|

시장보고서

상품코드

2063251

항공우주 및 방위 커넥터 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Aerospace and Defense Connectors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

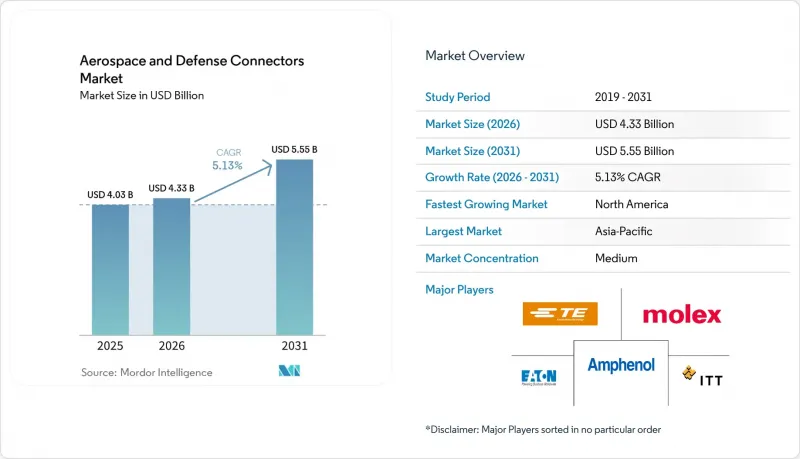

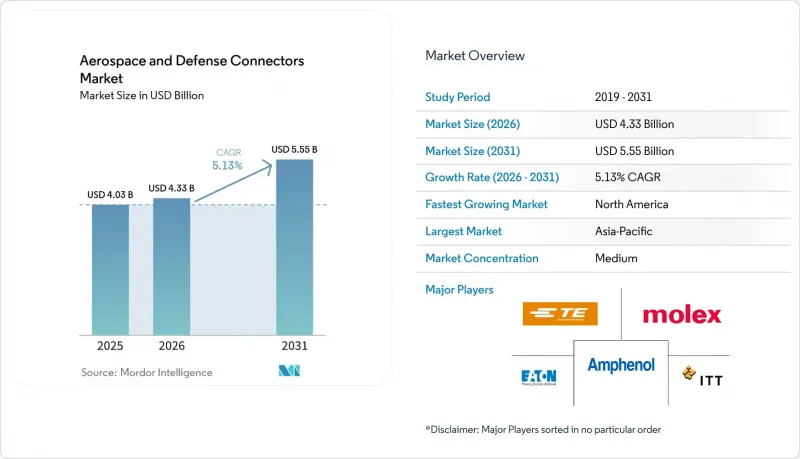

Mordor Intelligence에 의하면, 항공우주 및 방위 커넥터 시장은 2025년 40억 3,000만 달러로 평가되었습니다. 2026년 43억 3,000만 달러로 확대되고 2026년부터 2031년에 걸쳐 CAGR은 5.13%를 나타내, 2031년까지 55억 5,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 유형(전기, 광섬유, RF/마이크로파, 하이브리드, 고출력), 커넥터 형태(원형, 각형, 기판 간, 나노/마이크로 미니어처), 플랫폼(항공기 탑재, 지상 시스템 등), 최종 사용자(OEM 및 애프터마켓), 지역(북미, 유럽, 아시아태평양, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 항공우주 및 방위 커넥터 시장 동향과 인사이트

6G를 지원하는 고대역폭 항공전자 장비 링크가 차세대 연결성을 주도합니다.

6G 항공전자 장비로의 전환을 위해서는 D-밴드 mm파 주파수에 대응하는 커넥터 사양이 필요하며, 초저 삽입 손실과 위상 안정성이 요구됩니다. 군 당국은 현재 신호 저하를 허용할 수 없는 위상 배열 레이더 및 전자전 페이로드에 대응하기 위해 비접촉형 아키텍처를 요구하고 있습니다. 다중 도메인 전략으로 인해 실시간 데이터 통합에 따른 부하가 증가함에 따라, 항공우주 및 방위 커넥터 시장에서 고밀도 광 백본에 대한 수요가 높아지고 있습니다. 미국에서 조기 도입이 시작되고 차세대 전투기 개발이 가속화됨에 따라, 유럽의 몇몇 프로그램과 아시아의 주요 제조업체들도 이에 동참했습니다. CMMC 2.0의 사이버 보안 요구사항에 따라 모든 상호 연결에 암호화 및 변조 방지 요구사항이 추가됨에 따라, 표준 실적에 보안 하드웨어를 통합할 수 있는 공급업체가 차별화될 것입니다. 중기적으로는 6G 항공전자 장비의 사양이 수송기 및 급유기 기단에 도입됨에 따라, 항공우주 및 방위 커넥터 시장에서 장기적인 교체 수요가 지속될 것으로 보입니다.

방위 플랫폼의 전동화가 고출력 커넥터 채택을 가속화하고 있습니다.

회전익 항공기, 무인 전투 차량, 해군 플랫폼 분야에서 진행 중인 하이브리드 및 완전 전기 추진 기술 개발은 열 과열 현상 없이 고전압·고전류 수준을 처리할 수 있는 고출력 상호 연결 장치에 대한 꾸준한 수요를 창출하고 있습니다. 이러한 커넥터는 고밀도로 배치된 항공전자 장비 베이 내에서 전자기 호환성(EMC)도 확보해야 합니다. 유럽 및 북미의 시스템 통합사업자들은 이미 2차 비행 제어 액추에이터를 유압 시스템에서 전기 시스템으로 전환하고 있으며, FLRAA 등의 프로그램에서는 전기 구동 시스템이 기본 아키텍처로 채택되어 있습니다. 조달 주기가 수십 년에 달하기 때문에 연속되는 생산 로트에 동일한 인증 완료 커넥터가 필요해짐에 따라 누적 수요가 쌓이면서 항공우주 및 방위 커넥터 시장의 장기적인 수요를 강화하고 있습니다.

스위스커 및 마모 부식으로 인한 고장이 신뢰성을 저해

무연 솔더 규제로 인해, 길이가 최대 10mm에 달하는 전도성 위스커가 발생할 가능성이 있는 고주석 함유 표면 처리가 채택되었습니다. 이로 인해 밀폐성이 높은 MIL-DTL-38999 쉘 내부에서 인접한 접점이 단락될 우려가 있습니다. 헬리콥터나 전투기 환경에서는 플리팅 부식이 가속화되어, 결합면이나 전기적 전도성이 저하됩니다. 정비 기지에서는 교체율 상승과 항공기 가동 중단 시간 연장이 보고되고 있어, 이는 즉시 운용 준비 지표에 부담을 주고 있습니다. 새로운 니켈-인 도금 및 금-코발트 도금에 대한 기대가 높지만, 방위 규격에 부합하기까지 3년 이상 소요될 수 있어 실전 배치가 지연될 우려가 있습니다. 따라서 항공우주 및 방위 커넥터 시장에서는 대체 도금 기술이 성숙해질 때까지 품질 비용 상승에 직면해 있습니다.

부문별 분석

2025년에는 전기 부문이 29.40%로 가장 큰 점유율을 차지했습니다. 항공우주 및 방위 분야의 전기 커넥터는 특히 군용기나 해군 시스템에서 고출력 전기 아키텍처로의 전환과 밀접한 관련이 있습니다. F-35 라이트닝 II나 B-21 레이더와 같은 플랫폼에서는 전기 기계식 액추에이터, 첨단 레이더 시스템, 탑재형 처리 장치 등 전기 구동 방식의 하위 시스템에 대한 의존도가 높아지고 있습니다. 이러한 플랫폼은 270 VDC 및 새롭게 등장한 540 VDC 아키텍처에서 작동하며, 기존의 유압 시스템을 대체하여 효율성과 생존성을 향상시키고 있습니다. 광섬유 커넥터는 전자기 간섭에 대한 내성과 구리선의 한계를 뛰어넘는 데이터 버스 속도 향상에 힘입어, 2031년까지 5.55%라는 가장 높은 연평균 성장률(CAGR)을 기록하며 성장할 것으로 전망됩니다. 플랫폼이 센서 융합, 보안 네트워크, 실시간 비디오 스트림을 통합함에 따라 기존 배선에 부담이 가중될 것이며, 이러한 우위는 지속될 것입니다.

기존의 구리 기반 솔루션은 저속 텔레메트리나 안전상 중요한 제어에는 여전히 적합하며, 특히 회전익기의 경우 정비 담당자들이 익숙한 기술이 조달을 뒷받침하고 있습니다. RF/마이크로파 제품군은 정밀한 위상 정합 공차를 통해 위상 배열 레이더에 대응하며, 한편 고출력/HVDC 유닛은 800볼트의 전기 추진 버스 요구 사항을 충족합니다. 금속 매트릭스 복합재 접점과 첨단 유전체 인서트를 결합한 공급업체는 경량화와 높은 전류 밀도를 실현하여 노후화된 기체의 개조 및 업그레이드 시장을 선점하고 있습니다. 전반적으로, 이러한 제품 라인은 항공우주 및 방위 커넥터 시장이 요구하는 다양한 성능 요건을 충족시키고 있습니다.

원형 커넥터는 2025년에 45.46%의 시장 점유율을 차지했습니다. 이는 주로 MIL-DTL-38999의 변형에 기인한 것으로, 이러한 규격들은 고정익 항공기, 회전익 항공기, 장갑차에서 여전히 사실상의 표준 인터페이스로 자리 잡고 있습니다. 이러한 베요넷식 결합 방식과 환경 밀폐성은 염수 분무 시험 및 진동 시험에서 다른 대체 제품보다 뛰어난 성능을 발휘합니다. 그러나 위성 제조업체들이 전자 기기를 점점 더 소형 폼팩터에 집적하려고 함에 따라, 나노/마이크로 미니어처 패키지가 연평균 성장률(CAGR) 5.99%로 가장 빠르게 성장하고 있습니다. 따라서 항공우주 및 방위 커넥터 시장은 기존의 표준화와 적극적인 소형화 사이에서 균형을 맞추고 있습니다.

패널 밀도가 가장 중요하게 여겨지는 항공 전자 장비의 라인 교체 가능 유닛(LRRU)에서는 직사각형 형태의 솔루션이 주류를 이루고 있습니다. 기판 간 메자닌 커넥터는 모듈식 전자 기기를 보완하여 신속한 업그레이드 주기를 실현합니다. 적층 가공 기술을 통해 스트레인 릴리프와 방열판을 일체형으로 제작할 수 있게 되어, 부품 수를 줄일 수 있습니다. 디지털 스레드 설계가 보편화됨에 따라, 엔지니어들은 설계 단계에서 커넥터의 기류 및 EMI 성능을 모델링함으로써 항공우주 및 방위 커넥터 시장에서 후반 단계에 발생하는 재설계 비용을 최소화하고 있습니다.

지역별 분석

2025년 기준으로 아시아태평양은 시장의 31.76%를 차지했습니다. 이러한 우위는 중국, 인도, 일본 등 여러 국가에서 항공·방위 부문이 급속히 성장하고 있기 때문입니다. 한국의 KF-21이나 호주의 REDSPICE 사이버 프로그램 등의 노력에 힘입어, 보안이 강화된 광 링크에 대한 수요가 증가하고 있습니다. 인도의 ‘메이크 인 인디아’ 이니셔티브는 현지 생산을 추진하고 있지만, 뿌리 깊은 기술 격차로 인해 유럽 및 미국공급업체로부터의 수입 의존이 계속되고 있습니다. 또한, 특히 아세안 오프셋을 통한 지역 협력을 통해 외국 설계 제품의 현지 조립이 촉진되고 있습니다. 이 전략은 듀얼 소싱 관행을 정착시킬 뿐만 아니라, 항공우주 및 방위 커넥터 시장공급망을 안정시키는 데에도 기여할 것입니다.

북미는 성숙한 산업 기반, 유력한 주요 방위 기업, 그리고 상업 생산의 급증에 힘입어 연평균 성장률(CAGR) 5.35%를 나타낼 전망입니다. 이 지역의 항공우주 및 방위 커넥터 시장은 KC-46A, B-21, CH-53K와 같은 프로그램의 생산 확대에 힘입어 성장하고 있으며, 각 프로그램에는 수백 개의 인증 부품 번호가 포함되어 있습니다. 미국이 CMMC를 시행하는 가운데, 국내 공급업체들은 조기에 인증을 취득하여 조달 리드타임을 대폭 단축하고 있습니다. 캐나다는 정밀 기계 가공과 하네스 조립에 강점을 가지고 있는 반면, 멕시코의 마키라도라(수출가공구)에서는 성형 인서트와 접점 하위 어셈블리가 제조되어 USMCA(미국·멕시코·캐나다 협정) 경로를 통해 미국으로 원활하게 공급되고 있습니다. 이러한 국경을 초월한 협력은 엄격한 사이버 규정 준수를 유지하면서 회복탄력성을 강화하고 있습니다.

유럽에서는 NATO의 목표에 따라 조달이 증가하고 있으며, 독일이 주도하는 1,000억 유로(1,178억 9,000만 달러) 규모의 ‘존더페르모겐(Sondervermogen)’ 자금이 고가 항공기 및 방공 포대 조달에 사용되고 있습니다. 프랑스, 이탈리아, 스웨덴은 유럽의 밸류체인을 규정하는 차세대 전투기 파트너십을 추진하고 있습니다. REACH 및 PFAS 규제로 인해 대체 엘라스토머 및 도금재의 도입이 확대되면서 설계 변경이 불가피하게 되었으며, 이로 인해 커넥터의 납기가 일시적으로 지연되고 있습니다. 그러나 대체 소재가 EN-9100 인증을 획득하면, 유럽의 시스템 통합사업자들은 납기 관리의 주도권을 되찾을 것입니다. 동유럽 국가들의 에이브럼스 전차 및 HIMARS 부대 구매는 미국과 EU 간의 대서양 횡단 협력을 촉진하고, 공급 안정성을 확보하기 위해 양 대륙에 연결 장치 생산을 분산시키고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the aerospace and defense connectors market is expected to grow from USD 4.03 billion in 2025 to USD 4.33 billion in 2026 and to reach USD 5.55 billion by 2031, at a 5.13% CAGR over 2026-2031.

This report is Segmented by Product Type (Electrical, Fiber-Optic, RF/Microwave, Hybrid, and High-Power), Connector Shape (Circular, Rectangular, Board-To-Board, and Nano/Micro-Miniature), Platform (Airborne, Land Systems, and More), End User (OEM and Aftermarket), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Aerospace and Defense Connectors Market Trends and Insights

6G-Ready High-Bandwidth Avionics Links Drive Next-Generation Connectivity

The transition to 6G avionics necessitates connector specifications that cater to D-band millimeter-wave frequencies, requiring ultra-low insertion loss and phase stability. Militaries now request contactless architectures to serve phased-array radars and electronic-warfare payloads that cannot tolerate signal degradation. Multi-domain operations increase real-time data-fusion loads, boosting demand for high-density optical backbones in the aerospace and defense connectors market. Early adoption began in the US, and several European programs, and Asian primes followed as next-generation fighter development accelerated. CMMC 2.0 cybersecurity mandates add encryption and tamper-evident requirements to every interconnect, differentiating suppliers able to embed security hardware in standard footprints. Over the medium term, 6G avionics specifications will permeate transport and tanker fleets, sustaining long-tail replacement demand within the aerospace and defense connectors market.

Defense Platform Electrification Accelerates High-Power Connector Adoption

Hybrid and fully electric propulsion initiatives across rotorcraft, unmanned combat vehicles, and naval platforms create a steady pull for high-power interconnects that handle elevated voltage and current levels without thermal runaway. These connectors must also safeguard electromagnetic compatibility inside densely packed avionics bays. European and North American integrators have already migrated secondary flight-control actuators from hydraulic to electric systems, and programs such as FLRAA embed electric drive systems as the baseline architecture. As acquisition cycles span decades, cumulative demand builds as successive production lots require identical qualified connectors, reinforcing long-run volume in the aerospace and defense connectors market.

Tin-Whisker and Fretting Corrosion Failures Constrain Reliability

Lead-free solder regulations led to tin-rich surface finishes that can spawn conductive whiskers up to 10 millimeters in length, shorting neighboring contacts in tight MIL-DTL-38999 shells. Helicopter and fighter environments magnify fretting corrosion, degrading mating surfaces and electrical continuity. Maintenance depots report higher replacement rates and extended aircraft downtime, placing immediate pressure on readiness metrics. Novel nickel-phosphorus and gold-cobalt platings show promise, yet defense qualification can take over three years, delaying field availability. The aerospace and defense connectors market, therefore, contends with elevated quality costs until alternative finishes mature.

Other drivers and restraints analyzed in the detailed report include:

- Cybersecurity-by-Design Mandates Reshape Connector Architecture

- Satellite Constellation Growth Fuels Nano-Connector Innovation

- EU Fluoropolymer Restrictions Disrupt Sealing Solutions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The electrical segment held the largest share in 2025, at 29.40%. Electrical connectors in aerospace and defense are closely linked to the shift toward high-power electrical architectures, particularly in military aircraft and naval systems. Platforms such as the F-35 Lightning II and B-21 Raider increasingly rely on electrically driven subsystems, including electromechanical actuators, advanced radar systems, and onboard processing units. These platforms operate on 270 VDC and emerging 540 VDC architectures, replacing traditional hydraulic systems to enhance efficiency and survivability. Fiber-optic connectors will grow at the fastest CAGR of 5.55% through 2031, driven by their immunity to electromagnetic interference and the rising data-bus speeds that exceed copper's limits. This leadership endures as platforms integrate sensor fusion, secure networking, and real-time video streams that strain legacy cabling.

Legacy copper solutions still suit low-rate telemetry and safety-critical controls, particularly in rotorcraft, where maintenance familiarity underpins procurement. RF/microwave families support phased-array radars due to precise phase-matching tolerances, while high-power/HVDC units satisfy 800-volt e-propulsion buses. Suppliers that pair metal-matrix composite contacts with advanced dielectric inserts achieve lower weight and higher current density, capturing retrofit upgrades on aging fleets. Altogether, these product lines underpin the diverse performance envelope demanded by the aerospace and defense connectors market.

Circular connectors secured a 45.46% share in 2025, primarily driven by MIL-DTL-38999 variants, which remain the de facto interface across fixed-wing, rotorcraft, and armored vehicles. Their bayonet coupling and environmental sealing outperform alternatives during salt-spray and vibration trials. However, nano/micro-miniature packages are growing fastest, with a 5.99% CAGR, as satellite builders squeeze electronics into increasingly smaller form factors. Therefore, the aerospace and defense connectors market balances legacy standardization with aggressive miniaturization.

Rectangular solutions dominate avionics line-replaceable units, where panel density is a paramount consideration. Board-to-board mezzanine connectors complement modular electronics, facilitating rapid upgrade cycles. Additive manufacturing enables the creation of one-piece shells that integrate strain relief and heat sinks, thereby reducing the parts count. As digital-thread design proliferates, engineers model connector airflow and EMI performance upfront, minimizing late-stage redesign costs inside the aerospace and defense connectors market.

Geography Analysis

Asia-Pacific accounted for 31.76% of the market in 2025. This dominance can be attributed to the rapid growth of the aviation and defense sectors in nations such as China, India, and Japan. Initiatives such as South Korea's KF-21 and Australia's REDSPICE cyber program have heightened demand for secure optical links. While India's Make in India initiative promotes local production, persistent technology gaps continue to drive reliance on imports from Western suppliers. Moreover, regional collaborations, particularly through ASEAN offsets, facilitate the local assembly of foreign designs. This strategy not only embeds dual-sourcing practices but also stabilizes the supply chain in the aerospace and defense connectors market.

North America, buoyed by its mature industrial base, prominent defense primes, and a surge in commercial output, is set to grow at a 5.35% CAGR. The region's aerospace and defense connectors market is reaping benefits from the ramp-ups of programs like the KC-46A, B-21, and CH-53K, each integrating hundreds of qualified part numbers. With the US enforcing CMMC, domestic suppliers gain early certifications, slashing procurement lead times. Canada excels in precision machining and harness assembly, while Mexico's maquiladoras craft molded inserts and contact sub-assemblies, seamlessly flowing north through USMCA lanes. These cross-border collaborations bolster resilience, all while upholding stringent cyber compliance.

Europe increases procurement in line with NATO targets, led by Germany's EUR 100 billion (USD 117.89 billion) Sondervermogen funding for high-value aircraft and air-defense batteries. France, Italy, and Sweden are pursuing next-generation fighter partnerships that stipulate European supply chains. REACH and PFAS rules are driving the adoption of alternative elastomers and platings, forcing redesigns that temporarily slow connector deliveries. However, once replacement materials obtain EN-9100 approval, European integrators will regain schedule traction. The Eastern European states' purchase of Abrams and HIMARS units spurs US-EU transatlantic collaboration, distributing connector production across both continents to ensure security of supply.

- TE Connectivity plc

- Amphenol Corporation

- ITT Inc.

- Smiths Interconnect Group Limited

- Radiall SA

- Fischer Connectors SA

- Rosenberger Hochfrequenztechnik GmbH & Co. KG

- LEMO SA

- Glenair, Inc.

- ODU GmbH & Co. KG

- Molex, LLC (Koch, Inc.)

- Staubli International AG

- C&K Components LLC

- Harwin Plc

- Cinch Connectivity Solutions, Inc.

- Samtec, Inc.

- Caton Connector Corporation

- Eaton Corporation plc

- Phase 3 Connectors Ltd

- Winchester Interconnect

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing orders for 6G-ready high-bandwidth avionics links

- 4.2.2 Electrification of defense platforms (e-Propulsion, e-APU)

- 4.2.3 Mandated cybersecurity-by-design for mission-critical connectors

- 4.2.4 Lower-orbit satellite constellations driving nano-connector demand

- 4.2.5 Additive-manufactured metal housings slash lead-times

- 4.2.6 Rapid prototyping hubs inside major OEMs (digital thread integration)

- 4.3 Market Restraints

- 4.3.1 Chronic tin-whisker and fretting corrosion failures in vibration zones

- 4.3.2 EU "PFHxS" ban limits fluoropolymer sealants supply

- 4.3.3 Skilled crimp-operator shortage at MRO depots

- 4.3.4 Rising IP-theft risk deters open reference-design sharing

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Electrical (Signal and Power)

- 5.1.2 Fiber-Optic

- 5.1.3 RF/Microwave

- 5.1.4 Hybrid

- 5.1.5 High-Power

- 5.2 By Connector Shape

- 5.2.1 Circular

- 5.2.2 Rectangular

- 5.2.3 Board-to-Board (BTB)

- 5.2.4 Nano/Micro-Miniature

- 5.3 By Platform

- 5.3.1 Airborne

- 5.3.2 Land Systems

- 5.3.3 Naval and Sub-Surface

- 5.3.4 Space

- 5.4 By End User

- 5.4.1 OEM

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Israel

- 5.5.5.1.4 Rest of the Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 TE Connectivity plc

- 6.4.2 Amphenol Corporation

- 6.4.3 ITT Inc.

- 6.4.4 Smiths Interconnect Group Limited

- 6.4.5 Radiall SA

- 6.4.6 Fischer Connectors SA

- 6.4.7 Rosenberger Hochfrequenztechnik GmbH & Co. KG

- 6.4.8 LEMO SA

- 6.4.9 Glenair, Inc.

- 6.4.10 ODU GmbH & Co. KG

- 6.4.11 Molex, LLC (Koch, Inc.)

- 6.4.12 Staubli International AG

- 6.4.13 C&K Components LLC

- 6.4.14 Harwin Plc

- 6.4.15 Cinch Connectivity Solutions, Inc.

- 6.4.16 Samtec, Inc.

- 6.4.17 Caton Connector Corporation

- 6.4.18 Eaton Corporation plc

- 6.4.19 Phase 3 Connectors Ltd

- 6.4.20 Winchester Interconnect