|

시장보고서

상품코드

2062483

마이크로 배터리 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Micro Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

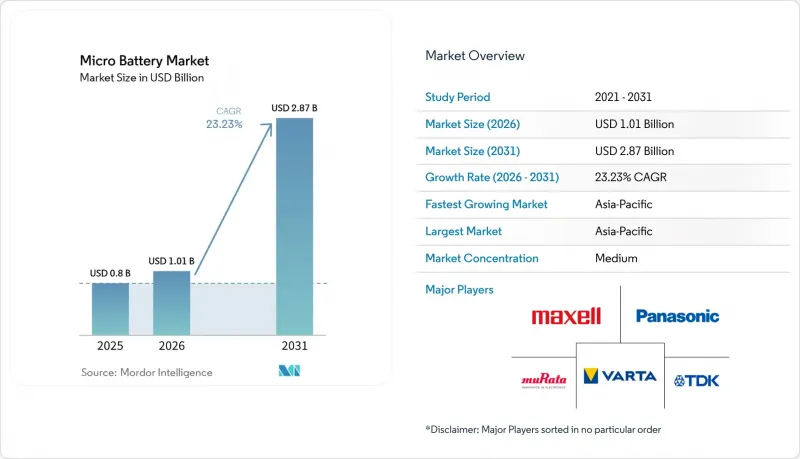

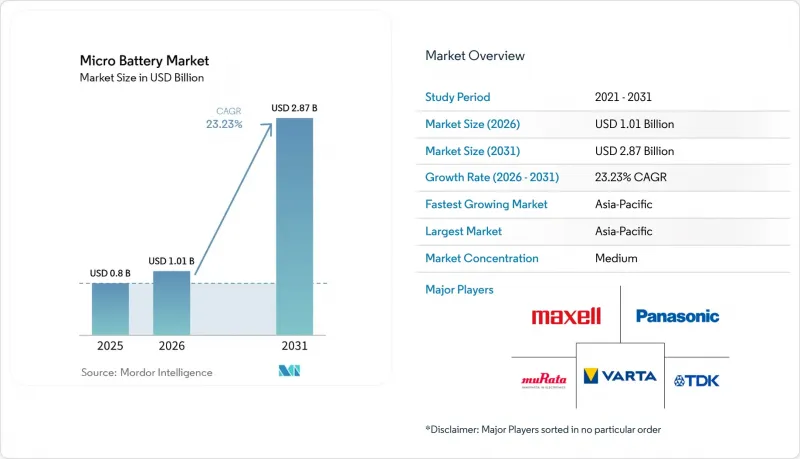

Mordor Intelligence에 의하면, 마이크로배 터리 시장 규모는 2025년 8억 달러로 평가되었습니다. 2026년 10억 1,000만 달러로 확대되어 2031년까지 28억 7,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR은 23.23%를 나타낼 전망입니다.

본 보고서는 유형별(박막, 고체, 프린트/플렉서블, 버튼형, 기타), 용도별(의료기기, 웨어러블, 스마트카드/RFID, 센서, 액세서리, 기타), 최종 사용자별(헬스케어, 소비자용 전자기기, 산업용, 자동차, 국방, 기타), 지역별(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 마이크로 배터리 시장 동향과 인사이트

웨어러블 기기의 보급

스마트 워치, 링형 기기, 히어러블(귀에 착용하는 기기)의 출하 대수는 마이크로 배터리 시장 수요를 지속적으로 끌어올리고 있습니다. 오픈 이어형 이어폰은 고밀도 셀과 적응형 전력 관리 기능을 통합함으로써, 사용 시간이 2025년의 5-6시간에서 2026년에는 8-12시간으로 연장되었습니다. 2024년에 발표된 Ensurge사의 650-750 Wh/L 고체 배터리 설계는 귀 내부에서 중요한 안전상의 이점을 제공하는 가연성 액체 전해질을 배제하고 있어, 이러한 히어러블 기기를 대상으로 하고 있습니다. 2025년에 25억 달러 규모 시장 성장이 예상되는 플렉서블 종이 배터리는 전력을 섬유 기판에 직접 내장함으로써, 무게와 부피를 늘리는 원인이 되는 경질 케이스를 없앴습니다. 전 세계적으로 오디오 기기용 IEC 62368-1 규격이 준수됨에 따라, 각 브랜드는 제조물 책임 위험을 줄일 수 있는 인증된 마이크로 배터리 공급업체에 대한 의존도를 높이고 있습니다.

이식형 의료용 전자기기의 성장

소형화된 심장박동기, 신경자극장치, 약물 전달 펌프는 교체 주기를 연장하고 수술 위험을 줄여주는 마이크로 배터리에 의존하고 있습니다. 2026년 2월에 시행될 FDA의 품질 관리 시스템 규정에 따라, 배터리 공급업체는 셀 단위의 상세한 추적성 시스템을 도입해야 할 의무가 부과됨에 따라, 중소규모 기업들은 규정 준수를 위해 외부에 위탁하거나 시장에서 철수할 수밖에 없는 상황에 처해 있습니다. Ilika사는 2026년 1월, Cirtec Medical사에 Stereax M300 고체 전지의 첫 본격적인 주문을 출하했으나, 기타 21개 기기 제조업체는 현재도 임상 검증 단계에 있습니다. 심실의 움직임을 이용해 에너지를 회수하는 연구용 프로토타입은 향후 배터리가 필요 없는 임플란트의 가능성을 시사하고 있지만, 장기적인 생체 적합성에 대한 연구는 현재도 진행 중입니다. 2025년 배터리 결함에 관한 경고문이 발표된 이후, 규제 당국의 감시가 강화되면서 ISO 13485 인증을 취득한 공급업체에 대한 수요가 증가하고 있습니다.

고체 마이크로 배터리의 높은 제조 비용

진공 증착, 특수 전구체 및 저처리량의 배치 공정을 통해 고체 전지의 비용은 리튬 이온 전지에 비해 3-5배 더 높습니다. ProLogium사의 덩케르크 공장은 2029년까지 4GWh의 생산과 kWh당 150달러 미만의 비용 목표를 세웠으나, 자본 부담이 막대합니다. 에너지 사용량을 47% 절감하는 건전극 라인은 유망하지만, 마이크로 배터리 규모에서의 실증은 아직 이루어지지 않았습니다. Elevated Materials사는 2025년에 100km가 넘는 리튬 금속 필름을 출하했으나, 2026년에는 생산량을 3배로 늘려야 하는 상황에서 박막 공급망의 병목 현상이 두드러지게 나타나고 있습니다. 비용이 낮아질 때까지는 의료, 국방 및 고급 웨어러블 기기 분야에 도입이 집중될 것입니다.

부문별 분석

2025년 기준으로 박막 전지는 마이크로 배터리 시장 점유율의 35.4%를 차지했으며, 그 기반은 오랜 인증 실적을 중시하는 의료용 임플란트 및 스마트카드에 있었습니다. 고체 전지 시장은 ProLogium사의 860 Wh/L 플랫폼과 Ilika사의 양산 확대에 힘입어 연평균 성장률(CAGR) 26.2%를 나타낼 전망입니다. 이러한 화학계는 1mm 미만의 초박형화를 추구하는 설계자들의 요구를 충족시키고, 가연성 액체 전해질을 배제하기 때문에 규제가 엄격한 의료기기 및 방위 기기에서 매우 매력적입니다. 인쇄형 및 플렉서블 배터리는 최대 용량보다는 초저비용과 형태적 유연성이 중시되는 일회용 센서 및 스마트 패키징 시장을 선점했습니다. 단추형 배터리는 기존 생산 라인에서 개당 몇 센트라는 가격으로 검증된 신뢰성을 제공하기 때문에 자동차 키풋이나 손목시계에서 여전히 필수적인 부품입니다.

제조 거점의 상황은 생산량과 이익률의 상이한 추세를 반영하고 있습니다. ProLogium의 타오위안 공장은 2025년에 60만 개 이상의 배터리를 출하하며, 롤-투-롤 방식을 통한 박막 제조의 확장성을 입증했습니다. 한편, Zinergy와 Flint는 일회용 용도를 위해 각각 수천 제곱미터 규모의 종이 배터리 생산 공간을 증설했습니다. 마이크로 배터리와 에너지 하베스터를 결합한 하이브리드 화학 기술에 대한 연구 자금이 증가하고 있으며, 이에 따라 마이크로 배터리 시장은 폼 팩터를 확대하지 않으면서도 도입 수명을 연장하는 멀티 파워 아키텍처로 나아가고 있습니다.

지역별 분석

아시아태평양은 2025년에 매출 점유율의 41.8%를 차지했습니다. 이는 배터리 제조 분야에서 중국의 우위와, 고체 배터리 연구 개발에 대한 일본의 6억 6,000만 달러 규모의 보조금에 힘입은 결과입니다. CATL의 전구체 조달에 따른 규모의 경제는 지역 전체 공급망의 비용 구조를 낮추고 있습니다. 한국 제조업체들은 수직 통합형 중국 경쟁사들에게 시장 점유율을 빼앗겼지만, 수익성을 회복하기 위해 전고체 배터리 생산 라인에 대한 재투자를 추진하고 있습니다. 2029년 가동을 예정하고 있는 ProLogium사의 4GWh 규모 덩케르크 프로젝트는 유럽의 OEM 제조업체들에게 지정학적 리스크를 회피할 수 있는 현지 조달이라는 선택지를 제공합니다.

북미에서는 중국산 부품 사용을 금지하는 방위 규제에 따라 공급망 재구축이 진행되고 있습니다. 미 육군의 표준화 전술 범용 배터리(STUB) 규격에 따라 국내 사전 인증이 의무화되었으며, 적합 제조업체로 제한됨에 따라 공급업체 선택의 폭이 좁아지고 있습니다. NEO Battery Materials의 한국 지사는 섹션 4872 준수를 요구하는 미국의 드론 프로그램에 제품을 공급하고 있습니다.

유럽에서는 EU 방위 기금의 보조금을, 민간용 웨어러블 기기와 군용 시스템 모두에 전력을 공급하는 이중 용도 마이크로 배터리 개발에 사용하고 있습니다. 2026년부터 2027년에 걸쳐 자금을 지원받는 HARVEST 프로젝트는 NATO의 상호운용성 요건을 충족하는 동시에 EU 배터리 규정의 추적성 규정도 충족하는 프로젝트의 한 예입니다. 남미 및 중동 및 아프리카(MEA) 지역은 여전히 수입에 의존하고 있으며, 환율 변동은 물론 현지 생산 능력이 제한적이라는 점 때문에 단기적인 보급이 저해되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the micro battery market size is expected to increase from USD 0.8 billion in 2025 to USD 1.01 billion in 2026 and reach USD 2.87 billion by 2031, growing at a CAGR of 23.23% over 2026-2031.

This report is Segmented by Type (Thin-Film, Solid-State, Printed/Flexible, Button-Cell, Others), Application (Medical Devices, Wearables, Smart Cards/RFID, Sensors, Accessories, Others), End-User (Healthcare, Consumer-Electronics, Industrial, Automotive, Defense, Others), and Geography (North America, Europe, Asia-Pacific, South America, MEA). The Market Forecasts are Provided in Terms of Value (USD).

Global Micro Battery Market Trends and Insights

Proliferation of Wearable Devices

Shipments of smartwatches, rings, and hearables continue to lift micro battery market demand. Open-ear earbuds moved runtime from 5-6 hours in 2025 to 8-12 hours in 2026 after integrating higher-density cells and adaptive power management. Ensurge's 650-750 Wh/L solid-state design, released in 2024, targets these hearables because it removes flammable liquid electrolytes, a critical safety benefit inside the ear canal. Flexible paper batteries worth USD 2.5 billion in 2025 are embedding power directly into textile substrates, eliminating rigid housings that add weight and bulk. Global compliance with IEC 62368-1 for audio devices is steering brands toward certified micro-battery suppliers that can mitigate product-liability exposure.

Growth in Implantable Medical Electronics

Miniaturized pacemakers, neurostimulators, and drug-delivery pumps rely on micro batteries that extend replacement intervals and lower surgical risk. The FDA's February 2026 Quality Management System Regulation forces battery vendors to implement granular cell-level genealogy, pushing smaller firms to outsource compliance or exit the market. Ilika shipped its first revenue order of Stereax M300 solid-state cells to Cirtec Medical in January 2026, while 21 additional device makers remain in clinical validation. Research prototypes harvesting ventricular motion hint at future battery-free implants, yet long-term biocompatibility studies are still underway. Heightened regulatory scrutiny since a 2025 warning letter on battery failures is amplifying demand for suppliers with ISO 13485 accreditation .

High Manufacturing Cost of Solid-State Micro Batteries

Vacuum deposition, specialty precursors, and low-throughput batch processing leave solid-state cells at a 3-5 X cost premium over lithium-ion. ProLogium's Dunkirk site aims for 4 GWh by 2029 and a sub-USD 150 kWh cost target, but the capital burden is significant. Dry-electrode lines that cut energy use 47% are promising yet unproven at the micro-battery scale. Elevated Materials shipped over 100 km of lithium metal film in 2025 and must triple output in 2026, underscoring thin-film supply-chain bottlenecks . Until costs fall, adoption concentrates in medical, defense, and premium wearables.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of IoT Edge-Sensor Networks

- Rising Demand for Compact Hearable Power Sources

- Limited Energy Density vs. Conventional Coin Cells

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Thin-film batteries held a 35.4% micro battery market share in 2025, anchored in medical implants and smart cards that value long qualification histories. Solid-state variants will grow at a 26.2% CAGR, powered by ProLogium's 860 Wh/L platform and Ilika's commercial ramp. These chemistries satisfy designer demands for sub-millimeter profiles and eliminate flammable liquid electrolytes, compelling in regulated healthcare and defense devices. Printed and flexible batteries captured disposable sensors and smart packaging, where ultralow cost and form flexibility matter more than maximum capacity. Button-cell formats remain essential in automotive key fobs and watches because incumbent production lines deliver proven reliability at cents-per-unit prices.

Manufacturing footprints reflect divergent volume and margin profiles. ProLogium's Taoyuan plant shipped over 600,000 cells in 2025, demonstrating roll-to-roll thin-film scalability, while Zinergy and Flint each added thousands of square meters of paper-battery floor space for single-use applications. Hybrid chemistries coupling micro batteries with energy harvesters are gaining research funding, positioning the micro battery market for multipower architectures that extend deployment lifetimes without enlarging form factors.

Geography Analysis

Asia-Pacific held 41.8% revenue share in 2025, supported by China's supremacy in battery manufacturing and Japan's USD 660 million subsidy for solid-state R&D. CATL's scale in precursor procurement lowers cost structures throughout the regional supply chain. Korean producers lost share to vertically integrated Chinese rivals, yet are reinvesting in all-solid-state lines to reclaim margin. ProLogium's 4 GWh Dunkirk project, scheduled for 2029, offers European OEMs a localized supply alternative that sidesteps geopolitical risk.

North America is reshaping supply networks under defense regulations that block Chinese content. The U.S. Army's standardized tactical universal battery (STUB) sizes force domestic pre-qualification, narrowing the vendor pool to compliant manufacturers. NEO Battery Materials' South Korean site serves U.S. drone programs seeking Section 4872 conformity.

Europe is channeling EU Defence Fund grants toward dual-use micro batteries that power both civilian wearables and soldier systems. HARVEST, funded in 2026-2027, exemplifies projects aligning with NATO interoperability needs while meeting EU battery regulation traceability rules. South America and MEA remain import-dependent, and currency volatility plus limited local manufacturing capacity restrain near-term uptake.

- Murata Manufacturing Co., Ltd.

- Maxell Holdings Ltd.

- Panasonic Corporation

- TDK Corporation

- VARTA AG

- Renata SA

- Cymbet Corporation

- Samsung SDI Co., Ltd.

- STMicroelectronics

- NEC Energy Solutions

- Ultralife Corporation

- EnerSys

- BrightVolt Inc.

- Blue Spark Technologies

- ProLogium Technology

- Ilika plc

- SolidEnergy Systems

- EVE Energy Co., Ltd.

- Imprint Energy

- BYD Company Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of wearable devices

- 4.2.2 Growth in implantable medical electronics

- 4.2.3 Expansion of IoT edge - sensor networks

- 4.2.4 Rising demand for compact hearable power sources

- 4.2.5 Self-powered printed-electronics ecosystem emerging

- 4.2.6 Defense adoption of smart-dust sensor nodes

- 4.3 Market Restraints

- 4.3.1 High manufacturing cost of solid-state micro batteries

- 4.3.2 Limited energy density v s. conventional coin cells

- 4.3.3 Supply-chain constraints for thin-film deposition materials

- 4.3.4 Lack of standardized micro-battery test protocols

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Thin-Film Batteries

- 5.1.2 Solid-State Micro Batteries

- 5.1.3 Printed/Flexible Batteries

- 5.1.4 Button-Cell Micro Batteries

- 5.1.5 Others

- 5.2 By Application

- 5.2.1 Medical Devices

- 5.2.2 Wearable Electronics

- 5.2.3 Smart Cards and RFID

- 5.2.4 Wireless Sensor Nodes

- 5.2.5 Consumer-Electronics Accessories

- 5.2.6 Others

- 5.3 By End-user

- 5.3.1 Healthcare

- 5.3.2 Consumer-Electronics

- 5.3.3 Industrial and Automation

- 5.3.4 Automotive and Mobility

- 5.3.5 Defense and Aerospace

- 5.3.6 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 NORDIC Countries

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 ASEAN Countries

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Murata Manufacturing Co., Ltd.

- 6.4.2 Maxell Holdings Ltd.

- 6.4.3 Panasonic Corporation

- 6.4.4 TDK Corporation

- 6.4.5 VARTA AG

- 6.4.6 Renata SA

- 6.4.7 Cymbet Corporation

- 6.4.8 Samsung SDI Co., Ltd.

- 6.4.9 STMicroelectronics

- 6.4.10 NEC Energy Solutions

- 6.4.11 Ultralife Corporation

- 6.4.12 EnerSys

- 6.4.13 BrightVolt Inc.

- 6.4.14 Blue Spark Technologies

- 6.4.15 ProLogium Technology

- 6.4.16 Ilika plc

- 6.4.17 SolidEnergy Systems

- 6.4.18 EVE Energy Co., Ltd.

- 6.4.19 Imprint Energy

- 6.4.20 BYD Company Limited

7 Market Opportunities & Future Outlook

- 7.1 Emerging Technologies & Innovations

- 7.2 Expansion into Untapped Applications

- 7.3 Government Incentives & Funding

- 7.4 Long-term Growth Prospects