|

시장보고서

상품코드

2063249

중국의 양돈 사료 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)China Swine Feed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

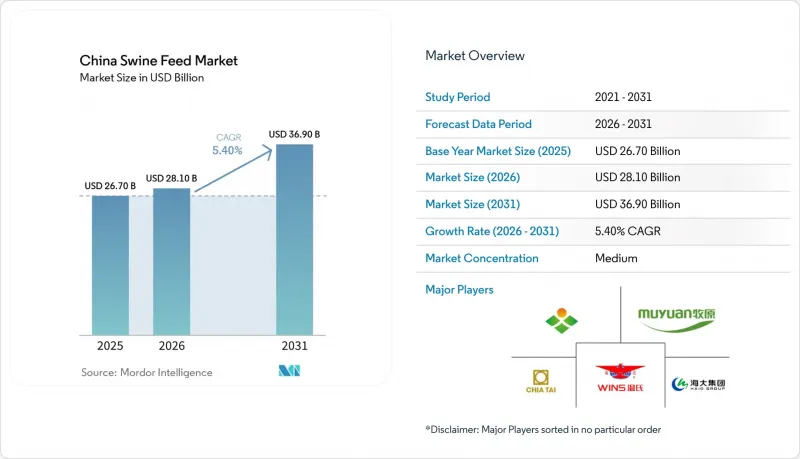

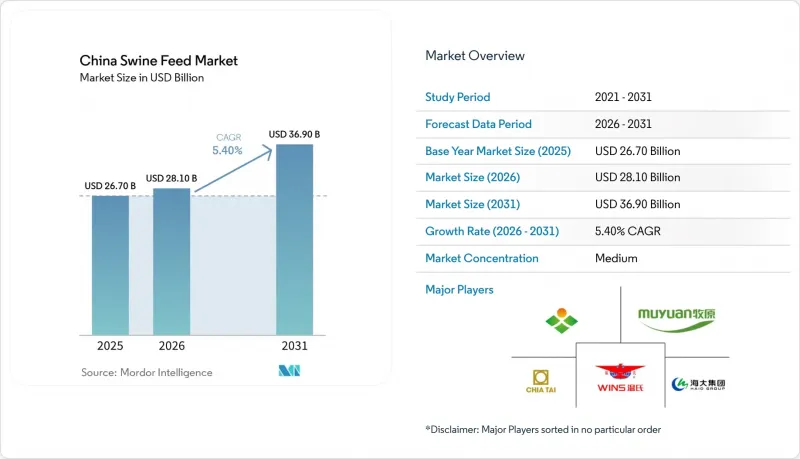

Mordor Intelligence에 의하면, 중국의 양돈 사료 시장 규모는 2025년 267억 달러로 평가되었습니다. 2026년 281억 달러에, 게다가 2031년까지 369억 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 5.4%를 나타낼 전망입니다.

본 보고서는 제품 유형(스타터 사료, 그로워 사료, 피니셔 사료, 브리더 사료), 형태(펠렛, 매시, 크럼블) 및 원료 유형(옥수수, 대두박, 아미노산 첨가제, 비타민·미네랄, 효소, 기타 곡물 및 유지)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

중국의 양돈 사료 시장 동향과 인사이트

대규모 양돈장의 급속한 통합

대규모 양돈장의 급속한 통합으로 인해, 조달 역량은 곡물 공급업체와 직접 협상하며 각 성장 단계에 맞는 사료 배합을 필요로 하는 수직 통합형 기업으로 전환되고 있습니다. 무위안 푸드(Muyuan Foods)는 2025년 3월 기준으로 1Kg당 12위안(1.65달러)의 완전 배분 번식 비용을 보고했습니다. 이러한 사업 규모 덕분에 통합형 기업은 현장의 사료 공장 운영, 엄격한 생물안전 대책의 시행, 그리고 절감된 비용을 영양 조사에 재투자하는 것이 가능해졌으며, 이로 인해 대규모 통합형 기업과 소규모 농가 간의 격차가 더욱 벌어지고 있습니다.

아프리카 돼지열병(ASF)을 계기로, 생물안전 대책이 적용된 시판 사료 수요가 급증

아프리카 돼지열병(ASF) 발생에 따라 양돈 농가들은 생물안전 대책을 강화하고, 보다 안전한 사료 조달로 전환하고 있습니다. 유엔 식량농업기구(FAO) 보고서에 따르면, 베트남의 아프리카돼지열병(ASF) 발생 건수는 2024년 1,600건 이상에서 2025년에는 약 2,495건으로 급증했으며, 약 127만 마리의 돼지가 살처분되었습니다. 이러한 증가는 기존 시스템에서 오염 위험이 높아지고 있음을 여실히 보여주고 있습니다. ASF는 사료나 농장 투입물을 통해 감염될 가능성이 있으므로, 생산자들은 생물학적 안전성이 확보된 공장에서 조달된, 열처리된 인증된 시판 사료로 전환하고 있습니다. 이러한 변화로 인해 추적성이 확보됨에 따라, HACCP 기준을 준수하는 배합 사료 제품에 대한 수요가 증가하고 있습니다.

국내 옥수수 가격 변동

2026년 2월, 국내 옥수수 가격은 1Kg당 2.320 위안(1Kg당 0.32 달러)에 거래되어, 2022년 말의 1Kg당 3 위안에서 크게 하락했습니다. 이러한 급격한 가격 하락은 옥수수 시장의 변동성을 여실히 드러내고 있으며, 생산자와 거래업자 모두에게 과제가 되고 있습니다. 이러한 가격 변동은 선물 계약에 불확실성을 야기하여, 생산자가 안정적인 가격을 확보하고 사업 계획을 효과적으로 수립하는 데 어려움을 주고 있습니다. 또한, 이러한 가격 변동성은 생산자들이 예방 조치로 재고 수준을 낮추는 요인이 되어 사료 수요 감소를 초래하고, 시장 역학에 추가적인 영향을 미칠 가능성이 있습니다.

부문별 분석

2025년, 중국의 양돈 사료 시장에서 육성기용 사료가 38%라는 가장 큰 점유율을 차지했습니다. 이는 체중 30-70Kg의 성장기에 사료 소비량이 많고, 1두당 배합사료량이 가장 많아지기 때문입니다. 스타터 사료 시장 규모는 2026년부터 2031년까지 연평균 성장률(CAGR) 5.9%를 기록하며 가장 높은 성장세를 보일 것으로 전망됩니다. 이러한 성장은 사망률 감소와 비육 기간 단축을 목표로 한 생후 초기 장 건강 프로그램에 대한 업계의 관심이 높아지고 있음을 반영하며, 양돈 생산의 주요 과제에 대한 대응이 이루어지고 있습니다. 피니셔 사료의 경우 생산 비용 최적화를 위한 비용 효율성에 계속해서 중점을 두고 있는 반면, 번식용 사료공급량은 모돈의 사육 두수 동향과 밀접한 관련이 있습니다.

생산자들은 스트레스를 최소화하고, 장내 환경을 개선하며, 성장 능력을 높이기 위해 이유기의 영양 관리 정확도를 높이는 데 주력하고 있습니다. 그 결과, 소화 흡수가 잘 되는 단백질, 유기산, 면역 및 영양 흡수를 촉진하는 사료 첨가제 등 기능성 원료의 사용이 증가하고 있습니다. 항생제 및 산화아연 사용에 관한 규제도, 규정을 준수하는 첨단 스타터 사료 솔루션의 개발을 더욱 촉진하고 있습니다. 또한, 대규모 농장과 위탁 사육 시스템의 확대에 힘입어 사료 효율 향상과 사망률 감소를 목표로 하는 통합 생산 모델에 힘입어, 고품질 스타터 사료에 대한 수요가 증가하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the china swine feed market size is projected to grow from USD 26.7 billion in 2025 to USD 28.1 billion in 2026, and further to USD 36.9 billion by 2031, with a CAGR of 5.4% from 2026 to 2031.

This report is Segmented by Product Type (Starter Feed, Grower Feed, Finisher Feed, Breeder Feed), by Form (Pellet, Mash, Crumbles), and by Ingredient Type (Corn, Soybean Meal, Amino-Acid Additives, Vitamins and Minerals, Enzymes, Other Cereals and Fats). The Market Forecasts are Provided in Terms of Value (USD).

China Swine Feed Market Trends and Insights

Rapid Consolidation of Large-Scale Pig Farms

The rapid consolidation of large-scale pig farms is shifting procurement power toward vertically integrated companies that negotiate directly with grain suppliers and require stage-specific feed rations. Muyuan Foods reported a fully allocated breeding cost of CNY 12 per kilogram (USD 1.65 per kilogram) in March 2025 . The scale of operations enables integrators to operate on-site feed mills, implement stringent biosecurity measures, and reinvest cost savings into nutrition research, further widening the gap between large integrators and smallholders.

African Swine Fever (ASF)-Triggered Surge in Biosecure Commercial Feed

In response to the African Swine Fever (ASF) outbreak, swine producers are tightening biosecurity measures and pivoting towards safer feed sourcing. The Food and Agriculture Organization reported a jump in ASF cases in Vietnam, rising from over 1,600 in 2024 to about 2,495 in 2025, leading to the culling of roughly 1.27 million pigs . This uptick underscores heightened contamination risks in conventional systems. Given that ASF can be transmitted via feed and farm inputs, producers are turning to heat-treated, certified commercial feed sourced from biosecure mills. This shift is propelling the demand for traceable, HACCP-compliant compound feed products.

Domestic Corn-Price Volatility

In February 2026, domestic corn was traded at 2.320 RMB per kilogram (USD 0.32 per kilogram), marking a significant decline from 3.000 RMB per kilogram in late 2022 . This sharp price drop highlights the volatility in the corn market, which poses challenges for producers and traders alike. Such fluctuations create uncertainty in forward contracting, making it difficult for producers to secure stable pricing and plan their operations effectively. Additionally, this price instability may prompt producers to reduce their inventory levels as a precautionary measure, potentially leading to a decline in feed demand and further impacting market dynamics.

Other drivers and restraints analyzed in the detailed report include:

- Swill-Feeding Ban Spurs Commercial Feed Uptake

- Roll-Out of Precision-Feeding IoT Platforms

- Slow Herd-Rebuilding Pace post ASF

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Grower feed accounted for the largest 38% of the China swine feed market share in 2025, driven by the high feed consumption during the 30 to 70 kilogram growth phase, which requires the largest ration volume per animal. The starter feed market size is projected to register the fastest CAGR of 5.9% from 2026 to 2031. This growth reflects the industry's increasing focus on early-life gut-health programs designed to reduce mortality rates and shorten finishing periods, addressing key challenges in swine production. Finisher Feed remains focused on cost efficiency to optimize production expenses, while Breeder Feed volumes are closely tied to sow inventory trends.

Producers are focusing on nutritional precision during the weaning phase to minimize stress, improve gut health, and enhance growth performance. This has resulted in increased use of functional ingredients, including easily digestible proteins, organic acids, and feed additives that promote immunity and nutrient absorption. Regulatory restrictions on the use of antibiotics and zinc oxide are further driving the development of advanced, compliant starter feed solutions. Additionally, the expansion of large-scale farms and contract rearing systems is boosting the demand for high-quality starter feed, supported by integrated production models aimed at improving feed efficiency and reducing mortality rates.

List of Companies Covered in this Report:

- New Hope Liuhe Co., Ltd.

- Chia Tai Investment Co., Ltd. (Charoen Pokphand Group)

- Wens Foodstuff Group Co., Ltd.

- Guangdong Haid Group Co., Ltd.

- Muyuan Foods Co., Ltd.

- Beijing Dabeinong Technology Group Co., Ltd. (DBN Group)

- Tongwei Co., Ltd.

- Liaoning Wellhope Agri-Tech Co., Ltd.

- Cargill, Incorporated

- Archer-Daniels-Midland Company

- DSM-Firmenich AG

- Evonik Industries AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid consolidation of large-scale pig farms

- 4.2.2 African Swine Fever (ASF)-triggered surge in biosecure commercial feed

- 4.2.3 Government soybean-meal reduction mandate

- 4.2.4 Roll-out of precision-feeding IoT platforms

- 4.2.5 Adoption of recombinant thermostable phytase

- 4.2.6 Retailers carbon-neutral pork procurement targets

- 4.3 Market Restraints

- 4.3.1 Domestic corn-price volatility

- 4.3.2 Slow herd-rebuilding pace post-ASF

- 4.3.3 Stricter antibiotic-use regulations

- 4.3.4 Rising share of insect/fermented proteins in rations

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecast (Value)

- 5.1 By Product Type

- 5.1.1 Starter Feed

- 5.1.2 Grower Feed

- 5.1.3 Finisher Feed

- 5.1.4 Breeder Feed

- 5.2 By Form

- 5.2.1 Pellet

- 5.2.2 Mash

- 5.2.3 Crumbles

- 5.3 By Ingredient Type

- 5.3.1 Corn

- 5.3.2 Soybean Meal

- 5.3.3 Amino-Acid Additives

- 5.3.4 Vitamins and Minerals

- 5.3.5 Enzymes (e.g., Phytase)

- 5.3.6 Other Cereals and Fats

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 New Hope Liuhe Co., Ltd.

- 6.4.2 Chia Tai Investment Co., Ltd. (Charoen Pokphand Group)

- 6.4.3 Wens Foodstuff Group Co., Ltd.

- 6.4.4 Guangdong Haid Group Co., Ltd.

- 6.4.5 Muyuan Foods Co., Ltd.

- 6.4.6 Beijing Dabeinong Technology Group Co., Ltd. (DBN Group)

- 6.4.7 Tongwei Co., Ltd.

- 6.4.8 Liaoning Wellhope Agri-Tech Co., Ltd.

- 6.4.9 Cargill, Incorporated

- 6.4.10 Archer-Daniels-Midland Company

- 6.4.11 DSM-Firmenich AG

- 6.4.12 Evonik Industries AG