|

시장보고서

상품코드

2063246

스페이서 유체 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Spacer Fluid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

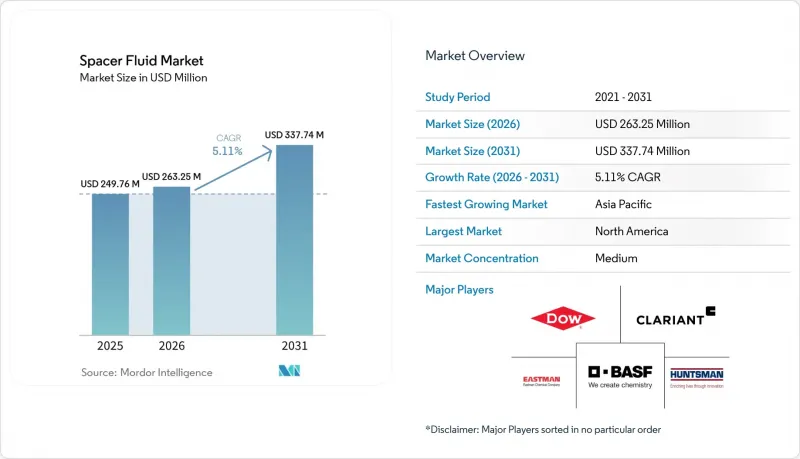

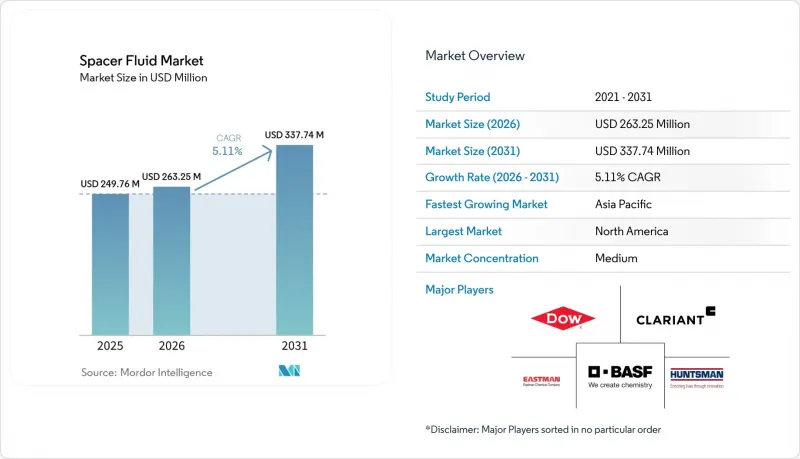

Mordor Intelligence에 의하면, 스페이서 유체 시장 규모는 2025년에 2억 4,976만 달러로 평가되었습니다. 2026년 2억 6,325만 달러에서 2031년까지 3억 3,774만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 5.11%를 나타낼 전망입니다.

본 보고서는 유체 기반(수계, 유계, 기타), 첨가제 화학 조성(점도 증진제 및 유변학 조절제, 기타), 기능(1차 시멘트 주입, 기타), 저류층 유형(탄산염암, 기타), 시추공 유형(HPHT, 기타), 입지(육상 및 해상), 그리고 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 스페이서 유체 시장 동향 및 인사이트

ESG에 기반한 메탄 누출 감축 의무

세계의 기후 정책에 따라, 가스 유출 방지를 위한 스페이서의 사양이 재구성되고 있습니다. 미국 환경보호청(EPA)의 2024년 규정에 따라 2026년에 톤당 1,500달러까지 인상되는 ‘폐기물 배출료’가 도입되며, 이에 따라 더 엄격한 밀도 범위와 케이싱 표면을 적셔 미세 고리형 공극의 형성을 억제하는 계면활성제 패키지의 사용이 의무화되었습니다. 유럽연합(EU)의 메탄 규제가 2024년에 시행되고, 수입 가스에도 규제 적용 범위가 확대됨에 따라 ISO 13503 인증을 획득한 유체에 대한 수요가 증가하고 있습니다. 퍼미안 분지에서 채택된 SLB사의 CemCRETE LiteCRETE 폴리머 스페이서는 벤토나이트계 유체와 비교해 가스 이동을 40% 줄였습니다. 작업자들은 환형 씰의 일관성을 확보하기 위해, 특히 압력 급상승으로 인해 경화되지 않은 시멘트가 박리될 우려가 있는 수평 셰일 유정에서 밀도 허용 오차를 ±0.2 lb/gal로 설정할 것을 점점 더 강력히 요구하고 있습니다. 이와 동시에, 디지털 누출 감지 플랫폼이 몇 분 이내에 이상을 감지하기 때문에 신속한 시정 조치가 요구되며, 프리미엄 스페이서의 도입이 더욱 촉진되고 있습니다.

HPHT 및 초심해 프로젝트의 급증

수십억 달러 규모의 심해 복합 시설로 인해, 스페이서 유체 시장은 합성계 및 유성계 시스템으로 전환되고 있습니다. 셰브론의 ‘앵커’ 프로젝트와 쉘의 ‘웨일’ 프로젝트는 각각 2만 psi 및 350°F를 초과하는 환경에서 가동되고 있으며, 열적으로 안정된 증점제와 최대 18 lb/gal의 밀도가 요구됩니다. 페트로브라스는 2024년 SLB사에 4억 3,000만 달러 규모의 계약을 수주했습니다. 이 계약은 28번 유정을 대상으로 하며, 나노 입자가 강화된 스페이서를 통해 1만 5,000 psi 조건에서 유체 손실을 50 ml/30분 미만으로 억제하고 있습니다. 산화 그래핀 등의 나노 입자는 불투수성 케이크를 형성하여 지층의 격리를 확보하는 동시에 지층 손상을 줄여줍니다. 따라서 HPHT 및 초심해에서 수요로 인해, 배출 기준 범위 내에서 생분해되면서도 극한의 해저 환경을 견딜 수 있는 합성 기반 유체에 대한 조달 경향이 강화되고 있으며, 이것이 프리미엄 화학제품의 장기적인 성장을 뒷받침하고 있습니다.

특수 바이오 폴리머의 가격 변동

2026년 1월, 중국 배양 업체들의 에너지 비용 상승에 따라 크산탄 가격은 전년 대비 10% 상승한 톤당 2,760달러에 달했습니다. 인도에서는 2024년 칼리프(우기) 시즌에 몬순의 변동성으로 인해 구아 생산량이 15% 감소한 데다, 10%-50%의 수입 관세가 부과됨에 따라 인도산 제품에 의존하는 서비스 기업의 비용이 상승했습니다. 합성 고분자는 안정성을 제공하지만, EU의 REACH 규제로 인해 환경적 우려가 제기되고 있어, 바이오 고분자를 완전히 대체할 수 있는 능력에는 한계가 있습니다. 스페이서는 우물 총 비용의 5-8%를 차지하기 때문에 비용이 급등하면 즉시 예산 초과로 이어지며, 특히 수익성이 낮은 재파쇄 작업이나 폐광 프로그램에서는 그 영향이 두드러집니다.

부문별 분석

수계 제제는 비용이 저렴하고 취급이 용이하기 때문에 2025년에는 스페이서 유체 시장 점유율의 63.8%를 차지했습니다. 그러나 폴리머를 풍부하게 함유한 스위치블 유체는 스페이서 유체 시장 전체보다 220 베이시스 포인트 높은 성장률을 보이고 있으며, pH 트리거에 의한 겔화가 수평 시추공의 층간 격리를 개선하기 때문에 2031년까지 연평균 성장률(CAGR) 7.3%로 확대되고 있습니다. 유성 제품은 고압·고온(HPHT) 환경 및 심해 유정에서 여전히 필수적입니다. 멕시코만과 같이 배출 규제가 엄격한 해역에서 선호되는 합성 기반 유체는 28일 이내에 생분해되며, 독성 기준을 충족합니다. 발포 및 초경량 시스템은 점도를 저하시키지 않으면서 밀도를 갤런당 6파운드까지 낮춤으로써, 고갈층이나 저압층에서의 작업을 가능하게 합니다.

스위치블 유체는 pH 12 이상에서 그 자리에서 겔화를 일으켜 시멘트 오염을 줄여줍니다. 이 기능을 통해 Fervo Energy사의 400개 유정에 이르는 지열 프로그램에서 유정당 스페이서 부피를 10% 줄일 수 있었습니다. 에스테르 및 폴리아알파올레핀과 같은 합성 베이스들은 450°F(약 232°C) 환경에서 12시간 동안 견딜 수 있으며, 지열 및 CCUS 요건을 충족합니다. 이러한 프리미엄 틈새 시장들이 결합되면서, 기존에 주류를 이루던 저사양 수성 시스템의 우위를 서서히 약화시키고, 스페이서 유체 시장 규모 분포를 재정의하고 있습니다.

증점제 및 유변학 조절제는 2025년 첨가제 수요의 34.5%를 차지했으나, 나노 강화 시스템은 2031년까지 연평균 성장률(CAGR) 7.5%로 확대될 전망이며, 고압·고온(HPHT) 조건 하에서 유체 손실 억제 효과를 30%-40% 개선합니다. 계면활성제 및 습윤성 개질제는 NPDES 독성 시험 기준을 충족하는 생분해성 화학물질로의 전환을 주도하고 있습니다. 자연 균열이 있는 저류층에서는 유체 손실 방지재와 브리징 파이버가 여전히 필수적입니다.

베이커 휴즈사가 개발한 실리카 나노 입자 스페이서는 350°F(약 177°C)에서 30분당 50 ml 미만의 유체 손실을 기록하며, 잔탄계 시스템을 능가했습니다. 산화 그래핀을 첨가함으로써 실험실 시험에서 시멘트의 압축 강도가 15% 향상되어, HPHT 완공 공사에의 도입이 촉진되고 있습니다. 따라서 첨가제의 구성은 벌크 유변학 개질제에서 성능을 향상시키는 한편 단위 비용을 소폭 상승시키는 엔지니어링 나노 첨가제로 점차 전환되고 있습니다.

지역별 분석

북미는 2024년에 시추된 1만 2,000개의 수평 셰일 유정을 바탕으로, 2025년 스페이서 유체 시장 점유율의 36.9%를 차지하며 1,500만 배럴의 완공 유체를 소비했습니다. 그러나 자본이 재프래킹으로 이동함에 따라, 해당 지역의 성장은 둔화되고 있습니다. 버넷 셰일 사례에서는 유정당 1만 5,000-3만 달러의 비용이 드는 하이브리드 스페이서를 사용함으로써 생산량이 30-50% 증가했습니다. 캐나다 몬토니 지역에서는 LNG 수출 수요에 힘입어, H2S가 풍부하게 포함된 유정을 위해 사워 가스 대응 스페이서가 필요로 하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 6.2%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. 인도에서는 2027년까지 시추용 화학 약품의 60%를 현지에서 조달하도록 하는 규정이 도입됨에 따라, 국내에서의 잔탄 발효 및 구아 가공이 촉진되고 있습니다. 중국해양석유(CNOOC)는 중국산 스페이서가 필요한 12억 달러 규모의 시추 계약을 체결했습니다. 한편, 인도네시아의 SKK Migas는 2030년까지 현지 조달률 50%를 목표로 삼고 있으며, 다국적 기업들에게 제휴 및 블렌딩 플랜트 건설을 촉구하고 있습니다.

유럽에서는 요한 스베르드루프와 같이 신규 개발과 대규모 P&A(유정 폐쇄)에 이중으로 초점을 맞추는 모습을 볼 수 있습니다. 영국 규제 당국은 2030년까지 북해의 2,000개 유정이 폐쇄될 것으로 전망하고 있으며, 이에 따라 갤런당 16파운드인 고밀도 스페이서에 대한 수요가 증가하고 있습니다. 남미는 12%를 차지하고 있으며, 브라질의 프레솔트층이 주를 이루고, 고압 유정에서는 합성 기반이 사용되고 있습니다. 중동 및 아프리카에서는 자푸라(Jafurah)의 비전통 가스 생산 확대와 가샤(Ghasha)의 초산성 가스가 호재로 작용하고 있으며, 두 지역 모두 유체 손실 방지 및 부식 억제 성분이 포함된 제품이 선호되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the spacer fluid market size was valued at USD 249.76 million in 2025 and is estimated to grow from USD 263.25 million in 2026 to reach USD 337.74 million by 2031, at a CAGR of 5.11% during the forecast period (2026-2031).

This report is Segmented by Fluid Base (Water-Based, Oil-Based, More), Additive Chemistry (Viscosifiers and Rheology Modifiers, More), Function (Primary Cementing, More), Reservoir Type (Carbonate, More), Well Type (HPHT, More), Location (Onshore and Offshore), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Spacer Fluid Market Trends and Insights

ESG-driven methane-leak reduction mandates

Global climate policy is reshaping spacer specifications toward gas-migration prevention. The U.S. EPA's 2024 rule introduced a Waste Emissions Charge that rises to USD 1,500 per metric ton in 2026, compelling tighter density windows and surfactant packages that wet casing surfaces and curb micro-annulus formation. The European Union's Methane Regulation went live in 2024, extending liability to imported gas and elevating demand for ISO 13503-certified fluids. SLB's CemCRETE LiteCRETE polymer spacer, deployed in the Permian, cut gas migration by 40% relative to bentonite fluids. Operators increasingly insist on density tolerances of +-0.2 lb/gal to ensure annular seal integrity, especially in horizontal shale wells where pressure spikes can dislodge unset cement. In parallel, digital leak-detection platforms flag anomalies within minutes, forcing rapid remediation and further boosting premium spacer uptake.

Surge in HPHT and ultra-deepwater projects

Multi-billion-dollar deepwater complexes are moving the spacer fluid market toward synthetic and oil-based systems. Chevron's Anchor and Shell's Whale projects each operate beyond 20,000 psi and 350 °F, demanding thermally stable viscosifiers and densities up to 18 lb/gal. Petrobras awarded SLB a USD 430 million contract in 2024 covering 28 wells where nanoparticle-enhanced spacers maintain fluid-loss below 50 ml/30 min at 15,000 psi. Nanoparticles such as graphene oxide form impermeable cakes that safeguard zonal isolation while lowering formation damage. HPHT and ultra-deepwater demand is therefore tilting procurement toward synthetic-base fluids that biodegrade within discharge limits yet survive extreme bottomhole environments, underpinning long-cycle growth for premium chemistries.

Volatile pricing of specialty biopolymers

Xanthan hit USD 2,760 per metric ton in Jan 2026, up 10% year-on-year, after Chinese fermenters faced higher energy costs. Guar output fell 15% in India's 2024 kharif season due to erratic monsoon, then faced 10%-50% import duties, lifting costs for service companies reliant on Indian supply. Synthetic polymers offer consistency but raise environmental flags under EU REACH, limiting their ability to fully replace biopolymers. Spacers make up 5%-8% of total well costs, so cost spikes translate quickly into budget overruns, especially for re-frac and abandonment programs with tight economics.

Other drivers and restraints analyzed in the detailed report include:

- Rising shale re-fracturing programs in North America

- Digitally designed rheology-tunable spacer formulations

- Stricter discharge limits on surfactant toxicity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Water-based formulations held 63.8% of the spacer fluid market share in 2025, thanks to low cost and easy handling. Yet polymer-rich switchable fluids are growing 220 basis points faster than the overall spacer fluid market, advancing at 7.3% CAGR to 2031 as pH-triggered gelling improves zonal isolation in horizontals. Oil-based products remain vital for HPHT and deepwater wells. Synthetic-base fluids favored in discharge-sensitive basins like the Gulf of Mexico, biodegrade within 28 days, a nd meet toxicity limits. Foamed and ultralight systems enable operations in depleted or low-pressure zones by cutting density to 6 lb/gal without losing viscosity.

Switchable fluids trim cement contamination by forming in-situ gels at pH 12 and above, a function that saved 10% spacer volume per well in Fervo Energy's 400-well geothermal program. Synthetic bases, often esters or polyalphaolefins, survive 450 °F for 12 hours, meeting geothermal and CCUS needs. Together, these premium niches are eroding the historical dominance of low-specification water-based systems, redefining the spacer fluid market size distribution.

Viscosifiers and rheology modifiers captured 34.5% of additive demand in 2025, but nano-enhanced systems are set to expand 7.5% CAGR through 2031, improving fluid-loss control by 30%-40% under HPHT conditions. Surfactants and wettability agents driven by the shift to biodegradable chemistries that meet NPDES toxicity tests. Lost-circulation materials and bridging fibers remain essential for naturally fractured reservoirs.

Silica nanoparticle spacers rolled out by Baker Hughes achieved fluid-loss below 50 ml/30 min at 350 °F, outclassing xanthan systems. Graphene oxide loading raised cement compressive strength by 15% in lab tests, supporting adoption in HPHT completions. The additive mix is therefore pivoting from bulk rheology modifiers to engineered nano-additives that elevate performance while nudging unit costs upward.

Geography Analysis

North America commanded 36.9% spacer fluid market share in 2025 on the back of 12,000 horizontal shale wells drilled in 2024, consuming 15 million barrels of completion fluids. Yet growth here moderates as capital pivots to re-fracs; Barnett campaigns showed 30%-50% production uplifts using hybrid spacers that cost USD 15,000-30,000 per well. Canada's Montney, buoyed by LNG export demand, needs sour-gas compatible spacers for H2S-rich wells.

Asia-Pacific is the fastest-growing region at 6.2% CAGR through 2031. India's 60% local-content rule for drilling chemicals by 2027 is spurring domestic xanthan fermentation and guar processing. CNOOC awarded USD 1.2 billion in drilling contracts requiring China-made spacers, while Indonesia's SKK Migas targets 50% local content by 2030, compelling multinationals to partner or build blending plants.

Europe reflects a dual focus on new developments like Johan Sverdrup and large-scale P&A. The UK regulator expects 2,000 North Sea wells to be abandoned by 2030, lifting demand for 16 lb/gal high-density spacers. South America, at 12%, is dominated by Brazil's pre-salt, where high-pressure wells use synthetic bases. The Middle East & Africa benefit from the Jafurah unconventional gas ramp-up and Ghasha ultra-sour gas, both favoring lost-circulation and corrosion-inhibited formulations.

- Halliburton Company

- Schlumberger (Now SLB)

- Baker Hughes Company

- Weatherford International

- CES Energy Solutions

- Newpark Resources Inc.

- TETRA Technologies Inc.

- Aubin Group

- Trican Well Service

- Calfrac Well Services

- Superior Energy Services

- Scomi Oiltools

- Nine Energy Service

- Petrochem Performance Chemicals

- Nalco Champion (Ecolab Energy)

- MI SWACO (SLB)

- Drilling Specialties Co. (DSCo)

- Panther Fluids Management

- Impact Fluid Solutions

- Obsidian Energy Chemicals

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 ESG-driven methane-leak reduction mandates

- 4.2.2 Surge in HPHT & ultra-deepwater projects

- 4.2.3 Rising shale re-fracturing programs in North America

- 4.2.4 Digitally designed rheology-tunable spacer formulations

- 4.2.5 CCUS well retrofits requiring novel spacer chemistries

- 4.2.6 National oil company local-content rules (MENA, APAC)

- 4.3 Market Restraints

- 4.3.1 Volatile pricing of specialty biopolymers

- 4.3.2 Stricter discharge limits on surfactant toxicity

- 4.3.3 Supply bottlenecks for food-grade xanthan/guar post-El Nino

- 4.3.4 AI-based mud-in-place simulators lowering spacer volumes

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Fluid Base

- 5.1.1 Water-Based Spacer Fluid

- 5.1.2 Oil-Based Spacer Fluid

- 5.1.3 Synthetic-Based Spacer Fluid

- 5.1.4 Polymer-Rich Switchable Fluids

- 5.1.5 Others (Foamed, Ultralight, etc.)

- 5.2 By Additive Chemistry

- 5.2.1 Viscosifiers and Rheology Modifiers

- 5.2.2 Surfactants and Wettability Agents

- 5.2.3 LCM/Bridging Fibers

- 5.2.4 Nanoparticle-Enhanced Systems

- 5.3 By Function

- 5.3.1 Primary Cementing

- 5.3.2 Remedial/Plug and Abandon

- 5.3.3 Drilling Mud Displacement

- 5.3.4 Enhanced Oil Recovery (EOR)

- 5.3.5 Wellbore Cleanup and Other Uses

- 5.4 By Reservoir Type

- 5.4.1 Carbonate

- 5.4.2 Sandstone

- 5.4.3 Naturally Fractured

- 5.4.4 Others

- 5.5 By Well Type

- 5.5.1 Conventional Vertical

- 5.5.2 HPHT

- 5.5.3 Unconventional Shale/Tight

- 5.5.4 Directional/Horizontal

- 5.5.5 Geothermal

- 5.6 By Location

- 5.6.1 Onshore

- 5.6.2 Offshore

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 NORDIC Countries

- 5.7.2.6 Russia

- 5.7.2.7 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 ASEAN Countries

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 South America

- 5.7.4.1 Brazil

- 5.7.4.2 Argentina

- 5.7.4.3 Rest of South America

- 5.7.5 Middle East and Africa

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 South Africa

- 5.7.5.4 Egypt

- 5.7.5.5 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Halliburton Company

- 6.4.2 Schlumberger (Now SLB)

- 6.4.3 Baker Hughes Company

- 6.4.4 Weatherford International

- 6.4.5 CES Energy Solutions

- 6.4.6 Newpark Resources Inc.

- 6.4.7 TETRA Technologies Inc.

- 6.4.8 Aubin Group

- 6.4.9 Trican Well Service

- 6.4.10 Calfrac Well Services

- 6.4.11 Superior Energy Services

- 6.4.12 Scomi Oiltools

- 6.4.13 Nine Energy Service

- 6.4.14 Petrochem Performance Chemicals

- 6.4.15 Nalco Champion (Ecolab Energy)

- 6.4.16 MI SWACO (SLB)

- 6.4.17 Drilling Specialties Co. (DSCo)

- 6.4.18 Panther Fluids Management

- 6.4.19 Impact Fluid Solutions

- 6.4.20 Obsidian Energy Chemicals

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment