|

시장보고서

상품코드

2062481

가솔린 발전기 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Gasoline Genset - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

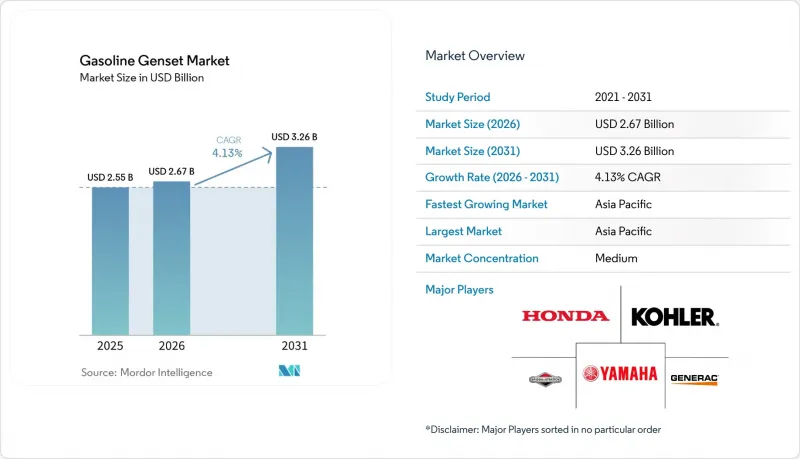

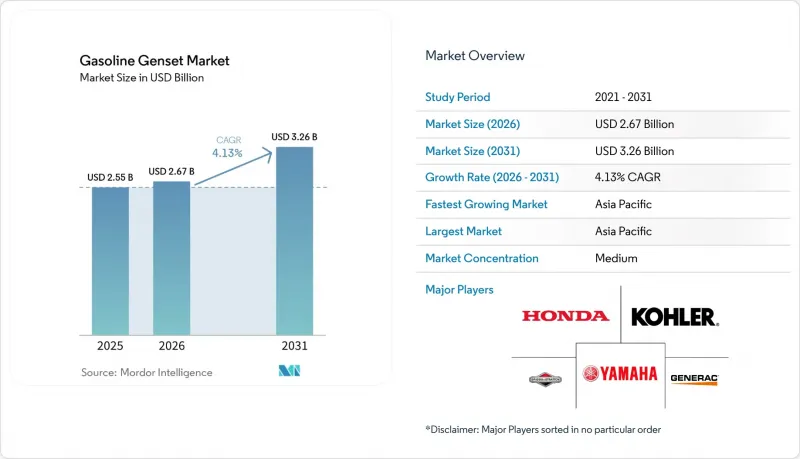

Mordor Intelligence에 의하면, 가솔린 발전기 시장 규모는 2025년 25억 5,000만 달러로 평가되었고, 2026년에는 26억 7,000만 달러로 추정되고, 2031년까지 32억 6,000만 달러에 이를 것으로 예상되고 있으며, 2026-2031년 CAGR 4.13%로 성장할 전망입니다.

본 보고서는 유형별(휴대용, 대기용, 인버터), 용량별(50KVA 미만, 50-330KVA, 330KVA 초과), 용도별(예비 전원, 피크 부하 완화, 주전원 및 연속 운전), 최종 사용자별(주거용, 상업용, 산업용), 지역별(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 가솔린 발전기 시장 동향 및 인사이트

노후화된 송전망 인프라로 인해 잦은 정전이 발생하고 있습니다.

미국의 전력 회사에 따르면, 송전선 및 변압기의 70% 이상이 설계 수명을 초과했으며, 이러한 노후화된 설비들이 2024년 허리케인 헬렌 당시 431건의 자동 정전 사태의 원인이 되었습니다. 뉴욕의 고객들은 2024년에 2023년 대비 162% 더 긴 정전 시간을 겪었으며, 이에 따라 많은 주택 소유자와 중소기업들이 확실한 장애 대비 체계를 확보하기 위해 예비용 가솔린 발전기를 구매할 수밖에 없었습니다. 유럽에서도 비슷한 추세가 나타나고 있으며, 여러 국가의 송전망에서는 지은 지 50년이 지난 목재 전신주가 여전히 사용되고 있어, 정기 점검 기간 중 백업 전원에 대한 수요가 증가하고 있습니다. 전력 회사들은 리클로저, 구획화 장치, 첨단 계측 장비를 도입하고 있지만, 송전망의 업그레이드는 수년 단위로 이루어지기 때문에 당분간은 가솔린 발전기 시장 수요가 높은 수준을 유지할 것으로 보입니다. 각 제조업체는 정전 발생 시 소유주에게 알리고 발전기 가동을 자동화하는 원격 모니터링 패키지를 도입함으로써 이러한 기회를 활용하고, 송전망 장애 시에도 중단 없는 가동을 보장하고 있습니다.

기상 이변에 따른 주택용 비상 전원 수요

미국 에너지정보청(EIA)의 기록에 따르면, 2024년에는 전력 회사 고객 1인당 10시간 이상의 정전이 발생했으며, 이는 지난 10년 동안 가장 높은 수준이었습니다. 그 중 80%는 대형 폭풍으로 인한 것이었습니다. 허리케인 '헬렌'과 '밀턴'으로 인해 470만 명의 고객이 정전 피해를 입은 데 이어, 캘리포니아주에서는 산불로 인한 공공 안전 확보를 위한 계획 정전이 급격히 확대되면서 각 가정에 예방 차원에서 비상 발전기를 설치할 것을 권고했습니다. 미국 해양대기청(NOAA)은 2026년 대서양 허리케인 시즌이 평년보다 활발할 것으로 예측하고 있으며, 이에 따라 주택 소유자들의 견고한 백업 시스템에 대한 수요가 더욱 높아지고 있습니다. 브릭스 앤 스트래튼의 26kW 'PowerProtect' 발전기는 65.6kVA의 모터 시동 능력을 갖추고 있으며, 연료 소비와 소음을 줄여주는 주 1회 간이 자가 진단 기능을 탑재하여 조용한 교외 지역 주민들에게 호평을 받고 있습니다. 며칠 동안 지속되는 정전 상황에서도 냉장고, 냉난방 설비, 주요 전자기기의 작동을 유지할 수 있는 턴키 솔루션을 찾는 가정이 늘어남에 따라, 가솔린 발전기 시장은 호황을 누리고 있습니다.

소형 점화식 엔진에 대한 배기가스 규제 강화

미국 환경보호청(EPA)의 3단계 규정에 따르면, 비이동식 엔진의 HC+NOx 배출 상한선을 8 g/kWh로 낮췄습니다. 한편, 유럽의 스테이지 V 규제에서는 입자 수 측정과 가동 중 적합성 감사가 추가되었습니다. 각 제조업체는 연료 분사 장치, 촉매 머플러, 증발 캐니스터를 도입하여 이에 대응하고 있지만, 그 결과 부품 비용이 상승하여 중량이나 차체 크기에 있어 설계상의 타협을 피할 수 없게 되었습니다. 인도의 CPCB IV+ 규정은 2024년 7월에 시행되었으며, 이미 최대 800kW 엔진을 대상으로 하고 있어, 각 OEM 업체에 대해 가솔린 및 디젤 모델 모두에 대한 인증 획득과 기존 차량에 대한 사후 장착 후처리 장치 제공을 의무화하고 있습니다. 적합성 시험 및 서류 작성은 엔지니어링 예산을 압박하고 제품 출시 주기를 길게 만들며, 학습 곡선과 규모의 경제를 통해 비용이 다시 낮아질 때까지는 가솔린 발전기 시장의 성장을 다소 둔화시킬 것입니다.

부문별 분석

2025년에는 휴대용 유닛이 가솔린 발전기 시장 매출의 54.2%를 차지했으며 시장 성장을 주도했습니다. 이는 일반 가정, 건설업체, 아웃도어 애호가들에게 어디든 휴대할 수 있다는 점이 확실한 매력임을 입증해 줍니다. 그러나 인버터 모델은 스마트 연료 분사 및 가변 속도 운전을 통해 소음과 연료 소비를 대폭 줄일 수 있어, 2031년까지 연평균 성장률(CAGR) 7.0%로 성장할 것으로 전망됩니다. 혼다의 iGX400 및 iGX430은 전자 제어, SAE J1939 연결성, 초크가 필요 없는 시동 기능을 통해 계절에 따른 사용 환경에서 고객이 겪는 문제를 어떻게 해결하고 있는지 보여줍니다. 비상용 발전기는 정전 증가라는 혜택을 누리고 있는 한편, 태양광 발전 및 에너지 저장 시스템과의 조용한 경쟁에 직면해 있습니다. 브릭스 앤 스트래튼의 26kW 'PowerProtect'는 비상 시 이외의 운전 주기에서도 인증을 받았으며, 소유자가 전력 회사 수요 반응 프로그램을 통해 수익을 창출할 수 있도록 함으로써 이러한 격차를 해소하고 있습니다. 따라서, 가솔린 발전기 시장은 청정 출력과 디지털 제어를 결합한 인버터 및 첨단 비상용 플랫폼으로 점차 전환되고 있습니다.

기존의 오픈 프레임형 휴대용 발전기는 특히 신흥 시장에서 경량 건설 및 DIY용 예비 전원으로 여전히 가격 면에서 우위를 점하고 있습니다. 그러나 각국의 소음 규제 및 엔진 기준 강화로 인해, 프리미엄 부문의 구매자들은 더욱 조용하고 친환경적인 인버터식 발전기로 전환하고 있습니다. 각 OEM 업체들은 손에 들고 다닐 수 있는 2-3kW 병렬 연결 지원 모델을 제품 라인업에 추가하고 있으며, 이러한 모델들은 5-7kW 오픈 프레임형 설계를 대체하는 모듈식 옵션으로서, 고부하 시에도 연결하여 사용할 수 있습니다. 소매 채널에서는 연료비 절감 시뮬레이터와 소음 수준 비교를 전면에 내세워, 기존 발전기 소유자들이 인버터식 발전기로 전환하도록 유도함으로써, 가솔린 발전기 시장에서 인버터식의 점유율 확대를 지속적으로 뒷받침하고 있습니다.

2025년에는 50kVA 미만 기종이 가솔린 발전기 시장 점유율의 73.5%를 차지했으며, 주택용 비상 전원, 키오스크, 소규모 건설 현장 등에서 활용되고 있습니다. 이 크기 등급에 대한 수요는 가정용 전기자동차의 보급 추세 및 소규모 비즈니스의 성장과 직접적으로 연동되어 있습니다. 한편, 330kVA를 초과하는 기종은 하이퍼스케일 데이터센터 건설, 전력회사의 피크 수요 대응 프로젝트, 광산 캠프 수요에 힘입어 연평균 성장률(CAGR) 6.4%로 성장할 것으로 전망됩니다. 커민즈의 신형 QSK50 및 QSK78 엔진을 탑재한 Centum 시리즈는 미션 크리티컬 워크로드를 위해 고밀도화와 신뢰성을 중시하며, 고출력화를 위한 노력을 구현하고 있습니다.

50-330kVA급 중용량 발전기는 호텔, 중층 오피스 빌딩, 렌탈 차량 등 다양한 분야에서 널리 사용되고 있습니다. 그러나 AI 칩 제조 공장이나 기가팩토리 등 산업 시설이 소수의 대규모 시설로 통합됨에 따라, 330kVA를 초과하는 발전기에 대한 수요가 증가하고 있습니다. 이에 대응하여 각 OEM 업체들은 수 메가와트 규모의 설치를 효율화하기 위해 모듈식 병렬 제어반과 온보드 진단 기능을 도입하고 있습니다. 한편, 50kVA 미만 부문에서는 중요 부하 회로를 대상으로 배터리와 결합된 옥상 태양광 발전 시스템과의 경쟁이 점차 치열해지고 있습니다. 그럼에도 불구하고, 이러한 소형 기기가 지닌 휴대성과 저렴한 초기 비용은 여전히 많은 구매자들을 매료시키고 있습니다. 그 결과, 가솔린 발전기 시장은 양극화되고 있습니다. 고출력 유닛은 에너지 집약형 산업 분야의 성장을 목표로 하는 반면, 소형 유닛은 기존의 광범위한 도입 기반을 유지하는 데 주력하고 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 46.4%를 차지했고, 가솔린 발전기 시장을 주도했으며, 2031년까지 연평균 성장률(CAGR) 5.7%라는 견실한 성장이 예상됩니다. 인도에서는 2024년 CPCB IV+ 규정에 따라 소형 엔진 배기가스 규제가 강화되었으나, 커민스 인디아는 여전히 2만 3,000대 이상의 규격 적합 기계를 출하하고 있으며, GOEM 딜러 네트워크를 127개 거점으로 확대하는 등 꾸준한 수요가 있음을 보여주고 있습니다. 중국의 인프라 확충 추진과 아세안(ASEAN) 국가들의 전기화 프로젝트에 힘입어, 휴대용 발전기 및 렌탈용 장비에 대한 수요는 꾸준히 증가하고 있습니다. 한편, 일본이나 한국에서는 엄격한 소음 규제 및 연비 기준을 충족하기 위해 인버터식 발전기가 선호되고 있습니다. 또한, 싱가포르와 인도네시아에서의 데이터센터 건설이 급속히 진행되면서 대용량 비상용 발전 설비의 수주도 증가하고 있습니다.

북미는 산불로 인한 정전과 격렬한 폭풍으로 인해 정전 시간이 길어지고 있어, 비상용 발전기 및 인버터식 발전기 구매 동향을 나타내는 지표로서의 위상을 유지하고 있습니다. 콜로라도주의 한 건설업체는 2024년 전력회사가 예방적 정전을 시작한 이후, 문의 건수가 연간 12건에서 주당 7건으로 급증했습니다. 제네락사는 증가하는 상업 및 산업용 수요에 대응하기 위해 2025년 위스콘신주 비버덤에 3,500만 달러를 투자해 35만 평방피트 규모의 시설을 개장했으며, 또한 서섹스의 공장을 2,000만 달러에 인수했습니다. 캐나다 외딴 지역의 광업 및 파이프라인 부문에 더해, 멕시코의 건설 붐이 이 지역의 성장을 견인하고 있습니다.

유럽의 가솔린 발전기 시장은 디젤 차량의 규제 준수 비용을 증가시키는 EU 스테이지 V 규제에 직면해 있으며, 그 결과 경부하 분야의 가솔린 모델이 간접적으로 혜택을 보고 있습니다. 독일과 북유럽 국가들에서는 건설 현장의 배기가스 감축을 위해 배터리-디젤 하이브리드 발전기가 도입되고 있지만, 오래된 건물이 많은 남유럽 국가들에서는 계절적인 폭염이 닥쳤을 때 여전히 기존의 휴대용 발전기에 의존하고 있습니다. 2026년 3월 아트라스코프코가 출시한 'QHS Integrated Hybrid'는 CO₂ 배출량을 최대 80%까지 감축한다고 밝히고 있으며, 이는 유럽의 각 OEM 업체들이 저탄소 솔루션으로 무게중심을 옮기고 있음을 보여줍니다. 한편, 사우디아라비아의 메가시티나 UAE의 데이터 허브와 같은 중동의 메가 프로젝트는 대기용 및 주전원용 발전 설비에 대한 수 메가와트 규모의 수주를 견인하고 있으며, 남아프리카공화국의 계획 정전은 사하라 이남 아프리카 전역의 주거용 및 C& I(상업 및 산업용) 시장 수요 증가를 뒷받침하고 있습니다. 라틴아메리카에서는 브라질의 건설 업계와 안데스 지역의 광업이 수요를 주도하고 있지만, 환율 변동으로 인해 수입이 주춤할 수도 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the gasoline genset market size is expected to increase from USD 2.55 billion in 2025 to USD 2.67 billion in 2026 and reach USD 3.26 billion by 2031, growing at a CAGR of 4.13% over 2026-2031.

This report is Segmented by Type (Portable, Standby, Inverter), Capacity (Below 50 KVA, 50 To 330 KVA, Above 330 KVA), Application (Standby, Peak Shaving, Prime/Continuous), End-User (Residential, Commercial, Industrial), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Gasoline Genset Market Trends and Insights

Aging Grid Infrastructure Causing Frequent Outages

U.S. utilities report that over 70% of transmission lines and transformers have exceeded their intended service life, and this aging fleet contributed to 431 automatic transmission outages during Hurricane Helene in 2024 . Customers in New York endured 162% more interruption hours in 2024 than in 2023, forcing many homeowners and small businesses to purchase standby gasoline sets for guaranteed resilience . Europe shows a similar pattern, with 50-year-old wooden distribution poles still in place across several national networks, pushing demand for backup power during scheduled maintenance windows. Although utilities are installing reclosers, sectionalizers, and advanced metering, grid upgrades occur over multi-year cycles, leaving a near-term window where gasoline genset market demand remains elevated. Manufacturers are capitalizing by promoting remote-monitoring packages that alert owners to outages and automate generator starts, ensuring seamless operation during grid failures.

Residential Backup-Power Demand from Extreme Weather Events

The U.S. Energy Information Administration recorded more than 10 outage hours per utility customer in 2024, the highest level in a decade, with 80% of those hours caused by major storms. Hurricanes Helene and Milton left 4.7 million customers without electricity, while wildfire-driven public-safety shutoffs in California expanded dramatically, encouraging households to install standby sets pre-emptively. NOAA forecasts an above-average Atlantic hurricane season in 2026, further intensifying homeowner appetite for robust backup systems . Briggs & Stratton's 26-kW PowerProtect generator offers 65.6 kVA of motor-starting capacity and a quick weekly self-test that reduces fuel use and noise, appealing to residents in quiet suburban areas. The gasoline genset market gains a tailwind as households seek turnkey solutions that ensure refrigeration, HVAC, and critical electronics remain operational during multiday blackouts.

Stricter Emission Norms for Small Spark-Ignition Engines

The U.S. EPA's Phase 3 rules impose HC+NOx limits as low as 8 g/kWh for non-handheld engines, while Europe's Stage V adds particulate-number counting and in-service conformity audits. Manufacturers answer with fuel injection, catalytic mufflers, and evaporative canisters, raising bill-of-materials costs and forcing design compromises on weight and enclosure size. India's CPCB IV+ regulation came into force in July 2024 and already covers engines up to 800 kW, obliging OEMs to certify both gasoline and diesel models and to offer retrofit aftertreatment for existing fleets. Compliance testing and paperwork stretch engineering budgets and lengthen product-launch cycles, marginally dampening gasoline genset market growth until learning curves and economies of scale bring costs back down.

Other drivers and restraints analyzed in the detailed report include:

- RV & Outdoor-Leisure Boom Boosting Portable Inverter Sales

- Urban Construction Surge in Emerging Economies

- Rising Uptake of Solar-Plus-Storage Home Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Portable units dominated the gasoline genset market size with a 54.2% revenue share in 2025, confirming their go-anywhere appeal for households, contractors, and outdoor enthusiasts. Inverter models, however, are forecast to climb at a 7.0% CAGR to 2031 because smart fuel injection and variable-speed operation slash noise and fuel burn. Honda's iGX400 and iGX430 demonstrate how electronic control, SAE J1939 connectivity, and choke-free starts attack customer pain points in seasonal-use scenarios. Standby sets benefit from rising grid outages, yet face silent competition from solar-plus-storage. Briggs & Stratton's 26-kW PowerProtect, certified for non-emergency cycles, bridges this gap by letting owners earn utility demand-response revenue. The gasoline genset market, therefore, tilts gradually toward inverters and advanced standby platforms that combine clean output with digital controls.

Traditional open-frame portables remain price leaders for light construction and do-it-yourself backup, especially in emerging markets. Nevertheless, country-level noise ordinances and stricter engine standards push buyers in premium segments toward quieter, cleaner inverter sets. OEMs are broadening their catalogs with parallel-ready 2-3 kW models that can be hand-carried yet linked for higher draws, providing a modular alternative to 5-7 kW open-frame designs. Retail channels highlight fuel-savings calculators and decibel comparisons to convert legacy-generator owners, supporting sustained inverter share gains inside the gasoline genset market.

Sub-50 kVA machines captured 73.5% gasoline genset market share in 2025, serving residential backup, kiosks, and light construction. Demand in this size class aligns directly with household outage trends and small-business growth. Conversely, units above 330 kVA are projected to grow at a 6.4% CAGR thanks to hyperscale data-center builds, utility peaking projects, and mining camps. Cummins' new QSK50- and QSK78-powered Centum Series sets exemplify the high-power push by emphasizing density and reliability for mission-critical workloads.

Middle-capacity gensets, ranging from 50 to 330 kVA, are consistently utilized in applications such as hotels, mid-rise office buildings, and rental fleets. However, as industrial operations consolidate into fewer, larger facilities, such as AI chip manufacturing plants and giga-factories, demand for gensets above 330 kVA is increasing. In response, original equipment manufacturers (OEMs) are introducing modular paralleling panels and on-board diagnostics to streamline multi-megawatt installations. At the same time, the sub-50 kVA segment is experiencing gradual competition from rooftop solar systems combined with batteries for essential-load circuits. Despite this, the portability and lower upfront costs of these smaller units continue to attract many buyers. Consequently, the gasoline genset market is diverging: high-horsepower units are targeting growth in energy-intensive industries, while smaller units focus on maintaining their extensive installed base.

Geography Analysis

Asia-Pacific led the gasoline genset market with 46.4% revenue in 2025 and is forecast at a brisk 5.7% CAGR to 2031. India tightened small-engine emissions with CPCB IV+ in 2024, yet Cummins India still shipped over 23,000 compliant units and expanded its GOEM dealer roster to 127 outlets, signaling strong underlying demand. China's infrastructure push and ASEAN electrification projects keep portable and rental fleets busy, while Japan and South Korea favor inverter units to meet stringent noise and fuel-efficiency criteria. Rapid data-center construction in Singapore and Indonesia also lifts orders for high-capacity standby sets.

North America remains the bellwether for standby and inverter purchases because wildfire-driven shutoffs and severe storms lengthen outage durations. One Colorado contractor saw inquiries soar from 12 per year to seven per week once utilities began preventive shutoffs in 2024. Generac opened a USD 35 million, 350,000-square-foot facility in Beaver Dam, Wisconsin, in 2025 and bought a Sussex plant for USD 20 million to meet climbing commercial-industrial demand. Canada's remote mining and pipeline sectors, plus Mexico's construction boom, round out regional growth.

Europe's gasoline genset market grapples with EU Stage V rules that inflate diesel compliance costs, indirectly benefiting gasoline models in light-duty niches. Germany and the Nordics embrace hybrid battery-diesel gensets to trim emissions on job sites, yet southern nations with older building stock still rely on conventional portables during seasonal heat waves. Atlas Copco's QHS Integrated Hybrid launch in March 2026 claims up to 80% CO2 savings, showing European OEMs' pivot to low-carbon solutions. Meanwhile, Middle East megaprojects like Saudi giga-cities and UAE data hubs drive multi-megawatt orders for standby and prime sets, while South Africa's rolling blackouts fuel residential and C&I uptake across sub-Saharan Africa. Latin America contributes via Brazilian construction and Andean mining, though currency volatility occasionally slows imports.

- Honda Motor Co., Ltd.

- Yamaha Motor Co., Ltd.

- Generac Holdings Inc.

- Briggs & Stratton Corporation

- Rehlko

- Cummins Inc.

- Caterpillar Inc.

- Champion Power Equipment

- Atlas Copco AB

- Hyundai Corporation

- Wacker Neuson SE

- Multiquip Inc.

- Westinghouse Electric Company LLC

- Denyo Co., Ltd.

- Perkins Engines Co. Ltd.

- Himoinsa S.L.

- Pramac S.p.A.

- Stanley Black & Decker, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging grid infrastructure causing frequent outages

- 4.2.2 Residential backup-power demand from extreme weather events

- 4.2.3 RV & outdoor-leisure boom boosting portable inverter sales

- 4.2.4 Urban construction surge in emerging economies

- 4.2.5 IoT-enabled remote monitoring improving OPEX economics

- 4.3 Market Restraints

- 4.3.1 Stricter emission norms for small spark-ignition engines

- 4.3.2 Rising uptake of solar-plus-storage home systems

- 4.3.3 Volatile copper & steel prices inflating production costs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Portable Gasoline Gensets

- 5.1.2 Standby Gasoline Gensets

- 5.1.3 Inverter Gasoline Gensets

- 5.2 By Capacity

- 5.2.1 Below 50 kVA

- 5.2.2 50 to 330 kVA

- 5.2.3 Above 330 kVA

- 5.3 By Application

- 5.3.1 Standby

- 5.3.2 Peak Shaving

- 5.3.3 Prime/Continuous

- 5.4 By End-user

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.4.3 Industrial

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 NORDIC Countries

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN Countries

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Honda Motor Co., Ltd.

- 6.4.2 Yamaha Motor Co., Ltd.

- 6.4.3 Generac Holdings Inc.

- 6.4.4 Briggs & Stratton Corporation

- 6.4.5 Rehlko

- 6.4.6 Cummins Inc.

- 6.4.7 Caterpillar Inc.

- 6.4.8 Champion Power Equipment

- 6.4.9 Atlas Copco AB

- 6.4.10 Hyundai Corporation

- 6.4.11 Wacker Neuson SE

- 6.4.12 Multiquip Inc.

- 6.4.13 Westinghouse Electric Company LLC

- 6.4.14 Denyo Co., Ltd.

- 6.4.15 Perkins Engines Co. Ltd.

- 6.4.16 Himoinsa S.L.

- 6.4.17 Pramac S.p.A.

- 6.4.18 Stanley Black & Decker, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment