|

시장보고서

상품코드

2063236

백 필터 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Bag Filter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

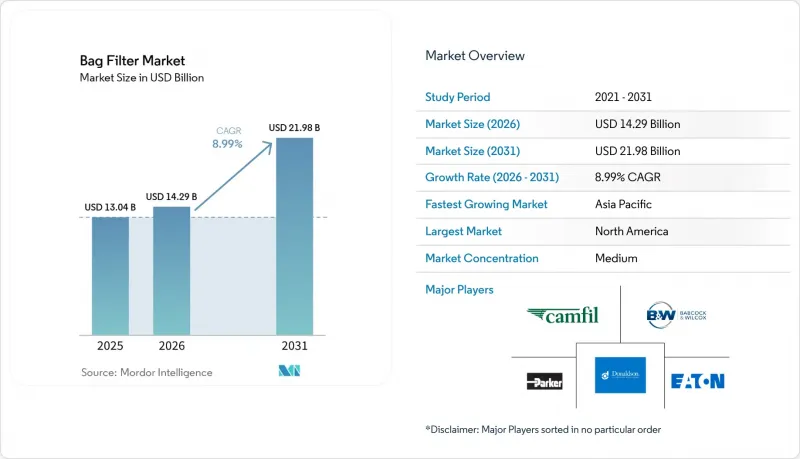

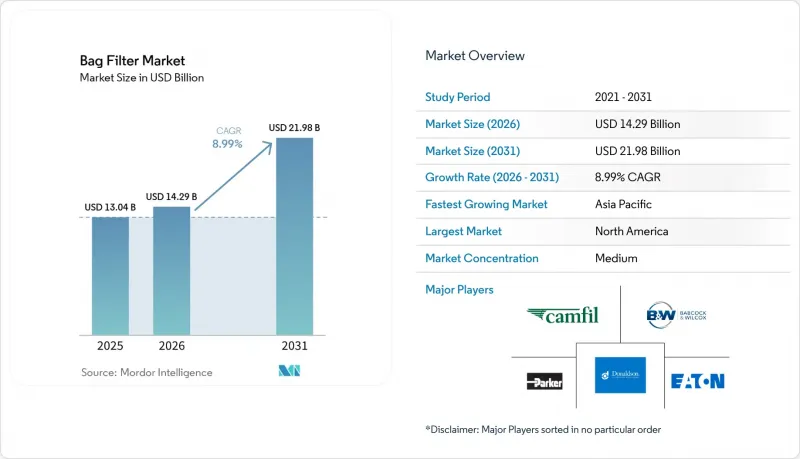

Mordor Intelligence에 의하면, 백 필터 시장 규모는 2025년에 130억 4,000만 달러로 평가되었습니다. 2026년 142억 9,000만 달러에서 2031년까지 219억 8,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 8.99%를 나타낼 전망입니다.

본 보고서는 유형(펄스 제트, 리버스 에어, 셰이커), 필터 매체(직물, 부직포, 유리섬유, 기타), 용도(분진 억제, 대기 오염 방지, 제품 회수, 수처리, 기타), 최종 사용자(발전, 시멘트, 화학, 기타), 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 백 필터 시장 동향 및 분석

더 엄격한 산업 배출 규제

중국은 신규 석탄 화력 발전소에 대해 30 mg/Nm3 미만의 미세먼지 배출 제한을 시행하고 있으며, 인도는 시멘트 가마에 대해 50 mg/Nm3 미만을 의무화하고 있어, 규제 준수를 위해 천 필터의 도입이 필수적입니다. 유럽연합(EU)의 ‘산업 배출 지침’ 개정에 따라 허용 분진 기준치가 하향 조정됨에 따라, 금속 및 폐기물 발전 시설 전반에 걸쳐 개보수 작업이 진행되고 있습니다. 일리노이주는 2025년 1월부터 PTFE-textiles의 사용을 금지했으며, 미국 환경보호청(EPA)은 현재 PFAS 사용 정보 공개를 의무화하고 있어, 플라즈마 처리 폴리에스터 및 나노섬유 펠트에 대한 연구를 장려하고 있습니다. 따라서 공급업체는 ISO 14001 및 각 지역의 대기질 규제에 대한 인증을 유지하기 위해, 아시아 시장용 PTFE 제품과 유럽·미국 시장용 무불소 제품이라는 두 가지 제품 포트폴리오를 관리해야 합니다. 사출, 필름 성형, 후가공을 자사에서 일관되게 관리하는 수직 통합형 기업이 이러한 양극화에 대응하는 데 있어 가장 유리한 입장에 있습니다.

신흥 아시아 지역의 석탄·바이오매스 발전 용량 확대

중국은 2025년에 78GW 규모의 신규 석탄 화력 발전 설비를 가동했으며, 같은 해에 추가로 161GW를 계획해, 총 291GW에 달하는 계획 중인 프로젝트가 백하우스(집진 장치)에 대한 지속적인 수요를 보장했습니다. 인도의 시멘트 제조업체들은 2026-28년도에 1억 6,000만-1억 7,000만 톤의 분쇄 능력 확충을 계획하고 있으며, 이는 지난 3년간 증가 속도의 3배에 해당합니다. 한편, 아세안(ASEAN)의 전력 회사들은 바이오매스를 혼소하고 있으며, 이로 인해 발생하는 재의 화학적 특성 때문에 신뢰성을 확보하기 위해 중복된 펄스 제트 라인이 필요합니다. 이러한 병행 투자가 고온·대용량 백 필터 시장의 성장을 뒷받침하며, 다른 지역에서 진행되고 있는 석탄 화력 발전소 폐쇄의 영향을 상쇄하고 있습니다.

OECD 회원국들의 석탄 화력 발전소 건설 둔화

미국과 유럽연합(EU)에서는 새로 건설되는 석탄 화력 발전소보다 폐쇄되는 발전소가 더 많은 상황이며, 2025년에는 미국 전력 공급에서 석탄이 차지하는 비중이 20% 미만으로 떨어졌습니다. 따라서 이 지역에서의 백 필터 수요는 개보수 공사나 애프터마켓용 필터 백에 집중되어 있어, 설비 판매에는 부담을 주고 있는 반면, 다각화를 추진한 공급업체에게는 소모품 매출을 유지하는 요인이 되고 있습니다.

부문별 분석

펄스 제트식 유닛은 2025년 매출의 63.9%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 9.5%를 기록할 전망입니다. 이는 지속적인 청소와 30 mg/Nm3 미만의 배출 보장을 요구하는 중국의 여러 기가와트급 석탄 화력 발전소에 의해 뒷받침되고 있습니다. 펄스 제트 방식 설계에는 차압 센서가 내장되어 있어, 솔레노이드의 작동 타이밍을 최적화함으로써 연간 최대 15%의 압축 공기를 절약합니다. 리버스 에어 시스템은 제약 및 특수 화학제품 분야의 취급이 까다로운 분말 생산 라인에 사용되는 반면, 셰이커 유닛은 성능보다 간편성이 중시되는 제재소나 곡물 엘리베이터에서 여전히 사용되고 있습니다. 프로이덴베르크사의 2026년형 저압손실 미디어는 펄스 제트 설비의 에너지 효율을 한층 더 높여줍니다. GEMCO의 목재 펠릿 가이드에서 권장하는 바와 같이, 여러 분진 발생원을 연결하는 집중형 펄스 제트 집진기는 설치 비용을 30% 절감하며, 이러한 구성이 백 필터 시장을 독점하고 있는 이유를 뒷받침하고 있습니다.

부직포 펠트는 2025년에 55.1%의 시장 점유율을 차지했습니다. 이는 직물에 비해 비용을 25% 절감하면서도 발수성을 높이는 PTFE나 플라즈마 처리된 최상층을 적용할 수 있는 확장성이 뛰어난 니들펀치 생산 방식 덕분입니다. 항저우 헝커(Hangzhou Hengke)의월50만 장에 달하는 생산 능력은 세계 공급을 뒷받침할 수 있는 그 규모를 여실히 보여주고 있습니다. 유리 섬유는 260℃를 초과하는 폐기물 발전 플랜트의 연도 구조물을 지탱하지만, 취성 및 산에 의한 부식으로 인해 사용량이 제한되고 있습니다. 열가소성 펠트의 자동 열용접을 통해 스티치 구멍이 제거되고 파열 강도가 30% 향상됨에 따라, 부직포 설계는 무균 등급의 식품 및 의약품용 백에 있어 매력적인 선택지가 되고 있습니다. PFAS 프리 코팅으로의 전환에 따라 플라즈마 챔버 및 나노파이버 라인에 대한 투자가 가속화되면서, 2031년까지 부직포 매체의 연평균 성장률(CAGR)은 9.4%를 유지할 것으로 전망됩니다.

지역별 분석

북미는 석탄에서 가스로의 전환, PFAS 규제, 그리고 뉴저지주와 노스캐롤라이나주의 밀집된 제약 클러스터에 힘입어 2025년 매출의 40.3%를 차지했습니다. 일리노이주의 PTFE 금지 조치와 EPA의 공개 규정에 따라, 공급업체들은 불소 무함유 펠트 인증을 받아야 하는 상황에 놓여 있으며, 자체적으로 플라즈마 기술을 보유한 수직 통합형 제조업체들이 유리한 입장에 서게 되었습니다. 도널드슨이 8억 2,000만 달러에 파셋을 인수한 것은 성숙한 장비 시장에서 소모품 분야로의 진출을 추진하려는 움직임을 뒷받침하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 11.6%를 기록할 전망이며, 이를 견인할 요인은 중국의 2025년 석탄 화력 발전소 78GW 증설과, 인도의 1억 6,000만-1억 7,000만 톤 규모의 시멘트 생산 확대 계획입니다. 중국의 30 mg/Nm3, 인도의 소성로에서 적용되는 50 mg/Nm3라는 엄격한 미세먼지 배출 기준은 천 필터의 필요성을 확고히 하고 있습니다. 아세안(ASEAN) 국가들에서 바이오매스 혼소 방식은 부식성 재를 발생시켜, 내화학성 펠트 및 이중화된 백하우스에 대한 수요를 견인하고 있습니다.

유럽에서는 개정된 산업 배출 지침에 따라 분진 규제가 강화되고 PFAS 금지 조치가 추진됨에 따라, PFAS가 포함되지 않은 필터 매체와 예측 유지보수용 센서가 주목받고 있습니다. 영국 공장에 LoRaWAN이 도입된 것은 해당 지역이 디지털 유지보수 분야에서 선도적인 위치를 차지하고 있음을 입증하고 있습니다. 러시아, 남미, 중동에서는 광업, 시멘트, 석유화학 프로젝트가 증가하고 있으며, 중국의 OEM 제조업체들이 자본 비용 측면에서 적극적으로 경쟁을 펼치고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the bag filter market size was valued at USD 13.04 billion in 2025 and is estimated to grow from USD 14.29 billion in 2026 to reach USD 21.98 billion by 2031, at a CAGR of 8.99% during the forecast period (2026-2031).

This report is Segmented by Type (Pulse Jet, Reverse Air, Shaker), Filter Media (Woven, Non-Woven, Glass Fiber, Others), Application (Dust Control, Air Pollution Control, Product Recovery, Water Treatment, Others), End-User (Power Generation, Cement, Chemical, and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Global Bag Filter Market Trends and Insights

Stricter Industrial Emission Regulations

China enforces sub-30 mg/Nm3 particulate limits for new coal plants, while India mandates sub-50 mg/Nm3 for cement kilns, making fabric filtration compulsory for compliance. The European Union's Industrial Emissions Directive revision reduces permitted dust thresholds, driving retrofits across metals and waste-to-energy sites. Illinois banned PTFE textiles effective January 2025, and the U.S. EPA now requires PFAS usage disclosure, pushing research into plasma-treated polyester and nanofiber felts. Suppliers must therefore manage dual portfolios, PTFE for Asia and fluorine-free for Western markets, to remain certified under ISO 14001 and regional air-quality codes. Vertically integrated companies that control yarn extrusion, membrane casting, and post-treatment are best placed to navigate this split.

Expansion of Coal and Biomass Capacity in Emerging Asia

China commissioned 78 GW of new coal units in 2025 and proposed another 161 GW during the same year, with a 291 GW pipeline ensuring sustained baghouse demand . India's cement producers plan 160-170 million ton of grinding additions in fiscal 2026-28, triple their prior three-year pace, while ASEAN utilities co-fire biomass, which creates ash chemistry that requires redundant pulse-jet lines for reliability. These parallel investments anchor high-temperature, high-volume bag filter market growth and offset coal retirements elsewhere.

Slowdown of Coal Power Build-Out in OECD

The United States and the European Union retire more coal units than they build, and coal generated less than 20% of U.S. electricity in 2025 . Bag filter demand in these regions, therefore, tilts toward retrofits and aftermarket bags, pressuring equipment sales but sustaining consumables revenue for diversified suppliers.

Other drivers and restraints analyzed in the detailed report include:

- Capacity Additions in Cement and Mining Industries

- Retrofit Shift from ESP to Baghouse Systems

- Volatile Prices of Polyester and PTFE

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pulse-jet units captured 63.9% of 2025 revenue and are on track for a 9.5% CAGR through 2031, supported by multi-gigawatt coal plants in China that require continuous cleaning and sub-30 mg/Nm3 guarantees. Pulse-jet designs integrate differential-pressure sensors that optimize solenoid timing, saving up to 15% compressed air per year. Reverse-air systems serve fragile powder lines in pharmaceuticals and specialty chemicals, while shaker units persist in sawmills and grain elevators where simplicity trumps performance. Freudenberg's 2026 low-pressure-drop media further improve energy efficiency in pulse-jet installations. Centralized pulse-jet collectors that link several dust sources, as promoted in the GEMCO wood-pellet guide, cut installed cost by 30% and demonstrate why this configuration dominates the bag filter market.

Non-woven felts held 55.1% share in 2025, thanks to scalable needle-punch production that keeps cost 25% below woven fabrics while allowing PTFE or plasma top-layers for hydrophobicity. Hangzhou Hengke's 500,000-piece monthly capacity exemplifies the scale that underpins global supply. Glass fiber supports waste-to-energy stacks above 260 °C, though brittleness and acid attack limit volumes. Automated heat-welding of thermoplastic felts removes stitch holes, boosting burst strength by 30% and making non-woven designs attractive for sterile-grade food and pharma bags. The shift to PFAS-free coatings accelerates investments in plasma chambers and nanofiber lines, sustaining a 9.4% CAGR for non-woven media through 2031.

Geography Analysis

North America generated 40.3% of 2025 revenue, supported by coal-to-gas retrofits, PFAS legislation, and dense pharmaceutical clusters in New Jersey and North Carolina. Illinois' PTFE ban and EPA disclosure rules force suppliers to qualify fluorine-free felts, favoring vertically integrated producers with in-house plasma technology. Donaldson's USD 820 million Facet deal underscores the push for consumables exposure in a mature equipment market.

Asia-Pacific will post an 11.6% CAGR to 2031, led by China's 78 GW of 2025 coal additions and India's 160-170 million ton cement expansion pipeline. Tight particulate standards of 30 mg/Nm3 in China and 50 mg/Nm3 in Indian kilns cement the need for fabric filtration. ASEAN biomass co-firing introduces corrosive ash that drives demand for chemically resistant felts and redundant baghouses.

Europe tightens dust limits under the updated Industrial Emissions Directive and advances PFAS bans, favoring PFAS-free media and predictive sensors. LoRaWAN deployments across UK factories prove the region's leadership in digital maintenance. Russia, South America, and the Middle East add mining, cement, and petrochemical projects where Chinese OEMs compete aggressively on capital cost.

- Donaldson Company Inc.

- Parker-Hannifin Corp.

- Camfil AB

- Babcock & Wilcox Enterprises

- Eaton Corp. plc

- Thermax Ltd.

- Danaher (Pall Corp.)

- Mitsubishi Power

- WL Gore & Associates

- Nederman Holding AB

- Ahlstrom-Munksjo Oyj

- American Air Filter (AAF Flanders)

- Menardi Filters

- Sly Inc.

- Lenntech B.V.

- JK Fenner (India) Ltd.

- Filtra-Systems Co.

- Aircon Corporation

- Hangzhou Filter Technology (China)

- Lydall Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter industrial emission regulations

- 4.2.2 Expansion of coal- & biomass-fired capacity in emerging Asia

- 4.2.3 Capacity additions in cement & mining industries

- 4.2.4 Retrofit shift from ESP to baghouse systems

- 4.2.5 Predictive-maintenance sensor adoption in baghouses

- 4.2.6 Solvent-recovery bag filters in pharmaceutical peptide lines

- 4.3 Market Restraints

- 4.3.1 Slowdown of coal power build-out in OECD

- 4.3.2 Volatile prices of polyester/PTFE filter media

- 4.3.3 Hybrid cartridge-ESP solutions eroding bag filter share

- 4.3.4 PFAS concerns over PTFE-coated bags

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Pulse Jet Bag Filters

- 5.1.2 Reverse Air Bag Filters

- 5.1.3 Shaker Bag Filters

- 5.2 By Filter Media

- 5.2.1 Woven Media

- 5.2.2 Non-Woven Media

- 5.2.3 Glass Fiber Media

- 5.2.4 Others

- 5.3 By Application

- 5.3.1 Dust Control

- 5.3.2 Air Pollution Control

- 5.3.3 Product Recovery

- 5.3.4 Water Treatment

- 5.3.5 Others

- 5.4 By End-user

- 5.4.1 Power Generation

- 5.4.2 Cement Production

- 5.4.3 Chemical and Petrochemicals

- 5.4.4 Pharmaceutical and Biotech

- 5.4.5 Food and Beverage Processing

- 5.4.6 Mining and Metallurgy

- 5.4.7 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 NORDIC Countries

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN Countries

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Donaldson Company Inc.

- 6.4.2 Parker-Hannifin Corp.

- 6.4.3 Camfil AB

- 6.4.4 Babcock & Wilcox Enterprises

- 6.4.5 Eaton Corp. plc

- 6.4.6 Thermax Ltd.

- 6.4.7 Danaher (Pall Corp.)

- 6.4.8 Mitsubishi Power

- 6.4.9 WL Gore & Associates

- 6.4.10 Nederman Holding AB

- 6.4.11 Ahlstrom-Munksjo Oyj

- 6.4.12 American Air Filter (AAF Flanders)

- 6.4.13 Menardi Filters

- 6.4.14 Sly Inc.

- 6.4.15 Lenntech B.V.

- 6.4.16 JK Fenner (India) Ltd.

- 6.4.17 Filtra-Systems Co.

- 6.4.18 Aircon Corporation

- 6.4.19 Hangzhou Filter Technology (China)

- 6.4.20 Lydall Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment