|

시장보고서

상품코드

2063233

기상 모니터링 솔루션 및 서비스 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Weather Monitoring Solutions And Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

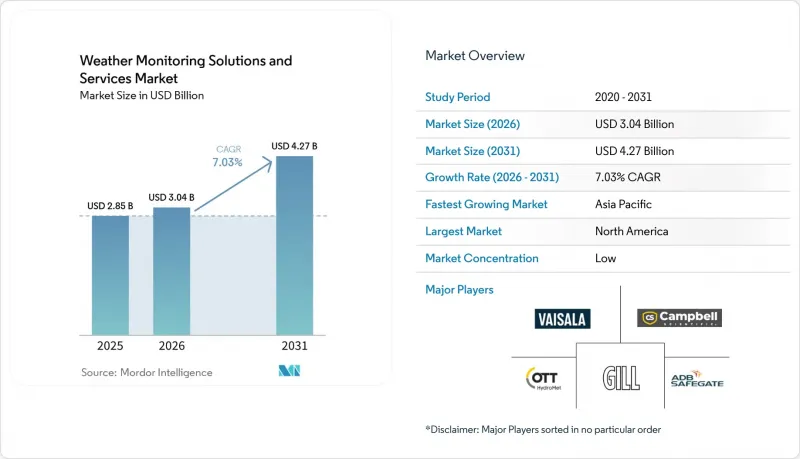

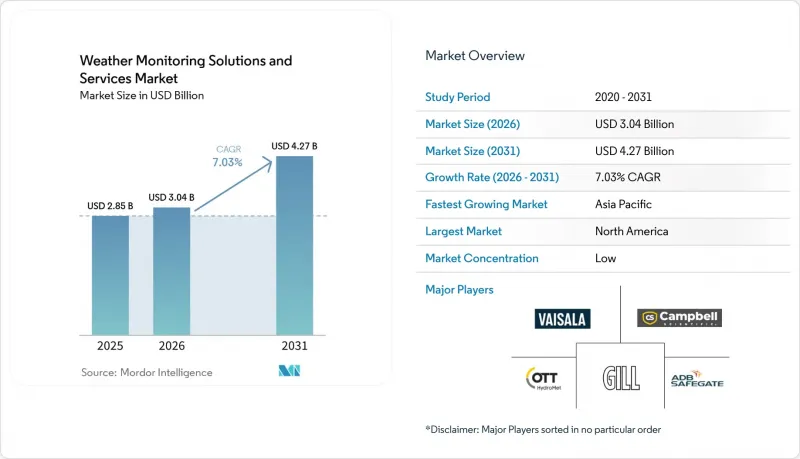

Mordor Intelligence에 의하면, 기상 모니터링 솔루션 및 서비스 시장 규모는 2025년에 28억 5,000만 달러로 평가되었습니다. 2026년 30억 4,000만 달러에서 2031년까지 42억 7,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 7.03%를 나타낼 전망입니다.

본 보고서는 제공 형태(하드웨어, 소프트웨어, 서비스), 시스템 유형(지상형, 기상 레이더 등), 용도(일기예보, 기후·환경 모니터링 등), 최종 사용자 산업(에너지 및 유틸리티, 해양·해상, 정부·국방 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 기상 모니터링 솔루션 및 서비스 시장 동향과 인사이트

정확한 자원 평가에 따른 재생에너지 수요

전력 회사와 프로젝트 개발자들은 현재, 풍력 및 태양광 발전 도입률이 높은 전력망의 균형을 맞추기 위해 1킬로미터 단위로 15분 간격의 예보가 필요합니다. 유럽 중기 기상 예보 센터(ECMWF)는 60초 미만의 시간 내에 10일간의 전 세계 기상 예보를 제공하는 AI 예보 시스템을 도입하여, 운영자가 신속하게 앙상블 시나리오를 실행할 수 있도록 했습니다. 바이살라의 ‘Compass’ 플랫폼은 위성 이미지, 드론을 통한 프로파일 데이터, 지상 센서 데이터를 융합하여 자산의 활용도를 높이는 현장별 일사량 곡선을 생성합니다. 북해에 배치된 부유식 라이더 및 기상 드론은 터빈 후류 모델링 오차를 15% 줄여, 해상 풍력 발전소의 유지보수 예산을 절감합니다. 넷 제로 목표를 법제화하는 관할 구역이 늘어남에 따라, 투자자들은 상세한 기상 정보를 단순한 선택적 보험이 아닌 필수적인 프로젝트 인프라로 인식하고 있습니다.

기후 변화로 인한 이상 기후 증가

홍수, 허리케인, 산불로 인한 보험금 지급액은 2024년에 1,000억 달러를 넘어섰으며, 초국지적 위험도 모델에 대한 재보험 요건이 강화되었습니다. 유럽연합(EU)은 기후 변화 적응 인프라에 연간 700억 유로(770억 달러)를 투자하여, 고밀도 강우량 관측망과 고산 지대의 돌발 홍수 대비를 위한 X-밴드 레이더에 자금을 지원하고 있습니다. 미국 해양대기청(NOAA)의 이중 편파 레이더 개량으로 인해, 지자체 대피 지시의 근거가 되는 우박 크기 추정 정확도가 향상되었습니다. 일본에서는 빗물 터널에 센서를 설치하고 수문을 자동으로 닫도록 함으로써, 사후 대응형에서 예측형 제어 방식으로 전환하고 있습니다. 10억 달러 규모의 재해 발생 빈도는 계속해서 두 배로 증가하고 있지만, 경보가 발령되기까지 걸리는 시간은 여전히 13분에 그치고 있어, 위상 배열 레이더와 머신러닝을 활용한 실시간 예보의 필요성이 부각되고 있습니다.

첨단 레이더 및 위성 탑재체의 높은 자본 비용

S-밴드 듀얼 편파 레이더는 대당 100만-500만 달러에 판매되고 있으며, 전체 수명 주기 동안 추가로 발생하는 설치 장소 및 전력 비용은 포함되어 있지 않습니다. 위성 영상 장비는 2억 달러에 달하며, 이는 WMO 회원국의 80%가 할당하는 기상 예산을 훨씬 웃도는 금액입니다. 스페인은 18기의 신형 레이더에 2,500만 유로(2,750만 달러)를 투자하여 2024년 자본 계획의 40%를 소진했습니다. 위상 배열 시제품의 가격은 1,500만 달러로 책정되어 있으며, 도입은 미국과 일본의 연구 분야로 한정되어 있습니다. 신흥국에서는 5,000달러 규모의 자동 관측소로 구성된 대략적인 관측망을 수용함으로써, 합리적인 가격을 실현하기 위해 경보 발령까지 걸리는 시간을 희생하고 있습니다.

부문별 분석

서비스 부문은 예측 기간 동안 연평균 성장률(CAGR) 8.11%로 확대될 전망이며, 2025년에는 하드웨어 매출 점유율 44.87%를 넘어섰습니다. 재생에너지 사업자, 항공사, 지자체는 데이터 수집, 품질 관리, 분석을 패키지화한 성과 기반 계약을 선호하고 있으며, 이를 통해 기상 모니터링 솔루션 및 서비스 시장에서 설비 투자(Capex)를 운영 비용(OpEx)으로 전환하고 있습니다. Baron Services는 2025년, 물류 기업이 기상 전문가를 고용하지 않고도 경보 기능을 통합할 수 있는 화이트 라벨 API를 출시했습니다. Meteomatics의 2,200만 달러 규모의 시리즈 C 자금 조달은 연간 라이선스 방식으로 판매되는 드론 기반 프로파일링 기술을 지원하기 위한 것입니다. 인도 내 1,800곳의 관측소 구축 등, 정부 조달에서는 여전히 하드웨어 판매가 주를 이루고 있지만, 10년 주기의 갱신 주기가 성장의 걸림돌이 되고 있습니다. 서비스로의 전환에 따라 벤더의 이익률은 25%에 달하고, 센서 하드웨어의 2배 수준이 되었으며, 지속적인 수익 창출이 강화되고 있습니다.

2세대 플랫폼은 하이브리드형 비즈니스 모델을 구현하고 있습니다. 바이살라(Vaisala)는 센서 패키지를 자사의 ‘Compass’ 클라우드 엔진과 결합하여, 바이어스를 보정한 풍속 곡선을 제공함으로써 발전 제한으로 인한 불이익을 줄이고 있습니다. 캠벨 사이언티픽(Campbell Scientific)의 ‘WeatherBrain’은 데이터 로거 군을 가변율 관개 지도로 변환하여, 농업 전문가들이 소프트웨어 라이선스를 통해 이에 접근할 수 있도록 합니다. 도입 기반이 확대됨에 따라 고객 락인 효과가 강화되고, 전환 비용이 구독 모델을 보호함으로써 기상 모니터링 솔루션 및 서비스 시장의 장기적인 현금 흐름이 유지됩니다.

2025년, 위성 플랫폼은 34.25%의 점유율을 차지하며 대륙 규모의 이미지를 제공했지만, 수직 방향의 상세도는 제한적입니다. 기상 드론은 격렬한 대류가 발생하는 고도 0-5킬로미터 구역을 관측하기 위해 7.89%의 성장률을 보이고 있습니다. Meteomatics사는 노르웨이 전역에서 30대의 Meteodrone을 운용하여 계곡 지역의 예보 오차를 20% 줄였습니다. 2024년에는 Black Swift사의 항공기가 허리케인 이다리아의 눈벽으로 진입하여, 상륙 지점의 불확실성을 20킬로미터 줄였습니다. 지상 관측소는 여전히 중요하지만, 드론으로는 복잡한 지형에서 발생하는 신호를 필요에 따라 포착할 수 없습니다.

레이더는 듀얼 편파 방식으로 업그레이드되어 비와 우박을 구분할 수 있게 되었습니다. 또한, 위상 배열 시제품은 30초마다 스캔을 수행하지만, 1,500만 달러에 달하는 비용이 상용화의 걸림돌이 되고 있습니다. WMO는 아프리카 전역에 저비용 LoRaWAN 기지국의 보급을 추진하고 있으나, 교정 실험실의 부족으로 인해 데이터 품질이 저하되고 있습니다. 레이더, 드론, 위성 데이터를 통합한 시스템군은 다중 재해 조기 경보를 위한 기상 모니터링 솔루션 및 서비스 시장 규모를 뒷받침하며, 회복탄력성 강화를 위한 노력을 뒷받침하고 있습니다.

지역별 분석

북미는 2025년 매출의 36.67%를 차지하며, 1980년대의 센서 어레이를 결빙 및 난기류를 실시간으로 보고하는 네트워크 연결형 장치로 대체하는 FAA NextGen 업그레이드가 주요 성장 동력이 되었습니다. NOAA는 2024년에 160곳의 레이더를 이중 편파 방식으로 개조하는 작업을 완료했으며, 이 데이터는 카운티 단위의 경보 시스템에 제공되어 토네이도 오경보를 줄이고 있습니다. 텍사스주와 캘리포니아주의 태양광 발전 사업자들은 확률론적 일사량 데이터를 활용해 출력 제한 위험을 헤지하고, 예측 정확도를 바탕으로 과태료를 피하고 있습니다. 캐나다는 2025년까지 WeatherBrain을 전국으로 확대하고, 가변율 관개 지도를 위한 토양 수분 원격 측정 서비스를 상업화했습니다.

아시아태평양은 7.78%라는 가장 높은 연평균 성장률(CAGR)을 기록하고 있습니다. 인도의 20억 달러 규모 ‘Mausam 2.0’ 프로젝트는 2025년에 레이와 프라야그라지에 도플러 장비를 추가했고, 2030년까지 레이더 60기와 관측소 1,800곳을 구축할 계획입니다. 중국은 2,400곳의 관측소와 236기의 레이더를 운영하고 있으며, 이들은 남중국해에서의 해상 풍력 발전 추진을 뒷받침하고 있습니다. 일본의 ‘히마와리 9호’ 위성은 태풍 추적을 위해 10분 간격으로 이미지를 제공하고 있으며, ‘히마와리 10호’는 2029년에 발사될 예정이며 화산재 감지 능력이 향상될 것입니다. 한국의 ‘GEO-KOMPSAT-2A’는 서울의 스모그 경보를 위해 2킬로미터 해상도의 대기질 이미지를 추가로 제공합니다. 아세안(ASEAN)의 다중 재해 네트워크는 국경을 넘어 레이더 데이터를 공유함으로써 몬순으로 인한 홍수 경보의 정확도를 높이고 있습니다.

유럽은 회복탄력성(재해 대응 능력) 강화 사업에 연간 700억 유로(770억 달러)를 투자하여, 이중 편파 레이더의 배치를 확대하고 나노위성의 탑재체 개발에 자금을 지원하고 있습니다. 스페인은 2024년에 2,500만 유로 규모의 계약을 바탕으로 구형 레이더를 교체했으며, 그리스는 2025년에 산불 경보용 신형 센서를 도입했습니다. 중동에서는 레이더망 구축과 AI를 활용한 인공 강우 예측에 투자가 이루어지고 있습니다. 남미에서는 WMO의 기술 지원을 받아 현대화가 진행되고 있지만, 교정 실험실 부족으로 인해 센서 인증이 지연되고 있습니다. 아프리카에서는 격차가 가장 두드러지지만, ‘Early Warnings for All’은 저비용 LoRaWAN 노드와 지역 사이렌을 활용하여 2027년까지 전체 인구를 대상으로 서비스를 제공하는 것을 목표로 하고 있습니다. 이러한 지역 프로그램들이 하나로 뭉쳐 폭넓은 활동을 지속함에 따라, 기상 모니터링 솔루션 및 서비스 시장은 지리적으로 계속해서 다양화되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the weather monitoring solutions and services market size was valued at USD 2.85 billion in 2025 and is estimated to grow from USD 3.04 billion in 2026 to reach USD 4.27 billion by 2031, at a CAGR of 7.03% during the forecast period (2026-2031).

This report is Segmented by Offering (Hardware, Software, and Services), System Type (Ground-Based, Weather Radar, and More), Application (Weather Forecasting, Climate and Environmental Monitoring, and More), End-User Industry (Energy and Utilities, Marine and Offshore, Government and Defense, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Weather Monitoring Solutions And Services Market Trends and Insights

Renewable-Energy Demand for Accurate Resource Assessment

Utilities and project developers now require 1-kilometer, 15-minute forecasts to balance grids with high wind and solar penetration. The European Center for Medium-Range Weather Forecasts introduced an AI forecasting system that delivers 10-day global predictions in under 60 seconds, letting operators run fast ensemble scenarios. Vaisala's Compass platform fuses satellite imagery, drone profiles, and ground sensors to craft site-specific irradiance curves that raise asset utilization. Floating lidar and weather drones deployed in the North Sea reduce turbine-wake modeling error by 15%, cutting maintenance budgets for offshore arrays. As more jurisdictions legislate net-zero targets, investors are treating granular weather intelligence as essential project infrastructure rather than optional insurance.

Climate-Change-Driven Rise in Extreme Weather Events

Insured losses from floods, hurricanes, and wildfires surpassed USD 100 billion in 2024, hardening reinsurance requirements for hyperlocal peril models. The European Union directs EUR 70 billion (USD 77 billion) annually to adaptation infrastructure, funding dense rain-gauge grids and X-band radars for alpine flash-flood defense. NOAA's dual-polarization radar retrofit improves hail-size estimates that underpin municipal evacuation triggers. Japan embeds sensors in stormwater tunnels to automate floodgate closures, shifting from reactive to anticipatory control. The frequency of billion-dollar disasters keeps doubling, yet warning lead times remain stuck at 13 minutes, spotlighting the need for phased-array radar and machine-learning nowcasting.

High Capital Costs for Advanced Radar and Satellite Payloads

S-band dual-polarization radars sell for USD 1 million to USD 5 million per unit, excluding site and power costs that add 15% across the lifecycle. Satellite imagers climb to USD 200 million, dwarfing meteorological budgets in 80% of WMO member states. Spain spent EUR 25 million (USD 27.5 million) on 18 new radars, consuming 40% of its 2024 capital plan. Phased-array prototypes priced at USD 15 million, limiting deployment to the U.S. and Japan research fields. Emerging economies accept coarser coverage from USD 5,000 automatic stations, sacrificing warning lead time for affordability.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Precision Agriculture and Smart Farming

- Expanding Deployment of IoT-Enabled Sensor Networks

- Proprietary Data Silos and Sharing Restrictions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The services segment is expanding at an 8.11% CAGR during the forecast period, outstripping hardware's 44.87% revenue share in 2025. Renewables traders, airlines, and municipalities prefer outcome-based contracts that bundle ingestion, quality control, and analytics, converting capex to opex in the weather monitoring solutions and services market. Baron Services launched a white-label API in 2025 that lets logistics firms embed alerts without hiring meteorologists. Meteomatics' USD 22 million Series C backs drone profiling sold under annual licenses. Hardware sales still anchor government procurements such as India's 1,800-station rollout, but 10-year replacement cycles cap growth. The services tilt lifts vendor margins to 25%, double those of sensor hardware, reinforcing the pivot toward recurring revenue.

Second-generation platforms illustrate hybrid economics. Vaisala bundles sensor packages with its Compass cloud engine, delivering bias-corrected wind curves that shave curtailment penalties. Campbell Scientific's WeatherBrain turns datalogger fleets into variable-rate irrigation maps that agronomists access through software seats. As the installed base expands, customer lock-in rises, and switching costs protect subscriptions, sustaining long-run cash flows within the weather monitoring solutions and services market.

Satellite platforms owned 34.25% share in 2025, supplying continental imagery but limited vertical detail. Weather drones grow at 7.89% as they profile the 0-5 kilometer layer where severe convection forms. Meteomatics operates 30 Meteodrones across Norway, cutting valley forecast error by 20%. Black Swift aircraft entered Hurricane Idalia's eyewall in 2024, shrinking landfall uncertainty by 20 kilometers. Ground stations remain critical yet miss complex terrain signals that drones capture on demand.

Radars upgrade to dual-polarization, distinguishing rain from hail, while phased-array prototypes scan every 30 seconds, but USD 15 million tags stall commercialization. WMO drives low-cost LoRaWAN station growth across Africa, yet a lack of calibration labs undermines data quality. Integrated fleets that mix radar, drone, and satellite streams underpin the weather monitoring solutions and services market size for multi-hazard early warning, strengthening resilience agendas.

Geography Analysis

North America generated 36.67% of 2025 revenue, anchored by FAA NextGen upgrades that replace 1980s sensor arrays with networked devices reporting icing and turbulence in real time. NOAA finished its 160-site radar dual-polarization retrofit in 2024, feeding county-level alert systems that cut tornado false alarms. Solar operators in Texas and California hedge curtailment risk through probabilistic irradiance feeds, translating forecast skill into avoided penalties. Canada expanded WeatherBrain nationwide by 2025, monetizing soil-moisture telemetry for variable-rate irrigation maps.

Asia-Pacific records the fastest 7.78% CAGR. India's USD 2 billion Mausam 2.0 added Doppler units in Leh and Prayagraj in 2025 on a path to 60 radars and 1,800 stations by 2030. China runs 2,400 stations and 236 radars that support its South China Sea offshore wind push. Japan's Himawari-9 satellite provides 10-minute imagery for typhoon tracking, and Himawari-10 launches in 2029 with better volcanic-ash detection. Korea's GEO-KOMPSAT-2A adds 2-kilometer air-quality frames for Seoul smog advisories. ASEAN's multi-hazard network shares radar data across borders, improving monsoon flood warnings.

Europe channels EUR 70 billion (USD 77 billion) annually into resilience works, upgrading dual-polarization radar fleets, and funding nanosatellite payloads. Spain replaced legacy radars under a EUR 25 million contract in 2024, while Greece deployed new sensors for wildfire alerts in 2025. The Middle East invests in radar coverage and AI cloud-seeding forecasts. South America modernizes under WMO technical aid but faces calibration-lab shortages that slow sensor certification. Africa holds the widest gaps; Early Warnings for All targets full population coverage by 2027 through low-cost LoRaWAN nodes and community sirens. Together, regional programs maintain broad engagement, ensuring the weather monitoring solutions and services market continues to diversify geographically.

- Vaisala Oyj

- Campbell Scientific Inc.

- OTT Hydromet GmbH

- Gill Instruments Limited

- ADB SAFEGATE

- Delta OHM S.r.l. a Socio Unico

- Lufft Mess- und Regeltechnik GmbH

- Airmar Technology Corporation

- R.M. Young Company

- Pessl Instruments GmbH

- Hobo / Onset Computer Corporation

- Columbia Weather Systems, Inc.

- Perry Weather, Inc.

- Baron Services, Inc.

- RIKA Sensors Co., Ltd.

- Davis Instruments Corporation

- Teledyne Marine (Teledyne Technologies Inc.)

- Meteomatics AG

- Earth Networks, Inc.

- Senseca Germany GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Renewable-Energy Demand for Accurate Resource Assessment

- 4.2.2 Climate-Change-Driven Rise in Extreme Weather Events

- 4.2.3 Adoption of Precision Agriculture and Smart Farming

- 4.2.4 Expanding Deployment of IoT-Enabled Sensor Networks

- 4.2.5 Government Mandates for Aviation and Maritime Safety Compliance

- 4.2.6 Emergence of Low-Earth-Orbit Nanosatellite Constellations

- 4.3 Market Restraints

- 4.3.1 High Capital Costs for Advanced Radar and Satellite Payloads

- 4.3.2 Proprietary Data Silos and Sharing Restrictions

- 4.3.3 Lack of Certified Calibration Labs in Emerging Markets

- 4.3.4 Lithium Supply Tightness for Remote-Sensor Batteries

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By System Type

- 5.2.1 Ground-based Stations

- 5.2.2 Satellite-based Systems

- 5.2.3 Weather Radar

- 5.2.4 Weather Drones/Unmanned Systems

- 5.3 By Application

- 5.3.1 Weather Forecasting

- 5.3.2 Climate and Environmental Monitoring

- 5.3.3 Disaster and Public-Safety Management

- 5.3.4 Renewable-Energy Resource Optimization

- 5.4 By End-user Industry

- 5.4.1 Agriculture

- 5.4.2 Energy and Utilities

- 5.4.3 Aviation and Airports

- 5.4.4 Marine and Offshore

- 5.4.5 Transportation and Logistics

- 5.4.6 Government and Defense

- 5.4.7 Media and Consumer Services

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of the Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Vaisala Oyj

- 6.4.2 Campbell Scientific Inc.

- 6.4.3 OTT Hydromet GmbH

- 6.4.4 Gill Instruments Limited

- 6.4.5 ADB SAFEGATE

- 6.4.6 Delta OHM S.r.l. a Socio Unico

- 6.4.7 Lufft Mess- und Regeltechnik GmbH

- 6.4.8 Airmar Technology Corporation

- 6.4.9 R.M. Young Company

- 6.4.10 Pessl Instruments GmbH

- 6.4.11 Hobo / Onset Computer Corporation

- 6.4.12 Columbia Weather Systems, Inc.

- 6.4.13 Perry Weather, Inc.

- 6.4.14 Baron Services, Inc.

- 6.4.15 RIKA Sensors Co., Ltd.

- 6.4.16 Davis Instruments Corporation

- 6.4.17 Teledyne Marine (Teledyne Technologies Inc.)

- 6.4.18 Meteomatics AG

- 6.4.19 Earth Networks, Inc.

- 6.4.20 Senseca Germany GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment