|

시장보고서

상품코드

2063238

라이저 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Risers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

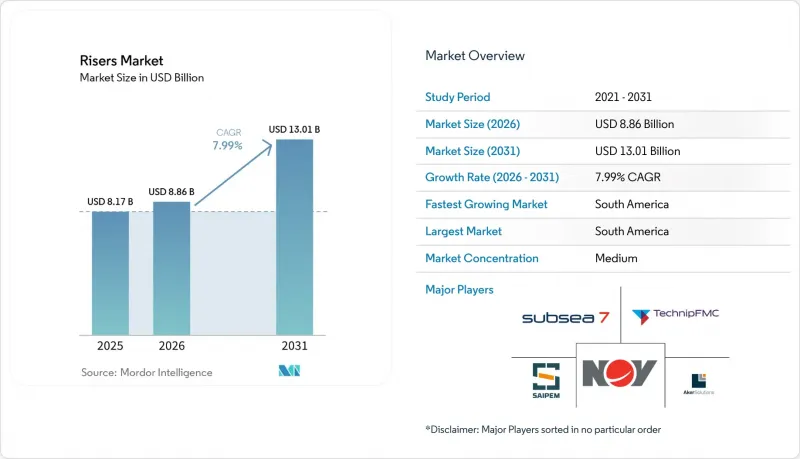

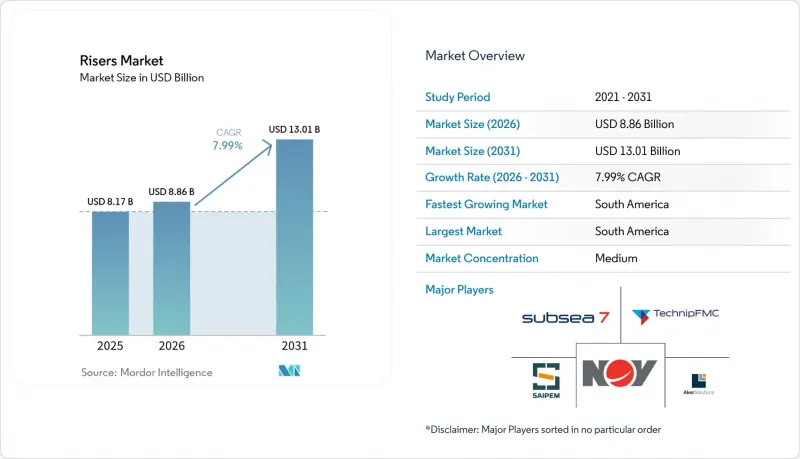

Mordor Intelligence에 의하면, 라이저 시장 규모는 2025년에 81억 7,000만 달러로 평가되었습니다. 2026년 88억 6,000만 달러에서 2031년까지 130억 1,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 7.99%를 나타낼 전망입니다.

본 보고서는 유형(플렉서블 라이저, 리지드 라이저, 하이브리드 라이저), 재질(강철, 복합재, 열가소성 복합 파이프, 기타), 설치 수심(얕은 바다, 심해, 초심해), 용도(시추, 생산, 워크오버, 기타), 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 라이저 시장 동향 및 인사이트

심해 및 초심해 프로젝트의 최종 투자 결정(FID) 재개

엑슨모빌은 가이아나의 ‘해머헤드’ 프로젝트에 68억 달러를 투자하기로 승인했습니다. 이 프로젝트는 2029년 가동을 목표로 하고 있으며, 라이저의 길이는 얕은 바다 기준보다 30-40% 더 길게 설계되었습니다. 한편, 페트로브라스는 ‘SEAP II’를 승인하고, 프레솔트층의 생산 능력을 하루 12만 배럴 증대할 예정입니다. 이를 위해서는 수심 2,200미터에 대응하는 24개의 강철 카테너리 라이저가 필요합니다. 2028년까지 승인된 심해 유전 생산량의 60%를 차지하는 브라질과 가이아나에서 대규모 최종 투자 결정(FID)이 집중되면서, 현지 조선소를 보유한 종합 SURF 도급업체들에게 유리한 상황이 조성되고 있습니다. 안정적인 철강 가격을 바탕으로 EPC 계약을 조기에 체결함으로써, 이러한 개발 프로젝트들은 최근 금속 재료 비용 변동의 영향을 받지 않게 되었으며, 라이저 시장 수요를 향후 수년에 걸쳐 뒷받침하고 있습니다.

브라질과 가이아나에서 SURF 패키지 수주가 급증

Subsea 7은 18개의 플렉서블 라이저를 포함한 14억 달러 규모의 부지오스 11호 프로젝트를 수주한 반면, 테크닙 FMC는 리지드 라이저 공급과 앰빌리컬을 결합한 2억 5,000만-5억 달러 규모의 해머헤드 프로젝트를 확보했습니다. 현재 SURF 패키지의 평균 계약액은 8억 달러를 초과하고 있습니다. 이는 운영사가 공급, 설치 및 상태 관리 서비스를 단일 입찰로 통합하여 성과 위험을 이전하는 동시에 제조 리드타임을 단축하고 있기 때문입니다. 페트로브라스의 프로젝트에서 현지 조달 비율 60% 의무화는 브라질 국내에 제조 능력을 갖춘 계약업체에 경쟁 우위를 가져다주는 반면, 해외 전문 제조업체에게는 시장 진입 장벽이 되고 있습니다.

원유 가격 변동이 FID 시기에 영향을 미침

국제에너지기구(IEA)는 2026년에 하루 150만-250만 배럴공급 과잉이 발생할 것으로 전망하고 있으며, 이로 인해 브렌트유 가격은 배럴당 70달러 아래로 떨어질 압력을 받을 가능성이 있습니다. 브라질과 가이아나의 심해 프로젝트는 손익분기점이 28-35달러인 만큼 영향을 덜 받는 상황이지만, 수익성이 낮은 서아프리카 프로젝트는 6-12개월의 연기에 직면해 있어 라이저 시장의 단기 수주 흐름이 위축되고 있습니다.

부문별 분석

리지드 설계는 연평균 성장률(CAGR) 8.7%를 기록하며, 라이저 시장에서 가장 높은 성장률을 보일 것으로 전망됩니다. 이는 운영자가 검증된 템플릿을 복제함으로써 엔지니어링 주기를 단축하고 일괄 조달을 가능하게 하기 위함입니다. 쉘의 멕시코만 브라운필드 프로그램에서는 3개 유전 간 설비 공통화율을 95% 달성하고, 프런트엔드 엔지니어링 비용을 40% 절감했습니다. 플렉서블 라이저는 뛰어난 동적 추종성 덕분에 2025년 수요의 45.3%를 계속 차지했으며, 테크닙 FMC의 ‘해머헤드’ 수주 프로젝트에서는 왁스 침적을 방지하기 위해 전기 가열식 플렉서블 라인이 채택되었습니다. 하이브리드 콘셉트는 여전히 틈새 시장 수준에 머물러 있지만, 상부 장력이 1,000톤을 넘는 초심해에서는 필수적인 요소이며, 해저에 고정된 리지드 섹션과 내피로성이 뛰어난 복합재로 제작된 탑스트링을 결합한 구조입니다. 표준화된 리지드 시스템으로의 전환은 조달 계획의 확실성을 뒷받침하며, 대용량 스풀 기반을 갖춘 계약업체들에게 시장 점유율을 몰아주고 있습니다.

업계의 모듈화는 애프터마켓 수익도 끌어올리고 있습니다. 표준화된 설계를 통해 예비 부품의 재고 관리가 간소화되고, 검사 절차가 합리화됨으로써 총 소유 비용이 절감됩니다. 그렇긴 하지만, 기존 인프라로 인해 구불구불한 배관 경로가 필요한 복잡한 타이백이나 수명 연장 프로그램의 경우, 플렉서블 라인은 여전히 필수적입니다. 탄소섬유 인장 보강재가 최종 인증 요건을 충족함에 따라, 복합재와 강철을 결합한 하이브리드 제품이 보급될 전망입니다. 이를 통해 중량이 경감되어 라이저 시장에서 선택할 수 있는 선박의 폭이 넓어지고, 설치 기간을 단축할 수 있게 됩니다.

복합재로 만든 대체품은 연평균 성장률(CAGR) 9.1%로 성장하며, 2025년 라이저 시장 규모에서 철강의 69.5% 점유율을 차지했습니다. 스트롬사의 열가소성 수지 파이프는 이미 물 주입 용도 단계를 넘어, 2027년에는 페트로브라스사와의 본격적인 생산 업무로 전환될 전망입니다. 마그마·세카이사는 강철 파이프의 경우 고비용의 능동 냉각이 필요한 서아프리카의 고온 유정을 주요 대상으로 삼고 있습니다. 현장 데이터에 따르면, 무게는 77.7% 감소했음에도 인장 강도는 동등한 것으로 나타났으며, 강관으로는 데크 하중을 견딜 수 없는 릴 부설 작업에서 복합재는 매력적인 대안이 되고 있습니다.

DNV가 영구적인 사용에 대한 비금속 라이저를 승인함에 따라, 규제상의 승인이라는 마지막 장벽이 제거되었습니다. 적층재에 내장된 광섬유 센싱 기술을 통해 각 복합재 라이저는 자체 모니터링 기능을 갖춘 자산이 되며, 외부 계측 장비가 필요 없어집니다. 그러나 1만 5,000 psi를 초과하는 초고압의 산성 환경에서는 폴리머 매트릭스의 수소 취성이 여전히 우려되므로, 강재가 여전히 우위를 점하고 있습니다. 릴레이 선박공급 부족과 초기 자재비 상승으로 인해 도입 속도가 둔화되고 있지만, 수명 주기 비용 측면에서는 여전히 매력적이며, 예측 기간 동안 복합재가 라이저 시장 점유율을 서서히 확대해 나갈 것으로 확실시되고 있습니다.

지역별 분석

남미는 2025년에 세계 수요의 35.7%를 차지했으며, 연평균 성장률(CAGR) 8.4%로 확대되어 모든 지역 중 가장 높은 성장률을 보일 것으로 전망됩니다. 페트로브라스의 SEAP II 프로젝트만 해도 10,000 psi의 내압 성능을 갖춘 라이저 24개가 필요한 반면, 엑슨모빌의 가이아나 해머헤드 개발 프로젝트에서는 2029년까지 생산용 라이저 6개가 추가로 도입될 예정입니다. 브라질에서는 허가 절차의 효율화로 승인 기간이 12개월로 단축되었으며, 가이아나에서는 300억 달러 규모의 투자 계획에 따라 2028년까지 40개 이상의 신규 라이저가 도입될 전망입니다. 라이저 시장은 지역 내 제조를 촉진하고 물류 체인을 단축하는 예측 가능한 현지 조달 규정의 혜택을 받고 있습니다.

북미에서는 기존 시설의 최적화가 주를 이루고 있습니다. 쉘의 카이키아스 워터플러드 사업과 멕시코만 내의 여러 개조 프로젝트로 인해 서비스 수요는 높은 수준을 유지하고 있는 반면, 미국 BOEM(해양에너지관리국)의 보증금 제도 변경으로 인해 초기 비용 부담이 증가하고 있습니다. 유럽에서는 북해에서 슈퍼 오퍼레이터를 중심으로 통합이 진행되고 있습니다. 쉘과 에퀴놀의 아두라 벤처는 규모의 경제를 활용한 통합 검사 프로그램 하에서 하루 14만 배럴 상당의 원유 생산량을 관리하고 있습니다. 2026년에 시행될 영국의 탄소 포집 규정에 따라, 신규 개발 프로젝트에 대한 타당성 조사가 의무화되며, 향후 최종 투자 결정(FID)은 통합형 CCS(탄소 포집 및 저장) 구상과 연계될 것입니다.

중동 및 아시아·태평양 지역은 제2의 거점으로 부상하고 있습니다. ADNOC의 SARB Deep Gas 및 Nasr-115 확장 프로젝트에서는 사워 가스 생산을 위해 내식성 합금 라이저가 도입된 반면, CNOOC는 남중국해에서의 활동을 확대하며 카이핑 18-1에서 리지드 스트링을 채택하고 있습니다. 동남아시아는 가격의 불확실성과 자금 조달 제약으로 인해 뒤처지고 있지만, 말레이시아와 인도네시아는 계속해서 꾸준한 기여를 이어가고 있습니다. 이러한 동향들이 복합적으로 작용함에 따라, 수익의 지리적 구성이 다양화되어 전 세계 라이저 시장이 단일 분지에서 발생하는 충격으로부터 보호받게 될 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the risers market size was valued at USD 8.17 billion in 2025 and is estimated to grow from USD 8.86 billion in 2026 to reach USD 13.01 billion by 2031, at a CAGR of 7.99% during the forecast period (2026-2031).

This report is Segmented by Type (Flexible Risers, Rigid Risers, Hybrid Risers), Material (Steel, Composite, Thermoplastic Composite Pipe, Others), Deployment Depth (Shallow Water, Deepwater, Ultra-Deepwater), Application (Drilling, Production, Workover, Others), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Global Risers Market Trends and Insights

Revival of Deep and Ultra-Deepwater Project FIDs

ExxonMobil sanctioned USD 6.8 billion for Hammerhead in Guyana, with start-up set for 2029 and riser lengths 30%-40% above shallow-water norms, while Petrobras approved SEAP II, adding 120,000 barrels per day of pre-salt capacity that requires 24 steel catenary risers rated for 2,200-meter depths . The clustering of large-scale FIDs in Brazil and Guyana, which together hold 60% of sanctioned deepwater barrels to 2028, benefits integrated SURF contractors owning local yards. Early locking of EPC contracts at stable steel prices has insulated these developments from recent metallurgy cost swings, anchoring a multiyear floor under risers market demand.

Surge in SURF Package Awards in Brazil and Guyana

Subsea7 won a USD 1.4 billion Buzios 11 award covering 18 flexible risers, whereas TechnipFMC secured a USD 250-500 million Hammerhead scope that bundles rigid-riser supply with umbilicals. Average SURF packages now exceed USD 800 million because operators consolidate supply, installation, and integrity services under single tenders, transferring performance risk and compressing fabrication lead times. Mandatory 60% local sourcing on Petrobras projects drives competitive advantage toward contractors with Brazilian fabrication capacity, creating barriers for foreign pure-play fabricators.

Crude-Oil Price Volatility Impacting FID Timing

The International Energy Agency foresees a 1.5-2.5 million-barrel-per-day supply surplus in 2026, which could pressure Brent below USD 70 per barrel . Deepwater projects in Brazil and Guyana remain insulated with breakevens at USD 28-35, but marginal West African prospects face deferrals of six to 12 months, trimming near-term order flow for the risers market.

Other drivers and restraints analyzed in the detailed report include:

- Life-Extension Demand for Aging Shallow-Water Risers

- Rapid Adoption of Thermoplastic Composite Pipe Risers

- Escalating HSE and Environmental Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rigid designs will post an 8.7% CAGR, the fastest growth in the risers market, as operators replicate proven templates that compress engineering cycles and enable bulk sourcing. Shell's Gulf of Mexico brownfield program achieved 95% equipment commonality across three fields, trimming front-end engineering by 40%. Flexible risers still hold 45.3% of 2025 demand thanks to superior motion compliance, with TechnipFMC's Hammerhead order featuring electrically heated flexible lines to combat wax deposition. Hybrid concepts remain niche but vital in ultra-deepwater where top tension exceeds 1,000 tons, blending a seabed-anchored rigid section with a fatigue-resistant composite top string. The shift toward standardized rigid systems underpins procurement predictability, tilting market share toward contractors with high-capacity spoolbases.

Industry modularization also boosts aftermarket revenue: cataloged designs simplify spares stocking and streamline inspection protocols, lowering total cost of ownership. Nonetheless, flexible lines remain indispensable for complex tiebacks and life-extension programs where existing infrastructure dictates serpentine routing. Composite-steel hybrids are likely to proliferate as carbon-fiber tensile armor clears final qualification hurdles, offering weight savings that widen vessel choice and shrink installation windows in the risers market.

Composite alternatives will advance at 9.1% CAGR, eroding steel's 69.5% 2025 hold on the risers market size. Strohm's thermoplastic pipe is already moving beyond water-injection service toward full production duty with Petrobras in 2027. Magma Global targets high-temperature West African wells where steel would need costly active cooling. Field data show 77.7% weight reduction and comparable tensile capability, making composites attractive for reel-lay campaigns that cannot tolerate the deck loads of steel.

Regulatory acceptance removed the last barrier when DNV endorsed non-metallic risers for permanent service. Integrated fiber-optic sensing baked into the laminate turns each composite riser into a self-monitoring asset, obviating external instrumentation. Yet steel retains primacy in ultra-high-pressure sour service above 15,000 psi, where hydrogen embrittlement of polymer matrices is still a concern. Limited availability of reel-lay vessels and high initial material cost temper adoption speed, but the lifecycle economics remain compelling, ensuring composites capture incremental risers market share through the forecast period.

Geography Analysis

South America accounted for 35.7% of global demand in 2025 and will expand at an 8.4% CAGR, the fastest among all regions. Petrobras's SEAP II alone requires 24 risers rated for 10,000-psi pressures, while ExxonMobil's Hammerhead development in Guyana adds six production risers by 2029. Streamlined Brazilian permitting now cuts approval times to 12 months, and Guyana's USD 30 billion investment pipeline promises more than 40 new risers through 2028. The risers market benefits from predictable local-content rules that encourage regional fabrication and generate shorter logistics chains.

North America centers on brownfield optimization. Shell's Kaikias waterflood and multiple Gulf of Mexico refurbishments keep service demand elevated, while U.S. BOEM bonding changes lift up-front cost burdens. In Europe, the North Sea consolidates around super-operators; Shell and Equinor's Adura venture manages 140,000 boe/d under unified inspection programs that harvest economies of scale. UK carbon-capture regulations, effective in 2026, compel feasibility studies on new developments, tying future FIDs to integrated CCS concepts.

The Middle East and Asia-Pacific emerge as secondary poles. ADNOC's SARB Deep Gas and Nasr-115 expansions add corrosion-resistant alloy risers for sour-gas production, while CNOOC ramps up South China Sea activity with rigid strings at Kaiping 18-1. Southeast Asia lags due to price uncertainty and financing constraints, but Malaysia and Indonesia remain incremental contributors. Combined, these trends diversify the geographic revenue mix and insulate the global risers market from single-basin shocks.

- TechnipFMC

- Aker Solutions

- Subsea 7

- NOV Inc.

- Saipem

- Baker Hughes (OneSubsea)

- McDermott International

- Oceaneering International

- Vallourec

- Oil States Industries

- Prysmian Group

- Airborne Oil & Gas

- Shawcor

- Trelleborg Offshore

- Ocyan

- MODEC

- Kongsberg Maritime

- DeepOcean

- Sapura Energy

- Bourbon Offshore

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Revival of deep- & ultra-deepwater project FIDs

- 4.2.2 Surge in SURF package awards in Brazil & Guyana

- 4.2.3 Life-extension demand for ageing shallow-water risers

- 4.2.4 Rapid adoption of thermoplastic composite pipe (TCP) risers

- 4.2.5 CCS retrofit opportunities for offshore riser infrastructure

- 4.2.6 AI-enabled digital twins for predictive riser integrity

- 4.3 Market Restraints

- 4.3.1 Crude-oil price volatility impacting FID timing

- 4.3.2 Escalating HSE & environmental compliance costs

- 4.3.3 Scarcity of deepwater fatigue-analysis specialists

- 4.3.4 Long-lead forgings & metallurgy supply-chain bottlenecks

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Flexible Risers

- 5.1.2 Rigid Risers

- 5.1.3 Hybrid Risers

- 5.2 By Material

- 5.2.1 Steel

- 5.2.2 Composite

- 5.2.3 Thermoplastic Composite Pipe

- 5.2.4 Others

- 5.3 By Deployment Depth

- 5.3.1 Shallow Water (Up to 500 m)

- 5.3.2 Deepwater (500 to 1,500 m)

- 5.3.3 Ultra-Deepwater (Above 1,500 m)

- 5.4 By Application

- 5.4.1 Drilling

- 5.4.2 Production

- 5.4.3 Workover

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 NORDIC Countries

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN Countries

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 TechnipFMC

- 6.4.2 Aker Solutions

- 6.4.3 Subsea 7

- 6.4.4 NOV Inc.

- 6.4.5 Saipem

- 6.4.6 Baker Hughes (OneSubsea)

- 6.4.7 McDermott International

- 6.4.8 Oceaneering International

- 6.4.9 Vallourec

- 6.4.10 Oil States Industries

- 6.4.11 Prysmian Group

- 6.4.12 Airborne Oil & Gas

- 6.4.13 Shawcor

- 6.4.14 Trelleborg Offshore

- 6.4.15 Ocyan

- 6.4.16 MODEC

- 6.4.17 Kongsberg Maritime

- 6.4.18 DeepOcean

- 6.4.19 Sapura Energy

- 6.4.20 Bourbon Offshore

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment