|

시장보고서

상품코드

2063245

태양광 일조량 제어 시스템 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Solar Sunlight Control System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

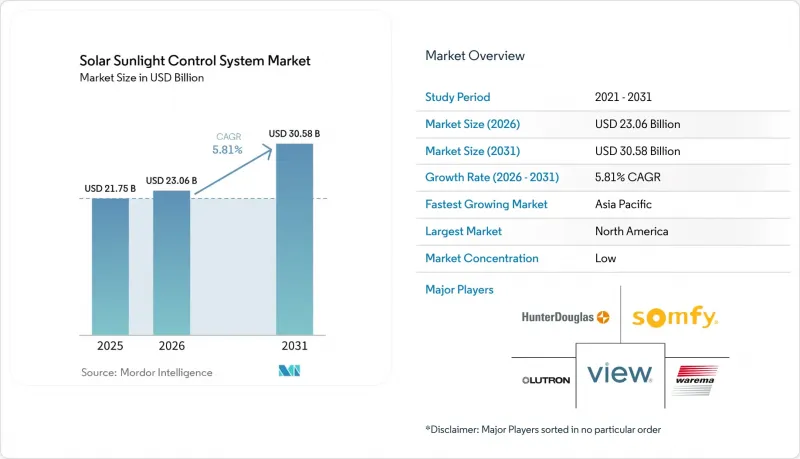

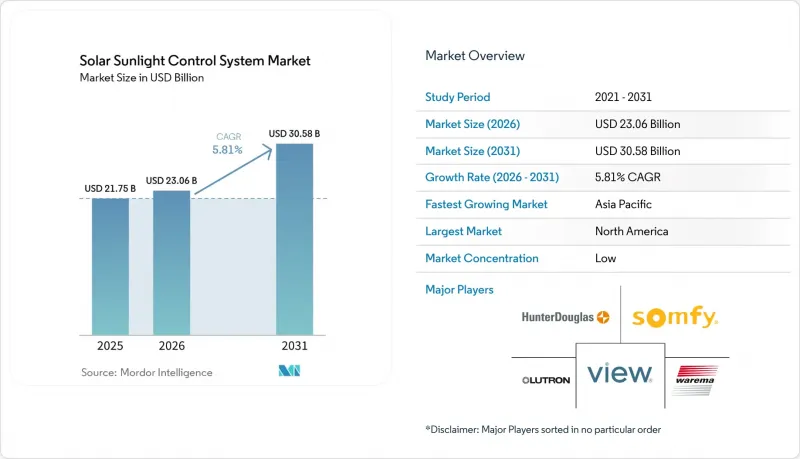

Mordor Intelligence에 의하면, 태양광 일조량 제어 시스템 시장 규모는 2025년에 217억 5,000만 달러로 평가되었습니다. 2026년 230억 6,000만 달러에서 2031년까지 305억 8,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 5.81%를 나타낼 전망입니다.

본 보고서는 제품 유형(수동식 태양광 일조량 제어 시스템 등), 기술(광전 센서 등), 구성 요소(액추에이터 등), 설치 유형(신규 설치 및 개조 설치), 용도(주거용 등) 및 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 태양광 일조량 제어 시스템 시장 동향 및 인사이트

더욱 엄격해진 친환경 건축물의 에너지 기준으로 인해, 채광 및 외관의 성능 요건이 높아지고 있습니다.

현재 전 세계의 건축 규제에는 채광 지표와 일사열 획득량의 상한선이 포함되어 있어, 실질적으로 동적 차광 및 일렉트로크로믹 유리의 사용이 의무화되어 있습니다. ASHRAE 90.1-2022에서는 가시광선 투과율의 기준치가 상향 조정된 반면, EU의 건축물 에너지 성능 지침(개정판)에서는 개보수 목표가 두 배로 늘어났으며, 자동 차광 장치가 각국의 건축 기준에 반영되고 있습니다. 중국의 GB/T 50378-2019 표준에서는 지능형 일사 제어 기능을 갖춘 프로젝트를 높이 평가하고 있기 때문에 일사 제어 시스템 시장은 단순한 선택적 업그레이드가 아닌 설계상의 핵심 고려 사항으로 자리 잡아가고 있습니다.

웰니스와 에너지 절약을 위한 상업용 부동산의 다이내믹 글레이징 전환

다이나믹 글레이징이 블라인드를 대체함에 따라, 집주인들로부터 임대료 인상이나 입주율 조기 달성 사례가 보고되고 있습니다. GREYSTAR사의 ‘Exo Apartments’에서는 View사의 스마트 창문을 도입한 후, 입주율 100% 달성까지 걸리는 기간이 80% 단축되었으며, 눈부심 없는 자연광이 입주자들의 만족도를 높이는 요인이 되었습니다. Kilroy Realty사는 View사의 네트워크 기반 플랫폼을 활용하여 소유 부동산 전체의 연간 에너지 비용을 100만 달러 절감했습니다. 생고방이 2025년에 출시한, 4개의 조광 구역을 갖춘 ‘SageGlass RealTone’은 거주자들이 원하는 시야의 선명도를 충족시켜, 도입을 더욱 촉진하고 있습니다.

스마트 유리와 전동 블라인드의 높은 초기 비용

일렉트로크로믹 유리는 일반 Low-E 유리에 비해 15%-25% 정도 비싸기 때문에 파사드 예산에 평방피트당 50-150달러가 추가되어 중저가 프로젝트의 추진을 저해하고 있습니다. 전동 쉐이드는 창문 하나당 300-800달러가 드는 반면, 수동 블라인드는 50-150달러에 불과하기 때문에 동남아시아나 남미의 개발업자들은 비용 절감을 위해 설계 단계에서부터 이를 제외하는 추세입니다. 총소유비용(TCO) 모델에서는 5-10년 내에 투자 회수가 가능하지만, 초기 비용에 대한 민감도가 여전히 걸림돌로 작용하고 있습니다.

부문별 분석

2025년 매출액 중 자동 차광 시스템이 45.3%를 차지하며, 전동화가 조기에 주류로 자리 잡을 것임을 보여주었습니다. 한편, 스마트 제어 시스템은 2031년까지 연평균 성장률(CAGR) 12.0%로 확대될 것으로 예상되며, 이는 태양광 일조량 제어 시스템 시장 전체의 성장 속도의 2배 이상에 해당합니다. 현재 구매자들은 단순한 작동 기능뿐만 아니라 예측 인텔리전스를 바탕으로 가치를 판단하고 있으며, 스마트 제품군에는 클라우드 분석, AI 알고리즘, SaaS 과금을 가능하게 하는 오픈 API가 탑재되어 있습니다. 그 결과, 기존의 수동식 제품은 가격에 민감한 개보수 공사나 전력 공급이 불안정한 지역에서만 여전히 수요가 있습니다.

스마트 플랫폼은 연간 소프트웨어 요금 증가율이 하드웨어 비용 감소율을 상회함에 따라, 매출총이익률 구조도 변화시키고 있습니다. 예를 들어, Lutron사의 ‘Athena’ 클라우드 서비스는 제곱피트 단위의 구독 요금을 책정하고 있으며, 그 금액은 해당 회사의 모터 상각 원가를 상회하고 있습니다. 이는 미래 이익의 기반이 기계적인 요소가 아니라 분석 기능이라는 점을 여실히 보여주고 있습니다. 프로젝트 사양에서 BACnet, Matter 또는 Bluetooth Mesh와의 호환성이 점점 더 요구되는 가운데, 스마트 제어 업체들은 상호 운용성과 사이버 보안 보장 측면에서 우위를 점하고 있습니다.

광전식 센서는 접근성이 뛰어나고 부품 원가(BOM)가 저렴하다는 점 덕분에 2025년 매출의 40.0%를 차지했으나, 건물 소유주들이 단일 기기로 열 부하 데이터와 재실 데이터를 요구하게 됨에 따라, 적외선 센서는 2031년까지 연평균 성장률(CAGR) 11.1%를 나타낼 것으로 보입니다. 2025년 IEEE 현장 시험에서 LoRa 기반 적외선 노드는 99.2%의 네트워크 가동률을 유지하면서 배터리 수명을 80% 연장하는 것으로 나타났으며, 이는 과거 무선 기술 도입을 제한했던 유지보수 관련 우려를 직접적으로 해소했습니다.

또한, 적외선 어레이는 실시간 히트맵 데이터를 AI 엔진으로 전송하여, 이용자가 불편함을 느끼기 몇 초 전에 차양 조절이 가능하도록 합니다. 따라서 열 센서 번들은 HVAC(냉난방 및 공조) 시스템의 부하 급증을 억제합니다. 이것이 바로 생명과학 연구소나 데이터센터가 대당 10%의 할증 가격이 있음에도 불구하고 이를 채택하고 있는 이유입니다. Matter나 Zigbee 3.0과 같은 무선 프로토콜은 실리콘 수준에서 보안 키를 내장하고 있기 때문에 구매자들은 무선 기술의 신뢰성을 인정하게 되었고, 이로 인해 유선 광전 루프 시장 점유율을 더욱 잠식하고 있습니다.

지역별 분석

북미는 2025년 매출의 33.4%를 차지했으며, IRA(인플레이션 억제법)에 따른 30%-50%의 투자 세액 공제 덕분에 일렉트로크로믹 유리(변색 유리)가 주류 사양으로 자리 잡았습니다. 캘리포니아주와 뉴욕주에서 시행되고 있는 엄격한 주 차원의 건축 기준은 태양열 획득량의 상한선을 매년 더욱 강화하고 있으며, 이에 따라 태양광 일조량 제어 시스템 시장은 의무화된 성능 기준에 따라 성장을 이어가고 있습니다. 2032년까지의 세제 안정성은 보다 장기적인 개발 파이프라인을 촉진하고 있으며, 풍부한 스마트 빌딩 전문 지식이 리모델링 공사의 전환을 가속화하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 6.7%를 기록하며, 지역별로는 가장 빠른 성장세를 보일 전망입니다. 이는 중국, 인도 및 아세안(ASEAN) 국가들이 건축 허가 기준에 채광 기준을 포함하고 있기 때문입니다. 중국의 GB/T 50378-2019 규격은 지능형 차광 기능을 갖춘 프로젝트에 최고 등급을 부여하고 있으며, 대형 개발사들은 더 높은 임대료를 확보하기 위해 이 인증 취득을 목표로 하고 있습니다. 인도에서는 2024년에 개정된 ‘에너지 절약 건축 기준’에 따라, 고온 건조 지역의 신축 사무실에 대해 일사열 획득률을 0.25 미만으로 억제해야 할 의무가 부과되어, 사실상 다이내믹 글레이징의 도입이 필수화되었습니다. 도시화가 진행되고 초고층 빌딩의 수가 늘어남에 따라, 자동화된 파사드 솔루션은 필수적인 요소가 되고 있습니다.

유럽에서는 2030년까지 대규모 개보수 비율을 두 배로 늘리는 것을 목표로 하는 ‘리노베이션 웨이브’ 이니셔티브가 추진되고 있습니다. 상고반의 ‘스마트 캠퍼스 보르도’와 같은 프로젝트는 일렉트로크로믹 기술의 확장성을 보여주고 있으며, 한편 인건비 상승으로 인해 수동식 블라인드보다 자동화 방식이 비용 대비 효과가 더 높아지고 있습니다. 라틴아메리카와 중동은 세계 평균에는 미치지 못하지만, 여전히 한 자릿수 중반대의 성장률을 유지하고 있습니다. 사우디아라비아와 아랍에미리트(UAE)에서는 냉방 에너지 비용 증가가 차양 자동화를 촉진하고 있는 반면, 브라질과 아르헨티나에서는 경제 불안정이 대규모 도입을 저해하고 있습니다. 전반적으로, 지역별 정책의 일관성 덕분에 태양광 일조량 제어 시스템 시장은 전 세계적으로 상승세를 보이고 있으며, 기후 목표와 경제적 인센티브가 점차 조화를 이루고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the solar sunlight control system market size was valued at USD 21.75 billion in 2025 and is estimated to grow from USD 23.06 billion in 2026 to reach USD 30.58 billion by 2031, at a CAGR of 5.81% during the forecast period (2026-2031).

This report is Segmented by Product Type (Manual Solar Control Systems and More), Technology (Photoelectric Sensors, and More), Component (Actuators, and More), Installation Type (New Installations and Retrofit Installations), Application (Residential, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Solar Sunlight Control System Market Trends and Insights

Stricter Green-Building Energy Codes Elevating Daylight & Facade Performance Requirements

Building regulations worldwide now embed daylight metrics and solar-heat-gain caps, effectively mandating dynamic shading or electrochromic glazing. ASHRAE 90.1-2022 raises visible-transmittance thresholds, while the EU's Energy Performance of Buildings Directive recast doubles renovation targets and pushes automated shading into national codes. China's GB/T 50378-2019 awards higher ratings to projects with intelligent sunlight control, locking the Solar sunlight control system market into core design considerations rather than optional upgrades.

Commercial Real-Estate Shift Toward Dynamic Glazing for Wellness & Energy Savings

Landlords report rent premiums and faster lease-ups when dynamic glazing replaces blinds. GREYSTAR's Exo Apartments reached full occupancy 80% faster after installing View Smart Windows, linking glare-free daylight to tenant appeal. Kilroy Realty cut annual energy spend by USD 1 million across properties using View's networked platform. Saint-Gobain's 2025 launch of SageGlass RealTone with four tint zones satisfies occupant preference for view clarity, further boosting adoption.

High Upfront Cost of Smart Glass & Motorized Shading

Electrochromic glazing commands a 15%-25% premium over static low-E glass, adding USD 50-USD 150 per ft2 to facade budgets and deterring mid-market projects. Motorized shades cost USD 300-USD 800 per window versus USD 50-USD 150 for manual blinds, prompting developers in Southeast Asia and South America to value-engineer them out. Although total-cost-of-ownership models yield 5- to 10-year paybacks, first-cost sensitivity remains a hurdle.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Residential Retrofits Seeking Energy-Efficient Window Coverings

- U.S. Inflation Reduction Act's 30%-50% ITC for Electrochromic Smart Windows

- Skilled-Labour Shortage for Complex Retrofit Installations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Automated shading captured 45.3% of 2025 revenue, illustrating the early mainstreaming of motorization, yet smart control systems are forecast to expand at a 12.0% CAGR to 2031, more than twice the overall Solar sunlight control system market pace. Buyers now judge value on predictive intelligence rather than motion alone, and the smart tier embeds cloud analytics, AI algorithms, and open APIs that unlock SaaS billing. Consequently, legacy manual products remain relevant only in price-sensitive retrofits and regions with unreliable power.

Smart platforms also reshape gross-margin profiles because annual software fees rise faster than hardware costs fall. Lutron's Athena cloud service, for example, charges per-square-foot subscriptions that exceed the amortized cost of its motors, underscoring how analytics rather than mechanics anchor future profits. As project specifications increasingly require BACnet, Matter, or Bluetooth mesh compatibility, smart control vendors win on interoperability and cybersecurity assurances.

Photoelectric sensors held 40.0% of 2025 revenue because of familiarity and low BOM costs, but infrared sensing will climb at an 11.1% CAGR through 2031 as building owners demand thermal-load and occupancy data in one device. A 2025 IEEE field trial showed LoRa-based infrared nodes sustaining 99.2% network uptime while extending battery life by 80%, directly addressing maintenance concerns that once limited wireless adoption.

Infrared arrays also feed real-time heat-map data to AI engines, enabling shading adjustments seconds before occupants perceive discomfort. Thermal-sensor bundles therefore reduce HVAC spikes, which is why life-science laboratories and data centers specify them despite the 10% unit premium. As wireless protocols such as Matter and Zigbee 3.0 embed security keys at the silicon level, buyers accept wireless reliability, further tipping the share away from wired photoelectric loops.

Geography Analysis

North America retained 33.4% of 2025 revenue as the IRA's 30%-50% investment tax credit pushed electrochromic glazing into mainstream specifications. State-level stretch codes in California and New York tighten solar-heat-gain caps annually, ensuring the Solar sunlight control system market continues to grow on mandated performance thresholds. Tax certainty through 2032 encourages longer development pipelines, and abundant smart-building expertise accelerates retrofit conversions.

Asia-Pacific will record a 6.7% CAGR to 2031, the fastest regional trajectory, because China, India, and ASEAN economies embed daylight metrics into occupancy permits. China's GB/T 50378-2019 standard awards premium ratings to projects with intelligent shading, and tier-1 developers chase that label to secure higher lease rates. India's 2024 update of the Energy Conservation Building Code forces new offices in hot-dry zones to achieve solar-heat-gain coefficients below 0.25, effectively mandating dynamic glazing. As urbanization pushes skyscraper counts higher, automated facade solutions become indispensable.

Europe benefits from the Renovation Wave initiative, which aims to double deep retrofit rates by 2030. Projects such as Saint-Gobain's Smart Campus Bordeaux showcase electrochromic scalability, while high labor costs make automation more cost-effective than manual blinds. Latin America and the Middle East trail global averages yet still log mid-single-digit growth; cooling-energy premiums in Saudi Arabia and the UAE motivate shade automation, whereas economic volatility tempers large-scale adoption in Brazil and Argentina. Collectively, regional policy convergence places the Solar sunlight control system market on a worldwide upswing that aligns climate targets with financial incentives.

- Hunter Douglas

- Somfy Systems

- Lutron Electronics

- Warema Renkhoff SE

- View Inc.

- Saint-Gobain (SageGlass)

- 3M Company

- Eastman Chemical (LLumar/Solar Gard)

- Guardian Industries

- Kawneer Company

- Griesser AG

- ABB Ltd.

- Siemens AG

- Johnson Controls International

- Skyco Shading Systems

- Pleotint LLC

- EControl-Glas GmbH

- Smartglass International

- Heliotrope Technologies

- Renson Sun Protection Screens

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter green-building energy codes elevating daylight & facade performance requirements

- 4.2.2 Commercial real-estate shift toward dynamic glazing for wellness & energy savings

- 4.2.3 Surge in residential retrofits seeking energy-efficient window coverings

- 4.2.4 U.S. Inflation Reduction Act's 30-50 % ITC for electrochromic smart windows

- 4.2.5 AI-driven predictive shading software delivering <3-year payback

- 4.2.6 Health-centric certifications (WELL, Fitwel) rewarding circadian-light management

- 4.3 Market Restraints

- 4.3.1 High upfront cost of smart glass & motorised shading

- 4.3.2 Skilled-labour shortage for complex retrofit installations

- 4.3.3 Limited recyclability of multi-layer smart films creating EoL liabilities

- 4.3.4 Cyber-security threats to IoT-connected shading networks

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Manual Solar Control Systems

- 5.1.2 Automated Solar Control Systems

- 5.1.3 Smart Control Systems

- 5.2 By Technology

- 5.2.1 Photoelectric Sensors

- 5.2.2 Thermal Sensors

- 5.2.3 Infrared Sensors

- 5.2.4 Wireless Technology

- 5.3 By Component

- 5.3.1 Actuators

- 5.3.2 Controllers

- 5.3.3 Sensors

- 5.3.4 Software Solutions

- 5.3.5 Others

- 5.4 By Installation Type

- 5.4.1 New Installations

- 5.4.2 Retrofit Installations

- 5.5 By Application

- 5.5.1 Residential

- 5.5.2 Commercial

- 5.5.3 Industrial

- 5.5.4 Agriculture

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 NORDIC Countries

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 ASEAN Countries

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 South Africa

- 5.6.5.4 Egypt

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Hunter Douglas

- 6.4.2 Somfy Systems

- 6.4.3 Lutron Electronics

- 6.4.4 Warema Renkhoff SE

- 6.4.5 View Inc.

- 6.4.6 Saint-Gobain (SageGlass)

- 6.4.7 3M Company

- 6.4.8 Eastman Chemical (LLumar/Solar Gard)

- 6.4.9 Guardian Industries

- 6.4.10 Kawneer Company

- 6.4.11 Griesser AG

- 6.4.12 ABB Ltd.

- 6.4.13 Siemens AG

- 6.4.14 Johnson Controls International

- 6.4.15 Skyco Shading Systems

- 6.4.16 Pleotint LLC

- 6.4.17 EControl-Glas GmbH

- 6.4.18 Smartglass International

- 6.4.19 Heliotrope Technologies

- 6.4.20 Renson Sun Protection Screens

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment