Corporation

- 6.4.10 Chesapeake Energy Corporation

- 6.4.11 PetroChina Company Limited

- 6.4.12 Equinor ASA

- 6.4.13 Occidental Petroleum Corporation

- 6.4.14 CNOOC Ltd

- 6.4.15 Gazprom PJSC

- 6.4.16 Woodside Energy Group Ltd

- 6.4.17 QatarEnergy

- 6.4.18 Repsol S.A.

- 6.4.19 Ecopetrol S.A.

- 6.4.20 Santos Limited

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment