|

시장보고서

상품코드

2062484

석유 및 가스 인프라 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Oil and Gas Infrastructure - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

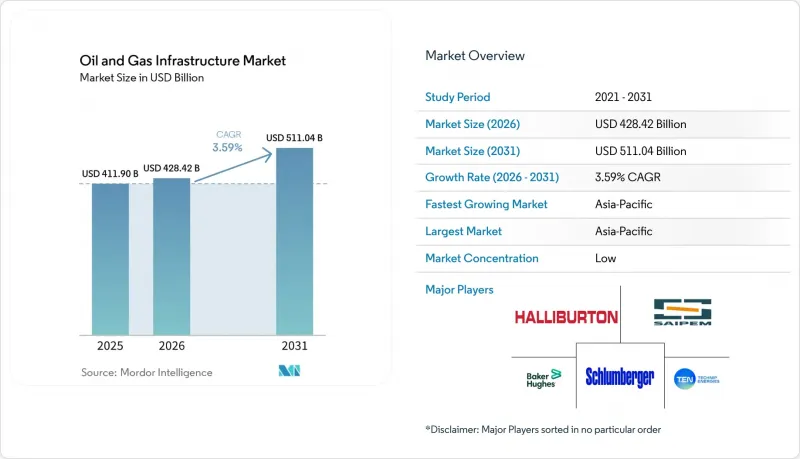

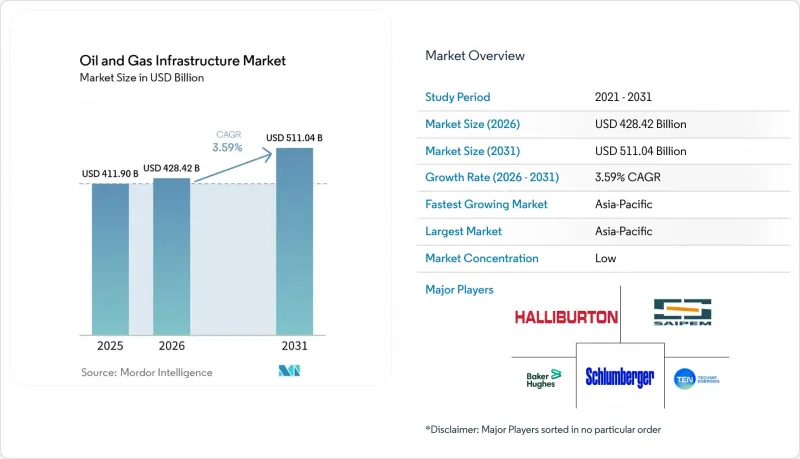

Mordor Intelligence에 의하면, 석유 및 가스 인프라 시장 규모는 2025년에 4,119억 달러로 평가되었습니다. 2026년에는 4,284억 2,000만 달러에 이르고, 2031년까지 5,110억 4,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR은 3.59%를 나타낼 전망입니다.

본 보고서는 유형별(파이프라인, 저장 시설, 처리·정제 설비, 시추 플랫폼, LNG 수출입 터미널, 압축기 및 펌프 스테이션), 용도별(탐사·생산, 수송, 기타), 지역별(북미, 유럽, 아시아·태평양, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 석유 및 가스 인프라 시장 동향과 인사이트

노후된 파이프라인의 교체 주기

북미의 사업자들은 2025년에 하루 63억 입방피트의 새로운 가스 파이프라인 용량을 추가했으나, 그 건설의 대부분은 1960년대와 1970년대에 설치된 부식된 구간을 단순히 교체한 것에 불과했습니다. 같은 해, 워싱턴은 부식 방지 및 강관 개량을 위해 19개 주에 1억 9,600만 달러의 연방 보조금을 지급했습니다. 대서양을 사이에 둔 유럽에서는 고압 파이프라인망의 약 40%가 1980년 이전에 건설된 것으로, 규제 당국은 ISO 16708에 따라 검사 주기를 단축할 것을 촉구하고 있습니다. 이러한 움직임이 고품질 강재 및 자동 용접 장비에 대한 단기적인 수요를 견인하고 있습니다. 가즈프롬은 2028년까지 8,000킬로미터의 간선 파이프라인을 폐쇄하고, 그 자금을 새로운 북극해 노선에 투입할 계획입니다. 이는 변화하는 무역 양상에 적합한 프로젝트를 우선시하고, 노후화된 자산에 대한 투자가 뒷전으로 밀려나고 있는 실태를 보여줍니다. 철강 가격의 급등으로 인해 발주가 지연되는 경우도 있지만, 전반적으로 볼 때 이러한 갱신 흐름은 파이프 제조업체와 부식 방지 업체에 지속적인 호재가 되고 있습니다.

세계 LNG 무역의 확대

LNG 무역량은 2025년에 4억 1,200만 톤에 달하고, 전년 대비 4.8% 증가했습니다. 이는 러시아산 파이프라인 공급량 1,550억 입방미터의 감소를 보충해야 하는 상황에 직면한 유럽과, 석탄에서 가스로의 전환을 지속하고 있는 아시아의 동향을 반영한 것입니다. 미국의 3개 수출 터미널인 칼카슈 패스 2, 골든 패스, 프락민스는 2025년에 최종 승인을 받아 2020년대 말까지 총 연간 3,960만 톤의 정격 처리 능력을 추가하게 될 것입니다. 유럽에서는 2022년부터 2025년에 걸쳐 850억 입방미터 규모의 추가 재기화 설비가 가동을 시작했습니다. 그중 3분의 1은 부유식 저장·재기화 설비(FSRU)를 통해 실현되어, 신속한 구축과 초기 비용 절감이 가능해졌습니다. 카타르는 2025년 시점에서 세계 수출 점유율 20%를 유지했으나, 2026년 3월 호르무즈 해협 봉쇄 사태 당시 특정 화물에 대해 불가항력을 선언할 수밖에 없었으며, 이로 인해 해당 해협의 좁은 항로에서 발생하는 집중 위험이 드러났습니다. 인프라 확충은 시스템의 복원력을 높이는 한편, 재생에너지의 보급으로 인해 장기적인 가스 수요가 억제될 경우, 좌초 자산(스트랜드드 어셋)에 대한 우려도 증폭시킬 것입니다.

원유 가격의 극심한 변동

2026년 초, 전 세계적으로 하루 140만-250만 배럴공급 과잉이 지속되는 가운데, 브렌트유 가격은 배럴당 평균 62-65달러를 기록했습니다. 2026년 3월 호르무즈 해협 위기 사태로 인해 가격은 일시적으로 78달러까지 치솟았으나, 전략 비축유 방출과 희망봉 주변으로의 항로 변경으로 인해 10일 이내에 가격이 정상화되었습니다. 사업자들은 일반적으로 장기 주기의 플랫폼이나 국경을 넘는 파이프라인 건설을 승인하기 위해 70달러 이상의 가격 수준이 필요합니다. 따라서 70달러 미만의 가격이 장기화되면, 최종 투자 결정이 미뤄지게 됩니다. 미국의 셰일 시추 기업들은 2026년 초 예산을 8% 삭감하고, 생산량 확대보다 주주 환원을 우선시함에 따라 관련 수거 시스템의 확장이 중단되었습니다. 라틴아메리카의 국영 기업들도 비슷한 압박에 직면했습니다. 페트로브라스는 2025년 예정이던 부유식 생산선 2척의 도입을 연기했으며, YPF는 바카 무에르타 지역을 대상으로 한 25억 달러 규모의 간선 파이프라인 확장 계획을 보류했습니다.

부문별 분석

자산군 중에서는 LNG 터미널의 확장이 가장 빠르게 진행되고 있으며, 2031년까지 연평균 7.0%의 성장률을 기록하고 있습니다. 다만, 2025년 시점에서도 파이프라인은 석유 및 가스 인프라 시장 점유율의 42.8%를 차지하고 있었습니다. 2022년부터 2025년 사이에 유럽에서만 850억 입방미터의 재기화 용량이 증설되었는데, 이는 1년 이내에 계류할 수 있는 부유식 저장·재기화 설비(FSRU)에 크게 의존한 결과입니다. 브뤼셀이 매년 11월 1일 기준으로 90%의 재고 목표를 의무화하고 있기 때문에 저장 인프라도 마찬가지로 증가하고 있으며, 이는 동굴 저장 시설로의 전환과 새로운 소금 돔 침출을 촉진하고 있습니다. 정제·가공 시설의 동향은 제각각입니다. 2025년에는 전 세계 명목 생산 능력이 하루 1억 200만 배럴에 달했으나, 전기차 보급률 상승에 따라 OECD 국가들의 가동률은 82% 전후로 유지되고 있어, 성숙한 시장에서 합리화의 가능성이 있음을 시사하고 있습니다.

한편, 시추 플랫폼과 해저 시스템은 심해 개발의 부활로 인해 혜택을 보고 있습니다. 페트로브라스는 2025년에 부유식 생산·저장·하역선(FPSO) 4척을 발주했으며, 그 총액은 140억 달러에 달했습니다. 각 선박의 처리 능력은 하루 18만 배럴이 될 예정입니다. 압축기 스테이션에서는 전기화 개보수 공사가 진행되고 있습니다. 세노바스사는 2025년, 포스터 크릭에 총 16메가와트 규모의 전기식 발전 설비 25기를 설치하여 연료 가스 소비량을 18% 줄였습니다. 테크닙 에너지는 2026년, 카타르의 노스 필드 웨스트 LNG 확장 프로젝트에서 12억 달러 규모의 EPC 계약을 수주했습니다. 이 프로젝트에서는 모듈식 플랜트를 채택하여, 기존의 현장 조립형 메가 프로젝트에 비해 현장 설치 기간을 18개월 단축했습니다. 따라서 LNG 터미널과 관련된 석유 및 가스 인프라 시장 규모는 향후 10년 동안 신규 장거리 파이프라인 시장 규모를 넘어설 것으로 예상되며, 이는 밸류체인 전반에 걸친 설비 투자 배분 구조를 재편하게 될 것입니다.

지역별 분석

북미는 2025년 지출의 34.7%를 차지했습니다. 이는 에너지 이전(Energy Transfer)을 통한 50억-55억 달러 규모의 중류 부문 설비 투자에 더해, 2030년까지 미국을 세계 최대의 LNG 수출국으로서의 지위를 공고히 할 3개의 주요 LNG 수출 터미널 건설 승인이 주도한 결과입니다. 캐나다의 TC 에너지(TC Energy)는 2025년에 60억 달러 상당의 자산을 가동하고, 36억 3,000만 달러 규모의 프로젝트를 승인하는 한편, 태평양 연안의 LNG 캐나다에 공급하기 위한 코스트 가스링크(Coast GasLink)를 완공했습니다. 멕시코 남동부의 산업 지역에서는 파이프라인의 수송 능력이 수요를 따라가지 못하고 있어, 여전히 고가의 현물 LNG 화물에 대한 의존이 지속되고 있으며, 국경을 넘어선 확장을 위한 미개척 기회가 부각되고 있습니다.

아시아태평양은 인도의 수천억 달러 규모의 인프라 구축 계획과 인도네시아가 탄클로 및 마코 등의 해양 허브를 승인한 데 힘입어, 2031년까지 연평균 성장률(CAGR) 6.3%를 기록하며 가장 빠르게 성장하는 지역이 될 전망입니다. 말레이시아의 BIGST 클러스터는 2025년에 최종 투자 결정(FID)에 도달했으며, 2029년에 첫 가스 공급이 시작될 것으로 전망됩니다. 또한, 페트로나스의 로즈마리-마조람 프로젝트는 하루 8억 입방피트공급을 목표로 하고 있습니다. 일본과 한국에서 LNG 비축 의무가 강화됨(90일분)에 따라 지하 저장 시설에 대한 임대 수요가 더욱 증가하고 있으며, 수입 터미널의 EPC 수주 잔고는 견조한 추세를 보이고 있습니다.

유럽에서는 러시아산 파이프라인 공급량 1,550억 입방미터를 단계적으로 폐지하는 가운데, 재기화 터미널 및 저장 시설 확장에 계속해서 자본이 투입되고 있습니다. 2025년 10월 1일 재고율은 83%에 달했으며, 러시아산 공급량이 감소했음에도 불구하고 EU의 11월 목표인 90%까지 한 달밖에 남지 않은 상황에서 한파가 닥쳤을 때는 인출율이 억제되었습니다. GASCADE의 수소 대응 파이프라인과 Fluxys의 20억 유로 규모 개보수 계획 덕분에, 이 지역은 혼합 가스 수송 기술의 최전선에 서 있습니다. 남미의 설비 투자는 브라질에 집중되어 있으며, 페트로브라스는 2025년에 12억 달러 규모의 해저 공사를 발주하고 부유식 생산선의 수주를 확대했지만, 아르헨티나의 바카 무에르타는 여전히 파이프라인 병목 현상으로 어려움을 겪었습니다. 중동 및 아프리카는 막대한 저비용 매장량과 지정학적 위험을 동시에 안고 있습니다. 카타르는 2026년 3월 발생한 운송 차질에도 불구하고 2025년 세계 LNG 수출 점유율 20%를 유지했습니다. UAE는 푸자이라 저장 시설의 용량을 4,200만 배럴 증설했으며, 모잠비크의 코랄 노르테는 육상 메가 프로젝트 없이도 부유식 LNG가 심해 유전 개발을 가능하게 한다는 점을 입증하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the oil and gas infrastructure market size was USD 411.90 billion in 2025 and is expected to reach USD 428.42 billion in 2026 and reach USD 511.04 billion by 2031, growing at a CAGR of 3.59% over 2026-2031.

This report is Segmented by Type (Pipelines, Storage Facilities, Processing and Refining Units, Drilling Platforms, LNG Import/Export Terminals, Compressor and Pumping Stations), Application (Exploration and Production, Transportation, and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Oil and Gas Infrastructure Market Trends and Insights

Ageing Pipeline Replacement Cycle

North American operators added 6.3 billion cubic feet per day of new gas-line capacity in 2025, yet most construction simply swapped out corroded segments installed in the 1960s and 1970s . Washington disbursed USD 196 million of federal grants to 19 states for corrosion control and steel-line upgrades that same year . Across the Atlantic, about 40% of Europe's high-pressure grid predates 1980, encouraging regulators to tighten inspection intervals under ISO 16708, a move that is driving short-cycle demand for high-grade steel and automated welding equipment. Gazprom intends to retire 8,000 kilometers of trunk lines by 2028 and redirect funds toward newer Arctic routes, illustrating how aging assets are being de-prioritized in favor of projects that match shifting trade patterns. Collectively, the replacement wave is a durable catalyst for pipe mills and corrosion-protection vendors even though steel-price spikes occasionally delay orders.

Rising Global LNG Trade

LNG trade climbed to 412 million tons in 2025, a 4.8% year-over-year rise that reflected Europe's need to offset the loss of 155 billion cubic meters of Russian pipeline volumes and Asia's ongoing coal-to-gas switch . Three U.S. export terminals, Calcasieu Pass 2, Golden Pass, and Plaquemines, gained final approval in 2025 and will collectively add 39.6 million tons per annum of nameplate capacity by decade-end. Europe commissioned an additional 85 billion cubic meters of regasification space between 2022 and 2025, one-third of which was realized via floating storage and regasification units, enabling rapid deployment and lowering upfront costs . Qatar retained a 20% global export share in 2025 but was forced to declare force majeure on specific cargoes during the March 2026 Strait of Hormuz disruption, exposing concentration risk in the Strait's narrow shipping lane. Although the build-out strengthens system resilience, it also amplifies stranded-asset concerns should renewable penetration curb long-term gas demand.

Extreme Oil-Price Volatility

Brent averaged USD 62 to USD 65 per barrel in early 2026 amid a 1.4 million- to 2.5 million-barrel-per-day global surplus. The March 2026 Strait of Hormuz scare briefly lifted prices to USD 78, but values normalized within ten days following strategic-reserve releases and route diversions around the Cape of Good Hope. Operators typically need a USD 70-plus threshold to green-light long-cycle platforms and cross-border pipelines; therefore, prolonged sub-USD 70 pricing defers final investment decisions. U.S. shale drillers cut budgets by 8% in early 2026, prioritizing shareholder returns over volume growth, which then suspends related gathering-system expansions. Latin American national companies felt similar pressure: Petrobras postponed two floating production vessels in 2025, and YPF deferred a USD 2.5 billion trunk-line expansion serving Vaca Muerta.

Other drivers and restraints analyzed in the detailed report include:

- Deep- & Ultra-Deep-Water CAPEX Upswing

- National Energy-Security Programs

- Net-Zero & ESG Capital-Allocation Shifts

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

LNG terminals are expanding the fastest among asset classes, clocking a 7.0% annual growth rate through 2031, even though pipelines still held 42.8% of the oil and gas infrastructure market share in 2025. Europe alone added 85 billion cubic meters of regasification capacity between 2022 and 2025, leaning heavily on floating storage and regasification units that can be moored in under a year. Storage infrastructure is rising in tandem because Brussels mandates a 90% inventory target each November 1, encouraging cavern conversions and new salt-dome leaching. Refining and processing units face mixed fortunes: global nameplate capacity touched 102 million barrels per day in 2025, but OECD utilization hovered near 82% amid rising electric-vehicle penetration, signaling potential rationalization in mature markets.

Drilling platforms and subsea systems, however, are benefiting from a deep-water renaissance. Petrobras placed orders for four floating production, storage, and offloading vessels in 2025, cumulatively worth USD 14 billion, each slated for 180,000-barrel-per-day throughput. Compressor stations are undergoing electrification retrofits; Cenovus installed 25 electric units totaling 16 megawatts at Foster Creek in 2025, lowering fuel-gas burn by 18%. Technip Energies captured a USD 1.2 billion EPC contract for Qatar's North Field West LNG expansion in 2026, a project embracing modular trains that cut field-erection times by 18 months compared with stick-built megaprojects. The oil & gas infrastructure market size for LNG terminals is therefore poised to surpass that of new long-haul pipelines in the next decade, reshaping capex allocation across the value chain.

Geography Analysis

North America captured 34.7% of 2025 spending, driven by USD 5 billion to USD 5.5 billion of midstream capex from Energy Transfer and the sanctioning of three major LNG export terminals that will consolidate the United States' position as the world's largest LNG shipper by 2030. Canada's TC Energy commissioned USD 6 billion of assets in 2025 and green-lit another USD 3.63 billion, while completing Coastal GasLink to feed LNG Canada on the Pacific Coast. Mexico's industrial southeast still relies on expensive spot LNG cargoes because pipeline capacity lags demand, underlining an untapped opportunity for cross-border expansions.

Asia-Pacific is the fastest-growing zone at a 6.3% CAGR to 2031, propelled by India's multi-hundred-billion-dollar infrastructure drive and Indonesia's approval of offshore hubs such as Tangkulo and Mako. Malaysia's BIGST cluster reached final investment decision in 2025, with first gas expected in 2029, and Petronas' Rosmari-Marjoram project aims to deliver 800 million cubic feet per day. Japan and South Korea's stricter 90-day LNG reserves mandate is spurring additional cavern leasing, keeping import-terminal EPC order books healthy.

Europe continues to funnel capital into regasification terminals and storage expansions as it phases out 155 billion cubic meters of Russian pipeline supply. Inventory reached 83% by October 1, 2025, only one month shy of the bloc's 90% November target despite lower Russian volumes, yet draw-down rates remain constrained during cold snaps. GASCADE's hydrogen-ready line and Fluxys' EUR 2 billion retrofit plan place the region at the forefront of mixed-gas transmission technology. South America's capex is concentrated in Brazil, where Petrobras awarded USD 1.2 billion of subsea work in 2025 and is ramping up floating production vessel orders, though Argentina's Vaca Muerta remains hampered by pipeline bottlenecks. The Middle East and Africa combine vast low-cost reserves with geopolitical risk: Qatar maintained a 20% share of global LNG exports in 2025 despite the March 2026 shipping disruption. The UAE boosted Fujairah storage by 42 million barrels, and Mozambique's Coral Norte is proving that floating LNG can unlock deep-water fields without onshore megaprojects.

- Schlumberger

- Halliburton

- Baker Hughes

- Technip Energies

- Saipem

- Wood PLC

- Fluor Corporation

- Worley

- Petrofac

- National Oilwell Varco

- McDermott International

- CPECC

- KBR Inc.

- Bechtel Corporation

- Subsea 7

- Aker Solutions

- JGC Corporation

- Larsen & Toubro

- Samsung Engineering

- TC Energy

- Kinder Morgan

- Enbridge

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ageing Pipeline Replacement Cycle

- 4.2.2 Rising Global LNG Trade

- 4.2.3 Deep- & Ultra-Deep-water CAPEX Upswing

- 4.2.4 National Energy-Security Programs

- 4.2.5 Pipeline Hydrogen-Blending Retrofits

- 4.2.6 Digital-Twin-based Predictive O&M

- 4.3 Market Restraints

- 4.3.1 Extreme Oil-Price Volatility

- 4.3.2 Net-Zero & ESG Capital-Allocation Shifts

- 4.3.3 Modular Floating-LNG Competition

- 4.3.4 Cyber-security Driven Project Delays

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Pipelines

- 5.1.2 Storage Facilities

- 5.1.3 Processing and Refining Units

- 5.1.4 Drilling Platforms

- 5.1.5 LNG Import/Export Terminals

- 5.1.6 Compressor and Pumping Stations

- 5.2 By Application

- 5.2.1 Exploration and Production

- 5.2.2 Transportation

- 5.2.3 Processing and Refining

- 5.2.4 Storage and Distribution

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 NORDIC Countries

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 ASEAN Countries

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Egypt

- 5.3.5.5 Rest of Middle East and Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Schlumberger

- 6.4.2 Halliburton

- 6.4.3 Baker Hughes

- 6.4.4 Technip Energies

- 6.4.5 Saipem

- 6.4.6 Wood PLC

- 6.4.7 Fluor Corporation

- 6.4.8 Worley

- 6.4.9 Petrofac

- 6.4.10 National Oilwell Varco

- 6.4.11 McDermott International

- 6.4.12 CPECC

- 6.4.13 KBR Inc.

- 6.4.14 Bechtel Corporation

- 6.4.15 Subsea 7

- 6.4.16 Aker Solutions

- 6.4.17 JGC Corporation

- 6.4.18 Larsen & Toubro

- 6.4.19 Samsung Engineering

- 6.4.20 TC Energy

- 6.4.21 Kinder Morgan

- 6.4.22 Enbridge

7 Market Opportunities & Future Outlook

- 7.1 Emerging Markets & Investment Hotspots

- 7.2 Green Infrastructure & Sustainability Trends

- 7.3 Digital Transformation & Smart Infrastructure

- 7.4 Public Private Partnerships & Policy Support