|

시장보고서

상품코드

2063252

터빈 드립 오일 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Turbine Drip Oil - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

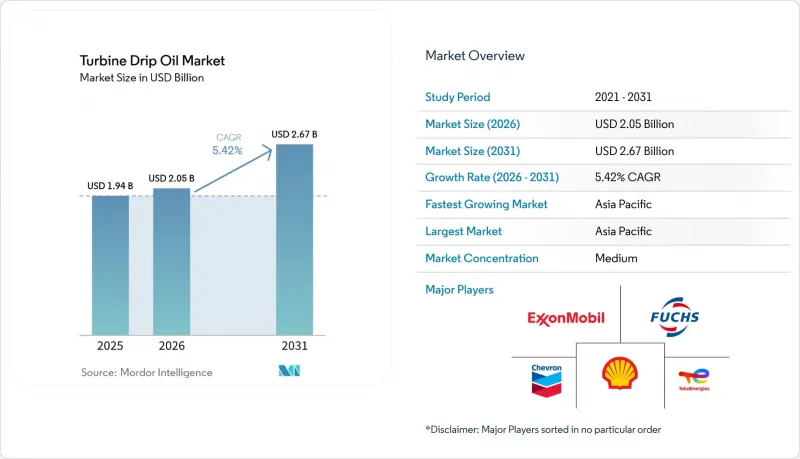

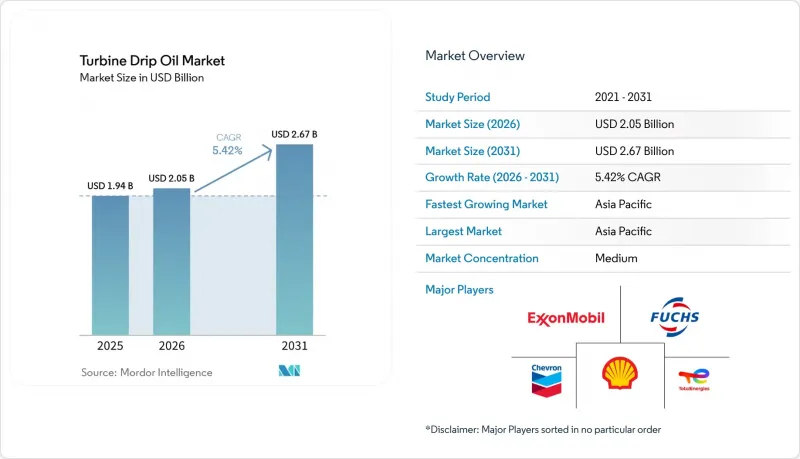

Mordor Intelligence에 의하면, 터빈 드립 오일 시장 규모는 2025년에 19억 4,000만 달러로 평가되었습니다. 2026년에 20억 5,000만 달러에 달하고, 2031년까지 26억 7,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR은 5.42%를 나타낼 전망입니다.

본 보고서는 유형별(광물계, 합성계, 바이오계), 점도 등급별(저점도, 중점도, 기타), 용도별(증기 터빈, 가스 터빈, 기타), 최종 사용자별(발전 사업자, 제조업, 기타), 지역별(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 터빈 드립 오일 시장 동향 및 인사이트

화력·수력 발전의 성장

H급 복합 사이클 가스 터빈의 리드타임은 현재 2030년까지 연장되었으며, 이는 열효율 약 60%에 달하는 고효율 가스 발전 설비로 노후화된 석탄 화력 설비를 대체하려는 전 세계적인 추세를 반영한 것입니다. 폴란드와 도미니카 공화국에서 진행되는 신규 건설 프로젝트에서는 각각 1만 6,000시간의 교환 주기에 대응하는 프리미엄 ISO VG 46 드립 오일이 사용됩니다. 수력 발전 설비 확충도 꾸준히 진행되고 있습니다. 2024년에 중국에서만 14.4GW가 도입되면서, 내수성을 갖춘 비용 효율적인 ISO VG 46 광물유에 대한 수요가 지속되고 있습니다.

산업용 터빈 및 회전 장비에 대한 수요

액화 플랜트, 중류 압축기 스테이션 및 정유시설의 가스 압축기 트레인에는 점도 지수 140 이상의 급속 탈기성 오일(ASTM D3427 기준 5분 이내)이 필요합니다. 알래스카 LNG의 80만 마력 냉동 압축기와 벤처·세계의 프락민즈 2단계 확장 프로젝트를 합치면, 초기 터빈 오일 충전량은 수십만 리터에 달할 전망입니다. Sasquene Energy와 Energy Transfer에서 진행된 유사한 현대화 프로그램은 북미 가스망에서 합성 ISO VG 32의 소비량이 증가하고 있음을 보여줍니다.

환경·안전 규제

EPA의 선박 일반 허가(Vessel General Permit)에 따르면, 선미관용 윤활유는 90% 이상의 생분해성을 갖춰야 하며, 공급업체들은 기존 그룹 II 오일보다 최대 2배의 비용이 드는 에스테르계 및 PAG계 화학제품으로 전환해야 하는 상황에 직면해 있습니다. ECHA의 CLP 규정에 따르면, 특정 미처리 베이스 오일이 발암성 물질로 분류되어 있어, 유럽에서는 수소 처리 및 합성 대체품으로의 전환이 가속화되고 있습니다. 중국의 GB 11120-2011 규격에서는 현재 점도 지수 90 이상 및 인화점 200°C 이상을 요구하고 있으며, 저품질 광물유는 단계적으로 폐지되고 있습니다.

부문별 분석

2025년, 광물유는 합성 대체품에 비해 3분의 1에서 5분의 1 수준이라는 유리한 가격 책정을 바탕으로 터빈 점적유 시장에서 67.8%의 점유율을 유지했습니다. 이러한 배합은 터빈 오일 안정성 시험에서 2,000-4,000시간의 수명을 달성했으며, 수력 터빈이나 저압 증기 설비에는 충분한 성능을 발휘합니다. 합성유는 비용이 높고, 교환 주기가 6배 더 길며, 뛰어난 유화 분산성을 갖추고 있어 복합 사이클 가스터빈의 사양 요건을 충족합니다. 바이오 오일은 EPA 및 EU의 친환경 라벨 규정의 혜택을 받아 연평균 성장률(CAGR) 9.5%로 성장하고 있습니다. 트리메틸올프로판 에스테르에 대한 조사 결과, 현재는 점도 지수가 160에 육박하고 유동점이 -40°C 이하인 제품이 개발되었습니다.

중점도 등급(ISO VG 32-68)은 2025년 총량의 49.1%를 차지했지만, 각 OEM 업체들이 에너지 효율 향상을 추구하는 가운데, 저점도 등급(ISO VG 15-32)은 연평균 성장률(CAGR) 7.4%를 나타낼 전망입니다. 베이커 휴즈의 조사에 따르면, ISO VG 15-22 등급의 오일은 ISO VG 32 등급에 비해 기계적 손실을 5-15% 줄일 수 있으며, 천연가스 가격이 4달러/MMBtu를 초과할 경우 플랜트 차원에서 0.3-0.5%의 연료 절감 효과를 가져옵니다.

고점도 오일(ISO VG 100-150)은 선박용 추진 터빈이나 대형 기어박스 등 특수 용도로 사용되며, 금속 간의 접촉을 방지하기 위해 더 두꺼운 유막이 필요합니다. Baker Hughes사와 Eni사의 조사에 따르면, VG 15-22 등급의 배합유는 ISO VG 32에 비해 점도 손실을 5-15% 줄여주며, 복합 사이클 발전소에서 0.3-0.5%의 연료 절감 효과를 가져온다는 사실이 밝혀졌습니다. 가스 터빈에는 점도 지수가 140 이상인 저점도 합성유가 선호되지만, 풍력 터빈의 경우 그리스 사용량을 줄이기 위해 ISO VG 130 오일로 전환하는 추세가 확산되고 있습니다. 고성능 첨가제와 산화 안정성 시험을 통해 열 스트레스 조건 하에서도 성능이 보장되며, OEM 요건을 충족합니다.

지역별 분석

아시아태평양은 2025년에 매출의 45.0%를 차지했으며, 인도의 1,450억 달러 규모 인프라 구축 추진과 중국의 수력 및 풍력 발전 도입 확대에 힘입어 2031년까지 연평균 성장률(CAGR) 6.3%를 나타낼 것으로 전망됩니다. 국내 생산 능력 확충에 더해, 인도 석유공사(Indian Oil Corporation)와 엑슨모빌 인디아(ExxonMobil India)의 현지 블렌딩 사업 확대가 맞물리면서, 그룹 II 및 그룹 III 제품의 지역 자급률이 강화되고 있습니다.

북미와 유럽에서는 엄격한 환경 규제와 탈탄소화 의무화로 인해 저VOC 합성유 및 바이오 오일에 대한 수요가 증가하고 있지만, 석탄 화력 발전소의 폐쇄에 따라 수요량은 감소하고 있습니다. LNG 중류 부문에 대한 투자와 복합 사이클 발전소의 재가동으로 인해, 증기 터빈용 오일 수요 감소분이 일부 상쇄되고 있습니다.

만안 지역의 석유화학 단지에선 고온용 합성 윤활유가 요구되고 있는 반면, 브라질에서는 수력 발전이 주류를 이루고 있어 ISO VG 46 광물유에 대한 수요가 유지되고 있습니다. 아르헨티나의 바카 무에르타 파이프라인 계획과 이집트의 가스 터빈 설비 증설은 사막 기후에 적합한 윤활유 제품군을 보유한 공급업체들에게 추가적인 고수익 기회를 제공합니다. 사우디아라비아와 아랍에미리트(UAE)에서는 고온 환경에서 사용이 가능하고 유지보수를 최소화할 수 있는 고품질 합성 윤활유가 필요한 복합 사이클 발전소의 가동이 시작되었습니다. 남아프리카공화국에서는 재생에너지 도입이 확대되고 있음에도 불구하고, 노후화된 석탄 화력 발전소가 광물유 수요를 지탱하고 있습니다. 브라질의 수력 및 풍력 발전 부문은 ISO VG 46 오일과 ISO VG 320 그리스에 대한 수요를 주도하고 있습니다. 아르헨티나의 바카 무에르타 셰일 유전은 합성유 사용을 촉진하고 있지만, 이집트와 나이지리아에서는 정치적·경제적 문제로 인해 수요 증가가 제한되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the turbine drip oil market size is projected to be USD 1.94 billion in 2025, USD 2.05 billion in 2026, and reach USD 2.67 billion by 2031, growing at a CAGR of 5.42% from 2026 to 2031.

This report is Segmented by Type (Mineral-Based, Synthetic, and Bio-Based), Viscosity Grade (Low Viscosity, Medium Viscosity, Others), Application (Steam Turbines, Gas Turbines, Others), End-User (Power Generation Utilities, Manufacturing, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Turbine Drip Oil Market Trends and Insights

Growth of Thermal & Hydro-Power Generation

Lead times for H-class combined-cycle gas turbines now extend to 2030, reflecting a worldwide push to replace aging coal assets with high-efficiency gas units that reach about 60% thermal efficiency. New builds in Poland and the Dominican Republic will each consume premium ISO VG 46 drip oils designed for 16,000-hour drain intervals. Hydropower additions remain robust. China alone brought on 14.4 GW in 2024, maintaining demand for cost-effective ISO VG 46 mineral oils resistant to water ingress.

Demand from Industrial Turbines & Rotating Equipment

Liquefaction plants, midstream compressor stations and refinery gas-compressor trains require rapid air-release oils (≤5 min per ASTM D3427) with viscosity indices above 140. Alaska LNG's 800,000 HP refrigeration compressors and Venture Global's Plaquemines Phase 2 expansion together translate into several hundred thousand liters of initial turbine oil fills. Similar modernization programs at SaskEnergy and Energy Transfer demonstrate the upswing in synthetic ISO VG 32 consumption within North America's gas grid.

Environmental & Safety Regulations

The EPA Vessel General Permit obliges stern-tube lubricants to exhibit > 90% biodegradability, pushing suppliers toward ester and PAG chemistries that cost up to twice conventional Group II oils. ECHA's CLP rules classify certain untreated base stocks as carcinogenic, accelerating the shift to hydrotreated and synthetic alternatives in Europe. China's GB 11120-2011 standard now requires viscosity indices ≥90 and flash points > 200 °C, phasing out low-quality mineral oils.

Other drivers and restraints analyzed in the detailed report include:

- Industrial Expansion in Emerging Economies

- Predictive-Maintenance-Driven Auto-Lubrication Adoption

- Shift Toward Renewable Energy Sources

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mineral oils retained 67.8% share of the turbine drip oil market in 2025 on the back of favorable pricing, one-third to one-fifth of synthetic alternatives. These formulations deliver Turbine Oil Stability Test life of 2,000-4,000 h, adequate for hydro turbines and low-pressure steam units. Synthetics, while costlier, offer six-times-longer drain intervals and superior demulsibility, winning specifications in combined-cycle gas turbines. Bio-based oils, benefiting from EPA and EU ecolabel mandates, are advancing at 9.5% CAGR; trimethylolpropane ester research now yields viscosity indices near 160 and pour points below -40 °C.

Medium grades (ISO VG 32-68) still represent 49.1% of 2025 volume, but low-viscosity grades (ISO VG 15-32) are set to expand at 7.4% CAGR as OEMs chase energy-efficiency gains. Baker Hughes studies show that ISO VG 15-22 oils can cut mechanical losses by 5-15% versus ISO VG 32, translating to 0.3-0.5% plant-level fuel savings when natural-gas prices exceed USD 4 / MMBtu.

High-viscosity oils (ISO VG 100-150) are used in specialized applications like marine propulsion turbines and heavy-duty gearboxes, requiring thicker films to prevent metal-to-metal contact. Research by Baker Hughes and Eni showed VG 15-22 formulations reduce viscous losses by 5%-15% versus ISO VG 32, saving 0.3%-0.5% fuel in combined-cycle plants. Low-viscosity synthetics with viscosity indices above 140 are preferred for gas turbines, while wind turbines are shifting to ISO VG 130 oils to reduce grease use. Advanced additives and oxidation-stability testing ensure performance under thermal stress, meeting OEM requirements.

Geography Analysis

Asia-Pacific commanded 45.0% revenue in 2025 and is projected to expand at 6.3% CAGR through 2031, supported by India's USD 145 billion infrastructure push and China's hydropower and wind roll-outs. Domestic capacity additions, combined with localized blending expansions by Indian Oil Corporation and ExxonMobil India, reinforce regional self-sufficiency in Group II and Group III output.

In North America and Europe, tight environmental regulations and decarbonization mandates stimulate demand for low-VOC synthetics and bio-based oils, but shrink volumes as coal fleets retire. LNG midstream investments and repowering of combined-cycle plants partially offset lost steam-turbine volumes.

Gulf petrochemical complexes require high-temperature synthetics, while Brazil's hydropower dominance sustains ISO VG 46 mineral demand. Argentina's Vaca Muerta pipeline projects and Egypt's gas-turbine additions present incremental, high-margin opportunities for suppliers with desert-climate lubricant portfolios. Saudi Arabia and the UAE are commissioning combined-cycle plants requiring premium synthetics for high temperatures and minimal maintenance. South Africa's aging coal fleet sustains mineral oil demand despite renewable energy efforts. Brazil's hydropower and wind sectors drive demand for ISO VG 46 oils and ISO VG 320 greases. Argentina's Vaca Muerta shale boosts synthetic oil use, while Egypt and Nigeria see incremental demand constrained by political and economic challenges.

- ExxonMobil Corporation

- Chevron Corporation

- Royal Dutch Shell plc

- TotalEnergies SE

- Fuchs Petrolub SE

- Phillips 66 (Kendall)

- Suncor (Petro-Canada Lubricants)

- Indian Oil Corporation Ltd.

- Bharat Petroleum Corp. Ltd.

- Amsoil Inc.

- Idemitsu Kosan Co.

- Valvoline Inc.

- Sinopec Lubricants

- ENEOS Holdings

- PetroChina Lubricants

- Gazpromneft-SM

- Caltex Australia

- Petronas Lubricants

- Quaker Houghton

- BP Castrol

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth of thermal & hydro-power generation

- 4.2.2 Demand from industrial turbines & rotating equipment

- 4.2.3 Industrial expansion in emerging economies

- 4.2.4 Predictive-maintenance-driven auto-lubrication adoption

- 4.2.5 OEM shift to premium low-VOC drip oils

- 4.3 Market Restraints

- 4.3.1 Environmental & safety regulations

- 4.3.2 Shift toward renewable energy sources

- 4.3.3 Base-oil price volatility & supply swings

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Mineral-based

- 5.1.2 Synthetic

- 5.1.3 Bio-based

- 5.2 By Viscosity Grade

- 5.2.1 Low Viscosity

- 5.2.2 Medium Viscosity

- 5.2.3 High Viscosity

- 5.3 By Application

- 5.3.1 Steam Turbines

- 5.3.2 Gas Turbines

- 5.3.3 Wind Turbines

- 5.3.4 Hydro Turbines

- 5.4 By End-user

- 5.4.1 Power Generation Utilities

- 5.4.2 Oil and Gas

- 5.4.3 Manufacturing

- 5.4.4 Marine and Transportation

- 5.4.5 Others (Mining, Pulp and Paper)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 NORDIC Countries

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN Countries

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 ExxonMobil Corporation

- 6.4.2 Chevron Corporation

- 6.4.3 Royal Dutch Shell plc

- 6.4.4 TotalEnergies SE

- 6.4.5 Fuchs Petrolub SE

- 6.4.6 Phillips 66 (Kendall)

- 6.4.7 Suncor (Petro-Canada Lubricants)

- 6.4.8 Indian Oil Corporation Ltd.

- 6.4.9 Bharat Petroleum Corp. Ltd.

- 6.4.10 Amsoil Inc.

- 6.4.11 Idemitsu Kosan Co.

- 6.4.12 Valvoline Inc.

- 6.4.13 Sinopec Lubricants

- 6.4.14 ENEOS Holdings

- 6.4.15 PetroChina Lubricants

- 6.4.16 Gazpromneft-SM

- 6.4.17 Caltex Australia

- 6.4.18 Petronas Lubricants

- 6.4.19 Quaker Houghton

- 6.4.20 BP Castrol

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

- 7.2 Emerging OEM specs & turbine upgrades

- 7.3 Bio-based & sustainable lubricant R&D

- 7.4 Digital supply-chain & service bundles