|

시장보고서

상품코드

2063243

주택용 발전기 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Residential Generators - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

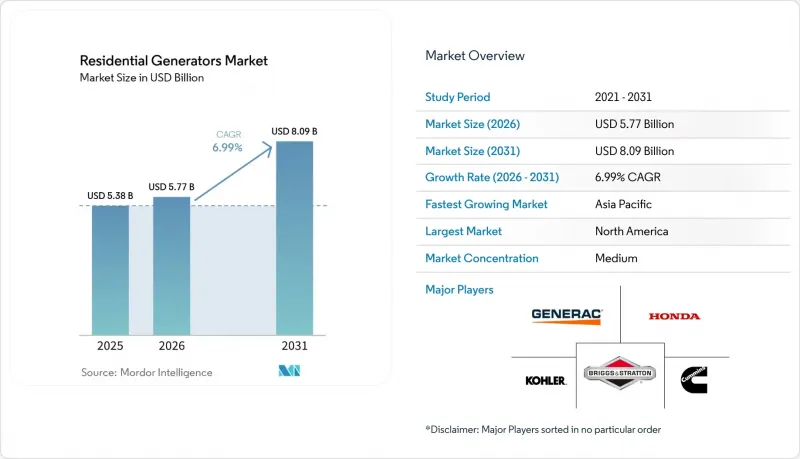

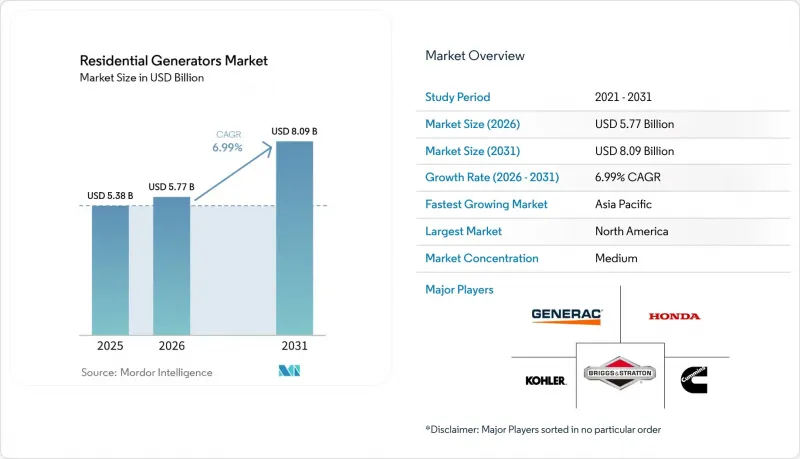

Mordor Intelligence에 의하면, 주택용 발전기 시장 규모는 2025년에 53억 8,000만 달러로 평가되었습니다. 2026년 57억 7,000만 달러에서 2031년까지 80억 9,000만 달러에 이르고 예측 기간(2026-2031년) CAGR은 6.99%를 나타낼 전망입니다.

본 보고서는 연료 유형(디젤 등), 출력(3kW 미만 등), 상수(단상, 3상), 유형(휴대용, 대기용, 인버터), 기술(기존, 인버터, 하이브리드), 용도(비상용 백업 등), 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 단위로 제시되어 있습니다.

세계의 주택용 발전기 시장 동향과 인사이트

기상 이변으로 인한 정전 발생 빈도 증가

2000년부터 2023년까지 미국의 정전 사고 중 80.1%는 격렬한 폭풍으로 인해 발생했으며, 2022년에 발생한 주요 정전 사고의 평균 지속 시간은 229분이었습니다. 이는 10년 전의 일반적인 복구 시간의 2배에 해당합니다. 2025년에는 전 세계적으로 유사한 경향이 나타났으며, 칠레의 전국적 정전과 이라크의 폭염으로 인한 정전은 복합적인 기후 스트레스 요인이 이미 용량 한계에 근접해 가동되고 있는 송전망을 어떻게 붕괴시키는지를 여실히 보여주었습니다. 카운티 단위 조사에 따르면, 기온이 32.2℃를 넘는 날에 바람이나 비가 겹치면 정전 건수가 급증하는 것으로 확인되었으며, 캘리포니아주, 텍사스주 및 남동부 지역의 가정에서는 며칠 동안 지속되는 정전에도 대응할 수 있는 자동 가동형 솔루션에 대한 수요가 높아지고 있습니다. 냉장고, 공조 시스템, 통신 기기 등이 모두 필수 불가결한 요소로 자리 잡은 가운데, 구매자들은 가동 시간이 길고 원격 모니터링 기능을 갖춘 대기형 또는 하이브리드형 발전기를 점점 더 많이 선택하고 있습니다. 그 결과, 백업 전원이 주택 복원력 계획의 핵심 요소로 자리 잡으면서 주택용 발전기 시장은 지속적인 성장세를 보이고 있습니다.

노후화된 송배전 인프라

현재 미국의 송전선 및 대형 변압기의 약 70%가 가동 개시 후 25년이 넘었습니다. 이 내구 연수 범위는 극한 기온 조건에서 고장률 증가와 상관관계가 있습니다. 2025년에 4,800억 달러, 2035년까지 5조 8,000억 달러를 투입하는 계획적인 송전망 강화 투자를 통해 궁극적으로는 부하가 완화될 전망이지만, 인허가 지연이나 인력 부족으로 인해 완공 시기가 늦어짐에 따라 향후 10년 동안, 주택 소유자들은 위험에 노출된 상태로 남게 될 것입니다. 북미의 신뢰성 평가에 따르면, 이미 23개 지역 중 13개 지역에서 위험이 높아지고 있는 것으로 지적되고 있으며, 전력 회사가 투자를 하더라도 예비 발전 설비에 대한 수요는 계속되고 있습니다. 서유럽에서도 이와 유사한 설비 교체 지연 현상이 나타나고 있으며, 그곳에서는 노후화된 인프라와 증가하는 전력 수요가 맞닥뜨리고 있습니다. 그 결과, 주택용 발전기 시장은 장기적인 명확한 수요 전망의 혜택을 누리고 있으며, 제조업체들은 판매망, 자금 조달 옵션, 하이브리드 제품 라인 확대를 추진하고 있습니다.

소형 엔진 배기가스 규제 강화

EPA Tier 2, 캘리포니아주의 소형 오프로드 엔진 규제 및 EU Stage V 기준에 따르면, 입자상 물질 필터, 촉매 환원 장치, 첨단 분사 시스템의 장착이 의무화되어 있으며, 20kW 미만의 세트의 경우 부품 원가가 15-20% 증가합니다. 콜러(Kohler)와 같은 공급업체들은 규제 기준이 강화되는 상황에서도 시장 접근성을 유지하기 위해 수소 및 HVO 대응 제품을 통해 리스크 헤지를 도모하고 있습니다. 규제 준수 비용은 휴대용 및 보급형 비상 발전기 모델에 가장 큰 타격을 주고 있으며, 이로 인해 이익률이 압박받고, 구매자들은 연소 제한을 피할 수 있는 저소음 인버터식이나 배터리식 솔루션으로 눈을 돌리고 있습니다. 규제로 인한 영향은 중간 정도이지만 지속적이며, 주택용 발전기 시장의 예상 연평균 성장률(CAGR)을 0.8포인트 끌어내리고 있습니다.

부문별 분석

2025년, 천연가스 발전기는 파이프라인 구축 현황, 자동 시동의 용이성, 그리고 kWh당 낮은 연료비를 바탕으로 주택용 발전기 시장 점유율의 34.8%를 차지했습니다. 온타리오주와 미국의 선벨트 지역에서 지속적으로 진행되고 있는 송전망 확장은 대상 고객 기반을 확대하고, 꾸준한 판매량을 뒷받침하고 있습니다. 주택용 발전기 시장에서 천연가스식 세트 시장 규모는 설치 방식이 수동 전환 스위치에서 건물 전체를 아우르는 완전 자동화 시스템으로 전환됨에 따라 2031년까지 32억 달러에 달할 것으로 전망됩니다. 한편, 태양광·배터리 하이브리드는 연평균 성장률(CAGR) 11.0%로 성장을 지속하고, 있으며, 보조금에 따른 경제성과 저소음 운전을 강점으로 삼아 소음에 민감한 도시 지역 구매자들의 관심을 끌고 있습니다. 디젤 발전기는 며칠간의 자급 전원이 필요한 지방의 Off-grid 시설에서 여전히 중요한 역할을 하고 있지만, 배기가스 규제에 대응함에 따라 시스템 비용이 증가하고 있습니다. 가솔린식 휴대용 발전기는 여전히 초보자를 대상으로 한 틈새 시장에 머물러 있지만, 더 안전하게 보관할 수 있고 청정하게 작동하는 LPG 듀얼 연료 모델에 시장 점유율을 빼앗기고 있습니다. 듀얼 연료 및 트리플 연료 기능을 모두 갖춘 제품을 출시하는 제조업체는 겨울철 파이프라인 압력이 떨어질 가능성이 있다는 점을 신뢰성 기관으로부터 지적받고 있는 인프라가 혼재된 시장을 가장 효과적으로 공략할 수 있습니다.

재생에너지의 도입이 미래의 선호도를 좌우합니다. 지붕 위 태양광 발전 보급률이 20% 이상의 지역에서는 낮 동안 자체 충전을 하고, 배터리를 이용해 저녁 시간대의 피크 수요를 감당하는 하이브리드 방식에 대한 의존도가 높아지고 있습니다. 반면, 천연가스망이 잘 갖춰진 교외 지역에서는 공조 설비나 전기차 충전기의 부하에 맞춘 용량의 연료식 비상 발전 세트가 선호되고 있습니다. 따라서 전략적 포지셔닝은 브랜드화된 생태계 내에서 제로 에미션과 듀얼 연료라는 두 가지 선택지를 모두 제공하는 데 초점을 맞추고, 정책 및 가격 동향의 변화에 따라 고객이 모듈을 추가하거나 교체할 수 있도록 하는 것입니다.

시장 점유율 42.1%를 차지하는 3-10kW급 발전기는 냉장고, HVAC 송풍기, 조명, 재택근무용 전자기기를 위한 주류 선택지로 자리 잡고 있습니다. kW당 설치 비용과 설치 면적이 단독주택에 적합하기 때문에 하이브리드형이 부상하고 있는 상황에서도 출하량은 높은 수준을 유지하고 있습니다. 이 출력 대역과 관련된 주택용 발전기 시장 규모는 2031년까지 35억 달러에 달할 것으로 예상되지만, 대형 주택 및 전기차 충전의 보급에 따른 업그레이드 수요로 인해 시장 점유율은 소폭 하락할 전망입니다. 10-20kW 대역은 연평균 성장률(CAGR) 7.7%로 가장 빠르게 성장하고 있으며, 이는 레벨 2 충전기의 보급과 전기 히트펌프의 채택 확대를 반영한 것입니다. 3kW 미만의 휴대용 전원 장치는 캠핑이나 테일게이트 파티의 요구를 충족시켜 주는 소음이 적고 실내에서도 사용할 수 있는 배터리 덕분에 소형 가솔린 발전기 수요를 잠식하고 있습니다. 20kW를 초과하는 기종은 여전히 틈새 시장인 고급 주택, 농장, 소규모 사업장에 주로 사용되지만, V2G(Vehicle-to-Grid) 규정에 따라 높은 설비 투자 비용을 상쇄할 수 있는 전력 판매 수익이 인정된다면 시장 규모가 확대될 가능성이 있습니다.

용량 계획에서는 평균 소비 전력이 아니라 히트 펌프나 전기차 충전기의 피크 시간대 가동 부하가 점점 더 중요시되면서, 가정에서는 더 대용량인 기종을 선택하는 경향이 강해지고 있습니다. 각 제조업체들은 가전제품을 동적으로 조절하는 부하 관리 모듈을 강조하고 있으며, 이를 통해 10kW 발전기로 15kW의 연결 부하를 순차적으로 가동할 수 있게 되어, 비용을 절감하면서도 최적의 운영 범위를 확대할 수 있습니다.

지역별 분석

북미는 2025년 매출의 37.0%를 차지했으며, 이러한 선도적 지위는 성숙한 천연가스 네트워크, 비상 설비 설치 허가 절차의 간소화, 그리고 인증된 백업 시스템과 연계된 보험 할인에 힘입어 유지되고 있습니다. 지속적인 허리케인, 산불, 얼음 폭풍의 발생으로 인해 소비자들의 관심은 높은 수준을 유지하고 있습니다. 캐나다 온타리오주에서 엠브리지(Embridge)사의 확장 사업으로 인해 파이프라인의 서비스 범위가 확대되고, 2027년까지 2,200가구의 농촌 가정이 가스식 비상전원을 이용할 수 있게 됨에 따라 주택용 발전기 시장이 확대될 전망입니다. 멕시코에서는 저소득 지역에서 휴대용 발전기가 주류를 이루고 있기 때문에 매출 증가세보다 설치 대수 증가세가 더 빠릅니다. 2035년까지의 정전 위험 평가에 따르면, MISO, PJM, ERCOT, WECC에서 자원의 적정 공급량이 부족해질 것으로 지적되고 있으며, 이는 수요의 장기적인 증가를 시사하고 있습니다.

연평균 성장률(CAGR) 8.5%로 가장 빠르게 성장하고 있는 아시아태평양에서는 국가별 상황이 크게 다릅니다. 인도의 지방 도시에서는 잦은 정전이 발생하고 있으며, 이로 인해 휴대용 발전기의 보급이 확대되고 있습니다. 혼다가 2026년에 시작할 UPS 임대 사업은 이처럼 합리적인 가격을 중시하는 틈새 시장을 공략하는 것입니다. 일본의 태풍 시즌과 송전망 노후화로 인해 대기 수요가 증가하는 반면, 호주의 사이클론 벨트 지역에서는 듀얼 연료식 휴대용 발전기의 판매가 늘고 있습니다. 중국 본토에서는 농촌 지역의 전력 공급 격차로 인해 여전히 매주 정전이 발생하고 있으며, 저가형 가솔린 발전기의 판매량이 꾸준히 유지되고 있습니다. 인도네시아와 필리핀에서는 허가 및 인가 절차의 장벽과 연료 물류 문제로 인해 비상용 발전기의 보급이 더딘 편이지만, 인구 밀도가 높은 도시 지역 중 소음 규제가 적용되는 곳에서는 인버터식 휴대용 발전기 시장 점유율이 확대되고 있습니다.

유럽에서는 재생에너지의 간헐성이 심화되는 가운데, 엄격한 배출 규제와 정전 위험 증가가 겹치고 있습니다. EU 스테이지 V 규제에 대응하기 위한 비용 때문에 구매자들은 인버터식이나 하이브리드식 발전기를 선택하는 경향이 있으며, 지자체의 소음 규제로 인해 60dBA 미만의 기기가 선호되고 있습니다. 2025년 아일랜드의 송전망에 피해를 입힌 폭풍 ‘에오윈’은 아무리 첨단 송전망이라 해도 취약할 수 있음을 보여주었습니다. 독일, 이탈리아, 스페인에서는 태양광 발전과 축전지를 결합한 하이브리드 시스템을 장려하기 위해 유리한 고정가격임베디드제도(FIT)가 도입되어, 단시간 동안 발전기 수요를 압박하고 있습니다. 남미에서는 브라질과 아르헨티나에 수요가 집중되어 있지만, 경제의 변동성으로 인해 고급 제품의 판매는 주춤하고 있습니다. 중동에서는 전력망이 불안정한 지역에서 디젤 발전이 주전원으로 활용되고 있으며, 레바논에서 디젤 발전의 점유율이 80%에 달한다는 사실이 이를 뒷받침하고 있습니다. 또한 소득 수준이 높기 때문에 발전기 출하 대수는 상당한 규모를 유지하고 있습니다. 사하라 이남 아프리카에서 연간 250만 대의 휴대용 전원 장치가 판매된 것은 송전망 구축이 도시화 속도를 따라가지 못하고 있음을 반영하는 것으로, 남아프리카공화국에서는 2023년에 200일 동안 계획 정전이 발생했습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the residential generators market size was valued at USD 5.38 billion in 2025 and is estimated to grow from USD 5.77 billion in 2026 to reach USD 8.09 billion by 2031, at a CAGR of 6.99% during the forecast period (2026-2031).

This report is Segmented by Fuel Type (Diesel, and More), Power Rating (Below 3 KW, and More), Phase (Single-Phase, Three-Phase), Type (Portable, Standby, Inverter), Technology (Conventional, Inverter, Hybrid), Application (Emergency Backup, and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). Market Forecasts are Provided in Value (USD).

Global Residential Generators Market Trends and Insights

Growing frequency of extreme-weather-related outages

Severe storms generated 80.1% of U.S. power interruptions between 2000 and 2023, and the average major event lasted 229 minutes in 2022, double the restoration windows common a decade earlier . Similar patterns emerged worldwide in 2025 when Chile's nationwide outage and Iraq's heat-wave blackout underscored how compound climate stressors topple grids already operating near capacity. County-level studies confirm that days above 32.2 °C combined with wind or precipitation sharply elevate outage counts, pushing households in California, Texas, and the Southeast toward automatic-start solutions that can cover multi-day disruptions. As refrigerators, HVAC systems, and connectivity equipment all become mission-critical, buyers increasingly select standby or hybrid units featuring long runtime and remote monitoring. The outcome is a sustained uplift in the Residential generators market as backup power becomes a core element of household resilience planning.

Aging transmission & distribution infrastructure

Roughly 70% of U.S. transmission lines and large transformers now exceed 25 years of service, a lifespan bracket correlated with higher failure rates during extreme temperatures . Planned grid-hardening investments of USD 480 billion in 2025 and USD 5.8 trillion through 2035 will ease the strain eventually, but permitting delays and labor shortages stretch completion timelines, leaving homeowners exposed for the next decade. North American reliability assessments already flag 13 of 23 regions at elevated risk, so demand for backup generation persists even as utilities invest. Similar replacement lags characterize Western Europe, where legacy infrastructure meets rising electrification loads. Consequently, the Residential generators market benefits from a long, visible demand horizon that encourages manufacturers to expand dealer networks, financing options, and hybrid product lines.

Tightening small-engine emission limits

EPA Tier 2, California's small off-road engine rules, and EU Stage V standards demand particulate filters, catalytic reduction, and advanced injection systems that add 15-20% to the bill of materials for sub-20 kW sets . Vendors such as Kohler hedge with hydrogen-compatible and HVO-ready products to preserve market access as thresholds tighten. Compliance costs hit portable and entry-level standby models hardest, compressing margins and nudging buyers toward quieter inverter or battery solutions that sidestep combustion limits. The regulatory drag is moderate yet persistent, shaving 0.8 percentage points off forecast CAGR in the Residential generators market.

Other drivers and restraints analyzed in the detailed report include:

- Hybrid Solar-Storage-Generator Resilience Packages

- Work-from-Anywhere Surge in Home Critical Electronics

- Falling Lithium-Ion Home-Battery Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Natural-gas units accounted for 34.8% Residential generators market share in 2025 on the back of pipeline availability, automatic-start ease, and lower fuel cost per kWh. Ongoing grid expansions in Ontario and the U.S. Sun Belt widen the addressable base, supporting steady volume. The Residential generators market size for natural-gas sets is projected to reach USD 3.2 billion by 2031 as installations migrate from manual transfer switches to fully automated whole-home coverage. Meanwhile, solar-battery hybrids log an 11.0% CAGR, luring urban, noise-sensitive buyers with rebate-driven economics and silent operation. Diesel remains relevant for rural, off-grid properties requiring multi-day autonomy, but emission compliance raises system cost. Gasoline portables cling to entry-level niches yet lose share to dual-fuel LPG models that store safer and run cleaner. Manufacturers hedging across dual- and tri-fuel capabilities best capture mixed-infrastructure markets flagged by reliability agencies where winter pipeline pressure can drop.

Renewables adoption steers future preferences. Regions crossing 20% rooftop solar penetration lean heavily toward hybrids that self-charge daily and ride through evening peaks on batteries. In contrast, suburban tracts with mature natural-gas grids prefer fuel-based standby sets sized for HVAC and EV-charger loads. Strategic positioning, therefore, revolves around offering both zero-emission and dual-fuel pathways inside branded ecosystems so customers can add or swap modules as policy or price signals evolve.

With 42.1% share, 3-10 kW generators represent the mainstream choice for refrigerators, HVAC blowers, lighting, and home-office electronics. Their installed cost per kW and footprint suit single-family dwellings, keeping shipment volume high even as hybrids gain ground. The Residential generators market size tied to this band is forecast to climb to USD 3.5 billion by 2031, though share inches down as larger homes and EV charging drive upgrades. The 10-20 kW bracket grows fastest at 7.7% CAGR, reflecting Level 2 charger prevalence and rising adoption of electric heat pumps. Portable power stations under 3 kW eat into small gasoline generator demand thanks to silent, indoor-safe batteries that meet camping and tailgating needs. Units above 20 kW remain niche-luxury estates, farms, and small businesses-but could scale if vehicle-to-grid rules allow export revenues that offset higher capex.

Capacity planning increasingly accounts for peak-start loads of heat pumps and EV chargers rather than average draw, nudging households to size up. Manufacturers emphasize load-management modules that orchestrate appliances dynamically, letting a 10 kW generator run a 15 kW connected load sequentially, stretching the sweet spot while containing costs.

Geography Analysis

North America anchored 37.0% of 2025 revenue, a leadership position sustained by mature natural-gas grids, streamlined permitting for standby installations, and insurance discounts tied to certified backup systems. Chronic hurricane, wildfire, and ice-storm activity keeps consumer awareness high. Canada's Enbridge expansions in Ontario broaden pipeline coverage and enlarge the Residential generators market as gas standbys become feasible for another 2,200 rural homes by 2027. Mexico shows faster unit growth than revenue growth because portable sets dominate in lower-income regions. Outage-risk assessments through 2035 flag resource adequacy shortfalls in MISO, PJM, ERCOT, and WECC, pointing to a long demand runway.

Asia-Pacific, the quickest riser at an 8.5% CAGR, features highly varied national profiles. India's tier-2 cities endure frequent blackouts, boosting portable uptake; Honda's 2026 UPS leasing rollout captures this affordability-focused niche. Japan's typhoon seasons and aging grid elevate standby demand, while Australia's cyclone belt fuels dual-fuel portable sales. Mainland China's rural electrification gaps still prompt weekly outages, sustaining low-price gasoline generator volume. Permitting hurdles and fuel-logistics issues slow standby penetration in Indonesia and the Philippines, but inverter portables gain share where noise limits apply in dense urban areas.

Europe blends strict emission policies with growing outage risk as renewable intermittency rises. EU Stage V compliance costs push buyers toward inverter and hybrid sets, and municipal sound ordinances drive less than 60 dBA equipment preference. Storm Eowyn's 2025 damage to Ireland's network showed that even advanced grids remain vulnerable. Germany, Italy, and Spain use generous feed-in tariffs to promote solar-battery hybrids, eating into short-duration generator demand. South America clusters demand in Brazil and Argentina, though economic volatility caps high-end sales. The Middle East relies on diesel prime power where grids falter, evidenced by Lebanon's 80% diesel share, yet income levels support sizeable unit shipments. Sub-Saharan Africa's 2.5 million annual portable sales reflect urbanization outpacing grid build-out, with South Africa recording 200 load-shedding days in 2023.

- Generac Holdings Inc.

- Kohler Co.

- Briggs & Stratton Corp.

- Cummins Inc.

- Honda Motor Co., Ltd.

- Atlas Copco AB

- Caterpillar Inc.

- Yamaha Motor Co., Ltd.

- Champion Power Equipment Inc.

- Wacker Neuson SE

- Honeywell (Home Standby Licensing)

- Westinghouse Electric Corp.

- Hyundai Power Products

- FG Wilson (Caterpillar)

- DEUTZ AG

- Wartsila Corp.

- Rolls-Royce plc (MTU Power Systems)

- Siemens Energy AG

- PRAMAC Group

- Ingersoll Rand Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing frequency of extreme-weather-related outages

- 4.2.2 Aging transmission & distribution infrastructure

- 4.2.3 Expansion of residential natural-gas grids

- 4.2.4 "Work-from-anywhere" surge in home load-critical electronics

- 4.2.5 Hybrid solar-storage-generator resilience packages

- 4.2.6 Grid-cybersecurity breach concerns among homeowners

- 4.3 Market Restraints

- 4.3.1 Tightening small-engine emission limits (EU Stage V, CARB)

- 4.3.2 Municipal noise / zoning restrictions

- 4.3.3 Falling Li-ion home-battery costs

- 4.3.4 Insurance rebates favouring zero-emission backup

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Fuel Type

- 5.1.1 Diesel

- 5.1.2 Natural Gas

- 5.1.3 Gasoline

- 5.1.4 Solar-Battery Hybrid

- 5.1.5 Others

- 5.2 By Power Rating

- 5.2.1 Below 3 kW

- 5.2.2 3 to 10 kW

- 5.2.3 10 to 20 kW

- 5.2.4 Above 20 kW

- 5.3 By Phase

- 5.3.1 Single-Phase

- 5.3.2 Three-Phase

- 5.4 By Type

- 5.4.1 Portable Generators

- 5.4.2 Standby Generators

- 5.4.3 Inverter Generators

- 5.5 By Technology

- 5.5.1 Conventional

- 5.5.2 Inverter

- 5.5.3 Hybrid

- 5.6 By Application

- 5.6.1 Emergency Backup

- 5.6.2 Prime/Continuous

- 5.6.3 Recreational / Outdoor

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 NORDIC Countries

- 5.7.2.6 Russia

- 5.7.2.7 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 ASEAN Countries

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 South America

- 5.7.4.1 Brazil

- 5.7.4.2 Argentina

- 5.7.4.3 Rest of South America

- 5.7.5 Middle East and Africa

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 South Africa

- 5.7.5.4 Egypt

- 5.7.5.5 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Generac Holdings Inc.

- 6.4.2 Kohler Co.

- 6.4.3 Briggs & Stratton Corp.

- 6.4.4 Cummins Inc.

- 6.4.5 Honda Motor Co., Ltd.

- 6.4.6 Atlas Copco AB

- 6.4.7 Caterpillar Inc.

- 6.4.8 Yamaha Motor Co., Ltd.

- 6.4.9 Champion Power Equipment Inc.

- 6.4.10 Wacker Neuson SE

- 6.4.11 Honeywell (Home Standby Licensing)

- 6.4.12 Westinghouse Electric Corp.

- 6.4.13 Hyundai Power Products

- 6.4.14 FG Wilson (Caterpillar)

- 6.4.15 DEUTZ AG

- 6.4.16 Wartsila Corp.

- 6.4.17 Rolls-Royce plc (MTU Power Systems)

- 6.4.18 Siemens Energy AG

- 6.4.19 PRAMAC Group

- 6.4.20 Ingersoll Rand Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment